Reports

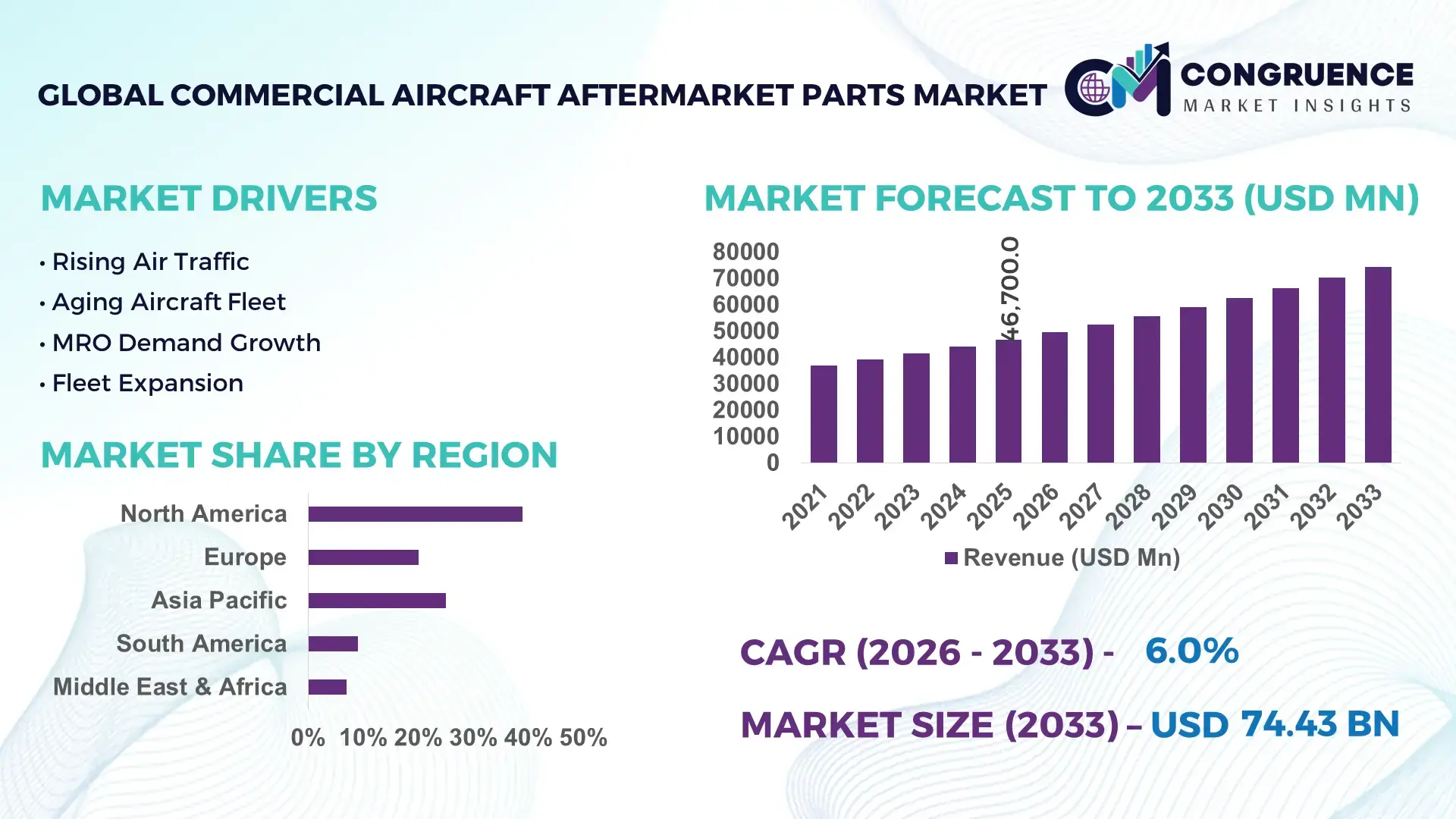

The Global Commercial Aircraft Aftermarket Parts Market was valued at USD 46700 Million in 2025 and is anticipated to reach a value of USD 74432.7 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Growth is being driven by rising global aircraft utilization rates, expanding maintenance cycles for aging fleets, increased deployment of predictive maintenance systems, and accelerated replacement demand for engine, avionics, and structural components across commercial aviation networks.

The United States remains the dominant market, accounting for approximately 34% of global aftermarket activity, supported by the world's largest commercial fleet, over 5,000 active maintenance facilities, and sustained investments in digital MRO technologies. Compared with China, where fleet expansion and domestic MRO capacity continue to scale rapidly, the U.S. maintains stronger parts distribution infrastructure and higher advanced analytics adoption exceeding 60% among major operators. Ongoing fleet modernization initiatives and supply-chain realignment following geopolitical disruptions in aerospace manufacturing further reinforce market leadership.

For industry participants, strengthening inventory localization, repair capabilities, and digital parts tracking systems remains critical to securing long-term competitive positioning.

Market Size & Growth: USD 46,700 million in 2025 reaching USD 74,432.7 million by 2033, supported by predictive maintenance adoption and fleet life-extension strategies across global airlines.

Top Growth Drivers: Aircraft utilization rates up 12%, digital MRO deployment up 18%, and engine overhaul demand increasing 15% globally.

Short-Term Forecast: By 2028, maintenance turnaround times decline 10% while parts availability efficiency improves 14% through advanced inventory systems.

Emerging Technologies: AI-driven diagnostics, digital twins, and additive manufacturing reduce inspection time by up to 25% and lower component lead times by 20%.

Regional Leaders: North America exceeds USD 24 billion, Asia-Pacific surpasses USD 19 billion, and Europe approaches USD 16 billion, driven by fleet modernization and MRO expansion.

Consumer/End-User Trends: More than 65% of major carriers prioritize condition-based maintenance programs to optimize operational reliability.

Pilot/Case Example: In 2026, a large airline maintenance digitization program improved parts traceability by 30% and reduced unscheduled downtime by 12%.

Competitive Landscape: Leading suppliers collectively control nearly 40% market share, with major participants including Boeing, Airbus, GE Aerospace, Safran, and RTX.

Regulatory & ESG Impact: Sustainable maintenance initiatives reduce material waste by approximately 15% while supporting stricter aviation compliance standards.

Investment & Funding: More than USD 8 billion is being directed toward MRO facilities, digital platforms, and regional expansion projects amid supply-chain diversification.

Innovation & Future Outlook: High-growth adoption of smart inventory platforms and certified 3D-printed components is accelerating next-generation aftermarket service models.

Commercial Aircraft Aftermarket Parts Market demand is concentrated in engine components, avionics systems, landing gear assemblies, and high-cycle structural parts. Advanced predictive analytics, digital inventory management, and certified additive manufacturing are improving maintenance planning and reducing component lead times. Nearly 30% of major operators have expanded data-driven maintenance workflows, while ongoing supply-chain localization and airworthiness compliance requirements are reshaping procurement strategies, setting the foundation for broader strategic market evaluation.

The Commercial Aircraft Aftermarket Parts Market has become a strategic component of aviation competitiveness as airlines prioritize fleet availability, maintenance efficiency, and lifecycle cost optimization. The industry is increasingly influenced by supply-chain restructuring, with operators reducing dependence on single-source suppliers and expanding regional parts inventories. As aircraft utilization rates remain above pre-pandemic levels across major aviation corridors, aftermarket support capabilities are becoming a critical differentiator for airlines, MRO providers, and aerospace manufacturers.

Digital transformation is reshaping maintenance operations. AI-enabled predictive maintenance platforms reduce unscheduled component removals by approximately 20% compared with traditional scheduled maintenance models while improving parts planning accuracy by nearly 15%. The United States continues to lead in digital MRO deployment and certified repair capacity, while China is rapidly expanding domestic maintenance infrastructure and component repair ecosystems. A practical example is the deployment of digital parts traceability systems that shorten inventory search times and improve maintenance turnaround performance across large commercial fleets.

Over the next two to three years, adoption of predictive analytics, additive manufacturing, and digital inventory management is expected to expand across more than 50% of large airline maintenance networks. Companies are increasing investments in localized repair facilities, strategic supplier partnerships, and advanced logistics capabilities. Organizations that secure resilient supply chains and data-driven maintenance ecosystems will achieve stronger operational control, higher asset utilization, and sustained competitive advantage.

Global aircraft utilization rates have increased by approximately 12% since major travel markets normalized operations, creating sustained demand for replacement components and repair services. More than 60% of large commercial operators now integrate predictive maintenance tools into maintenance planning, reducing unexpected equipment failures and improving fleet availability. A significant industry shift is the expansion of digital maintenance ecosystems across the United States, where airlines are investing in real-time health monitoring and inventory optimization platforms. The direct impact is higher parts consumption visibility and faster maintenance execution. In response, aftermarket suppliers are expanding repair capacity, strengthening OEM partnerships, and investing in regional distribution hubs. A notable strategic insight is that data ownership and maintenance intelligence are becoming as valuable as physical inventory in securing long-term customer contracts.

Commercial aircraft aftermarket operations continue to face supply limitations driven by material shortages, extended certification timelines, and concentrated supplier networks. Lead times for selected engine and avionics components remain 20–30% above historical averages, while some repair cycles have lengthened by more than 15%. The United Kingdom and United States aerospace supply chains continue addressing bottlenecks linked to specialized castings and precision-machined components. These constraints directly increase inventory carrying costs, delay maintenance schedules, and reduce operational flexibility for airlines and MRO providers. To mitigate exposure, companies are diversifying supplier portfolios, increasing localized inventory holdings, and securing long-term procurement agreements. A key operational insight is that inventory resilience has become a competitive requirement rather than a cost-efficiency strategy, particularly for high-turnover critical components.

Advanced digital inventory platforms and certified additive manufacturing are creating new value pools across the commercial aircraft aftermarket ecosystem. Additive manufacturing can reduce production lead times by nearly 40% for selected low-volume components, while digital inventory optimization systems improve stock accuracy by approximately 20%. China and India are expanding aviation infrastructure investments, creating opportunities for localized repair and component manufacturing capabilities. An emerging trend is the increasing certification of 3D-printed aerospace parts, enabling decentralized production closer to maintenance locations. Companies are responding through targeted R&D programs, technology partnerships, and investments in smart logistics networks. A non-obvious opportunity lies in digitized component traceability, where improved asset visibility reduces excess inventory requirements while strengthening compliance and maintenance planning efficiency.

The market faces growing execution challenges related to skilled labor availability, digital system integration, and evolving compliance requirements. More than 45% of aviation maintenance organizations report difficulty recruiting experienced technical personnel, while digital platform integration projects frequently require 15–20% longer implementation periods than initially planned. In Germany and the United States, expanding maintenance technology deployments are increasing demand for specialists capable of managing connected maintenance environments. These challenges affect deployment consistency, operational scalability, and long-term productivity improvements. Companies must invest in workforce development programs, cloud-enabled maintenance architectures, and collaborative technology partnerships to address capability gaps. A critical strategic insight is that organizations able to combine technical talent, digital infrastructure, and regulatory expertise will establish stronger competitive positioning than businesses relying solely on physical maintenance capacity expansion.

Predictive Maintenance Scaling Rapidly: Airlines are expanding predictive maintenance programs, with adoption exceeding 60% among large fleet operators and fault-detection accuracy improving by nearly 25%. Digital aircraft health monitoring systems are reducing unscheduled maintenance events by 15–20% while improving component planning efficiency. Labor shortages and pressure to maximize fleet utilization are accelerating deployment, prompting suppliers and MRO providers to expand analytics partnerships and integrated maintenance platforms.

Localized Inventory Networks Expanding: Supply-chain disruptions have encouraged operators to increase regional parts stocking levels by approximately 18%, while critical component localization initiatives have grown by over 20% in key aviation hubs. U.S. and Middle Eastern maintenance networks are restructuring distribution strategies to reduce lead-time exposure. The shift improves aircraft availability and lowers logistics delays, leading companies to establish new warehousing partnerships and digitally connected inventory ecosystems.

Certified Additive Manufacturing Adoption: Aerospace-certified additive manufacturing is reducing lead times for selected replacement parts by up to 40% and lowering low-volume production costs by nearly 15%. Demand is expanding beyond prototyping into operational maintenance applications. Regulatory progress in component certification is supporting wider deployment, while aftermarket suppliers are investing in distributed manufacturing capabilities and qualification programs to strengthen responsiveness.

Digital Traceability Becoming Standard: Parts traceability platforms now cover more than 50% of maintenance transactions among leading operators, improving compliance verification and reducing documentation processing times by around 30%. A non-obvious benefit is stronger residual asset value management through enhanced component history visibility. Companies are integrating blockchain-enabled records, automated compliance workflows, and supplier connectivity tools to strengthen operational transparency.

Engine Parts represent the leading segment within the Commercial Aircraft Aftermarket Parts Market, accounting for the largest share of maintenance expenditure due to high replacement frequency, stringent airworthiness requirements, and complex overhaul cycles. More than 40% of aftermarket spending is linked to engine-related components, reflecting their critical role in aircraft performance and operational reliability. Airlines and MRO providers continue expanding engine repair capabilities and long-term maintenance agreements to control lifecycle costs. Airframe Parts maintain strong demand due to aging fleets, while Landing Gear Parts remain strategically important because of recurring inspection and refurbishment requirements.

Avionics Components are the fastest-growing type segment, supported by increasing digital cockpit upgrades, navigation modernization, and connectivity enhancements. Avionics-related retrofit activity has increased by approximately 18% across several major airline fleets. Cabin Interior Parts are also gaining traction as carriers invest in passenger experience improvements and premium cabin upgrades. Companies are prioritizing product development, repair capacity expansion, and strategic OEM partnerships to capture higher-value component demand while balancing maintenance efficiency and operational performance.

Engine Overhaul remains the dominant application segment because engines account for the highest maintenance complexity, regulatory oversight, and lifecycle expenditure within commercial aviation operations. Major airlines allocate a substantial portion of maintenance budgets to overhaul programs, while overhaul demand has increased by nearly 14% alongside rising aircraft utilization rates. Base Maintenance continues to play a critical role for heavy inspections and structural work, whereas Line Maintenance remains essential for daily operational readiness and dispatch reliability.

Component Repair is emerging as the fastest-growing application segment as operators focus on cost optimization and faster asset recovery. Repair cycle efficiency has improved by approximately 20% through digital diagnostics and automated workflow management. Cabin Refurbishment is also expanding as airlines modernize interiors and differentiate passenger offerings. In response, MRO providers are scaling repair facilities, implementing digital maintenance systems, and expanding specialized service capabilities. Demand concentration is increasingly shifting toward applications that reduce aircraft downtime while extending component service life.

Airlines represent the leading end-user segment due to their direct responsibility for fleet reliability, maintenance planning, and operational continuity. Large commercial carriers account for the majority of aftermarket parts consumption, with fleet utilization increases driving replacement demand across engines, avionics, and structural systems. More than 65% of major carriers have expanded digital maintenance planning initiatives to improve inventory control and reduce operational disruptions. OEM Service Providers maintain a strong position through integrated support agreements and long-term maintenance programs.

MRO Providers are the fastest-growing end-user segment as airlines increasingly outsource specialized repair and overhaul activities. Outsourced maintenance activity has expanded by approximately 15%, creating opportunities for independent service providers with advanced repair capabilities. Aircraft Leasing Companies are becoming more active buyers due to stricter asset management requirements, while Cargo Operators continue increasing aftermarket spending as freight fleets age. Aviation Service Companies are strengthening ecosystem participation through logistics, technical support, and inventory management services. Companies are targeting these groups through customized service packages, partnership-driven support models, and integrated aftermarket solutions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Digital Maintenance Ecosystems Strengthen Market Leadership

North America remains the largest commercial aircraft aftermarket parts hub due to its extensive airline fleet, mature MRO infrastructure, and high concentration of aerospace suppliers. The region accounts for approximately 38% of global aftermarket activity, supported by strong deployment of predictive maintenance technologies and integrated inventory management systems. More than 60% of large commercial operators utilize advanced digital maintenance platforms to improve component availability and reduce turnaround times. Ongoing investments in engine repair facilities, parts distribution centers, and aviation data analytics continue strengthening operational efficiency. Strategic collaborations between airlines, OEMs, and independent MRO providers are accelerating the deployment of real-time maintenance planning and traceability solutions.

United States Market Outlook: The United States dominates regional demand through the world's largest commercial aviation fleet and one of the most extensive aerospace support networks. More than 5,000 aviation maintenance facilities support continuous parts replacement and overhaul activity. Investments in predictive maintenance technologies, digital twins, and advanced repair capabilities are improving fleet availability and maintenance productivity. Strong defense-industrial capabilities and a highly developed supplier ecosystem further reinforce the country's position as the primary aftermarket parts center.

Sustainability and Fleet Modernization Drive Operational Upgrades

Europe maintains a strong position in the commercial aircraft aftermarket parts market through advanced aerospace manufacturing capabilities, stringent maintenance standards, and fleet modernization programs. The region accounts for approximately 27% of global aftermarket demand, supported by extensive airline and MRO networks. Sustainable aviation initiatives are influencing maintenance practices, with digital inspection technologies reducing maintenance processing times by nearly 15%. Increasing adoption of predictive maintenance tools and automated repair workflows is improving operational efficiency across major aviation hubs. Continued investments in component repair facilities and avionics upgrade programs are strengthening long-term aftermarket competitiveness.

Germany Market Outlook: Germany serves as a key aerospace maintenance and engineering center, supported by advanced manufacturing infrastructure and a highly skilled workforce. The country has expanded investments in digital MRO operations and automated inspection systems to improve maintenance precision. Strong collaboration between airlines, engineering firms, and technology providers supports efficient component lifecycle management. Germany's position within the European aerospace supply chain provides a strategic advantage for aftermarket parts distribution and repair operations.

Fleet Expansion Creates Large-Scale Aftermarket Demand

Asia-Pacific is the fastest-expanding market due to rapid airline fleet growth, airport infrastructure development, and increasing domestic maintenance capabilities. The region represents approximately 24% of global aftermarket activity and continues gaining share through expanding aircraft utilization rates. Several countries are increasing investment in local MRO ecosystems, reducing dependence on overseas maintenance services. Digital maintenance adoption has risen by more than 20% among leading operators, supporting improved fleet reliability and component management. Infrastructure expansion, growing passenger traffic, and localized repair capabilities continue driving aftermarket demand across the region.

China Market Outlook: China is the most strategically significant market in Asia-Pacific due to its expanding commercial fleet and substantial aviation infrastructure investments. Domestic MRO capacity continues to grow alongside airport development programs and aircraft acquisition activity. Local operators are increasing adoption of predictive maintenance technologies and digital inventory systems, improving operational visibility and reducing maintenance delays. Strong government support for aviation industrial development is accelerating the expansion of repair, overhaul, and component support capabilities.

Fleet Utilization Supports Maintenance Demand Growth

South America is experiencing steady aftermarket expansion driven by increasing aircraft utilization, fleet aging, and growing demand for maintenance optimization. The region contributes approximately 6% of global aftermarket activity and is strengthening local repair capabilities to improve operational efficiency. Airlines are focusing on component repair and lifecycle extension strategies to manage maintenance costs. Investments in maintenance infrastructure and logistics capabilities are helping reduce dependency on imported repair services. Despite infrastructure limitations and supply-chain complexity, operators continue prioritizing fleet reliability and maintenance productivity improvements.

Brazil Market Outlook: Brazil leads the regional market through its established aerospace ecosystem, extensive airline operations, and technical maintenance capabilities. The country benefits from strong engineering expertise and a growing network of maintenance facilities supporting both domestic and international fleets. Increasing investment in component repair services and digital maintenance tools is enhancing operational efficiency. Brazil's aviation sector continues emphasizing localized maintenance capacity to reduce turnaround times and improve aircraft availability.

Infrastructure Investment Accelerates Aviation Transformation

The Middle East & Africa market is advancing through large-scale aviation investments, fleet modernization programs, and expanding maintenance infrastructure. The region contributes approximately 5% of global aftermarket activity while strengthening its position as an international aviation transit hub. Several operators are investing in advanced maintenance facilities capable of supporting next-generation aircraft platforms. New MRO developments and strategic aviation partnerships are improving regional service capabilities, while digital maintenance technologies are increasing operational visibility and compliance efficiency. The market continues benefiting from long-haul fleet deployment and aviation diversification strategies.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's leading aviation maintenance hub due to its strategic location, world-class airport infrastructure, and significant airline presence. Major aviation operators are investing in advanced engine overhaul, component repair, and digital maintenance capabilities. The country has expanded aviation support infrastructure to accommodate growing fleet requirements and international maintenance demand. Strong connectivity, modern logistics networks, and continuous aerospace investment reinforce its position as a critical aftermarket services center.

The competitive landscape is led by Boeing Global Services, Airbus Services, GE Aerospace, Safran, and RTX, which collectively control approximately 45% of the commercial aircraft aftermarket parts market. Competition primarily occurs between OEM-affiliated service providers and independent aftermarket specialists, while regional MRO networks compete on turnaround speed and cost efficiency. OEMs leverage proprietary technical data and integrated support contracts, whereas independent suppliers focus on repair flexibility and lower operating costs. Predictive maintenance platforms have improved maintenance planning efficiency by nearly 20%, while advanced inventory systems reduce parts fulfillment delays by approximately 15%. Companies are strengthening positions through repair facility expansion, digital maintenance partnerships, localized inventory networks, and vertical integration strategies. The current competitive shift centers on digital traceability, certified additive manufacturing, and supply-chain control. Certification requirements, technical expertise, and regulatory compliance create substantial entry barriers. Winning requires superior maintenance intelligence, resilient component availability, rapid service execution, and strong airline and MRO relationships.

Boeing Global Services

Airbus Services

GE Aerospace

Safran

RTX Corporation

Lufthansa Technik

ST Engineering Aerospace

AAR Corp.

Barnes Aerospace

MTU Aero Engines

Turkish Technic

SR Technics

SIA Engineering Company

HAECO Group

Commercial aircraft aftermarket operations are increasingly driven by predictive maintenance platforms, digital twins, and AI-enabled inspection technologies. More than 60% of large airline and MRO organizations now utilize some form of predictive analytics to monitor component health and optimize replacement schedules. AI-assisted inspection systems improve fault-detection accuracy by approximately 20% while reducing inspection time by nearly 15%. Digital twin integration is enabling real-time asset monitoring across engines, avionics, and structural components, helping operators improve fleet availability and reduce maintenance disruptions. Companies with mature digital maintenance ecosystems are achieving faster turnaround times and stronger inventory control than operators relying on conventional maintenance planning.

Emerging technologies are reshaping parts manufacturing and supply-chain responsiveness. Aerospace-certified additive manufacturing reduces lead times by up to 40% for selected low-volume components while lowering production costs by approximately 15%. Cloud-connected inventory platforms improve stock visibility by nearly 20%, enabling more accurate parts allocation across maintenance networks. Adoption levels for digital traceability systems have exceeded 50% among major commercial operators, strengthening compliance management and component lifecycle tracking.

Between 2026 and 2028, AI-driven maintenance orchestration, automated repair workflows, and blockchain-enabled parts traceability are expected to accelerate deployment. Compared with legacy schedule-based maintenance, predictive maintenance programs can reduce unscheduled removals by approximately 20%. Airlines, OEM service providers, and advanced MRO networks are positioned to benefit most. Organizations that invest now in integrated maintenance intelligence and digital supply-chain capabilities will secure stronger operational resilience and aftermarket competitiveness.

February 2025 – GE Aerospace expanded its Singapore MRO footprint with a new LEAP engine module repair facility as part of a US$300 million investment program. The expansion strengthens regional repair capacity and reduces turnaround times for Asia-Pacific operators. Source: geaerospace.com

July 2025 – GE Aerospace announced a global investment exceeding US$1 billion to expand and modernize MRO and component repair facilities. The initiative adds engine test capacity and advanced inspection technologies, improving repair throughput and operational efficiency. Source: aviationpros.com

January 2026 – TransDigm Group agreed to acquire Jet Parts Engineering and Victor Sierra Aviation for approximately US$2.2 billion, strengthening its proprietary aftermarket parts portfolio. The move enhances product availability and competitive positioning in aircraft replacement components. Source: reuters.com

March 2026 – Lufthansa Technik opened a new 25,000-square-foot component services facility in Tulsa, adding 90 workstations and expanded avionics capabilities. The project increases repair capacity, improves regional parts availability, and supports faster maintenance execution. Source: aviationweek.com

This report provides comprehensive analysis of the Commercial Aircraft Aftermarket Parts Market across major component categories including Engine Parts, Airframe Parts, Avionics Components, Landing Gear Parts, and Cabin Interior Parts. The study evaluates demand patterns across Line Maintenance, Base Maintenance, Engine Overhaul, Component Repair, and Cabin Refurbishment applications while assessing procurement behavior among airlines, MRO providers, leasing companies, cargo operators, OEM service providers, and aviation service companies. More than 60% of market activity is linked to maintenance-intensive engine and component support operations, reflecting the sector's operational priorities.

The report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining fleet expansion, maintenance infrastructure, digital adoption, and supply-chain developments. Key technologies analyzed include predictive maintenance, digital twins, additive manufacturing, AI-enabled inspection systems, and traceability platforms. Strategic insights support expansion planning, supplier evaluation, investment prioritization, competitive benchmarking, partnership strategies, and long-term positioning between 2026 and 2033, with additional focus on emerging maintenance technologies and evolving aftermarket business models.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 46700 Million |

|

Market Revenue in 2033 |

USD 74432.7 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Boeing Global Services, Airbus Services, GE Aerospace, Safran, RTX Corporation, Lufthansa Technik, ST Engineering Aerospace, AAR Corp., Barnes Aerospace, MTU Aero Engines, Turkish Technic, SR Technics, SIA Engineering Company, HAECO Group, |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |