Reports

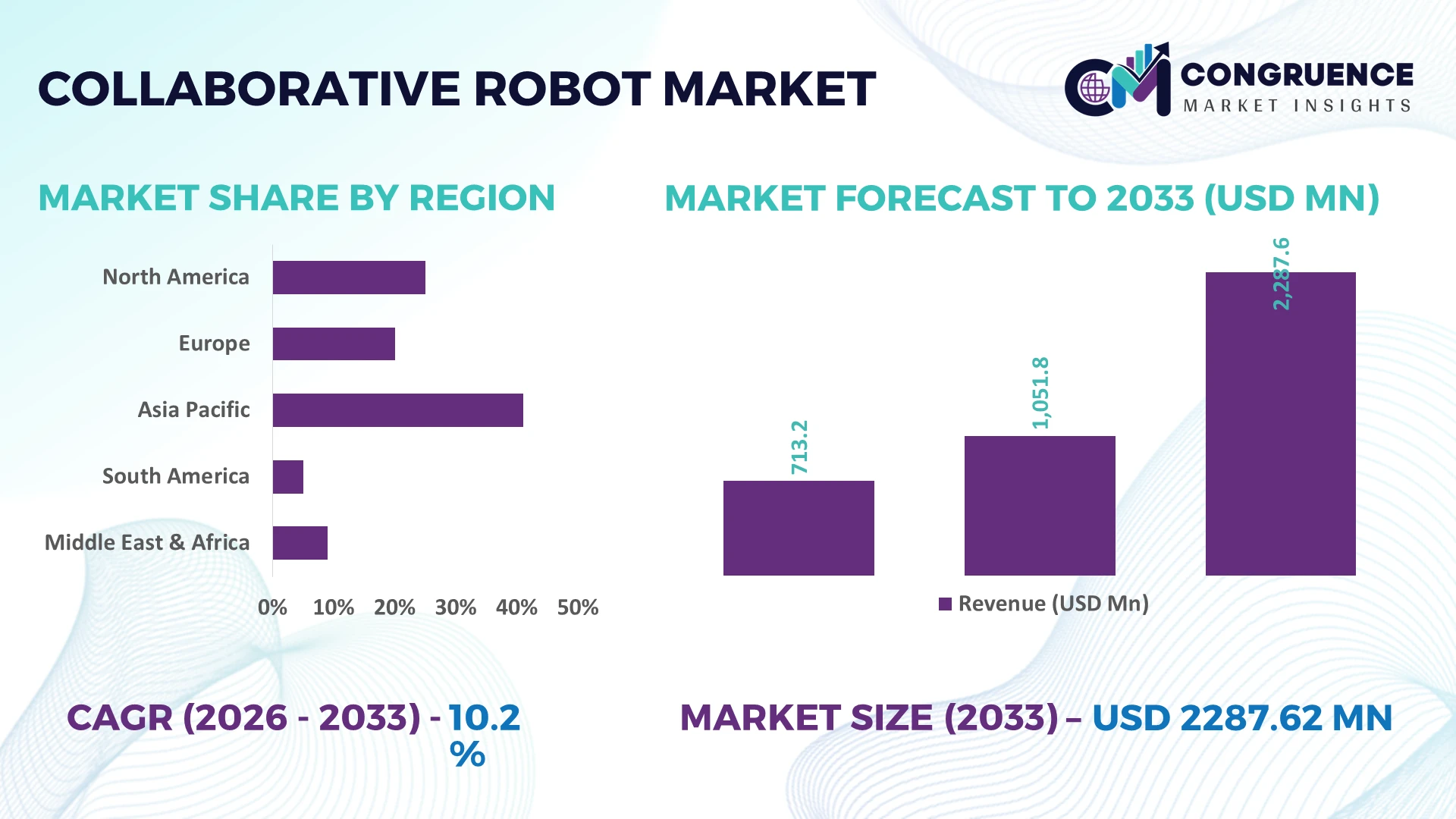

The Global Collaborative Robot Market was valued at USD 1051.79 Million in 2025 and is anticipated to reach a value of USD 2287.62 Million by 2033 expanding at a CAGR of 10.2% between 2026 and 2033. Growth is driven by accelerated smart factory deployment, AI-enabled robot programming, labor shortages, and increasing adoption of flexible automation across electronics, automotive, healthcare, logistics, and precision manufacturing.

China dominates the global collaborative robot market with approximately 42% of worldwide installations, supported by large-scale manufacturing investments, expanding domestic robot production, and strong electronics and automotive sectors. Japan follows with advanced industrial automation and higher robot density exceeding 390 industrial robots per 10,000 manufacturing employees, while ongoing supply chain diversification beyond East Asia continues to strengthen regional manufacturing resilience in 2026.

Businesses investing in AI-integrated collaborative robotics, localized production, and scalable automation platforms are positioned to achieve stronger operational efficiency and long-term competitive advantage.

Market Size & Growth: USD 1051.79 Million (2025) to USD 2287.62 Million (2033) at 10.2% CAGR, driven by AI-enabled automation and flexible manufacturing expansion.

Top Growth Drivers: AI adoption (+35%), labor shortages (+28%), smart factory investments (+31%) accelerate collaborative robot deployment globally.

Short-Term Forecast: By 2028, deployment reduces production changeover time by nearly 30% while improving assembly efficiency by over 22%.

Emerging Technologies: AI vision, digital twins, and edge computing improve programming speed by nearly 40% and boost operational flexibility.

Regional Leaders: Asia-Pacific leads above USD 1.0 Billion, Europe exceeds USD 520 Million, North America approaches USD 470 Million with rapid warehouse automation expansion.

Consumer/End-User Trends: More than 55% of new manufacturing automation projects integrate collaborative robots alongside existing production systems.

Pilot/Case Example: 2026 electronics assembly deployment improved production throughput by 26% while reducing manual quality defects by 18%.

Competitive Landscape: Universal Robots holds approximately 35% market share alongside ABB, FANUC, KUKA, and Doosan Robotics.

Regulatory & ESG Impact: Energy-efficient automation lowers operational energy consumption by around 15% while supporting workplace safety compliance.

Investment & Funding: More than USD 2 Billion supports robotics expansion through manufacturing capacity, partnerships, and advanced AI integration amid supply chain localization.

Innovation & Future Outlook: AI-powered autonomous programming, mobile collaborative robots, and cloud-connected automation strengthen high-growth industrial productivity strategies.

Collaborative Robot Market demand continues expanding across electronics assembly, automotive manufacturing, pharmaceutical production, logistics, and food processing as manufacturers prioritize flexible automation and rapid deployment. AI-powered vision systems and intuitive no-code programming accelerate implementation, while over 60% of new installations emphasize human-robot collaboration. Supply-chain regionalization and evolving industrial safety requirements further reinforce strategic investment, setting the stage for deeper competitive and operational analysis.

Collaborative robots are becoming a strategic manufacturing asset as companies prioritize production flexibility, workforce resilience, and localized operations. Supply-chain restructuring since recent global disruptions has accelerated investments in modular automation that can be deployed without major factory redesign. Manufacturers increasingly integrate collaborative robots to support high-mix, low-volume production while reducing dependence on manual processes. More than 60% of new automation projects now emphasize human-robot collaboration to improve productivity without replacing existing production infrastructure.

Modern AI-enabled collaborative robots complete programming and deployment up to 45% faster than conventional industrial robotic cells while reducing integration costs by nearly 30% through intuitive software and sensor-based safety systems. China continues leading deployment through electronics and automotive manufacturing, whereas Germany emphasizes precision engineering and advanced machine integration for high-value production. Over the next two to three years, AI-assisted programming, machine vision, and cloud-based fleet management are expected to increase average robot utilization by approximately 20% across medium-sized manufacturing facilities.

Automotive component manufacturers increasingly deploy collaborative robots for machine tending, inspection, and packaging, improving production consistency while lowering changeover time. Leading suppliers are expanding AI capabilities, forming software partnerships, and strengthening localized manufacturing footprints to support customer-specific automation requirements. Companies that combine intelligent robotics with digital manufacturing platforms will secure stronger operational resilience, higher production agility, and durable competitive positioning.

Persistent labor shortages, increasing product customization, and digital factory modernization are accelerating collaborative robot adoption across manufacturing. AI-powered vision systems improve inspection accuracy by nearly 35%, while automated programming reduces deployment time by approximately 40% and production downtime by over 20%. China's industrial modernization initiatives and expanding electronics manufacturing ecosystem continue supporting large-scale automation investment. Manufacturers are responding by expanding collaborative robot portfolios, investing in intelligent software platforms, and partnering with industrial automation providers to deliver integrated production solutions. A notable strategic shift is the growing transition from fixed automation toward flexible robotic cells capable of supporting multiple production lines, enabling faster product launches and improving factory utilization without extensive capital-intensive infrastructure changes.

Despite strong adoption momentum, deployment remains constrained by integration complexity, skilled engineering shortages, and dependence on precision components. Nearly 30% of small manufacturers require significant production-line modifications before collaborative robot implementation, while advanced sensors and motion-control components account for almost 25% of total system costs. Semiconductor supply fluctuations and specialized actuator sourcing continue affecting delivery schedules in Japan and other manufacturing hubs. Companies are mitigating these pressures by localizing component procurement, adopting standardized communication protocols, and negotiating long-term supplier agreements. Organizations that prioritize modular integration architectures reduce deployment disruption while improving operational scalability and lowering lifecycle maintenance requirements across multiple production facilities.

The strongest opportunities extend beyond hardware into AI-enabled automation ecosystems, predictive maintenance, and robotics-as-a-service business models. Cloud-connected collaborative robots can improve equipment utilization by over 25%, while predictive analytics reduce unplanned downtime by approximately 30%. India is rapidly expanding industrial automation across electronics manufacturing and warehouse operations, supported by digital manufacturing initiatives and rising domestic production investments. Companies are increasing R&D spending, developing industry-specific software platforms, and establishing technology partnerships to deliver scalable automation packages. An important strategic opportunity lies in combining collaborative robots with autonomous mobile robots, creating integrated production and logistics workflows that significantly improve factory responsiveness without major infrastructure expansion.

Achieving enterprise-wide deployment remains challenging because collaborative robots must operate seamlessly across diverse software platforms, legacy equipment, and cybersecurity frameworks. More than 40% of manufacturers identify interoperability as a primary deployment challenge, while cybersecurity incidents targeting industrial control systems have increased by over 20% in recent years. Germany's advanced manufacturing facilities increasingly require secure data exchange between robotic systems and digital production platforms, raising compliance and operational complexity. Companies must invest in standardized industrial communication protocols, workforce upskilling, and secure edge-computing infrastructure while strengthening technology partnerships. Organizations that successfully integrate secure, interoperable robotics ecosystems will establish long-term operational consistency, manufacturing resilience, and sustainable competitive differentiation.

AI-Powered Shopfloor Intelligence: Manufacturers are integrating AI vision, adaptive motion control, and machine learning into collaborative robots, improving inspection accuracy by nearly 35% and reducing programming time by about 40%. Labor shortages and digital manufacturing initiatives are accelerating deployment, particularly in China and Germany. Companies are expanding software partnerships and embedding edge AI to deliver faster commissioning, lower engineering effort, and more autonomous production workflows.

Modular Automation Deployment Expands: Enterprises increasingly favor modular collaborative robot cells that can be reconfigured across production lines, reducing line changeover time by approximately 30% and lowering installation effort by over 25%. Electronics manufacturers are restructuring production to support shorter product cycles, while automation suppliers are introducing standardized hardware interfaces and scalable robotic platforms to simplify multi-site deployment and improve factory responsiveness.

Cloud-Connected Robot Operations: Connected robot fleets are becoming standard across high-volume manufacturing, with cloud monitoring increasing equipment utilization by around 20% and predictive maintenance reducing unexpected downtime by nearly 28%. Growing industrial cybersecurity requirements are encouraging companies to deploy secure edge computing alongside centralized fleet management. Vendors are strengthening digital service portfolios and long-term software support to improve operational continuity and lifecycle performance.

Human-Centric Production Integration: Collaborative robots are moving beyond repetitive assembly into inspection, packaging, and machine tending, increasing operator productivity by roughly 22% while reducing ergonomic risks by over 30%. Aging workforces and stricter workplace safety expectations are accelerating this transition. Companies are redesigning production workflows, investing in employee upskilling, and deploying intuitive no-code programming tools that allow operators to reconfigure robotic tasks without specialized engineering expertise.

Articulated Robots represent the largest segment due to their flexibility, multi-axis movement, and compatibility with assembly, inspection, palletizing, and machine-tending operations. They account for approximately 48% of collaborative robot deployments because manufacturers prioritize versatile automation across diverse production environments. Mobile Robots are the fastest-growing type as factories increasingly integrate autonomous material transport with collaborative workstations, improving internal logistics efficiency by nearly 30%. Dual-Arm Robots are expanding in precision electronics assembly where synchronized manipulation improves productivity, while SCARA Robots remain preferred for compact high-speed pick-and-place applications. Cartesian Robots continue serving cost-sensitive linear automation requirements where repeatability and straightforward integration remain priorities.

Manufacturers are expanding articulated robot portfolios while investing in AI-enabled mobile platforms and modular software architectures that simplify deployment across multiple facilities. Product innovation increasingly emphasizes sensor fusion, simplified programming, and interoperability, shifting investment toward intelligent robotic ecosystems rather than standalone hardware.

Assembly remains the leading application because collaborative robots enable consistent precision, flexible production, and rapid product changeovers without extensive production-line modifications. More than 45% of deployments support assembly processes across automotive and electronics manufacturing. Machine tending is emerging as the fastest-growing application as manufacturers automate repetitive loading and unloading tasks, improving equipment utilization by approximately 25% while reducing idle machine time. Packaging applications continue expanding within food and consumer goods industries, whereas inspection benefits from AI-powered vision systems capable of improving defect detection by nearly 35%. Material handling maintains stable demand as factories optimize internal workflow efficiency.

Technology providers are expanding application-specific software, end-effectors, and vision systems to accelerate deployment while reducing customization requirements. Strategic partnerships with machine builders and system integrators are strengthening turnkey automation offerings, allowing enterprises to scale collaborative robotics across multiple operational processes with reduced implementation complexity.

Automotive remains the dominant end-user because vehicle manufacturers require highly flexible automation for welding support, assembly, inspection, and component handling across complex production lines. Approximately 38% of collaborative robot deployments are concentrated within automotive manufacturing, supported by continuous factory modernization. Logistics is the fastest-growing end-user as warehouse automation and fulfillment operations expand, increasing collaborative robot utilization by nearly 32% for picking, sorting, and palletizing. Electronics continues adopting collaborative systems for precision assembly, while healthcare benefits from laboratory automation and pharmaceutical handling. Food & Beverage manufacturers prioritize hygienic automation, and broader manufacturing industries increasingly deploy collaborative robots to address workforce shortages and improve operational consistency.

Suppliers are introducing industry-specific robotic solutions, customized software, and integrated service packages while expanding channel partnerships to strengthen adoption across diverse industrial sectors. Investment priorities increasingly favor scalable platforms capable of supporting multiple production environments with minimal engineering intervention.

Asia-Pacific accounted for the largest market share at 51.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 12.4% CAGR between 2026 and 2033.

Advanced Manufacturing and AI Automation Integration

North America maintains a strong position through advanced manufacturing modernization, high labor costs, and widespread deployment of intelligent automation across automotive, electronics, logistics, and healthcare industries. The region represents approximately 22% of global collaborative robot deployments, supported by increasing AI integration and factory digitalization. More than 65% of newly commissioned manufacturing automation projects now incorporate collaborative robotic systems alongside existing production assets. Major enterprises continue expanding partnerships with software providers and automation integrators to improve production flexibility, reduce engineering time, and strengthen domestic manufacturing resilience through localized automation investments.

United States Market Outlook: The United States leads the regional market through extensive manufacturing infrastructure, advanced robotics software development, and strong investment in smart factories. Automotive, aerospace, semiconductor, and logistics industries continue accelerating collaborative robot deployment, while AI-enabled robotic programming shortens commissioning time across production facilities. More than half of North America's collaborative robot installations are concentrated in the United States, supported by increasing investments in domestic semiconductor manufacturing and warehouse automation that reinforce long-term industrial competitiveness.

Precision Manufacturing and Sustainable Factory Modernization

Europe remains a technology-driven collaborative robot market where precision manufacturing, industrial digitalization, and sustainability targets shape deployment priorities. The region contributes nearly 21% of global installations, supported by strong automotive, machinery, pharmaceutical, and electronics production. Manufacturers increasingly deploy energy-efficient collaborative robots capable of lowering production energy consumption by approximately 15% while improving operational flexibility. Industrial automation suppliers continue strengthening partnerships with machine builders and software companies to deliver standardized robotic solutions compatible with evolving European manufacturing requirements.

Germany Market Outlook: Germany serves as Europe's collaborative robotics hub through its globally competitive automotive, industrial machinery, and engineering sectors. Smart manufacturing initiatives continue accelerating AI-enabled robotic deployment across medium-sized and large enterprises. Factory operators increasingly combine collaborative robots with digital twins and industrial IoT platforms, while high robot density and continuous investment in advanced manufacturing technologies strengthen Germany's position as the region's leading innovation and deployment center.

Manufacturing Scale and Automation Leadership

Asia-Pacific dominates the collaborative robot market through unmatched manufacturing capacity, expanding electronics production, and government-supported industrial automation programs. The region accounts for approximately 51.8% of global market activity, driven by large-scale deployment across automotive, semiconductor, consumer electronics, and precision engineering industries. Manufacturing investments continue supporting new robotic production facilities, while localized supply chains improve equipment availability and deployment speed. AI-powered collaborative robots are increasingly replacing conventional automation systems to improve production flexibility and support shorter product development cycles across export-oriented industries.

China Market Outlook: China remains the largest national market due to its extensive electronics manufacturing ecosystem, automotive production capacity, and expanding domestic robotics industry. Approximately 42% of worldwide collaborative robot installations are concentrated in China, supported by continuous smart factory investment and industrial modernization initiatives. Domestic manufacturers are increasing AI integration, improving robotic software capabilities, and expanding production capacity to reduce import dependence while strengthening global competitiveness across industrial automation markets.

Industrial Modernization Supports Automation Demand

South America is gradually expanding collaborative robot adoption as manufacturers modernize production facilities and improve operational efficiency across automotive, food processing, packaging, and consumer goods industries. The region represents approximately 4% of global deployment activity, with increasing automation investment focused on productivity improvements rather than large-scale factory replacement. Several industrial operators have reduced manual production tasks by nearly 18% through phased collaborative robot implementation. Companies increasingly prioritize modular robotic systems that can be integrated into existing manufacturing environments without significant infrastructure redevelopment.

Brazil Market Outlook: Brazil leads the regional market through its diversified manufacturing base, automotive production, food processing industry, and expanding logistics infrastructure. Industrial enterprises continue investing in flexible automation to improve production quality while addressing workforce availability challenges. Manufacturing companies are strengthening partnerships with robotics integrators and automation suppliers to accelerate deployment across assembly and packaging operations, supporting gradual but consistent adoption of collaborative robotic technologies.

Industrial Diversification and Smart Infrastructure Investment

Middle East & Africa is emerging as a high-priority market as governments accelerate industrial diversification, advanced manufacturing, and logistics modernization initiatives. Although current deployment levels remain comparatively modest, investments in industrial infrastructure and smart manufacturing continue increasing across strategic sectors. Manufacturing modernization projects have improved automated production capacity by nearly 20% within selected industrial zones, while international automation providers are expanding regional partnerships to support local implementation capabilities. Growth is increasingly supported by digital transformation strategies and industrial policy initiatives rather than traditional manufacturing expansion alone.

Saudi Arabia Market Outlook: Saudi Arabia leads regional collaborative robot adoption through industrial diversification programs, advanced manufacturing investments, and logistics infrastructure expansion. Automotive component manufacturing, warehousing, and food production facilities are increasingly deploying collaborative robotics to improve operational efficiency and workforce productivity. Government-backed industrial development initiatives continue encouraging technology localization, while partnerships with international automation providers strengthen technical expertise and accelerate deployment across strategically important manufacturing sectors.

The competitive landscape is led by Universal Robots, ABB, FANUC, KUKA, and Doosan Robotics, while regional manufacturers in China compete aggressively on pricing and localized customization. Global automation leaders compete against cost-focused domestic suppliers, whereas robotics software innovators challenge traditional OEMs through AI-enabled programming and digital integration. The top five companies collectively control approximately 68% of global market activity. Competition centers on deployment speed, AI capabilities, interoperability, and lifecycle support rather than hardware alone. AI-assisted programming reduces commissioning time by nearly 40%, modular robot platforms lower integration costs by about 30%, and predictive maintenance improves equipment availability by approximately 25%. Companies are expanding manufacturing capacity, acquiring software expertise, strengthening channel partnerships, and vertically integrating sensors, controllers, and cloud platforms to secure customer retention. The market is shifting toward intelligent automation ecosystems where software increasingly differentiates vendors. High certification requirements, application engineering expertise, and industrial integration capabilities remain significant entry barriers. Sustainable competitive advantage depends on delivering scalable AI-driven automation, rapid deployment, secure connectivity, and strong aftermarket service.

Universal Robots

ABB

FANUC

KUKA

Doosan Robotics

Techman Robot

Yaskawa Electric Corporation

Kawasaki Heavy Industries

Epson Robots

Omron Corporation

Elite Robots

Franka Robotics

AUBO Robotics

Hanwha Robotics

Collaborative robotics technology is rapidly shifting from standalone automation toward intelligent, connected production platforms. AI-powered machine vision, force sensing, and edge computing now enable collaborative robots to perform adaptive assembly, inspection, and machine tending with approximately 35% higher accuracy while reducing programming effort by nearly 40% compared with conventional teach-pendant systems. More than 60% of newly deployed collaborative robots incorporate integrated vision or AI-assisted programming, allowing manufacturers to shorten commissioning cycles and improve production flexibility across multiple product variants.

Emerging technologies include digital twins, cloud fleet management, predictive maintenance, and no-code programming interfaces that reduce unexpected downtime by around 30% while increasing equipment utilization by approximately 20%. AI-native robotics platforms increasingly replace legacy rule-based automation because they adapt to changing production conditions without extensive reconfiguration. Automotive, electronics, and logistics operators gain the strongest competitive advantage by combining collaborative robots with industrial IoT and autonomous material handling systems to create synchronized manufacturing workflows.

Between 2026 and 2028, multimodal AI, advanced robotic perception, secure edge intelligence, and collaborative mobile robotics will redefine factory automation. Vendors investing in software ecosystems, cybersecurity, and interoperable architectures will outperform hardware-focused competitors by enabling faster deployment, continuous optimization, and scalable automation across distributed manufacturing networks. Organizations acting now will strengthen operational resilience, improve workforce productivity, and establish long-term competitive differentiation.

May 2025 Universal Robots introduced the UR15 collaborative robot featuring a maximum TCP speed of 5 m/s, delivering up to 30% faster cycle times for pick-and-place applications, enabling manufacturers to improve throughput while lowering automation costs across high-volume production environments.

June 2025 Universal Robots launched UR Studio, an online simulation platform that enables manufacturers to validate robot cells before deployment, helping optimize workflows and calculate cycle times digitally, reducing commissioning risks and accelerating production planning across industrial automation projects. Source: nasdaq.com

July 2025 ABB expanded its China robotics portfolio with three new robot families targeting mid-sized manufacturers, addressing a domestic market projected to grow by 8% annually, strengthening localized production capabilities and widening automation access across electronics, food processing, and metals industries. Source: reuters.com

March 2026 Universal Robots partnered with Scale AI to launch the UR AI Trainer, enabling AI-driven robot training through imitation learning and high-fidelity industrial data collection, significantly accelerating deployment of intelligent robotic applications while strengthening next-generation factory automation capabilities. Source: universal-robots.com

The report provides a comprehensive assessment of the collaborative robot market across major robot types, applications, end-user industries, and regional markets between 2026 and 2033. It evaluates articulated, SCARA, Cartesian, dual-arm, and mobile robots, covering deployment across assembly, machine tending, inspection, packaging, and material handling. The analysis spans automotive, electronics, healthcare, logistics, food & beverage, and broader manufacturing sectors, where more than 60% of new automation projects increasingly integrate collaborative robotics into existing production environments.

The study delivers strategic insights into AI-enabled robotics, machine vision, edge computing, cloud connectivity, digital twins, and intelligent software ecosystems shaping industrial automation. It compares competitive positioning, technology adoption, deployment trends, investment priorities, and regional manufacturing dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report supports product strategy, market entry, expansion planning, partnership evaluation, supply-chain optimization, and long-term competitive decision-making by identifying emerging deployment models, operational priorities, and high-potential industrial opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1051.79 Million |

Market Revenue in 2033 | USD 2287.62 Million |

CAGR (2026 - 2033) | 10.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Universal Robots, ABB, FANUC, KUKA, Doosan Robotics, Techman Robot, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Epson Robots, Omron Corporation, Elite Robots, Franka Robotics, AUBO Robotics, Hanwha Robotics |

Customization & Pricing | Available on Request (10% Customization is Free) |