Reports

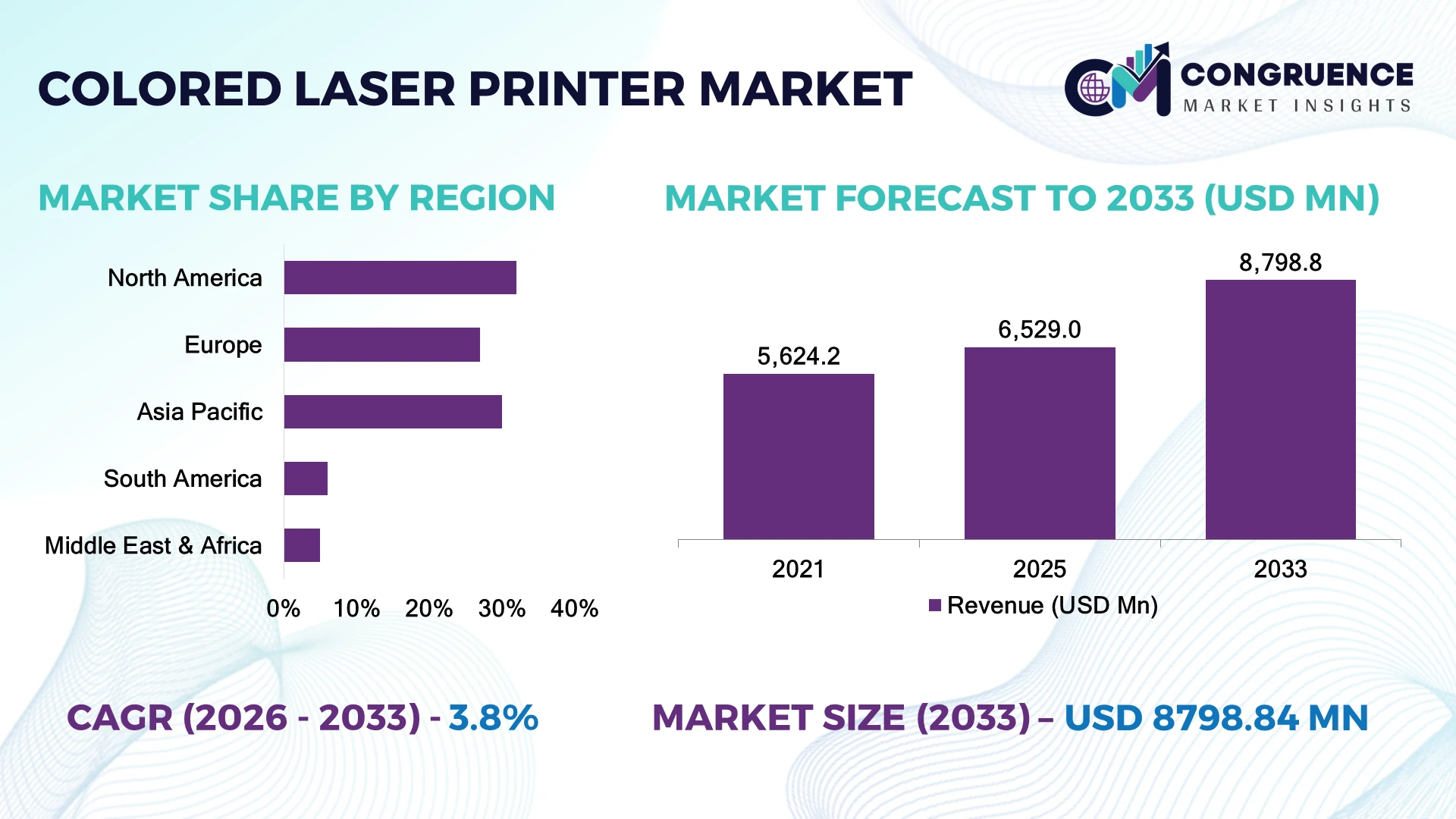

The Global Colored Laser Printer Market was valued at USD 6,529.0 Million in 2025 and is anticipated to reach a value of USD 8,798.8 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. Growth is driven by rising enterprise digitization, demand for secure high-volume document management, and adoption of energy-efficient laser printing technologies across commercial environments.

The United States dominates the colored laser printer market with nearly 32% share, supported by strong enterprise printing infrastructure, corporate automation investments, and high adoption across healthcare, education, and government sectors. China follows with around 25% share, backed by large-scale manufacturing capacity and expanding office automation demand. The U.S. enterprise sector deploys advanced managed printing solutions across over 60% of large organizations, while Asia-Pacific benefits from rapid industrial expansion and supply-chain localization initiatives linked to global manufacturing shifts.

Strategic decisions increasingly focus on automation, cybersecurity, and cost-efficient printing ecosystems.

Market Size & Growth: USD 6.5 billion market in 2025 reaching USD 8.8 billion by 2033 at 3.8% CAGR, driven by enterprise automation and secure document workflows.

Top Growth Drivers: Enterprise digitization 35%, managed print adoption 28%, and energy-efficient printer upgrades 22% are accelerating market expansion.

Short-Term Forecast: By 2028, automated print management adoption increases by 25%, reducing operational costs by 15% across large enterprises.

Emerging Technologies: AI-based print analytics, cloud printing platforms, and advanced toner materials are reshaping next-generation printer systems.

Regional Leaders: North America reaches USD 3.0 billion with high enterprise adoption, Asia-Pacific reaches USD 2.8 billion through manufacturing expansion, and Europe reaches USD 1.9 billion through sustainable office initiatives.

Consumer/End-User Trends: Over 55% of enterprises prioritize multifunction color laser devices for productivity, security, and workflow integration.

Pilot/Case Example: In 2024, corporate managed printing deployments achieved nearly 20% paper waste reduction through centralized monitoring and automation.

Competitive Landscape: HP leads with approximately 30% market share, followed by Canon, Brother, Xerox, and Ricoh competing through enterprise-focused product innovation.

Regulatory & ESG Impact: Energy-efficient printing standards improve power consumption performance by around 20%, supporting corporate sustainability targets.

Investment & Funding: More than USD 1 billion is directed toward printing technology upgrades, cloud integration, and strategic enterprise partnerships.

Innovation & Future Outlook: Next-generation printers emphasize AI security, connected workflows, and low-maintenance designs, creating stronger competitive differentiation.

The Colored Laser Printer Market is gaining importance as businesses prioritize reliable digital-to-physical workflows, secure printing environments, and efficient office operations. Demand is expanding across corporate offices, healthcare facilities, educational institutions, and government agencies, where advanced color accuracy and productivity remain critical. Around 40% of enterprise printing environments are shifting toward managed solutions, while global manufacturers are restructuring supply chains to improve component availability amid semiconductor and logistics challenges. Recent product innovations include AI-enabled monitoring, automated toner management, and cloud-connected printing platforms. Regional adoption remains strong in North America and Europe, while Asia-Pacific is becoming a major production and deployment hub. The market is transitioning toward smarter, connected, and sustainable printing ecosystems.

The Colored Laser Printer Market is becoming strategically important as enterprises seek secure, efficient, and digitally integrated printing infrastructure. Organizations are replacing fragmented printing networks with centralized managed solutions that improve operational control, cybersecurity, and resource utilization. The shift toward hybrid workplaces and automated business processes is accelerating investments in connected printing technologies.

Modern color laser printers deliver faster processing, improved security, and lower operating expenses compared with traditional office printers. Advanced devices with automated monitoring reduce maintenance requirements by nearly 20% and improve workflow efficiency through cloud-based management. North America continues to lead through enterprise technology adoption, while Asia-Pacific demonstrates faster deployment growth due to expanding commercial infrastructure and manufacturing capabilities.

Companies are strengthening partnerships around software integration, supply-chain resilience, and sustainable product development. For example, large enterprises are deploying centralized print management systems to monitor device usage, reduce unnecessary printing, and improve document security. Manufacturers are prioritizing energy-efficient designs, recyclable materials, and smart connectivity features to meet evolving business requirements. Competitive positioning in this market increasingly depends on innovation speed, operational efficiency, and the ability to deliver secure, intelligent printing ecosystems.

Enterprise automation and demand for secure document infrastructure are accelerating colored laser printer adoption across corporate environments. Over 60% of large enterprises are integrating managed print solutions, while nearly 55% prioritize cybersecurity-enabled printing systems to control sensitive workflows. The shift toward hybrid workplaces and centralized document management is increasing demand for high-speed, multifunction laser platforms. In the United States, healthcare and financial institutions are expanding secure printing networks to meet compliance requirements. Companies are responding through cloud-connected product launches, software partnerships, and investments in AI-based monitoring tools that reduce downtime and improve operational efficiency.

Colored laser printer manufacturers face structural pressure from component price fluctuations, semiconductor dependency, and supply-chain concentration. Approximately 35% of printer components rely on specialized electronic suppliers, while toner and imaging unit costs account for nearly 40% of total device lifecycle expenses. Disruptions in Asian manufacturing hubs have increased procurement complexity and extended inventory cycles. Companies are reducing exposure through supplier diversification, localized production strategies, and long-term component agreements. Leading manufacturers are also redesigning product architectures to improve material efficiency and reduce dependency on high-cost components, supporting more stable margins and scalable deployment.

The expansion of smart office ecosystems creates opportunities for advanced colored laser printer solutions integrated with cloud platforms, analytics, and automation tools. Around 45% of enterprises are adopting cloud-based document workflows, while AI-enabled device monitoring can reduce maintenance requirements by nearly 20%. Countries such as India and Indonesia are witnessing rising demand from expanding SMEs and digital business operations. Manufacturers are investing in software-driven printing platforms, subscription-based service models, and connected device ecosystems. A key opportunity lies in transforming printers from standalone hardware into intelligent workflow assets that improve productivity, security, and resource management.

Increasing connectivity introduces cybersecurity and interoperability challenges for enterprise printing networks. Nearly 50% of organizations identify connected device security as a major concern, while over 30% of businesses operate mixed printer environments requiring complex integration management. The expansion of cloud printing and remote access solutions increases exposure to unauthorized access and data vulnerabilities. Companies must strengthen encryption technologies, firmware security, and compatibility frameworks to maintain deployment reliability. In markets such as Japan and Germany, strict data protection requirements are influencing product design priorities. Long-term competitiveness depends on balancing intelligent connectivity with secure, seamless, and sustainable printing operations.

Cloud Printing Integration Shift Enterprise printing is moving toward cloud-managed platforms, with nearly 45% of large organizations adopting centralized print management and over 30% integrating remote monitoring capabilities. This transition improves workflow visibility, reduces administrative workload, and enables faster device optimization. Companies are expanding software partnerships and developing connected printer ecosystems to support hybrid workplace operations.

AI-Based Workflow Automation AI-driven printer analytics are gaining traction, with approximately 25% of enterprises deploying predictive maintenance features and nearly 20% reducing service interruptions through automated diagnostics. The adoption of intelligent monitoring is changing printer management from reactive maintenance to proactive optimization. Manufacturers are embedding machine learning capabilities and automation tools to improve device performance and customer retention.

Sustainable Printing Transformation Environmental compliance and resource efficiency are influencing procurement decisions, with around 40% of enterprises prioritizing energy-efficient printing equipment and 35% seeking recyclable consumable solutions. Regulatory pressure in countries such as Germany and Japan is accelerating sustainable product development. Companies are redesigning hardware, improving toner efficiency, and adopting circular manufacturing practices.

Secure Document Infrastructure Growth Rising cybersecurity concerns are reshaping enterprise printing strategies, with more than 50% of organizations strengthening connected device security policies. Supply-chain disruptions have also encouraged companies to localize printer component sourcing and improve inventory resilience. Manufacturers are responding through encrypted firmware, authentication systems, and strategic production expansion to protect enterprise document environments.

Color multifunction printers dominate the colored laser printer market with approximately 55% share due to their ability to combine printing, scanning, copying, and workflow management within a single platform. Their scalability, lower operational complexity, and integration with enterprise software systems make them preferred across corporate offices, healthcare institutions, and government facilities. Single-function colored laser printers maintain strong demand among cost-sensitive users, accounting for nearly 30% of deployments, while compact models support small office environments with space-efficient solutions. The fastest-growing type is advanced network-enabled multifunction printers, supported by increasing demand for cloud connectivity, automated workflows, and secure document handling. Around 40% of new enterprise installations include connected management capabilities, prompting manufacturers to prioritize software integration and cybersecurity features. Companies are shifting investment toward intelligent multifunction platforms that provide higher productivity and reduced maintenance requirements.

Enterprise document management represents the leading application segment with nearly 60% market share, driven by high-volume printing requirements across banking, healthcare, education, and corporate sectors. Organizations rely on colored laser printers for secure reports, presentations, compliance documents, and customer communications. Commercial offices account for over 45% of enterprise deployments, supported by increasing demand for reliable and fast color output. The fastest-growing application is cloud-connected workflow printing, expanding as businesses adopt digital transformation strategies and hybrid work models. Approximately 35% of organizations are integrating cloud-based print solutions to improve accessibility and reduce manual processes. Other applications, including educational institutions and government documentation systems, continue to grow through modernization programs. Companies are responding by developing subscription-based services, automated workflow tools, and integrated software platforms to capture evolving enterprise requirements.

Corporate enterprises represent the largest end-user segment with approximately 65% market share due to extensive printing requirements, centralized infrastructure, and demand for secure document workflows. Financial services, healthcare providers, and multinational companies maintain large printer fleets requiring advanced management capabilities. Small and medium enterprises contribute around 25% of demand, increasingly adopting compact and cloud-enabled devices to improve productivity without significant infrastructure investment. The fastest-growing end-user group is healthcare organizations, driven by rising documentation needs, regulatory compliance, and secure patient information management. Healthcare facilities are increasing investments in connected printing systems, with adoption rates improving by nearly 30% as digital healthcare operations expand. Educational institutions and government users continue modernizing printing infrastructure through efficiency-focused procurement programs. Companies are targeting these segments through customized service agreements, managed print partnerships, and sector-specific security solutions.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America held approximately 32% of the global colored laser printer market in 2025, supported by high enterprise penetration, advanced IT infrastructure, and strong adoption of managed print services. The United States contributes nearly 28% of global demand, with significant deployment across banking, healthcare, education, and government sectors. More than 60% of large enterprises in the region utilize centralized printing management solutions to improve security and operational control. Companies are strengthening cloud-print partnerships, cybersecurity capabilities, and AI-enabled monitoring platforms to support evolving workplace requirements.

United States Market Outlook: The United States remains the regional technology leader due to mature enterprise infrastructure and strong demand for secure document solutions. Nearly 65% of large organizations have integrated managed print environments, while businesses continue investing in connected devices, workflow automation, and cybersecurity-focused printing platforms to optimize operational efficiency.

Europe accounted for approximately 27% of the colored laser printer market in 2025, driven by sustainability requirements, enterprise modernization, and strict data security standards. Germany, the United Kingdom, and France represent major deployment markets due to strong corporate infrastructure and industrial activity. Around 45% of European enterprises prioritize energy-efficient office equipment as sustainability policies influence procurement decisions. Manufacturers are expanding recyclable consumable solutions, improving device efficiency, and developing secure printing technologies aligned with European environmental and data protection frameworks.

Germany Market Outlook: Germany leads European adoption through its advanced industrial base, automation capabilities, and strong corporate technology spending. More than 50% of large German enterprises emphasize efficient workplace technologies, supporting demand for connected laser printers with lower maintenance requirements and improved energy performance across manufacturing and commercial environments.

Asia-Pacific represented nearly 30% of the colored laser printer market in 2025 and is positioned as the fastest-expanding market due to manufacturing scale, enterprise digitization, and expanding SME adoption. China, Japan, South Korea, and India are major contributors, supported by strong electronics ecosystems and growing office automation demand. China accounts for nearly 18% of global market demand, while regional manufacturers benefit from established component supply chains. Companies are increasing production capacity, forming technology partnerships, and introducing affordable connected printing solutions for expanding commercial users.

China Market Outlook: China remains the key regional hub due to extensive manufacturing capabilities and large-scale enterprise deployment. The country supports over 40% of global printer component production activities, while domestic businesses increasingly adopt multifunction and cloud-connected printing systems to improve productivity and operational management.

South America accounted for around 6% of the global colored laser printer market in 2025, with Brazil and Argentina representing the largest demand centers. Adoption is concentrated in corporate offices, government institutions, education facilities, and financial services. Brazil contributes nearly 4% of global demand due to its larger commercial base and expanding digital infrastructure. Companies are addressing infrastructure challenges through regional distribution partnerships, localized service networks, and cost-efficient product portfolios. Increasing digital documentation requirements are supporting gradual replacement of traditional printing systems.

Brazil Market Outlook: Brazil dominates South American adoption due to its commercial scale, industrial activity, and expanding enterprise technology investments. More than 50% of large Brazilian companies are upgrading workplace technology systems, creating demand for reliable color printing solutions integrated with digital workflow platforms.

Middle East & Africa accounted for approximately 5% of the colored laser printer market in 2025, supported by government modernization programs, enterprise expansion, and increasing investment in digital infrastructure. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are driving adoption through smart office initiatives and institutional upgrades. The UAE represents nearly 2% of global demand, supported by advanced commercial infrastructure and technology-focused investments. Companies are expanding partnerships with regional distributors and deploying secure printing solutions for government, healthcare, and financial sectors.

United Arab Emirates Market Outlook: The UAE remains the leading market within the region due to strong technology adoption, smart government programs, and advanced business infrastructure. More than 60% of government-related organizations have accelerated digital workplace transformation initiatives, supporting demand for connected, secure, and automated printing systems.

The colored laser printer market features global OEM leaders such as HP, Canon, Brother, Xerox, Ricoh, and Kyocera competing against regional suppliers and specialized document-management providers. The top five players collectively account for approximately 65% of the market, creating a moderately consolidated structure. Competition is driven by device performance, security features, software integration, toner efficiency, and service ecosystems. Around 45% of enterprises prioritize managed print capabilities, while nearly 35% evaluate cybersecurity and workflow automation features during procurement. Companies compete through cloud-print partnerships, AI-enabled monitoring, portfolio expansion, and vertical integration of consumables and hardware. The market is shifting toward connected printing platforms, with traditional hardware competition moving toward software-led differentiation. High technology investment requirements, distribution networks, and service infrastructure create entry barriers. Winning players must combine reliable hardware, intelligent software, secure ecosystems, and cost-efficient lifecycle management.

Canon Inc.

Brother Industries Ltd.

Xerox Holdings Corporation

Ricoh Company Ltd.

Kyocera Corporation

Seiko Epson Corporation

Lexmark International Inc.

Konica Minolta Inc.

Sharp Corporation

Fujifilm Business Innovation Corporation

Toshiba Tec Corporation

Modern colored laser printers are shifting from standalone devices toward connected workflow platforms integrating cloud management, AI analytics, and cybersecurity controls. AI-based predictive maintenance reduces service interruptions by nearly 20%, while cloud printing adoption has exceeded 40% among large enterprises. These technologies improve fleet visibility, reduce administrative workload, and strengthen document security.

Advanced toner formulations, automated calibration systems, and energy-efficient imaging technologies are improving print consistency and operating efficiency. New-generation laser systems deliver approximately 15% lower energy consumption compared with older models through optimized fixing technologies. Compared with traditional printer management, intelligent platforms improve operational monitoring by nearly 30%, giving enterprise users faster troubleshooting and better cost control.

Between 2026 and 2028, competitive advantage will increasingly depend on software integration, cybersecurity, and automation rather than hardware specifications alone. HP, Canon, Xerox, and Ricoh benefit from established enterprise ecosystems, while technology-focused providers gain opportunities through workflow partnerships. Companies investing in connected platforms, AI-enabled diagnostics, and sustainable components are positioned to capture demand from modern workplaces.

September 2024 Canon expanded its laser printer portfolio with new imageCLASS models designed for small offices and hybrid workplaces. The lineup included multifunction devices with speeds up to 35 pages per minute, improving productivity for enterprise users. Source: www.usa.canon.com

December 2024 Canon India introduced 10 new printer models across PIXMA and imageCLASS series, targeting SMB and enterprise users with enhanced connectivity and productivity features. Several laser models offered print speeds above 33 pages per minute, strengthening workplace automation capabilities. Source: www.in.canon.com

October 2025 Xerox introduced the Proficio Production Series at PRINTING United, integrating automation, AI-assisted intelligence, and advanced imaging technologies. The launch strengthened Xerox’s production color printing ecosystem and improved workflow efficiency for commercial print providers. Source: www.investors.xerox.com

June 2025 Xerox showcased workflow automation and digital color enhancement solutions at Amplify Print 2025, highlighting personalized printing technologies and integrated production ecosystems. The company focused on helping print providers improve operational efficiency through automation-driven solutions.

The Colored Laser Printer Market Report covers comprehensive analysis across product types, applications, end-users, regional markets, and emerging technology trends shaping enterprise printing ecosystems. The report evaluates multifunction printers, single-function printers, and connected printing solutions across corporate offices, healthcare, education, government, and commercial sectors.

The study provides strategic insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa markets, including adoption patterns, deployment models, competitive positioning, and innovation trends. It examines cloud printing, AI-enabled management, cybersecurity integration, and sustainable printing technologies influencing market direction. The report supports investment planning, expansion strategies, supplier evaluation, and competitive decision-making by analyzing evolving customer requirements and technology-driven transformation between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,529.0 Million |

| Market Revenue (2033) | USD 8,798.8 Million |

| CAGR (2026–2033) | 3.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | HP Inc.; Canon Inc.; Brother Industries Ltd.; Xerox Holdings Corporation; Ricoh Company Ltd.; Kyocera Corporation; Seiko Epson Corporation; Lexmark International Inc.; Konica Minolta Inc.; Sharp Corporation; Fujifilm Business Innovation Corporation; Toshiba Tec Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |