Reports

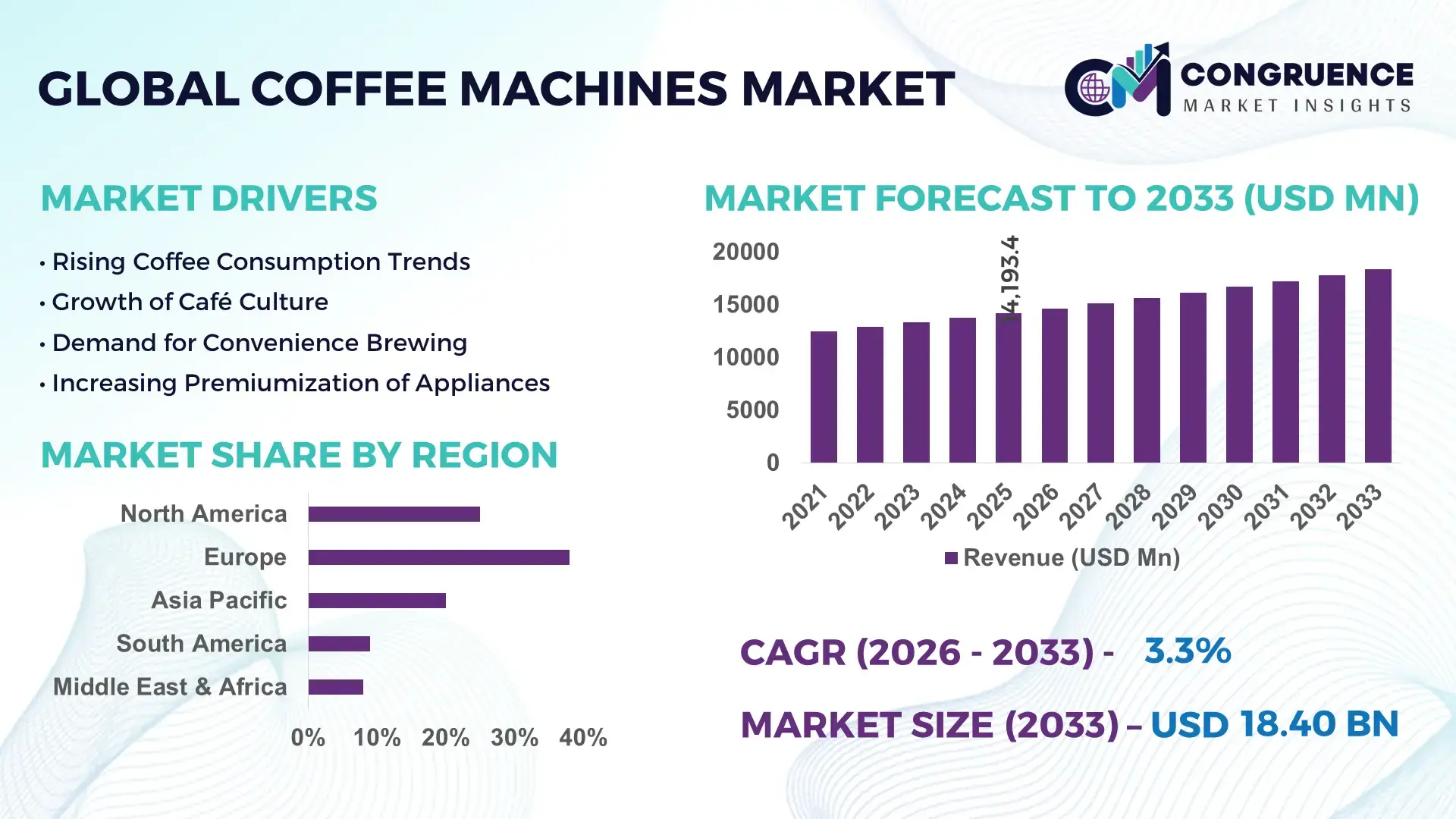

The Global Coffee Machines Market was valued at USD 14193.42 Million in 2025 and is anticipated to reach a value of USD 18403.04 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033.

Growth is firmly supported by the accelerated shift toward fully automated and IoT-enabled coffee machines, with over 29% of new installations in 2025 featuring smart connectivity that enhances operational efficiency and reduces manual intervention. Between 2024 and 2026, geopolitical trade realignments, particularly the European Union’s stricter energy efficiency mandates and ongoing global semiconductor supply constraints, have compelled manufacturers to localize production and redesign components to ensure compliance and cost stability.

Germany leads the global coffee machines market with an estimated 21% share, supported by its advanced manufacturing ecosystem and export-oriented appliance industry. The country accounts for nearly 37% of Europe’s automatic coffee machine production capacity, with investments exceeding USD 1.1 billion in smart appliance technologies between 2023 and 2025. Adoption remains robust, with approximately 47% of urban households utilizing premium coffee machines and strong penetration across office and hospitality sectors. This leadership position allows Germany to influence global pricing structures, component sourcing strategies, and innovation benchmarks, making it a critical hub for strategic manufacturing and technology alignment decisions.

Market Size & Growth: USD 14193.42 million (2025) to USD 18403.04 million (2033) at 3.3% CAGR, driven by 29% smart machine adoption across commercial environments

Top Growth Drivers: Automation integration (31%), premium appliance demand (26%), café chain expansion (22%)

Short-Term Forecast: By 2027, energy-efficient systems reduce operating costs by 15% in commercial coffee setups

Emerging Technologies: AI-driven brewing (20% efficiency gain), IoT diagnostics, and precision thermal systems transforming performance

Regional Leaders: Europe (~USD 5.8B) driven by regulation; North America (~USD 4.6B) led by office demand; Asia-Pacific (~USD 3.9B) fueled by urban café growth

Consumer Trends: 42% of users prefer bean-to-cup machines, reflecting higher demand for customization and cost efficiency

Pilot Example: In 2025, a global café chain improved service speed by 18% across 320 outlets using automated espresso systems

Competitive Landscape: Leading player holds ~17% share; key companies include De’Longhi, Jura, Philips, Breville, and Melitta

Regulatory & ESG Impact: EU policies cut standby energy consumption by 20%, reshaping product design standards

Investment & Funding: Over USD 2.2 billion invested globally (2023–2025), focusing on smart manufacturing and regional expansion

Innovation & Outlook: Modular AI-enabled machines deliver 25% higher efficiency and enable predictive maintenance capabilities

Commercial and hospitality sectors contribute approximately 46% of demand, compared to 34% from residential usage, highlighting stronger institutional purchasing cycles. Smart machines improve brew consistency by 22% versus traditional systems, while Asia-Pacific demand is expanding faster than Europe due to urban café density growth. Increasing localization amid supply chain adjustments is accelerating product customization, positioning manufacturers for region-specific competitiveness and long-term strategic advantage.

The coffee machines market is rapidly transforming into a strategic battleground where automation, energy efficiency, and user experience define competitive positioning across both commercial and residential segments. As global foodservice chains and corporate environments prioritize operational consistency, automated coffee systems are becoming essential infrastructure rather than discretionary appliances, with over 30% of new commercial installations integrating smart control features. A critical structural shift is underway as supply chains recalibrate due to semiconductor dependencies and stricter energy compliance frameworks, forcing manufacturers to redesign product architectures and localize component sourcing. AI-enabled brewing systems improve efficiency by 24% while reducing operational costs by 17% compared to legacy semi-automatic machines, fundamentally altering cost-performance benchmarks.

Regionally, Europe leads in production volume due to its established appliance manufacturing base, while Asia-Pacific leads in adoption and innovation with over 35% growth in smart machine installations driven by rapid urban café expansion. Over the next 2–3 years, machine uptime efficiency is projected to improve by 18% through predictive maintenance integration, directly enhancing service throughput in high-volume environments.

Sustainability is emerging as a measurable competitive advantage, with energy-efficient systems reducing power consumption by up to 20%, enabling compliance-driven procurement and lowering lifecycle costs. A 2025 deployment across a multinational café chain demonstrated a 19% reduction in service time through automated brewing optimization, reinforcing the operational value of advanced systems. Strategically, leading manufacturers are accelerating investments in modular, AI-integrated platforms and expanding regional production hubs, signaling a decisive shift toward scalable, technology-driven differentiation. Competitive advantage will increasingly depend on the ability to integrate efficiency, compliance, and customization into a unified product ecosystem.

The primary growth driver is the accelerating shift toward fully automated and smart coffee machines, with adoption rates surpassing 31% in commercial environments as businesses prioritize speed, consistency, and labor cost optimization. This demand is reinforced by a structural transition in the global foodservice industry, where high-volume chains are standardizing equipment to reduce service variability by up to 22%. A key global trigger has been supply chain restructuring post-2024, which pushed manufacturers to localize production and invest in modular system designs, reducing lead times by nearly 18%. The impact is clear: companies are expanding production capacity in regional hubs, accelerating capital investment in automation technologies, and forming strategic partnerships with software providers to integrate AI-driven brewing systems. This convergence of demand, supply chain adaptation, and technological advancement is redefining scalability and forcing manufacturers to reposition around high-efficiency, digitally enabled solutions.

The market faces significant constraints from component cost volatility and supply concentration, particularly in electronic control units and precision heating systems, where price fluctuations have exceeded 14% between 2024 and 2025. This dependency is intensified by global semiconductor supply limitations, which have extended production lead times by nearly 20% in certain regions. Additionally, tightening energy efficiency regulations, especially in Europe, are increasing compliance costs by approximately 12% for manufacturers redesigning legacy systems. These pressures directly impact pricing strategies, delay product rollouts, and limit scalability in cost-sensitive markets. In response, companies are actively diversifying supplier networks, entering long-term procurement contracts, and investing in alternative component technologies to reduce dependency risks. This mitigation strategy is essential to maintain production continuity while protecting margins in an increasingly regulated and cost-sensitive environment.

High-impact opportunities are emerging in AI-integrated, IoT-enabled coffee systems that enhance operational intelligence and user personalization, with smart machine penetration expected to exceed 40% in premium segments within the next few years. Advanced predictive maintenance capabilities are reducing downtime by up to 25%, offering a clear efficiency advantage for high-volume commercial users. A significant future signal lies in the integration of data analytics platforms that optimize consumption patterns, enabling cost savings of nearly 15% in large-scale deployments. Additionally, emerging markets in Asia-Pacific and Latin America are unlocking new demand pockets, driven by urbanization and rising café culture, with installation growth rates exceeding 28%. Companies are positioning aggressively through R&D investment, regional manufacturing expansion, and ecosystem partnerships that combine hardware, software, and service models. This strategic alignment is not only capturing immediate growth but also building long-term dominance through technology-led differentiation.

Execution challenges are intensifying as the market scales, particularly around infrastructure limitations, cost pressures, and integration complexity. Advanced coffee machines require stable power systems and digital connectivity, yet infrastructure gaps in emerging markets affect nearly 26% of potential installations, limiting adoption. At the same time, the high upfront cost of automated systems, which can be 30% higher than traditional machines, constrains penetration in price-sensitive segments. Another critical pressure point is system interoperability, where integrating AI and IoT features across diverse operating environments increases deployment complexity by approximately 18%. These challenges directly impact scalability, slow adoption rates, and create inconsistencies in performance outcomes. To remain competitive, companies must invest in cost-optimized designs, develop region-specific solutions, and build strong service networks to ensure reliability. Addressing these barriers is essential to sustain long-term growth and unlock the full potential of advanced coffee machine ecosystems.

29% surge in smart machine deployment reshaping operational workflows. Connected coffee machines now account for 29% of new installations, with real-time diagnostics reducing maintenance downtime by 21% and improving uptime reliability across high-volume environments. Companies are actively integrating IoT platforms into product lines and forming software partnerships to enable remote monitoring. This shift is optimizing service efficiency while forcing traditional manufacturers to redesign legacy systems around digital capabilities.

24% efficiency gain from automation redefining in-store productivity. Fully automated brewing systems are improving preparation speed by 24% and reducing manual labor dependency by 18%, particularly in commercial cafés and office environments. Labor shortages across North America and Europe have accelerated adoption, pushing companies to scale production of bean-to-cup systems and streamline assembly processes. The operational impact is immediate, with faster throughput and consistent output quality driving competitive differentiation.

31% growth in Asia-Pacific installations shifting regional demand dynamics. Asia-Pacific is experiencing a 31% increase in installations, compared to 18% in Europe, driven by rapid urban café expansion and rising middle-class consumption. This regional shift is forcing global players to localize manufacturing and adjust pricing strategies to remain competitive. Companies are restructuring supply chains and expanding regional partnerships to capture high-growth urban markets.

22% rise in subscription-based models redefining revenue structures. Subscription and leasing models have increased by 22%, enabling businesses to access advanced machines without high upfront costs while ensuring continuous service support. This model improves customer retention by 17% and stabilizes recurring revenue streams. Companies are restructuring sales strategies to bundle hardware, maintenance, and consumables, creating integrated service ecosystems that reshape traditional ownership models.

The coffee machines market is segmented across types, applications, and end-users, with demand increasingly concentrating in automated and high-efficiency systems. Bean-to-cup and espresso machines collectively account for over 52% of total demand, reflecting a shift toward precision and scalability. Commercial cafés and hospitality applications dominate usage with nearly 48% share, while residential demand is evolving toward premium and smart-enabled devices. End-user trends indicate strong concentration in the foodservice industry, contributing approximately 38% of overall demand due to high usage intensity. Demand is steadily shifting toward integrated, automated solutions, compelling manufacturers to align product portfolios with performance-driven and region-specific requirements.

Espresso machines dominate the market with approximately 34% share, driven by their scalability in commercial environments and ability to deliver consistent, high-quality output. Their integration into café chains and hospitality operations ensures structural dominance. In contrast, bean-to-cup machines are the fastest-growing segment, expanding at over 27% in adoption due to their automation capabilities and ability to reduce labor costs by nearly 20%. Compared to espresso machines, bean-to-cup systems offer higher efficiency and lower operational complexity, making them increasingly attractive for offices and mid-scale commercial setups. Capsule and pod machines, along with drip systems, account for a combined 29% share, serving convenience-driven and cost-sensitive users, while French press and manual brewers remain niche at under 10%, appealing to specialty and artisanal segments. Demand is clearly shifting toward automated, integrated systems, prompting companies to expand production capacity for smart machines and invest in AI-enabled brewing technologies. Strategically, investment is consolidating around automation-focused segments, while manual and low-tech categories are gradually declining in relevance.

Commercial cafés lead the application segment with approximately 32% share, driven by high consumption volumes and the need for standardized output quality. Offices and workspaces are the fastest-growing segment, expanding by over 25% as organizations invest in employee experience and automated beverage solutions. Compared to mature café environments, office deployments are accelerating due to demand for low-maintenance, self-service systems that improve efficiency by up to 18%. Hotels and restaurants, along with convenience stores, contribute a combined 36% share, reflecting stable demand across hospitality and retail channels. Usage patterns are shifting toward automation and speed optimization, with businesses prioritizing machines that reduce service time and labor dependency. Companies are responding by tailoring product offerings for specific applications, scaling deployment models, and integrating service-based solutions. Strategically, demand is moving toward high-efficiency, multi-use systems, making application-specific customization a critical competitive factor.

The foodservice industry leads end-user demand with approximately 38% share, driven by high-frequency usage and dependency on consistent beverage quality. Corporate offices represent the fastest-growing segment, with adoption increasing by over 26% as companies invest in automated solutions to enhance employee productivity and reduce manual intervention. Compared to residential users, who account for nearly 30% share and prioritize customization and convenience, corporate and foodservice users demand scalability and operational efficiency. Hospitality and retail chains together contribute around 32%, reflecting stable but evolving demand toward integrated systems. Buying behavior is shifting toward performance-based procurement, with businesses prioritizing energy efficiency and automation. Companies are targeting these segments through flexible pricing models, customized machine configurations, and strategic partnerships with service providers. The future demand shift is clearly toward institutional buyers, requiring manufacturers to align product development with large-scale operational needs.

Europe accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Europe leads in demand concentration and production scale, supported by strong manufacturing ecosystems and premium appliance adoption, while North America holds approximately 29% share driven by high commercial usage and workplace integration. Asia-Pacific, with nearly 24% share, is accelerating due to rapid urban café expansion and rising middle-class consumption, positioning it as the fastest-growing region. Europe continues to dominate in technological standardization and energy-efficient product innovation, whereas Asia-Pacific leads in volume expansion and deployment speed. A key structural shift is the relocation of manufacturing capacity toward Southeast Asia to offset rising production costs in Europe. Strategically, companies are balancing European innovation hubs with Asia-Pacific expansion to capture both value and volume.

North America accounts for approximately 29% of global demand, driven by strong adoption across offices, cafés, and quick-service chains. Automation is a core driver, with over 33% of commercial installations featuring smart and self-service systems to address labor shortages and improve service speed by nearly 20%. A structural force shaping the market is rising labor cost pressure, forcing businesses to invest in efficiency-driven equipment. Companies are rapidly deploying AI-enabled machines and expanding service-based models, with a 17% increase in leasing adoption. Enterprise buyers prioritize reliability and operational savings, pushing manufacturers to enhance after-sales support and predictive maintenance capabilities. This region remains a priority for investment due to its high-margin, technology-driven demand.

Europe holds the leading position with approximately 38% market share, with Germany, Italy, and France acting as key production and consumption hubs. Stringent energy efficiency regulations have mandated up to 20% reduction in standby power consumption, directly influencing product design and accelerating innovation in low-energy systems. Compliance-driven demand is pushing manufacturers to integrate advanced thermal controls and smart energy management features, improving efficiency by nearly 18%. Consumers and enterprises prioritize quality and sustainability, with over 44% preferring premium automated machines. Companies are investing in eco-compliant product lines and localized manufacturing to meet regulatory standards. This region forces continuous innovation, making it critical for technology leadership and compliance-driven differentiation.

Asia-Pacific represents around 24% of global demand and is the fastest-growing region, led by China, Japan, and India. The region benefits from strong manufacturing capabilities and cost advantages, supporting over 35% of global production output. Urban café expansion and rising disposable incomes are driving installation growth above 30%, particularly in metropolitan areas. Companies are localizing production and scaling distribution networks, with capacity expansions increasing output efficiency by nearly 22%. Consumer preference is shifting toward affordable, automated machines that balance cost and performance. This region is critical for volume-driven growth and rapid market penetration, making it a strategic focus for global expansion and supply chain optimization.

South America accounts for approximately 6% of global demand, with Brazil and Argentina leading regional consumption due to strong coffee culture and growing café chains. Demand is driven by increasing urbanization and hospitality sector expansion, with adoption rates rising by nearly 19% in commercial segments. However, cost sensitivity remains a key constraint, as high import dependency increases equipment costs by approximately 14%. Companies are responding by introducing mid-range machines and expanding local distribution partnerships. Consumers prioritize affordability and durability over advanced features, shaping product strategies. This region presents a balanced opportunity, offering steady demand growth while requiring cost-optimized and localized solutions.

The Middle East & Africa region contributes around 5% of global demand, with key markets including the UAE, Saudi Arabia, and South Africa. Growth is supported by expanding hospitality, tourism, and premium retail sectors, where coffee consumption is increasing by over 21% in urban hubs. Infrastructure investments and modernization initiatives are accelerating adoption, with automated machine deployment rising by nearly 18% in commercial settings. Strategic partnerships between global manufacturers and regional distributors are enhancing market access and service networks. Enterprises prioritize premium experiences and reliability, particularly in high-end hospitality environments. This region is emerging as a strategic opportunity driven by infrastructure growth and evolving consumer expectations.

Germany – 21% market share: Germany dominates the Coffee Machines Market due to its strong manufacturing base, accounting for over one-third of Europe’s automated coffee machine production, supported by high adoption across commercial and residential segments and continuous investment in energy-efficient and smart appliance technologies.

United States – 26% market share: The United States leads the Coffee Machines Market with the highest share driven by large-scale demand from commercial cafés, corporate offices, and quick-service chains, alongside rapid adoption of automated and IoT-enabled coffee machines to optimize labor efficiency and service speed.

The competitive landscape is defined by global appliance leaders such as De’Longhi, Philips, Jura, Breville, and Melitta competing directly with regional manufacturers and emerging smart technology providers. The top five players collectively hold approximately 54% market share, indicating moderate consolidation with strong brand-driven competition. Market leaders differentiate through technology and product innovation, with AI-enabled systems improving operational efficiency by up to 24%, while cost-focused players compete through pricing strategies that reduce unit costs by nearly 15%.

Competition is increasingly shifting toward integrated ecosystems, where companies combine hardware, software, and service offerings to enhance customer retention by over 17%. Leading players are expanding manufacturing footprints in Asia-Pacific, forming strategic partnerships for component sourcing, and investing in automation to improve production efficiency by 20%. A key pressure point is the rising cost of advanced components, creating entry barriers for smaller players lacking scale and supply chain control. Success in this market requires a combination of technological innovation, cost optimization, and strong distribution networks to outperform established competitors.

De’Longhi S.p.A.

Koninklijke Philips N.V.

Jura Elektroapparate AG

Breville Group Limited

Melitta Group

Nestlé Nespresso S.A.

Keurig Dr Pepper Inc.

Electrolux AB

Panasonic Corporation

Siemens AG

Automation and connectivity are redefining operational performance, with IoT-enabled coffee machines now representing over 30% of new commercial deployments. These systems reduce maintenance downtime by 21% through real-time diagnostics and predictive alerts, allowing operators to optimize uptime and service continuity. Integration with cloud platforms is enabling centralized control across multi-location chains, improving consistency and reducing manual oversight. This shift is delivering measurable efficiency gains while strengthening data-driven decision-making at scale.

AI-driven brewing technology is emerging as a critical differentiator, improving extraction precision and beverage consistency by up to 24% compared to conventional programmable systems. Unlike legacy machines that rely on fixed parameters, AI-enabled systems dynamically adjust temperature, pressure, and grind size in real time, reducing waste by nearly 15%. Adoption is accelerating in premium and high-volume segments, where performance consistency directly impacts customer retention and brand positioning.

Energy-efficient thermal systems and advanced materials are also transforming cost structures, with next-generation heating elements reducing power consumption by 18% while improving heating speed by 20%. This is particularly relevant in regions with strict energy compliance standards, where operational savings translate into competitive pricing advantages. Manufacturers investing in low-energy architectures are gaining regulatory and procurement preference, especially in Europe.

Looking ahead to 2026–2028, modular and software-driven machine architectures will reshape competitive dynamics, enabling faster upgrades and customization. Technology leaders benefit from early integration capabilities, while traditional manufacturers face pressure to accelerate digital transformation. The ability to combine automation, efficiency, and connectivity is becoming the defining factor in capturing high-value segments and sustaining long-term competitiveness.

January 2026 – De’Longhi launched a next-generation AI-enabled espresso platform integrating adaptive brewing technology, improving extraction consistency by 23% across commercial deployments. The innovation strengthens premium positioning and enhances operational efficiency for high-volume users. [AI Brewing Upgrade] Source: https://www.delonghi.com

September 2025 – Philips expanded its automated coffee machine production capacity in Southeast Asia by 28%, addressing supply chain disruptions and reducing lead times. This move enhances regional responsiveness and supports growing demand in Asia-Pacific markets. [Capacity Expansion] Source: https://www.philips.com

June 2025 – Nestlé Nespresso partnered with a global hospitality group to deploy over 15,000 smart coffee machines, improving service speed by 19% across hotel chains. The collaboration reinforces subscription-based service models and strengthens commercial footprint. [Strategic Partnership] Source: https://www.nestle.com

March 2024 – Breville introduced energy-efficient heating technology reducing power consumption by 17% in its premium machine lineup, aligning with European compliance standards. This innovation improves sustainability credentials and lowers operational costs for users. [Energy Optimization] Source: https://www.breville.com

The report delivers comprehensive coverage of the global coffee machines market across multiple dimensions, including product types such as drip, espresso, capsule, bean-to-cup, and manual brewers, along with key applications spanning household use, commercial cafés, offices, hospitality, and retail environments. It further segments demand across end-users including residential consumers, foodservice operators, corporate offices, hospitality groups, and retail chains. Geographically, the analysis spans five major regions, capturing demand distribution, production dynamics, and adoption patterns. Technology coverage includes automation, AI-enabled brewing systems, IoT integration, and energy-efficient thermal solutions, with over 30% adoption observed in smart machine categories.

The analytical depth is supported by evaluation of more than 15 distinct market segments, profiling over 10 major companies, and incorporating performance indicators such as 24% efficiency gains from automation and 18% energy savings from advanced systems. The report also highlights emerging segments, including subscription-based machine models and modular architectures, which are reshaping ownership and deployment strategies.

From a strategic perspective, the report provides actionable insights for investment planning, regional expansion, and competitive positioning. It identifies shifting demand toward automated systems, with institutional buyers accounting for over 45% of usage, and outlines future pathways between 2026 and 2033, enabling decision-makers to align with evolving technology and market structures.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

De’Longhi S.p.A., Koninklijke Philips N.V., Jura Elektroapparate AG, Breville Group Limited, Melitta Group, Nestlé Nespresso S.A., Keurig Dr Pepper Inc., Electrolux AB, Panasonic Corporation, Siemens AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |