Reports

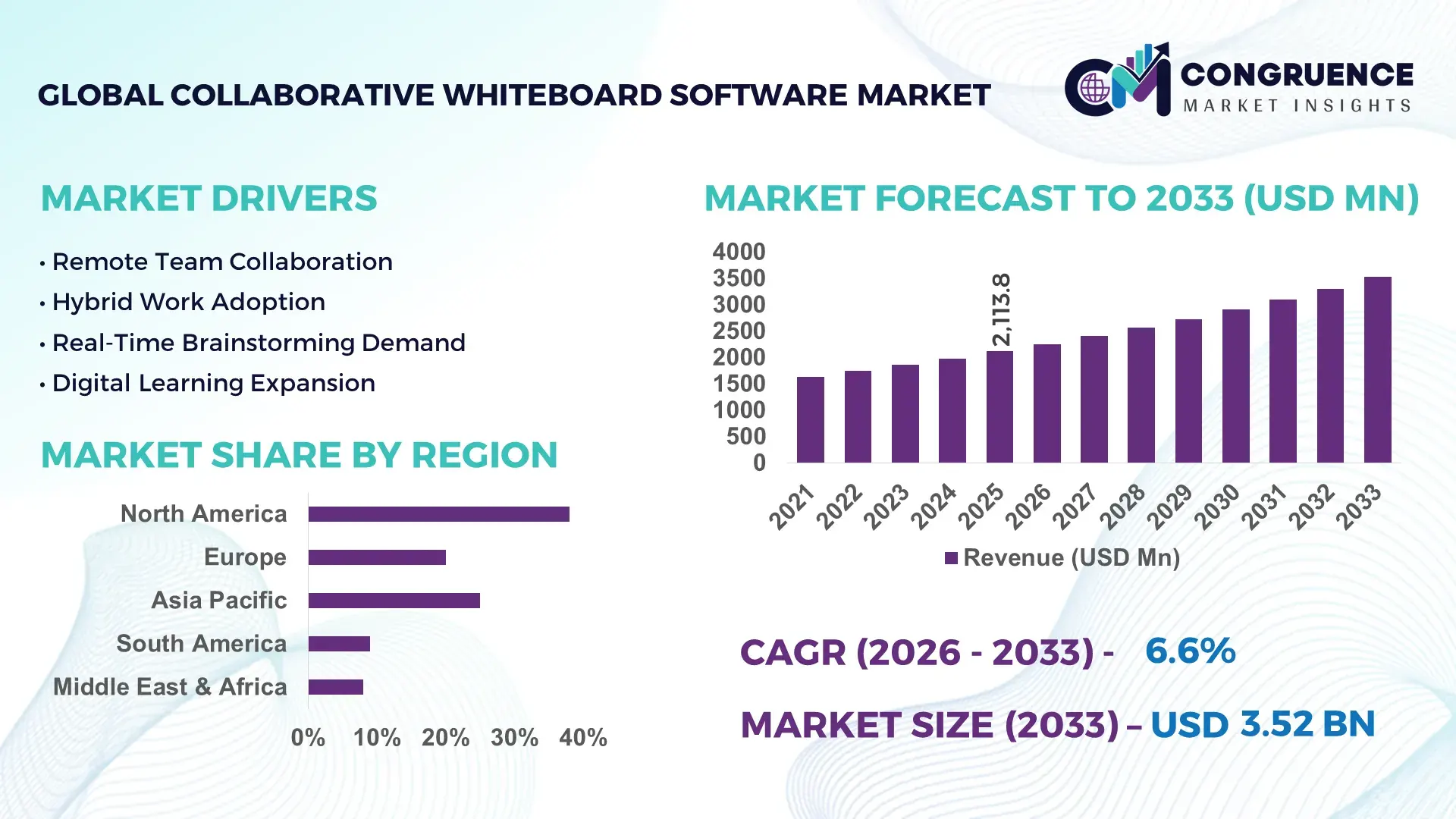

The Global Collaborative Whiteboard Software Market was valued at USD 2113.81 Million in 2025 and is anticipated to reach a value of USD 3524.72 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033.

Enterprise-wide hybrid collaboration strategies, AI-assisted visual workflow automation, and rising integration of whiteboard platforms with project management ecosystems accelerated enterprise deployment rates by over 28% across technology, education, consulting, and BFSI sectors during 2025. Between 2024 and 2026, global enterprises intensified digital workplace investments following stricter cross-border data governance requirements and rising distributed workforce models, while Asia-Pacific software procurement expanded due to regional cloud infrastructure localization initiatives and post-pandemic operational restructuring.

The United States maintained market leadership with nearly 34% global platform adoption share in 2025, supported by over USD 2.1 billion in enterprise collaboration software investments and strong penetration across IT services, higher education, and healthcare networks. More than 61% of Fortune 1000 firms integrated collaborative whiteboard applications into daily workflow orchestration and virtual brainstorming systems, compared with approximately 39% adoption across emerging Southeast Asian enterprises. Large-scale AI integration programs and advanced cybersecurity frameworks further strengthened enterprise-grade deployment, while federal digital modernization programs accelerated secure cloud collaboration adoption across public institutions.

Organizations prioritizing scalable visual collaboration ecosystems with AI-driven workflow intelligence and compliance-ready infrastructure are positioned to gain faster cross-functional productivity, lower meeting cycle time, and stronger distributed innovation capabilities.

Market Size & Growth: USD 2113.81 Million in 2025 rising toward USD 3524.72 Million by 2033 at 6.6% CAGR, driven by enterprise hybrid-work expansion and AI-powered workflow collaboration adoption.

Top Growth Drivers: Hybrid workforce deployment expanded 31%, cloud collaboration integration increased 27%, and AI-assisted visual productivity usage surged 36% during 2025.

Short-Term Forecast: By 2027, enterprises are projected to reduce remote meeting coordination time by 24% and improve project visualization efficiency by 29% through advanced whiteboard ecosystems.

Emerging Technologies: AI summarization tools, real-time multilingual collaboration, and embedded workflow automation improved task completion speed by nearly 33% across digital enterprises.

Regional Leaders: North America surpassed USD 980 Million with strong enterprise SaaS penetration, Europe crossed USD 620 Million through regulated digital workplace adoption, and Asia-Pacific exceeded USD 710 Million due to rapid cloud infrastructure expansion.

Consumer/End-User Trends: Nearly 58% of enterprise teams adopted persistent digital brainstorming environments, while education-sector collaborative usage increased 41% between 2024 and 2025.

Pilot/Case Example: In 2025, a multinational consulting deployment reduced project ideation cycles by 26% after integrating AI-enabled whiteboard software into distributed workflow systems.

Competitive Landscape: Leading vendors collectively controlled approximately 46% market share, with strong competition focused on AI integration, workflow analytics, and enterprise-grade cybersecurity capabilities.

Regulatory & ESG Impact: Data localization and compliance modernization policies increased secure cloud collaboration investments by 22%, especially across Europe and Asia-Pacific operational hubs.

Investment & Funding: Global collaboration software investments exceeded USD 3.4 billion during 2025, supported by strategic partnerships, AI expansion programs, and workplace digitization initiatives.

Innovation & Future Outlook: Next-generation collaborative whiteboard platforms are shifting toward predictive workflow intelligence, immersive visual collaboration, and integrated enterprise automation ecosystems.

Technology, education, consulting, and BFSI sectors collectively contributed more than 63% of global collaborative whiteboard software deployments in 2025, supported by rising distributed workforce management and digital training initiatives. AI-powered meeting summarization, workflow mapping, and multilingual visual collaboration tools improved enterprise productivity efficiency by nearly 30%, while Asia-Pacific demand expanded over 25% due to rapid cloud infrastructure localization. North American enterprises continued leading advanced deployment integration, whereas Europe strengthened adoption through stricter compliance-driven workplace modernization policies. Increasing integration with workflow analytics and immersive collaboration environments is expected to redefine enterprise communication strategies and accelerate long-term digital workplace transformation.

Collaborative whiteboard software is transforming from a communication utility into a core operational intelligence layer for distributed enterprises, making the market increasingly critical for investment competition and enterprise workflow modernization. Organizations integrating visual collaboration into project orchestration, product design, employee training, and agile development achieved nearly 32% faster decision-making cycles during 2025. Simultaneously, rising enterprise pressure for secure cloud collaboration and cross-border data compliance is accelerating platform consolidation and forcing vendors to optimize enterprise-grade security architecture. AI-driven collaborative systems now improve workflow efficiency by 38% while reducing manual coordination costs by 24% compared to legacy meeting and presentation systems.

North America leads in deployment volume due to large-scale enterprise digitization, while Asia-Pacific leads in innovation adoption with nearly 41% growth in AI-enabled collaboration integrations across technology and education sectors. Over the next three years, enterprise demand for persistent visual workflow platforms is projected to increase digital project completion efficiency by 27% and reduce onboarding time by 21%. ESG-focused workplace digitization strategies are also creating competitive advantages by lowering business travel dependency and reducing operational coordination costs by nearly 18%. In 2025, a multinational engineering company improved cross-border product planning accuracy by 29% after integrating AI-enabled whiteboard collaboration into hybrid design operations.

Technology vendors and enterprise software providers are rapidly shifting capital allocation toward integrated workflow ecosystems, embedded analytics, and immersive collaboration environments to secure long-term enterprise retention. Strategic partnerships between cloud infrastructure firms and productivity software developers are reshaping competitive positioning, while companies expanding AI-assisted collaboration capabilities are strengthening customer lock-in and operational scalability. Businesses prioritizing intelligent visual collaboration infrastructure are positioning themselves to dominate next-generation digital workplace transformation and enterprise productivity optimization.

Hybrid workforce expansion and enterprise workflow digitization are accelerating demand for collaborative whiteboard software across technology, consulting, education, and healthcare sectors. More than 58% of multinational enterprises integrated visual collaboration systems into daily operations during 2025, while AI-assisted workflow automation improved project coordination efficiency by 31%. Rising cross-border team structures and cloud-based operational models are forcing businesses to replace fragmented communication systems with centralized collaborative ecosystems. The rapid shift toward distributed engineering, remote training, and agile product development after global workplace restructuring significantly intensified deployment rates across North America and Asia-Pacific. In response, software providers are accelerating platform expansion, increasing AI investment, and forming strategic cloud partnerships to strengthen enterprise retention, scalability, compliance readiness, and workflow intelligence capabilities.

Data security concerns, integration complexity, and regulatory compliance pressures are constraining enterprise-scale deployment of collaborative whiteboard software. Nearly 43% of enterprises reported operational delays linked to legacy infrastructure incompatibility, while cybersecurity management costs increased by 26% across cloud collaboration ecosystems during 2025. Strict data localization frameworks across Europe and Asia-Pacific are forcing vendors to redesign storage architecture and increase regional infrastructure investments. Additionally, fragmented enterprise software environments are reducing deployment efficiency and increasing integration timelines by approximately 22%. Businesses operating in highly regulated sectors including BFSI and healthcare face elevated compliance risks related to cross-border collaboration and sensitive workflow sharing. To mitigate exposure, companies are diversifying cloud partnerships, strengthening encryption frameworks, and prioritizing interoperable platform development with enterprise-grade governance capabilities.

AI-enabled workflow intelligence and expanding digital infrastructure across emerging economies are reshaping long-term growth opportunities within the collaborative whiteboard software market. Enterprise adoption of predictive collaboration analytics increased by 34% during 2025, while automated meeting summarization tools reduced administrative workload by nearly 28%. Rapid cloud expansion across Southeast Asia, the Middle East, and Latin America is generating new demand pockets among education institutions, engineering firms, and mid-sized enterprises seeking lower operational coordination costs. The growing shift toward immersive collaboration environments and integrated project visualization platforms is creating significant competitive differentiation opportunities. In response, technology providers are accelerating R&D investment, expanding multilingual collaboration capabilities, and building ecosystem partnerships with workflow automation and cybersecurity vendors to secure future enterprise dominance and regional market expansion.

Infrastructure scalability limitations, inconsistent cross-platform performance, and rising enterprise customization demands are creating significant execution risks for collaborative whiteboard software providers. Approximately 37% of enterprises reported workflow disruption caused by latency issues and fragmented application synchronization during high-volume collaboration sessions in 2025. Increasing pressure for real-time AI processing, multilingual integration, and secure data handling is also raising infrastructure optimization costs by nearly 24%. Enterprises operating across multiple regions face operational complexity due to uneven cloud infrastructure maturity and varying regulatory requirements. These constraints are reducing deployment consistency and forcing providers to balance innovation speed with platform reliability. To remain competitive, companies must strengthen cloud partnerships, optimize low-latency architecture, accelerate cybersecurity innovation, and expand scalable enterprise support ecosystems across global markets.

AI-assisted collaboration adoption increased 36% across enterprise workflows in 2025. Organizations are embedding automated meeting summaries, intelligent task mapping, and predictive workflow suggestions directly into collaborative whiteboard environments to optimize execution speed. Enterprise users reduced manual documentation workload by 29% and shortened project review cycles by 24%. Software providers are rapidly restructuring product architecture around AI-native collaboration layers while expanding strategic cloud infrastructure partnerships to support higher processing demand and secure data governance requirements.

Cross-platform workflow integration deployments expanded 31% as enterprises consolidated productivity ecosystems. Businesses increasingly replaced fragmented communication stacks with unified collaboration environments connected to project management, CRM, and workflow automation systems. Integrated deployments improved cross-functional coordination efficiency by 27% while reducing software switching time by nearly 22%. Rising pressure to streamline distributed operations after workforce decentralization is forcing vendors to prioritize interoperability, API scalability, and embedded analytics capabilities to retain enterprise contracts and optimize operational continuity.

Asia-Pacific enterprise adoption accelerated 34% through localized cloud collaboration expansion. Regional demand shifted rapidly toward compliance-ready and multilingual collaborative whiteboard platforms, particularly across technology services and digital education sectors. Organizations reduced onboarding and training completion time by 26% using persistent visual collaboration environments. Companies are responding by expanding regional data hosting capacity, increasing localization investment, and forming channel partnerships to capture rapidly scaling enterprise procurement demand amid tightening regional data governance requirements.

Subscription-based enterprise licensing models grew 28% as operational flexibility redefined purchasing behavior. Businesses increasingly favored scalable consumption-based contracts over fixed licensing structures to optimize workforce variability and IT spending control. Flexible deployment models lowered collaboration infrastructure overhead by 19% while improving enterprise user retention rates. A non-obvious shift emerged as mid-sized firms prioritized modular collaboration suites rather than all-in-one platforms, forcing providers to redesign pricing architecture, bundle AI capabilities selectively, and accelerate customer-specific customization strategies.

The Collaborative Whiteboard Software Market is segmented by type, application, and end-user, with demand increasingly concentrating around scalable cloud collaboration and workflow-driven enterprise deployments. Cloud-based platforms accounted for nearly 57% of adoption in 2025 due to lower infrastructure dependency and stronger remote accessibility, while team collaboration and project planning applications collectively represented over 48% of platform usage. IT and telecom remained the dominant end-user segment because of high workflow integration intensity and distributed workforce operations. Demand is now shifting toward AI-enabled workflow management, online learning, and healthcare collaboration environments as organizations prioritize operational agility, secure visual coordination, and cross-platform productivity optimization across global digital workplace ecosystems.

Cloud-Based solutions dominated the Collaborative Whiteboard Software Market with approximately 57% adoption share in 2025 due to superior scalability, lower infrastructure dependency, and faster integration with enterprise productivity ecosystems. Large organizations increasingly prioritized cloud-native collaboration environments to support distributed workflows, AI-assisted project coordination, and cross-device accessibility, reducing deployment management costs by nearly 24%. Real-Time Boards emerged as the fastest-growing segment, expanding adoption by approximately 33% as enterprises accelerated demand for synchronous collaboration, agile workflow execution, and instant decision-making environments. Compared to traditional On-Premises systems, cloud-based platforms improved deployment flexibility by 31% while significantly reducing maintenance complexity. Visual Planning Tools and Presentation Boards collectively accounted for nearly 29% of total demand, maintaining strong relevance across consulting, education, and design-intensive industries requiring structured ideation and workflow visualization capabilities. Companies are increasingly reallocating product investment toward AI-enhanced cloud collaboration, low-latency synchronization, and modular deployment models, while On-Premises demand continues declining in smaller enterprises due to infrastructure inefficiencies and limited scalability. Strategic investment momentum is clearly shifting toward interoperable, AI-enabled real-time collaboration ecosystems.

“According to a 2025 report by the International Data Corporation (IDC), cloud-based collaborative workspace technologies were adopted by over 64% of large enterprises, resulting in nearly 27% improvement in workflow coordination efficiency, reinforcing their growing strategic importance.”

Team Collaboration remained the leading application segment with nearly 32% usage concentration in 2025, driven by enterprise-wide hybrid workforce management and rising demand for centralized visual communication environments. Organizations increasingly integrated collaborative whiteboard software into daily project discussions, remote operations, and agile workflow coordination to improve execution speed and reduce communication fragmentation. Workflow Management emerged as the fastest-growing application, expanding by approximately 35% as enterprises embedded AI-assisted task orchestration, automated process mapping, and cross-functional operational tracking into collaboration platforms. Compared with mature brainstorming applications, workflow management deployments demonstrated stronger operational dependency and higher enterprise retention value. Project Planning, Online Learning, and Employee Training collectively contributed around 44% of platform utilization, particularly across technology, education, and consulting sectors seeking scalable digital coordination environments. Businesses are actively repositioning collaboration software from communication utilities toward operational execution systems through deeper integration with productivity platforms and analytics tools. Demand is clearly shifting toward persistent workflow-centric collaboration environments capable of improving execution visibility, workforce alignment, and enterprise decision-making speed.

“According to a 2025 report by the World Economic Forum, workflow-centric collaboration platforms were deployed across over 120,000 enterprises globally, improving operational coordination efficiency by 30%, highlighting their rapid operational adoption.”

IT and Telecom dominated the Collaborative Whiteboard Software Market with approximately 36% usage share in 2025 due to high dependency on distributed engineering collaboration, agile development environments, and continuous workflow coordination across global teams. Large technology enterprises increasingly adopted AI-enabled collaborative platforms to streamline software planning, reduce communication latency, and improve sprint execution visibility. Education emerged as the fastest-growing end-user segment, recording nearly 34% expansion as institutions accelerated digital classroom transformation, remote learning integration, and interactive training deployment. Compared with BFSI, where adoption remains compliance-driven and security-focused, education institutions prioritized scalability, multilingual collaboration, and persistent learning engagement environments. Healthcare, Manufacturing, and Media and Entertainment collectively accounted for approximately 39% of total platform demand, supported by rising requirements for visual process coordination, remote operational planning, and cross-functional content collaboration. Companies are responding through sector-specific customization strategies, subscription flexibility, and targeted ecosystem partnerships to strengthen penetration across regulated and workflow-intensive industries. Future demand concentration is increasingly shifting toward sectors requiring secure, AI-assisted, and operationally integrated collaboration infrastructure.

“According to a 2025 report by UNESCO, adoption among education institutions increased by 38%, with over 85,000 organizations implementing collaborative digital learning platforms, leading to approximately 26% improvement in remote engagement efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

North America maintained demand leadership through large-scale enterprise collaboration deployment, advanced cloud infrastructure, and high AI integration intensity across IT, consulting, and healthcare sectors. Europe captured nearly 27% market share, driven by compliance-focused digital workplace modernization and stricter enterprise data governance frameworks. Asia-Pacific exceeded 29% demand contribution as enterprises accelerated cloud collaboration adoption across education, telecom, and digital services industries. While North America leads in enterprise-scale deployment, Asia-Pacific is reshaping innovation speed through localized SaaS expansion and lower operational scaling costs. Increasing regional data localization policies and distributed workforce expansion are forcing vendors to establish localized infrastructure partnerships. Global companies are prioritizing AI-enabled cloud collaboration expansion across Asia-Pacific while reinforcing compliance and enterprise security capabilities in North America and Europe.

North America held approximately 38% of the Collaborative Whiteboard Software Market in 2025, supported by strong enterprise SaaS penetration and large-scale hybrid workforce integration across IT, consulting, healthcare, and education sectors. More than 64% of large enterprises integrated visual collaboration platforms into workflow orchestration and agile project management environments, improving cross-functional execution efficiency by nearly 29%. Rising cybersecurity compliance expectations and stricter enterprise data governance frameworks are accelerating demand for secure AI-enabled collaboration ecosystems. Companies are rapidly expanding cloud infrastructure partnerships and embedding workflow analytics into collaboration suites to strengthen enterprise retention. Businesses increasingly prioritize scalable, interoperable, and automation-driven platforms, making North America a critical region for premium enterprise deployment, advanced AI integration, and long-term digital workplace transformation investment.

Europe accounted for nearly 27% of global Collaborative Whiteboard Software Market demand in 2025, led by Germany, the United Kingdom, and France through strong enterprise digital transformation programs. Regulatory pressure surrounding data sovereignty, cross-border collaboration governance, and ESG-focused workplace optimization is reshaping enterprise purchasing behavior across the region. More than 52% of enterprises prioritized compliance-ready collaboration platforms with localized data hosting and advanced encryption capabilities, while AI-assisted workflow management adoption increased by approximately 24%. Organizations are shifting toward secure cloud collaboration systems to reduce operational inefficiencies and support hybrid workforce continuity. Vendors are responding through regional infrastructure expansion, multilingual platform optimization, and compliance-focused product customization. Europe continues forcing innovation around secure enterprise collaboration architecture and operational transparency standards.

Asia-Pacific represented nearly 29% of Collaborative Whiteboard Software Market demand in 2025 and emerged as the fastest-scaling regional market due to rapid enterprise digitization across China, India, Japan, and Southeast Asia. Expanding cloud infrastructure investment, lower deployment costs, and accelerating remote workforce integration strengthened enterprise adoption across telecom, education, and technology sectors. More than 41% of regional deployments focused on AI-enabled collaboration environments supporting multilingual workflow coordination and real-time project execution. Enterprises reduced operational communication delays by approximately 26% through persistent visual collaboration ecosystems. Vendors are aggressively expanding regional cloud partnerships, localized SaaS deployment models, and low-cost enterprise subscription structures to capture volume-driven demand. Asia-Pacific remains strategically critical for scale expansion, operational agility, and high-speed enterprise collaboration adoption.

South America contributed approximately 8% of global Collaborative Whiteboard Software Market demand in 2025, with Brazil and Argentina leading regional enterprise adoption across education, financial services, and consulting industries. Rising digital workplace transformation and remote workforce expansion accelerated collaborative software deployment by nearly 22% during 2025. However, uneven cloud infrastructure maturity and enterprise IT budget constraints continue limiting large-scale implementation speed across mid-sized businesses. Organizations increasingly favor subscription-based deployment models and modular collaboration tools to reduce operational expenditure and improve workforce coordination flexibility. Vendors are responding through localized pricing strategies, channel partnerships, and lightweight cloud deployment solutions optimized for regional infrastructure conditions. South America presents strong long-term expansion potential, although companies must balance affordability, scalability, and infrastructure limitations to capture sustainable market growth.

Middle East & Africa accounted for nearly 6% of Collaborative Whiteboard Software Market demand in 2025, supported by rising digital infrastructure investment across the UAE, Saudi Arabia, and South Africa. Enterprise collaboration adoption accelerated across construction, oil and gas, education, and government modernization projects seeking faster project coordination and remote operational visibility. More than 28% of regional enterprises increased investment in cloud-based collaboration systems to support workforce decentralization and digital transformation initiatives. Governments and large enterprises are actively deploying AI-enabled collaboration environments to improve project execution speed and reduce administrative workflow inefficiencies by approximately 19%. Vendors are expanding regional cloud partnerships and localized enterprise support operations to strengthen deployment accessibility. The region is emerging as a strategic market for infrastructure-led digital collaboration transformation and enterprise modernization investment.

United States – Holds approximately 34% market share in the Collaborative Whiteboard Software market due to large-scale enterprise SaaS adoption, advanced AI integration, and strong hybrid workforce infrastructure.

China – Accounts for nearly 18% market share in the Collaborative Whiteboard Software market driven by rapid cloud collaboration deployment, expanding digital enterprise ecosystems, and aggressive workplace digitization initiatives.

The Collaborative Whiteboard Software Market is dominated by global enterprise collaboration providers competing against workflow-focused SaaS innovators and regional cloud productivity specialists. Leading players including Microsoft, Miro, Google, Cisco, and Zoom collectively controlled nearly 49% market share in 2025 through integrated ecosystem expansion and AI-driven workflow optimization. Competition is increasingly centered on interoperability, enterprise security, workflow automation, and low-latency collaboration performance, with AI-enabled productivity features improving enterprise retention rates by approximately 27%. Vendors are aggressively expanding API integration capabilities, forming cloud infrastructure partnerships, and embedding analytics-driven collaboration intelligence to strengthen operational differentiation. The competitive landscape is rapidly shifting from standalone visual collaboration tools toward integrated enterprise workflow ecosystems. Rising compliance costs, infrastructure scaling requirements, and enterprise customization demands are creating significant entry barriers for smaller providers. Winning in this market now requires scalable AI integration, enterprise-grade security architecture, ecosystem interoperability, and high-speed deployment execution across distributed workforce environments.

Microsoft Corporation

Miro

Cisco Systems, Inc.

Google LLC

Zoom Communications, Inc.

Lucidspark

Mural

Stormboard

Conceptboard

Bluescape

Creately

FigJam

InVision

Explain Everything

AI-assisted collaboration engines are reshaping enterprise whiteboard platforms through automated meeting summaries, workflow mapping, multilingual translation, and predictive task recommendations. During 2025, more than 46% of enterprise collaboration deployments integrated generative AI capabilities to reduce manual coordination workload and accelerate project execution. AI-enabled workflow systems improved collaboration efficiency by nearly 38% while lowering operational coordination costs by 24% compared to legacy presentation-centric platforms. Businesses are increasingly embedding whiteboard environments into project management, CRM, and communication ecosystems to optimize execution continuity and reduce software fragmentation across distributed teams.

Emerging technologies between 2026 and 2028 are accelerating adoption of real-time visual intelligence, immersive collaboration interfaces, and AI-driven workflow orchestration. Persistent collaborative environments integrated with low-latency cloud synchronization improved enterprise task completion speed by approximately 31%, while automated diagram generation reduced process documentation time by nearly 27%. Enterprises deploying AI-native visual collaboration platforms achieved stronger operational scalability than organizations relying on standalone whiteboarding tools. Technology providers are rapidly scaling API interoperability, cloud infrastructure partnerships, and advanced analytics integration to strengthen enterprise retention and competitive differentiation.

Disruptive innovation is increasingly centered on collaborative AI agents, immersive workspace ecosystems, and contextual workflow automation. AI-first collaboration platforms are transforming visual workspaces into operational execution systems capable of automating strategic planning, resource alignment, and knowledge management workflows. Organizations investing early in AI-integrated collaboration infrastructure are strengthening cross-functional productivity, improving workforce responsiveness, and securing long-term competitive advantages as enterprise workplace digitization accelerates globally.

October 2024 – Cisco launched Webex AI Agent and AI Assistant enhancements to strengthen intelligent collaboration and workflow automation capabilities across enterprise communication environments. The deployment improved customer interaction efficiency by nearly 39%, accelerating enterprise demand for AI-driven operational collaboration tools and expanding Cisco’s AI-focused enterprise ecosystem positioning. [AI Workflow Shift] Source: Cisco Newsroom

May 2024 – Microsoft introduced advanced Copilot agent capabilities across Microsoft 365 collaboration environments, enabling automated workflow orchestration, intelligent task management, and enterprise process automation. The update strengthened AI-assisted collaboration adoption across enterprise teams and accelerated operational productivity optimization through integrated AI-driven workplace execution systems. [Enterprise AI Expansion] Source: Microsoft 365 Blog

January 2026 – Miro expanded its AI Innovation Workspace with collaborative AI agents, workflow automation layers, and enterprise AI administration controls. The platform strengthened AI workflow integration across enterprise collaboration environments, while advanced analytics and moderation capabilities improved organizational visibility and AI governance efficiency across distributed enterprise teams. [AI Workspace Scaling] Source: Miro Help Center

March 2026 – Miro launched AI Workflows with Sidekicks and Flows, enabling real-time AI-assisted visual collaboration and automated deliverable generation inside enterprise whiteboard environments. The deployment accelerated enterprise workflow execution and strengthened AI-native collaboration adoption across education, consulting, and product development operations requiring faster project coordination and structured execution visibility. [Workflow Automation Push] Source: Miro AI Workflows Overview

The Collaborative Whiteboard Software Market report delivers comprehensive analysis across core product types including Cloud-Based, On-Premises, Real-Time Boards, Visual Planning Tools, and Presentation Boards, while evaluating key applications such as Team Collaboration, Workflow Management, Online Learning, and Employee Training. The report covers major end-user industries including IT and Telecom, BFSI, Education, Healthcare, Manufacturing, and Media and Entertainment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Advanced technology assessment includes AI-assisted collaboration engines, workflow automation, immersive collaboration systems, multilingual coordination tools, and cloud-native enterprise integration environments shaping operational transformation between 2026 and 2033.

The study analyzes more than 25 strategic market indicators, including enterprise adoption patterns, deployment intensity, workflow efficiency improvements, and regional demand concentration. Cloud-based deployment environments accounted for nearly 57% of enterprise usage, while AI-integrated workflow collaboration adoption exceeded 46% across large organizations during 2025. The report profiles leading collaboration technology providers and evaluates competitive positioning, infrastructure strategies, ecosystem expansion, and enterprise integration capabilities. Strategic insights support investment prioritization, regional expansion planning, product positioning, partnership development, and long-term enterprise collaboration transformation decisions within the rapidly evolving digital workplace ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2113.81 Million |

|

Market Revenue in 2033 |

USD 3524.72 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, Miro, Cisco Systems, Inc., Google LLC, Zoom Communications, Inc., Lucidspark, Mural, Stormboard, Conceptboard, Bluescape, Creately, FigJam, InVision, Explain Everything |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |