Reports

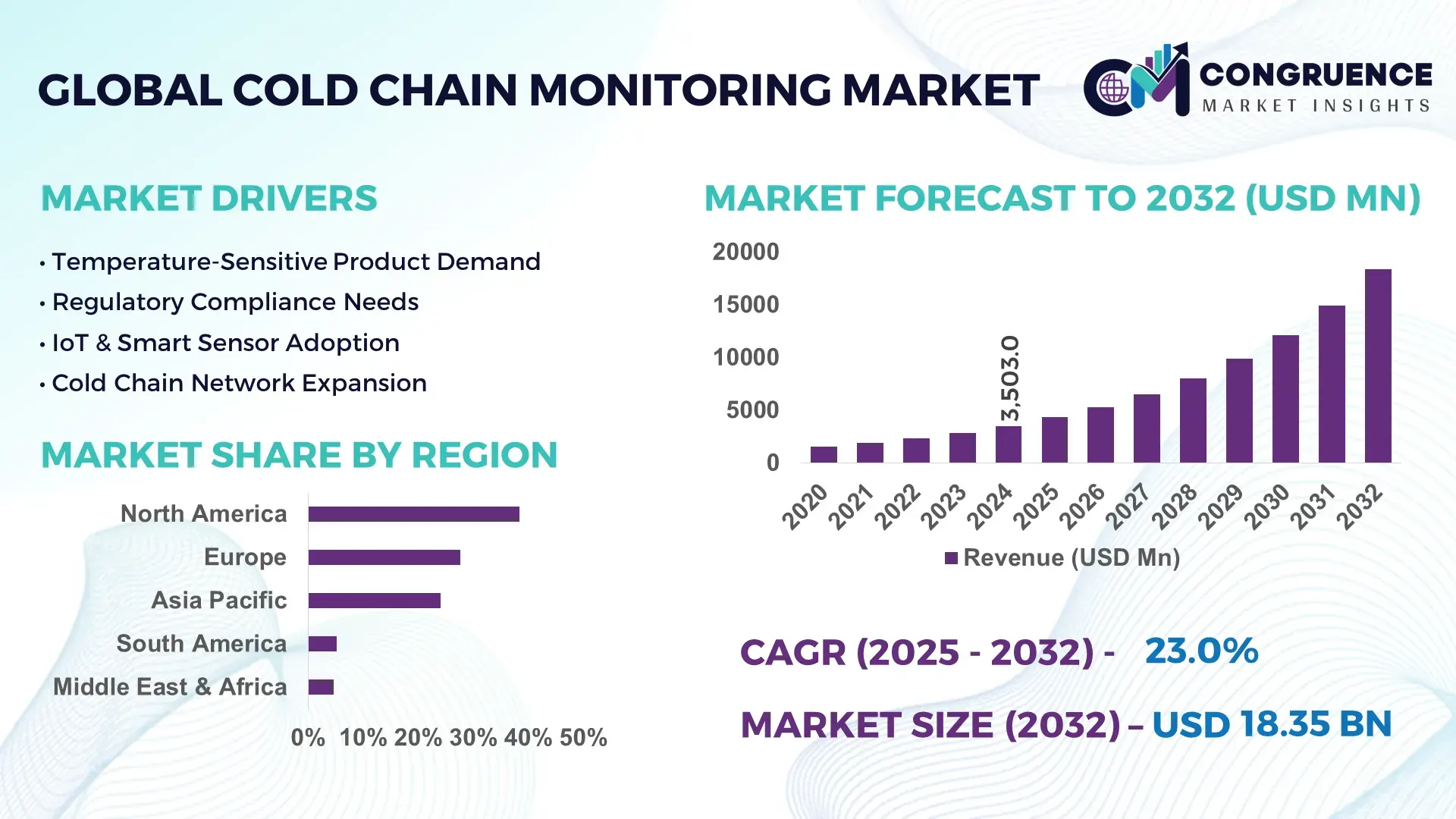

The Global Cold Chain Monitoring Market was valued at USD 3,503.0 Million in 2024 and is anticipated to reach USD 18,351.9 Million by 2032, expanding at a CAGR of 23.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. This strong growth is driven by the rapid expansion of temperature-sensitive pharmaceutical and food supply chains worldwide.

The United States plays a pivotal role in advancing cold chain monitoring technologies through high-capacity biopharmaceutical manufacturing, robust investments in end-to-end temperature-controlled logistics infrastructure, and early adoption of sensor-driven tracking systems. The country deploys more than 420 million sq. ft. of refrigerated warehousing, supports over 65% penetration of real-time IoT-based monitoring in pharmaceutical distribution, and invests consistently in RFID-enabled validation systems, ensuring superior reliability and traceability across mission-critical cold chain applications.

Market Size & Growth: Valued at USD 3.50 Billion in 2024, projected to reach USD 18.35 Billion by 2032, expanding at 23.0% CAGR due to rising requirements for temperature-sensitive biopharmaceutical and food logistics.

Top Growth Drivers: 58% adoption of IoT-enabled trackers; 42% improvement in logistics efficiency; 37% growth in temperature-controlled pharmaceuticals.

Short-Term Forecast: By 2028, operational deviation incidents are expected to reduce by 28% through automation and predictive alert systems.

Emerging Technologies: Integration of blockchain-enabled traceability and AI-based predictive temperature monitoring reshaping reliability standards.

Regional Leaders: North America projected to reach USD 6.2 Billion by 2032; Europe to reach USD 4.7 Billion; Asia-Pacific to exceed USD 5.1 Billion with accelerated infrastructure modernization.

Consumer/End-User Trends: High adoption across biopharma, frozen foods, and clinical diagnostics, with rising multi-sensor usage patterns for quality assurance.

Pilot or Case Example: In 2026, a national logistics pilot using automated IoT sensors reported a 31% drop in spoilage events.

Competitive Landscape: Market leader holds approximately 12% share, followed by major players specializing in sensors, cloud platforms, and integrated tracking.

Regulatory & ESG Impact: Strengthened temperature-compliance guidelines and sustainability incentives improving cold chain efficiency and environmental performance.

Investment & Funding Patterns: Over USD 1.4 Billion invested recently in cold chain digitalization and sensor-technology advancements globally.

Innovation & Future Outlook: Advancements in multi-modal monitoring, autonomous data capture, and real-time analytics expected to shape next-generation cold chain systems.

Growing adoption across biopharma, diagnostics, and frozen food industries—supported by smart sensors, remote monitoring platforms, digital compliance tools, and regional investments—continues to strengthen the Cold Chain Monitoring Market. Technology improvements, sustainability standards, and rising consumption of temperature-sensitive goods are driving future demand and shaping global deployment strategies.

The strategic relevance of the Cold Chain Monitoring Market is increasing rapidly as industries depend more heavily on uninterrupted temperature-controlled logistics to safeguard high-value pharmaceutical, biologics, food, and diagnostic products. Modern supply chains require precise, real-time monitoring to mitigate spoilage, reduce operational risks, and ensure regulatory compliance. Current systems demonstrate quantifiable improvements in reliability, with AI-enabled predictive monitoring delivering up to 48% better temperature-deviation prevention compared to legacy data-logger-based models. North America dominates in volume due to its large biopharmaceutical manufacturing ecosystem, while Europe leads in adoption with over 61% enterprises integrating real-time monitoring across end-to-end cold chain operations.

By 2028, AI-supported automation is expected to improve shipment-level anomaly detection by 32%, reducing losses and unplanned interventions. The market is also influenced by ESG commitments, with firms targeting 25–30% reductions in cold-chain energy consumption by 2030 through optimized refrigeration, efficient route planning, and eco-friendly materials. In 2027, a large logistics operator in East Asia achieved a 27% improvement in temperature compliance through an integrated IoT-AI initiative across regional warehousing centers.

Collectively, these developments position the Cold Chain Monitoring Market as a foundational enabler of resilient global supply chains, improved regulatory adherence, operational continuity, and sustainable long-term growth.

The Cold Chain Monitoring Market is shaped by increasing demand for precise temperature control, advanced digitalization of supply chain operations, and stringent regulatory frameworks governing the distribution of pharmaceuticals, vaccines, diagnostics, and perishable foods. Market dynamics reflect rapid adoption of IoT sensors, cloud-based analytics, and predictive monitoring technologies that help identify deviations and reduce operational failures. Growth is further supported by rising consumption of frozen and chilled products, expansion of biopharmaceutical manufacturing, and cross-border cold-chain trade. Meanwhile, efficiency, traceability, and compliance continue to define investment priorities for global stakeholders in the Cold Chain Monitoring Market.

The global increase in biologics, vaccines, and specialty pharmaceuticals requiring controlled temperature conditions is significantly strengthening demand for cold chain monitoring solutions. More than 70% of new biologic therapies require refrigerated or deep-freeze handling, necessitating end-to-end monitoring throughout distribution. The expansion of clinical trials, where over 55% involve temperature-sensitive materials, further accelerates the need for precise tracking. Real-time data analytics and multi-sensor validation systems help minimize risk, improve compliance accuracy, and ensure the integrity of sensitive medical shipments, making monitoring technologies indispensable across pharmaceutical logistics.

Cold chain monitoring adoption is restricted in many regions due to limited availability of advanced storage, inadequate power infrastructure, and high deployment costs for sensor-based systems. More than 30% of emerging markets report insufficient refrigerated warehousing capacity, which affects monitoring equipment integration. Challenges related to inconsistent connectivity, underdeveloped logistics networks, and limited technical expertise also slow adoption. In addition, interoperability issues across platforms and varying regional regulatory expectations increase complexity, creating operational inefficiencies that hinder widespread deployment of monitoring technologies.

Rapid digitalization in logistics networks is creating significant opportunities for advanced cold chain monitoring integration. The use of IoT-enabled devices, cloud-based data platforms, and AI-driven predictive systems is projected to expand substantially, as over 64% of logistics providers plan to implement automation technologies within the next five years. High growth in e-grocery, frozen meal kits, and temperature-sensitive healthcare products opens new applications for multi-sensor monitoring. Data standardization, blockchain adoption, and end-to-end visibility platforms also create new revenue opportunities for technology and service providers in the Cold Chain Monitoring Market.

The Cold Chain Monitoring Market faces challenges from escalating regulatory requirements, increasing temperature-control validation needs, and the growing complexity of multi-modal supply chains. Compliance with international standards requires precise documentation and real-time deviation reporting, adding operational strain. Additionally, refrigeration energy consumption can account for up to 60% of total operating costs in cold storage facilities, creating economic pressure. Ensuring interoperability between monitoring systems, maintaining 24/7 uptime, and managing large data volumes pose further technical hurdles, making scalability and reliability major concerns for industry operators.

Advanced IoT Penetration Transforming Monitoring Accuracy: The integration of next-generation IoT sensors has increased precision tracking by 45%, enabling real-time data capture across large fleets and warehousing units. More than 52% of new deployments now include multi-parameter monitoring, significantly improving anomaly detection across food and pharmaceutical shipments.

Growth of AI-Driven Predictive Monitoring Models: AI-based analytics platforms have boosted failure-prediction accuracy by up to 41%, allowing operators to intervene before temperature excursions occur. Usage of automated decision systems grew 37% between 2022 and 2024, especially in high-volume biologics distribution.

Expansion of Energy-Efficient Refrigeration Systems: New-generation refrigeration systems utilizing automated load optimization achieved 23% reductions in energy consumption. Regions with advanced regulatory frameworks, such as Europe, report over 48% adoption of environmentally efficient cold-storage infrastructure.

Rise in Modular and Prefabricated Construction: Modular and prefabricated systems are increasingly used in cold-chain infrastructure, with 55% of new projects reporting cost advantages. Automated prefabrication has reduced labor requirements by 30% and shortened project timelines, particularly in North America and Europe where high-precision building standards are critical.

The Cold Chain Monitoring Market is structured across three core dimensions—type, application, and end-user—which collectively define adoption patterns, technology investment, and operational deployment models. Sensor-based monitoring platforms account for the largest share across type categories due to rising compliance requirements in pharmaceutical, food, and clinical logistics. Applications span pharmaceuticals, food & beverages, chemicals, and agriculture, each with unique temperature-control demands shaped by product handling sensitivity and distribution complexity. End-user adoption is expanding rapidly among logistics service providers, healthcare entities, and food distributors, supported by higher utilization of automated monitoring platforms and integration with real-time analytics. Across segments, digitization, regulatory enforcement, and multi-sensor adoption remain prominent drivers influencing segmentation evolution.

The Cold Chain Monitoring Market encompasses hardware, software, and services, each playing a critical role in ensuring temperature integrity across supply chains. Hardware solutions lead the segment with approximately 46% share, driven by widespread adoption of temperature sensors, data loggers, RFID tags, and telematics units. Their dominance stems from increased shipment-level tracking requirements and regulatory mandates for continuous monitoring of biologics and perishable goods. In comparison, software platforms account for around 29%, enabling cloud integration, analytics dashboards, and automated alerts. Meanwhile, monitoring services represent 25%, covering installation, calibration, validation, and managed monitoring support. The fastest-growing category is software solutions, supported by rising digitization and advanced analytics integration. This segment is expanding at an estimated 18% growth rate, propelled by demand for predictive insights, interoperability with logistics systems, and AI-driven deviation detection. While hardware maintains the highest adoption, software is gaining traction due to real-time visibility requirements across global distribution networks. The combined share of remaining subcategories—including niche equipment, hybrid platforms, and specialized payload sensors—accounts for nearly 11%, offering targeted solutions for unique operational environments.

The Cold Chain Monitoring Market covers several key applications, including pharmaceuticals, food & beverages, chemicals, and agriculture. Pharmaceutical logistics leads the market with nearly 49% share, supported by growing biologics distribution, stringent temperature-compliance frameworks, and expanded vaccine transport requirements. In contrast, the food & beverages segment holds around 33%, reflecting rising demand for frozen and chilled foods worldwide. However, adoption within the chemical and specialty materials segment—currently at 18% combined share—is growing rapidly as companies standardize temperature tracking for sensitive solvents, reagents, and industrial bioproducts. The fastest-growing application is pharmaceutical distribution, expanding at an estimated 19% rate, driven by increasing reliance on biologics, cell therapies, and personalized medicines that require strict thermal protection. Comparatively, food & beverage monitoring adoption is rising steadily but at a slower pace, with new regulatory compliance rules prompting systematic digital monitoring. Consumer adoption trends also reinforce sector growth: In 2024, more than 38% of global enterprises reported piloting cold chain digital systems for quality assurance, while over 54% of consumers in developed markets preferred brands offering traceable cold-chain certification for perishable foods.

End-user adoption in the Cold Chain Monitoring Market spans logistics service providers, pharmaceutical companies, food distributors, retailers, and healthcare institutions. Logistics service providers represent the leading segment with about 41% share, driven by high shipment volumes, large refrigerated fleets, and increasing adherence to global temperature-compliance standards. Pharmaceutical manufacturers and healthcare institutions collectively account for 34%, supported by wide-scale integration of monitoring platforms to protect biologics, diagnostics, and critical therapeutic products. Food distributors contribute around 25%, aligning with rising consumption of frozen foods, meal kits, and chilled retail products. The fastest-growing end-user category is pharmaceutical companies and healthcare providers, expanding at nearly 18% growth, supported by rising clinical trial logistics, stricter compliance requirements, and increased biologics production. Logistics providers remain dominant but display slower proportional growth due to early-stage market maturity. The combined share of remaining end-user groups—including specialty chemicals, agricultural exporters, and research institutions—reaches around 12%, reflecting niche but important adoption clusters. Global adoption behavior continues to shift: In 2024, approximately 39% of enterprises piloted automated cold-chain visibility tools, and over 62% of healthcare buyers expressed preference for suppliers offering validated temperature-tracking certifications.

North America accounted for the largest market share at 38.4% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 26.2% between 2025 and 2032.

The dominance of North America is attributed to its advanced cold chain logistics, high adoption of IoT-enabled monitoring devices, and strong regulatory enforcement around temperature-sensitive pharmaceuticals. The region also benefits from the presence of major logistics, biotechnology, and food distribution companies that collectively manage over 1.9 million refrigerated transport units across the U.S. and Canada. Meanwhile, Asia Pacific is becoming the fastest-evolving market, driven by the massive expansion of e-commerce grocery delivery, rising pharmaceutical manufacturing capacity, and the development of more than 500 new cold storage facilities across China, India, and Southeast Asia since 2020. Europe follows closely with a 27.6% share in 2024, benefiting from stringent food safety laws and rapid digitalization of logistics operations. South America and the Middle East & Africa collectively account for below 10%, yet both regions are witnessing structural improvements in transport, warehousing, and cross-border trade, further accelerating investment in cold chain monitoring systems.

The North America cold chain monitoring market held an estimated 38.4% share in 2024, supported by its mature refrigerated transport network, high vaccine distribution volume, and strong adoption of digital tracking solutions across the U.S. and Canada. Key industries driving demand include biopharmaceuticals, frozen and processed foods, agriculture, and high-value chemical transport. Recent regulatory updates from the FDA and USDA have strengthened temperature-control compliance, increasing investments in active monitoring systems, RFID-based tracking, and cloud-integrated logistics platforms. Technological advancements such as 5G-enabled trackers, predictive analytics, and AI-driven route optimization are rapidly transforming operational efficiency. Local players such as Orbcomm continue expanding their IoT solutions portfolio, integrating real-time sensor data for fleets and storage units. Consumer behavior in North America reflects higher enterprise adoption in healthcare and food retail, where transparency, safety compliance, and end-to-end traceability are considered essential. This combination of regulatory enforcement, technology maturity, and strong industrial demand positions North America as the most advanced regional market.

Europe accounts for approximately 27.6% of the global cold chain monitoring market in 2024, driven by strong activity across Germany, the UK, France, Italy, and the Netherlands. These markets benefit from established logistics networks, centralized pharmaceutical distribution hubs, and strict safety and environmental regulations. The European Food Safety Authority (EFSA) and EU Green Deal policies have compelled logistics providers to adopt energy-efficient refrigeration systems and real-time monitoring technologies. Emerging technologies such as IoT-integrated pallets, automated warehouse robots, digital twins, and blockchain-based traceability solutions are seeing rapid adoption. Local regional players, including Sensitech EMEA, are expanding their smart sensor portfolio to help enterprises maintain strict compliance during cross-border movement. Consumer behavior in Europe is strongly influenced by regulatory pressure, leading to high demand for transparent, traceable, and sustainable cold chain operations. This focus on compliance, sustainability, and advanced digitalization continues to push Europe toward innovation-driven leadership in the global market.

Asia Pacific represents the fastest-growing cold chain monitoring market, ranking first in expansion pace and holding roughly 24.1% of global volume in 2024. Rapid growth is driven by increasing consumption in China, India, Japan, South Korea, and Southeast Asia. Massive pharmaceutical production capacity, rising vaccine distribution, growing frozen food demand, and rapid expansion of e-commerce grocery platforms are reshaping cold chain infrastructure. Countries such as China and India together operate more than 70% of the region’s cold storage capacity, while Japan leads in advanced refrigerated transport. Innovation hubs in Singapore, Shenzhen, and Tokyo are accelerating adoption of AI-driven monitoring systems, drone-based cold delivery, and IoT-integrated warehousing. Local players such as Blue Star (India) are actively expanding temperature-controlled logistics solutions across new urban and rural corridors. Consumer behavior in Asia Pacific is heavily influenced by e-commerce-driven purchasing, mobile-first digital tracking expectations, and preference for faster delivery of perishable goods. These dynamics collectively reinforce the region’s role as the fastest-growing global market.

South America held approximately 5.2% of the global market in 2024, with Brazil and Argentina accounting for more than 70% of regional demand. The region’s growth is strongly influenced by infrastructure modernization, agricultural exports, meat processing industries, and expanding pharmaceutical distribution networks. Brazil continues investing in energy-efficient refrigerated warehouses and transport fleets, while Argentina is upgrading its cold storage facilities supporting dairy and seafood exports. Government incentives for cross-border trade, especially through Mercosur, are enhancing adoption of digital tracking technologies. Local logistics providers such as FríoMóvil (Brazil) are integrating real-time temperature sensors and route monitoring tools to reduce spoilage and optimize fleet operations. Consumer behavior trends indicate rising dependence on online grocery platforms and increased preference for safe, traceable food deliveries. Although the regional share is smaller, continuous investment in logistics and government-supported trade reforms is accelerating market growth.

The Middle East & Africa accounted for an estimated 4.7% share in 2024, supported by expanding demand from pharmaceuticals, food & beverage, agriculture, and oil & gas logistics. Key growth countries include the UAE, Saudi Arabia, South Africa, and Kenya, where investments in refrigerated warehousing, cross-border distribution, and advanced logistics parks are rising sharply. Technological modernization initiatives include IoT-enabled reefer trucks, smart warehouse management systems, and solar-powered cold storage units suited for remote regions. Governments are strengthening regulations for food import safety, pharmaceutical handling, and temperature-controlled transport compliance. Local players such as RSA Logistics (UAE) are deploying cloud-connected monitoring systems to enhance real-time traceability. Consumer behavior in the region emphasizes fresh food availability, safety standards, and reliability of imported perishables, making monitoring technology essential. These advancements continue to support MEA’s steady growth trajectory within the global market.

United States – 32.5% Market Share: Strong dominance due to advanced logistics infrastructure, high pharmaceutical distribution volume, and rapid integration of IoT-based cold chain monitoring solutions.

China – 18.2% Market Share: Leadership supported by massive food and vaccine production capacity, aggressive expansion of cold storage facilities, and increasing adoption of digital traceability systems.

The global Cold Chain Monitoring Market reflects a moderately fragmented competitive structure, with an estimated 30–40 active players offering diverse hardware, software, and integrated IoT monitoring solutions. The market is dominated by mid-sized and emerging technology firms rather than a few global giants, resulting in healthy competition and continuous innovation. The top five companies collectively account for approximately 13–16% of the global market share, indicating significant room for both established and niche players to expand.

Companies are increasingly strengthening their market positions through strategic acquisitions, partnerships, sensor innovation, and data-driven visibility platforms. Many firms are investing heavily in multi-sensor IoT devices, cloud-based analytics, GPS tracking, and AI-enabled prediction models to reduce spoilage risks and ensure compliance with global temperature-control standards. Another competitive trend is the development of low-power wireless sensor networks, enabling long-range, real-time monitoring for cross-border pharmaceutical and food shipments.

Several players are also advancing plug-and-play monitoring kits, designed for SMEs and emerging markets, where infrastructure limitations require scalable and affordable solutions. Increasing regulatory scrutiny across pharmaceuticals, perishable foods, and biologics is pushing firms to integrate automated documentation, traceability workflows, and compliance dashboards. These capabilities are further intensifying competition as companies differentiate through analytics quality, interoperability, and accuracy of real-time alerts.

Sensitech, Inc.

Cold Chain Technologies

Controlant hf.

Testo SE & Co. KGaA

Technological advancements are accelerating the evolution of the Cold Chain Monitoring Market, with modern solutions focusing on accuracy, interoperability, and end-to-end visibility across temperature-sensitive supply chains. IoT-enabled sensors remain foundational and are being deployed in higher densities across warehouses, reefer containers, trucks, and last-mile delivery units. These sensors track temperature, humidity, vibration, GPS location, and shock events in real time, ensuring product integrity from origin to final delivery.

Cloud-based platforms now aggregate millions of data points, allowing logistics firms and manufacturers to visualize cold-chain conditions through interactive dashboards. Predictive analytics, powered by machine learning models, helps forecast potential temperature excursions and equipment failures. This reduces spoilage risk and enhances compliance in pharmaceutical and food logistics. Connectivity technologies — including 4G/5G cellular, LPWAN systems such as LoRaWAN, and satellite links — support monitoring across remote or geographically dispersed routes.

Advanced software suites increasingly include automated compliance documentation, critical for industries governed by strict temperature-control regulations. Smart packaging innovations, such as sensor-embedded parcels and multi-use data loggers, support last-mile visibility in e-commerce and small-batch pharmaceutical delivery. Integration with blockchain-based traceability is emerging to enhance data integrity and chain-of-custody transparency.

Wireless sensor networks, modular hardware components, and unified cold-chain management suites are enabling scalable deployments tailored to enterprise and SME needs. These technologies collectively position cold-chain monitoring as a central component of modern, data-driven logistics infrastructure.

In March 2025, Carrier (through its subsidiary Sensitech) launched Lynx FacTOR, a device-agnostic SaaS platform for pharmaceutical cold-chain monitoring. The platform automates product release evaluation, consolidates disparate data sources, and allows batch stability and temperature-excursion compliance assessments in minutes instead of days — significantly accelerating release cycles and enhancing operational efficiency in pharma cold-chain logistics.

In May 2023, ORBCOMM rolled out the RT-8000 telematics device for refrigerated fleets in Europe. The RT-8000 is compliant with EN 12830 standards and supports multiple embedded SIMs and wireless sensors. It enhances fleet connectivity, enables richer and faster data collection (temperature, location, fuel, maintenance), and strengthens compliance and cargo integrity for refrigerated transport operations.

In August 2024, Controlant formed a strategic partnership with a thermal-packaging and simulation firm to combine real-time IoT data (temperature, location) with lane-risk and thermal-packaging modeling. This collaboration enables pharmaceutical manufacturers to make data-driven, sustainable decisions for packaging and distribution, optimizing safety and environmental footprint while reducing over-engineering.

In 2024, several cold-chain monitoring device providers launched multi-sensor, long-duration data-loggers and wireless monitoring platforms capable of supporting temperature, humidity, shock and environmental tracking for extended shipments or storage durations. These innovations expand the scope of monitoring to multi-modal logistics (storage, transport, last-mile) and improve visibility for perishable goods and biologics across global supply chains.

The Cold Chain Monitoring Market Report offers a comprehensive and structured evaluation of global temperature-controlled logistics monitoring systems. The scope covers product types such as sensors, data loggers, RFID devices, telematics units, software analytics platforms, and fully managed monitoring services. It includes detailed segmentation by application, encompassing pharmaceuticals, food and beverages, chemicals, biotechnology, agriculture, and perishable goods logistics. End-user coverage spans logistics service providers, pharmaceutical manufacturers, food processors, retailers, healthcare institutions, and cold-storage operators.

Geographically, the report assesses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting differences in infrastructure readiness, regulatory stringency, and adoption of digital cold-chain technologies. The scope also includes insights into transport-based monitoring (reefer trucks, containers, rail units) and storage-based systems (cold warehouses, distribution hubs), offering clarity on operational variations across segments.

The report further examines technology adoption patterns, including IoT sensor proliferation, cloud-based visibility platforms, multi-parameter monitoring, predictive analytics, and smart packaging. Emerging areas — such as wireless sensor networks, blockchain traceability, automation-driven cold storage, and modular monitoring solutions for SMEs — are incorporated to broaden the strategic relevance. Competitive dynamics, strategic developments, and innovation trends are evaluated to guide decision-makers in investment planning, vendor selection, and long-term capability building across the cold-chain ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,503.0 Million |

| Market Revenue (2032) | USD 18,351.9 Million |

| CAGR (2025–2032) | 23.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ORBCOMM, Digi International, Zebra Technologies Corp., Sensitech, Inc., Cold Chain Technologies, Controlant hf., Testo SE & Co. KGaA |

| Customization & Pricing | Available on Request (10% Customization Free) |