Reports

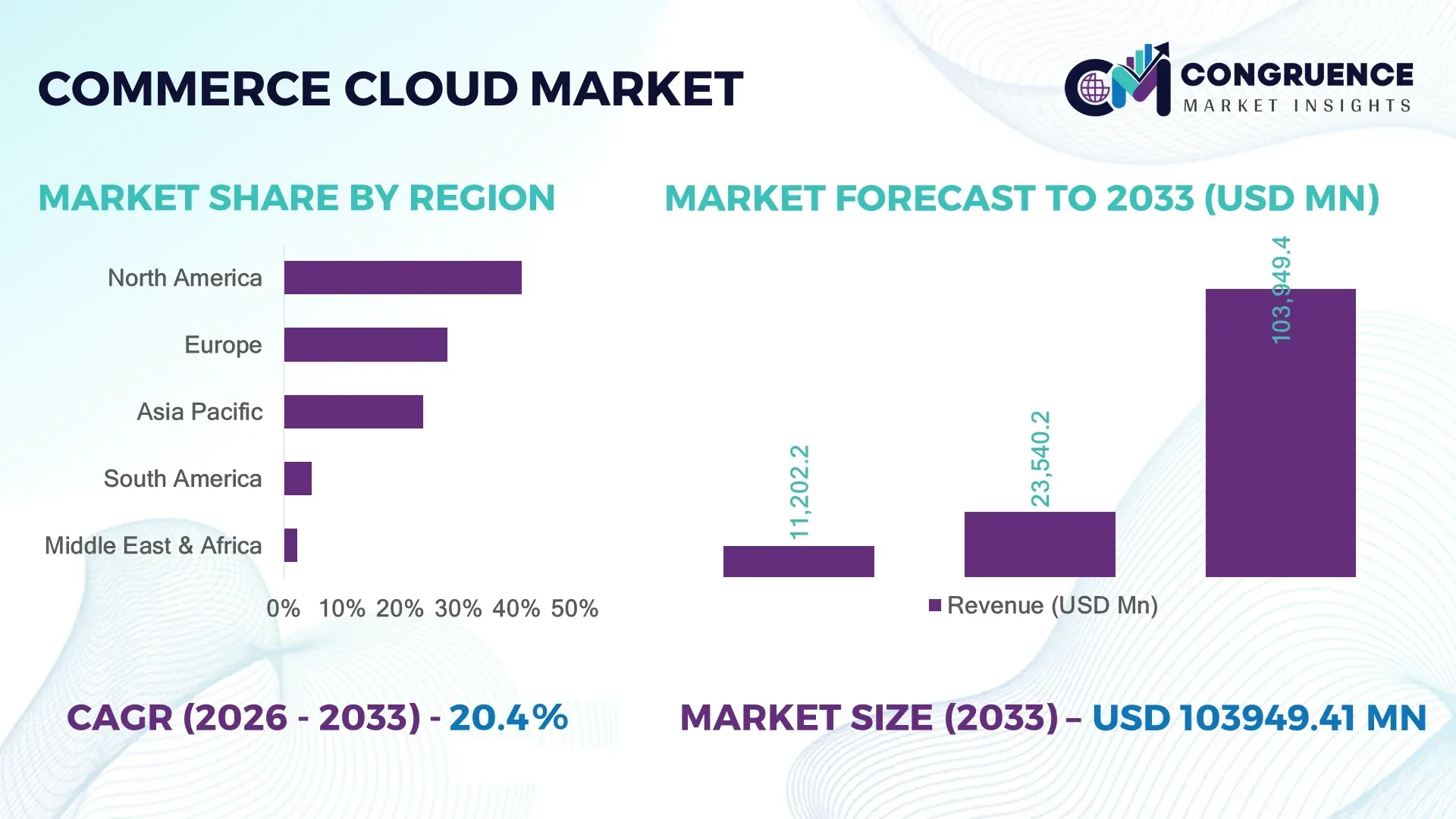

The Global Commerce Cloud Market was valued at USD 23,540.2 Million in 2025 and is anticipated to reach a value of USD 103,949.4 Million by 2033 expanding at a CAGR of 20.4% between 2026 and 2033. Growth is primarily driven by enterprise-wide digital commerce modernization, AI-powered customer personalization, omnichannel retail expansion, and increasing migration from legacy e-commerce infrastructure to cloud-native commerce platforms.

The United States continues to dominate the Commerce Cloud Market, accounting for approximately 39% of global enterprise commerce cloud deployments in 2025. More than 72% of Fortune 500 retailers operate at least one cloud-native commerce platform, while enterprise investment in digital commerce infrastructure exceeded USD 18 billion during the year. Retail, manufacturing, healthcare, and B2B wholesale collectively contribute over 68% of platform adoption. Compared with Germany, where enterprise cloud commerce penetration is close to 46%, the U.S. exceeds 63%, supported by AI-driven merchandising, composable commerce architecture, and extensive API ecosystem maturity. Following continued supply-chain restructuring after global trade disruptions, enterprises increasingly prioritize scalable cloud commerce platforms capable of supporting international fulfillment, localized storefronts, and real-time inventory orchestration.

This market increasingly rewards organizations investing in flexible, AI-enabled commerce ecosystems capable of rapidly adapting to evolving consumer behavior and global digital trade requirements.

Market Size & Growth: USD 23,540.2 Million (2025) to USD 103,949.4 Million (2033) at 20.4% CAGR, fueled by enterprise cloud transformation and AI-powered commerce.

Top Growth Drivers: AI personalization (64%), omnichannel retail adoption (58%), composable commerce deployment (47%).

Short-Term Forecast: By 2028, automated merchandising is projected to improve conversion rates by nearly 31%.

Emerging Technologies: Generative AI, headless commerce, predictive analytics, autonomous merchandising.

Regional Leaders: North America (~USD 39 Billion), Europe (~USD 26 Billion), Asia-Pacific (~USD 24 Billion) by 2033 with expanding enterprise digitalization.

Consumer Trends: Nearly 74% of online shoppers expect personalized product recommendations across every channel.

Enterprise Deployment: A 2025 retail transformation program reduced checkout abandonment by 26% through AI-driven optimization.

Competitive Landscape: Salesforce leads with approximately 24% market presence, followed by Adobe, SAP, Shopify, and Oracle.

Regulatory & ESG: Digital privacy regulations increased enterprise investment in compliant cloud architecture by nearly 29%.

Investment Activity: More than USD 9 billion has been invested globally in commerce cloud innovation, acquisitions, and platform expansion since 2024.

Innovation Outlook: Agentic AI, autonomous storefront management, and unified customer data platforms are reshaping enterprise commerce operations.

Commerce Cloud platforms have become mission-critical across retail, manufacturing, consumer goods, healthcare, and wholesale distribution as enterprises unify digital storefronts, order management, customer analytics, and inventory orchestration. AI-assisted merchandising, conversational commerce, and composable architectures now influence nearly 44% of new enterprise deployments, while continued global supply-chain diversification is accelerating demand for scalable multi-region commerce infrastructure, positioning the market for increasingly intelligent and automated digital commerce ecosystems.

The Commerce Cloud Market has evolved from a digital sales platform into a strategic enterprise infrastructure supporting customer engagement, supply-chain visibility, inventory optimization, and international business expansion. Organizations increasingly view commerce cloud investments as long-term competitive assets because digital purchasing now influences virtually every stage of the customer lifecycle across B2B and B2C industries. Growing cross-border commerce, marketplace expansion, and AI-driven personalization continue to reshape enterprise investment priorities.

Modern composable commerce architecture delivers approximately 42% faster deployment compared with traditional monolithic commerce platforms while reducing customization costs by nearly 34%. The United States continues to lead in enterprise-scale implementations, whereas Japan demonstrates one of the fastest adoption rates among manufacturing companies integrating commerce platforms with ERP, CRM, and warehouse automation systems. Over the next three years, AI-powered product discovery, conversational shopping assistants, and predictive merchandising are expected to improve customer conversion efficiency by approximately 28%.

Organizations are increasingly expanding strategic partnerships with cloud providers, payment companies, logistics providers, and AI developers to build unified digital commerce ecosystems. Several multinational retailers have shifted investments toward headless commerce deployments capable of supporting localized storefronts across more than 150 international markets while maintaining centralized inventory visibility and pricing consistency.

As enterprise competition increasingly shifts toward customer experience, operational agility, and digital resilience, the Commerce Cloud Market is becoming an essential foundation for scalable growth, technology leadership, and sustainable competitive differentiation.

The Commerce Cloud Market is undergoing structural transformation as organizations modernize legacy commerce infrastructure and integrate AI-driven automation into digital operations. Enterprise buyers increasingly prioritize cloud-native architectures capable of supporting omnichannel commerce, real-time inventory synchronization, intelligent merchandising, and personalized customer experiences. Digital transformation initiatives now extend beyond retailers into manufacturing, healthcare, telecommunications, automotive, financial services, and wholesale distribution. Businesses are simultaneously investing in cybersecurity, API-first architectures, low-code commerce development, and unified customer data platforms to improve operational flexibility. Meanwhile, increasing cross-border digital commerce, regulatory compliance requirements, and evolving consumer expectations continue reshaping platform capabilities and vendor competition.

Large enterprises continue replacing legacy commerce platforms with cloud-native ecosystems capable of supporting millions of simultaneous customer interactions while integrating logistics, inventory, CRM, and payment infrastructure. Approximately 67% of enterprise retailers now prioritize composable commerce strategies, while AI-driven product recommendation engines improve average order values by nearly 18%. Following global supply-chain restructuring, manufacturers increasingly deploy commerce cloud platforms to unify distributor, dealer, and direct-to-consumer sales channels. Technology vendors are responding through expanded AI capabilities, marketplace partnerships, and industry-specific cloud solutions. This structural transition creates stronger customer retention, faster deployment cycles, and significantly improved operational scalability, making commerce modernization a board-level investment priority across developed economies.

Many enterprises continue operating ERP, warehouse management, finance, and customer databases developed over multiple decades, making cloud migration considerably more complex than greenfield implementations. Nearly 48% of enterprise digital transformation projects require extensive middleware integration, while implementation timelines often extend beyond 12 months for multinational organizations. Data migration challenges, inconsistent product catalogs, and fragmented customer databases increase deployment costs and delay operational benefits. Organizations increasingly reduce these risks through phased modernization strategies, API management platforms, and hybrid deployment models that gradually replace legacy infrastructure while maintaining uninterrupted business operations.

Generative AI, autonomous merchandising, conversational shopping assistants, and predictive inventory optimization are creating entirely new business opportunities across the Commerce Cloud Market. More than 61% of enterprise buyers plan to expand AI investments within commerce operations before 2028. Dynamic pricing algorithms already reduce markdown losses by nearly 16%, while AI-assisted product content generation shortens merchandising workflows by approximately 52%. Technology providers increasingly invest in agentic commerce capabilities capable of automatically optimizing promotions, pricing, customer engagement, and inventory allocation. Organizations successfully integrating AI throughout commerce operations achieve faster decision-making, improved customer experiences, and stronger competitive differentiation.

As commerce cloud platforms become central enterprise operating systems, cybersecurity risks continue expanding alongside increasing regulatory obligations. Approximately 54% of enterprise security leaders identify API security as their primary digital commerce concern, while ransomware attacks targeting retail infrastructure continue increasing globally. International organizations must simultaneously comply with evolving privacy regulations, payment security standards, digital identity requirements, and cross-border data governance obligations. Companies increasingly address these challenges through zero-trust security architectures, continuous monitoring, AI-assisted fraud detection, and regional cloud deployment strategies. Long-term competitiveness increasingly depends on balancing digital innovation with enterprise-grade resilience, regulatory compliance, and trusted customer data management.

• AI-Powered Merchandising Expansion: AI-powered merchandising platforms now influence nearly 63% of enterprise product recommendation engines, increasing customer engagement by approximately 29% while improving average basket values by 17%. Retailers increasingly automate pricing, promotions, and catalog optimization through machine learning models capable of analyzing millions of purchasing signals daily. Technology vendors continue expanding partnerships with generative AI providers to accelerate intelligent commerce automation.

• Headless Commerce Adoption Accelerates: Nearly 58% of large digital retailers now prioritize headless commerce architectures because they shorten storefront deployment times by almost 41% while supporting omnichannel customer experiences. Enterprises increasingly separate frontend customer experiences from backend commerce engines, enabling faster innovation, localized experiences, and simplified integration with mobile applications, marketplaces, social commerce, and connected devices.

• Unified Customer Data Platforms Gain Momentum: Customer data platforms are becoming foundational components of modern commerce ecosystems. More than 69% of enterprise commerce organizations now integrate behavioral analytics, CRM, loyalty data, and purchasing history into unified AI-driven personalization engines. These capabilities improve customer retention by approximately 23% while enabling increasingly accurate predictive merchandising strategies across digital and physical channels.

• Cross-Border Digital Commerce Transformation: International digital commerce continues expanding as multinational organizations localize storefronts across multiple languages, currencies, and tax jurisdictions. Nearly 46% of enterprise commerce investments now prioritize global fulfillment optimization and localized customer experiences. Companies increasingly deploy cloud-native order orchestration, regional inventory visibility, and AI-assisted logistics optimization to reduce fulfillment costs while supporting resilient international expansion.

The Commerce Cloud Market is segmented by type, application, and end-user, reflecting the increasing diversification of enterprise digital commerce strategies across industries. Organizations are shifting from traditional monolithic platforms toward modular, cloud-native commerce environments that improve operational flexibility and customer engagement. AI-driven automation, API-first integration, and composable architecture continue to influence purchasing decisions across retailers, manufacturers, wholesalers, and service providers. Approximately 62% of new enterprise implementations now prioritize scalability and interoperability over standalone commerce functionality, while cloud-based deployment has surpassed 71% of all newly commissioned commerce platforms. Businesses increasingly select solutions based on deployment flexibility, integration capability, AI readiness, and support for global omnichannel operations, creating differentiated growth opportunities across every market segment.

The Commerce Cloud Market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud platforms. Public Cloud remains the leading deployment type, accounting for approximately 56% of enterprise implementations due to lower infrastructure costs, rapid deployment, automatic software updates, and virtually unlimited scalability. Global retailers, consumer brands, and digital-first enterprises continue migrating toward public cloud commerce platforms to support seasonal traffic spikes and international expansion without maintaining dedicated infrastructure.

Hybrid Cloud represents the fastest-growing segment and is expected to expand at a CAGR of approximately 22.6% through 2033. Large enterprises increasingly combine private environments for sensitive customer and payment data with public cloud infrastructure for customer-facing storefronts and AI workloads. This architecture provides improved compliance while maintaining operational flexibility. Private Cloud continues serving highly regulated industries including banking, government, and healthcare, contributing nearly 20% of market deployments where data sovereignty remains a primary consideration.

Technology vendors continue expanding hybrid deployment capabilities through containerized applications, Kubernetes orchestration, and API-driven interoperability, enabling organizations to modernize existing commerce operations without replacing mission-critical legacy systems.

According to the 2025 Flexera State of the Cloud Report, more than 73% of enterprises globally now operate hybrid cloud strategies as organizations increasingly balance scalability, security, and regulatory compliance across business-critical applications.

Based on application, the Commerce Cloud Market is segmented into Retail & Consumer Goods, Manufacturing, BFSI, Healthcare, Telecommunications, Media & Entertainment, and Others.

Retail & Consumer Goods continues leading adoption with approximately 44% of enterprise deployments as organizations modernize omnichannel commerce, personalized marketing, digital storefront management, and AI-powered customer engagement. Retailers increasingly integrate commerce platforms with loyalty systems, warehouse automation, social commerce, and marketplace operations to improve customer lifetime value while reducing operational complexity.

Manufacturing represents the fastest-growing application segment and is projected to expand at approximately 22.1% CAGR through 2033. Manufacturers increasingly deploy commerce cloud platforms for direct-to-customer sales, dealer management, spare parts ordering, distributor collaboration, and digital product configuration. BFSI, Healthcare, Telecommunications, Media & Entertainment, and other industries collectively contribute approximately 56% of total deployments as organizations expand digital service delivery and customer self-service capabilities.

Enterprise purchasing behavior continues evolving rapidly. Nearly 68% of organizations implementing commerce cloud platforms now integrate AI-powered recommendation engines, while over 59% deploy unified customer data platforms to strengthen omnichannel engagement and improve customer retention.

The 2025 Salesforce Connected Customer research reported that nearly 73% of customers expect companies to understand their unique needs across every interaction, reinforcing enterprise investment in AI-enabled commerce platforms.

The Commerce Cloud Market serves Large Enterprises, Small & Medium Enterprises (SMEs), and Government & Public Organizations.

Large Enterprises account for nearly 67% of total platform deployments owing to extensive digital commerce operations, multinational supply chains, complex customer engagement strategies, and significant IT investment capacity. These organizations increasingly adopt composable commerce, AI-powered merchandising, cloud-native order management, and unified customer experience platforms capable of supporting millions of daily transactions across multiple international markets.

Small and Medium Enterprises represent the fastest-growing end-user category and are expected to expand at approximately 23.4% CAGR through 2033. Subscription-based commerce platforms, low-code development environments, integrated payment ecosystems, and managed cloud services continue lowering implementation barriers. Government agencies and public organizations collectively contribute approximately 11% of deployments as citizen service portals, procurement modernization, and digital public service initiatives expand globally.

Business purchasing priorities increasingly emphasize operational agility rather than platform ownership. More than 65% of enterprise buyers now rank AI capability among their top three vendor selection criteria, while nearly 58% prioritize API ecosystem maturity when evaluating commerce cloud providers.

According to the 2026 IDC Future Enterprise Survey, more than 70% of digitally mature organizations identified unified commerce platforms as a core technology investment supporting customer experience transformation and enterprise operational resilience.

North America accounted for the largest market share at 40.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.7% between 2026 and 2033.

North America maintains leadership through mature enterprise cloud adoption, AI-driven retail transformation, and strong investments by major technology vendors. More than 71% of large enterprises in the region operate cloud-native digital commerce environments supporting omnichannel customer experiences. Europe follows with approximately 28.1% of global demand, driven by digital commerce modernization, regulatory compliance, and increasing B2B platform investments. Asia-Pacific represents the fastest-expanding regional marketplace as enterprise cloud adoption accelerates across China, India, Japan, South Korea, Singapore, and Australia. The region accounts for nearly 31% of global online retail transactions while enterprise digital transformation initiatives continue expanding rapidly across manufacturing, financial services, and consumer goods industries. South America continues benefiting from rapid marketplace expansion and digital payment adoption, whereas Middle East & Africa experience increasing investment in cloud infrastructure, smart city development, and enterprise modernization programs. Collectively, emerging economies now account for nearly 37% of all newly deployed commerce cloud platforms, illustrating a structural shift toward globally distributed digital commerce ecosystems.

Strategic Digital Commerce Leadership Through Enterprise AI Adoption

North America remains the largest regional Commerce Cloud Market, contributing approximately 40.8% of global enterprise deployments during 2025. Large retailers, healthcare providers, manufacturers, financial institutions, and technology companies continue modernizing commerce operations through composable architecture, AI-powered merchandising, predictive analytics, and cloud-native order management systems. More than 74% of Fortune 1000 organizations now utilize at least one enterprise commerce cloud platform. Strategic investments increasingly target headless commerce, unified customer data platforms, and AI-assisted customer engagement. Cloud infrastructure expansion, widespread API adoption, and mature cybersecurity frameworks further strengthen enterprise confidence. Consumer purchasing behavior reflects strong demand for personalized shopping experiences, subscription commerce, and omnichannel fulfillment capabilities, making North America the benchmark for advanced digital commerce transformation.

United States Market Outlook: The United States accounts for nearly 82% of North American Commerce Cloud deployments, supported by world-leading cloud infrastructure providers, advanced retail ecosystems, and high enterprise technology spending. More than 72% of Fortune 500 retailers utilize AI-enabled commerce platforms to optimize pricing, inventory management, customer personalization, and digital marketing. Enterprise investments increasingly prioritize composable commerce architectures supporting international expansion, marketplace integration, and automated fulfillment networks.

Strategic Regulatory Compliance Driving Enterprise Commerce Innovation

Europe accounted for approximately 28.1% of the global Commerce Cloud Market in 2025, supported by mature digital infrastructure, cross-border e-commerce expansion, and stringent data governance regulations. Germany, the United Kingdom, and France collectively contribute nearly 64% of regional enterprise deployments. Organizations increasingly prioritize cloud commerce platforms capable of supporting multilingual storefronts, localized taxation, and GDPR-compliant customer data management. More than 61% of European retailers have integrated AI-powered recommendation engines and automated inventory synchronization into their commerce operations. Sustainability initiatives are also shaping procurement decisions, with enterprises seeking energy-efficient cloud infrastructure and paperless digital transaction ecosystems. Technology vendors continue expanding regional cloud availability zones and compliance-certified data centers to support highly regulated industries including financial services, healthcare, and public administration.

Germany Market Outlook: Germany represents the largest Commerce Cloud Market within Europe due to its strong manufacturing base, advanced B2B commerce ecosystem, and rapid Industry 4.0 adoption. Approximately 49% of medium and large manufacturers have integrated cloud commerce platforms with ERP and supply chain management systems to support direct customer engagement and distributor collaboration. Investment continues toward AI-enabled procurement automation, digital product configuration, and intelligent order orchestration, reinforcing Germany's leadership in enterprise commerce modernization.

Large-Scale Digital Transformation Reshaping Enterprise Commerce

Asia-Pacific has become the fastest-growing Commerce Cloud Market globally, accounting for nearly 23.9% of worldwide deployments in 2025 while recording the highest enterprise implementation momentum. China, India, Japan, South Korea, Singapore, and Australia collectively account for more than 81% of regional commerce cloud investments. The region benefits from expanding internet penetration, widespread smartphone usage, digital payment ecosystems, and government-supported cloud transformation initiatives. More than 69% of newly established online retailers across Asia-Pacific deploy cloud-native commerce platforms from launch, while manufacturing enterprises increasingly digitize dealer management and B2B procurement systems. Regional cloud providers continue investing heavily in AI infrastructure, localized data centers, and developer ecosystems supporting high-volume digital commerce operations.

China Market Outlook: China remains the largest Commerce Cloud Market in Asia-Pacific, supported by its massive digital retail ecosystem, advanced logistics infrastructure, and AI-enabled commerce innovation. More than 78% of major online retailers leverage cloud-native commerce platforms integrated with intelligent recommendation engines, real-time inventory management, and automated fulfillment networks. Enterprise investment increasingly focuses on cross-border commerce, livestream shopping integration, and AI-powered customer engagement technologies that strengthen operational efficiency across domestic and international markets.

Digital Payment Expansion Accelerating Commerce Modernization

South America continues strengthening its Commerce Cloud Market through expanding digital payment adoption, growing online retail participation, and increasing investment in enterprise cloud modernization. The region contributes approximately 4.8% of global enterprise deployments, with Brazil and Argentina representing nearly 73% of regional demand. Retailers increasingly replace legacy e-commerce systems with cloud-native commerce platforms supporting mobile-first customer experiences, integrated payment gateways, and localized fulfillment capabilities. More than 57% of online purchases within the region now originate from mobile devices, encouraging businesses to prioritize responsive commerce architecture and AI-powered customer engagement. Infrastructure limitations remain in selected markets, yet continuous cloud investment and fintech innovation continue improving enterprise scalability.

Brazil Market Outlook: Brazil dominates the South American Commerce Cloud Market through its rapidly expanding digital economy and sophisticated payment ecosystem. Approximately 65% of medium and large retailers now operate cloud-based commerce environments integrated with digital wallets, installment payment solutions, and AI-assisted marketing automation. Continued expansion of omnichannel retail, marketplace participation, and logistics technology supports enterprise investment across both B2C and B2B commerce operations.

Enterprise Modernization Supporting Next-Generation Digital Commerce

The Middle East & Africa Commerce Cloud Market continues expanding as governments accelerate digital economy initiatives, cloud infrastructure investment, and smart city development. The region represents approximately 2.4% of global deployments while enterprise adoption continues strengthening across retail, banking, telecommunications, and public services. Countries including the UAE, Saudi Arabia, and South Africa have significantly expanded national cloud infrastructure to support enterprise digital transformation. More than 46% of newly established enterprise digital platforms now utilize cloud-native commerce architecture, while AI-driven customer engagement and digital payment integration continue improving operational efficiency. Regional technology partnerships increasingly emphasize cybersecurity, regulatory compliance, and localized cloud services to support sustainable digital commerce growth.

United Arab Emirates Market Outlook: The UAE has emerged as the regional leader in Commerce Cloud adoption through substantial investment in cloud infrastructure, digital government initiatives, and smart retail transformation. Nearly 62% of large enterprises have adopted cloud-based customer engagement platforms integrated with AI, omnichannel commerce, and advanced analytics. Continued investment in hyperscale data centers, fintech innovation, and cross-border digital trade positions the country as a strategic gateway for enterprise commerce expansion across the Middle East.

The Commerce Cloud Market remains moderately consolidated, with Salesforce, Adobe, Shopify, SAP, and Oracle competing aggressively for enterprise digital transformation projects while Microsoft, commercetools, BigCommerce, VTEX, and Elastic Path strengthen competition through composable commerce and API-first innovation. The top five vendors collectively control approximately 66% of global enterprise deployments, reflecting strong platform maturity and ecosystem advantages. Competition increasingly centers on AI capabilities, deployment speed, ecosystem integration, developer flexibility, and global infrastructure rather than pricing alone. AI-powered merchandising improves conversion performance by nearly 25%, while composable architectures reduce deployment timelines by approximately 40%, creating measurable competitive differentiation. Vendors continue expanding through strategic partnerships with hyperscale cloud providers, payment companies, logistics platforms, and generative AI developers. Vertical-specific cloud offerings for manufacturing, retail, healthcare, and B2B commerce are becoming increasingly important. The principal barrier for new entrants remains enterprise integration complexity, established partner ecosystems, and extensive implementation expertise. Success increasingly depends on delivering AI-native, scalable, secure, and highly interoperable commerce ecosystems capable of supporting multinational digital operations.

SAP

Oracle

commercetools

BigCommerce

VTEX

Elastic Path

Kibo Commerce

Spryker

HCL Commerce

Wix

Sitecore

Artificial intelligence has become the defining technology shaping the Commerce Cloud Market, enabling enterprises to automate merchandising, demand forecasting, customer segmentation, pricing optimization, and conversational shopping experiences. Nearly 68% of enterprise commerce implementations now integrate AI-powered recommendation engines, while predictive analytics improves inventory forecasting accuracy by approximately 31%. Generative AI further accelerates digital merchandising by reducing product content creation time by almost 55%, allowing retailers to launch new product catalogs significantly faster. Organizations adopting AI-first commerce platforms increasingly report stronger customer engagement and higher operational efficiency.

Composable commerce architecture is rapidly replacing traditional monolithic platforms. API-first infrastructure, microservices, headless storefronts, and event-driven integration improve deployment flexibility while reducing upgrade complexity. Compared with conventional commerce suites, composable platforms shorten implementation cycles by nearly 42% and reduce long-term customization costs by approximately 30%. Retailers, manufacturers, wholesalers, and marketplace operators benefit from greater agility because individual services can be upgraded independently without disrupting overall commerce operations. Cloud-native deployment also improves platform availability and global scalability for multinational organizations.

Between 2026 and 2028, autonomous commerce capabilities are expected to become increasingly mainstream through AI agents capable of optimizing promotions, inventory allocation, customer engagement, and pricing decisions without continuous human intervention. Organizations investing early in unified customer data platforms, AI-powered commerce automation, real-time analytics, and intelligent order orchestration will achieve stronger competitive positioning as enterprise digital commerce increasingly evolves toward highly automated, predictive, and personalized customer ecosystems.

September 2024 – Salesforce introduced Agentforce, its autonomous AI platform that extends Commerce Cloud with AI agents capable of handling customer service, sales, and marketing workflows. The platform integrates with Slack and MuleSoft while supporting multiple AI models, enabling enterprises to automate repetitive commerce interactions and improve customer engagement. Source: Salesforce News

September 2024 – Salesforce completed the acquisition of Own Company for approximately USD 1.9 billion, strengthening enterprise data protection, backup, and compliance capabilities across its cloud ecosystem. The acquisition enhances resilience for Commerce Cloud customers managing mission-critical customer and transaction data. Source: Salesforce News

June 2024 – Oracle announced a USD 1 billion investment to establish a new cloud region in Madrid in partnership with Telefónica. The expansion enhances cloud infrastructure for European enterprises, improves regulatory compliance, and supports faster deployment of Oracle Commerce and AI-enabled business applications across the region. Source: Oracle News

September 2024 – Salesforce expanded its enterprise cloud portfolio with Salesforce Foundations, bringing Sales Cloud, Service Cloud, Marketing Cloud, and Commerce Cloud capabilities into a unified offering. The release simplifies cross-functional deployment for small and mid-sized businesses while accelerating AI-powered customer engagement across multiple business functions. Source: Salesforce News

The Commerce Cloud Market Report provides a comprehensive assessment of the global industry by evaluating technology evolution, deployment models, enterprise adoption, competitive dynamics, and long-term digital commerce transformation across major industries. The report analyzes market performance across Public Cloud, Private Cloud, and Hybrid Cloud deployment models while examining applications in retail, manufacturing, BFSI, healthcare, telecommunications, media & entertainment, and other enterprise sectors. It further evaluates demand patterns among large enterprises, SMEs, and public-sector organizations, highlighting differences in digital maturity, deployment priorities, and operational strategies. More than 20 major countries across five key regions are assessed to provide detailed geographic intelligence and country-level investment trends.

The study also examines emerging technologies including generative AI, composable commerce, headless architecture, API-first integration, predictive analytics, customer data platforms, intelligent order management, and autonomous merchandising. Strategic analysis covers competitive positioning, enterprise digital transformation initiatives, cloud infrastructure investments, regulatory developments, cybersecurity considerations, ecosystem partnerships, and innovation strategies shaping future market direction. The report supports business leaders, investors, technology providers, and policymakers by identifying high-opportunity segments, evolving customer adoption patterns, deployment best practices, and competitive benchmarks expected to influence enterprise commerce strategies throughout the 2026–2033 forecast period.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 23,540.2 Million |

|

Market Revenue in 2033 |

USD 103,949.4 Million |

|

CAGR (2026 - 2033) |

20.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Salesforce, Adobe Commerce, Shopify, SAP, Oracle, commercetools, BigCommerce, VTEX, Elastic Path, Kibo Commerce, Spryker, HCL Commerce, Wix, Sitecore |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |