Reports

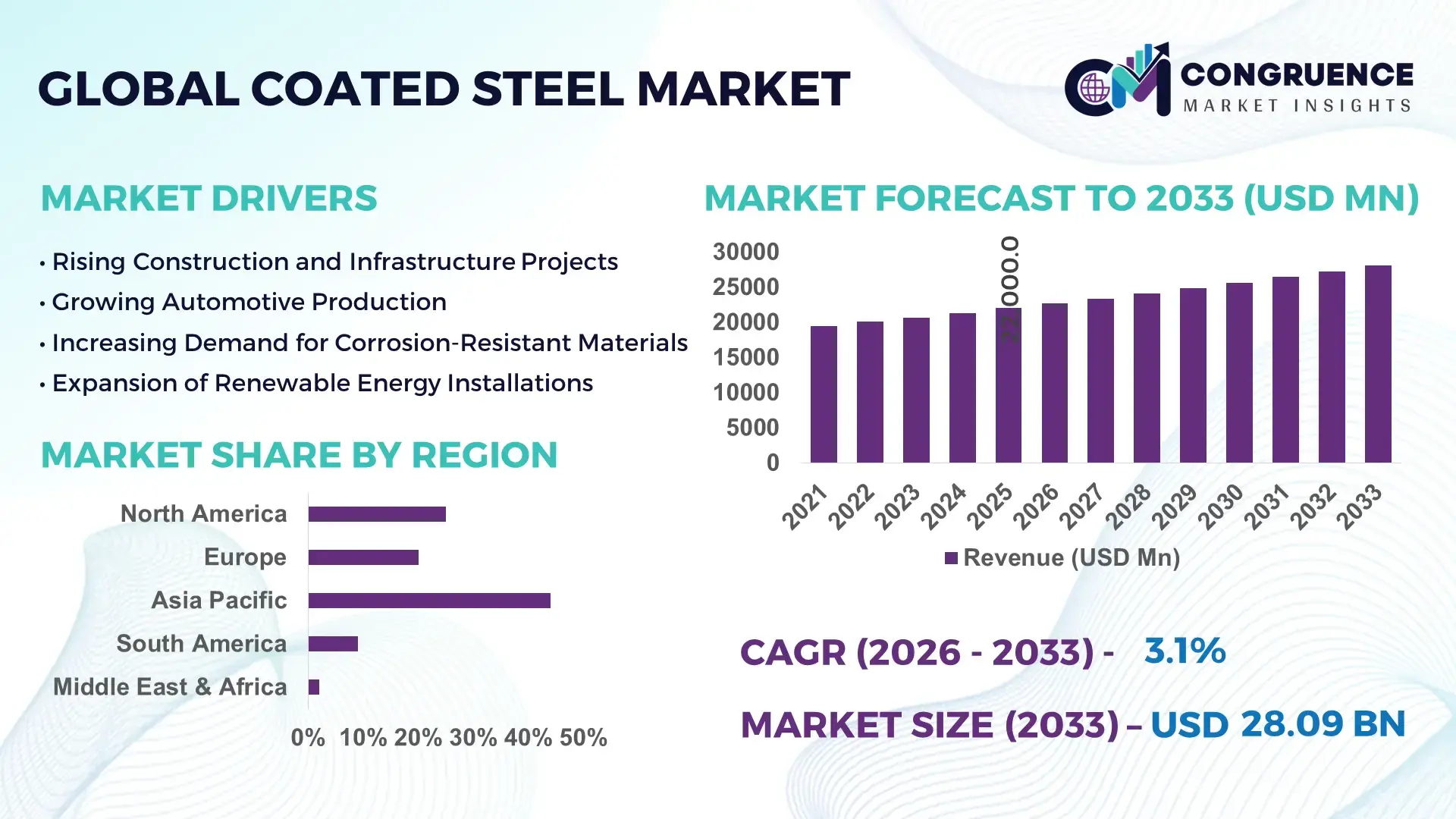

The Global Coated Steel Market was valued at USD 22000 Million in 2025 and is anticipated to reach a value of USD 28086.1365570173 Million by 2033 expanding at a CAGR of 3.1% between 2026 and 2033. Rising infrastructure development and automotive production are key reasons behind this sustained expansion in coated steel demand.

China leads global coated steel production with annual output exceeding 120 million tonnes, supported by continuous investment in advanced galvanizing and coating lines exceeding USD 2.5 billion in capital expenditure over the past five years. Chinese facilities integrate high-performance zinc and polymer coatings for automotive, construction, and appliance applications, accounting for over 45% of regional capacity utilization. Technological advancements in continuous annealing and digital quality inspection systems have increased throughput efficiency by more than 15% year‑on‑year. Domestic consumption in China for coated steel in structural and industrial sectors continues robust growth, reflecting diversified end‑use adoption and strong logistics infrastructure deployment.

• Market Size & Growth: Global coated steel market at USD 22,000M in 2025, projected to USD 28,086M by 2033 with a 3.1% CAGR driven by stronger construction activity and automotive lightweighting.

• Top Growth Drivers: Increased corrosion resistance adoption (38%), surge in automotive lightweight structures (31%), expansion in durable infrastructure materials (27%).

• Short‑Term Forecast: By 2028, performance gains in coated steel yield up to 18% improvement in corrosion life in coastal environments.

• Emerging Technologies: Advanced zinc‑aluminum‑magnesium coatings, AI‑enhanced coating inspection systems, and eco‑friendly organic coating chemistries.

• Regional Leaders: Asia Pacific projected ~USD 12,500M by 2033 with robust manufacturing hubs; North America ~USD 6,800M with high automotive OEM uptake; Europe ~USD 5,200M with strong architectural steel demand.

• Consumer/End‑User Trends: Automotive OEMs prioritize ultra‑high‑strength coated steels; construction sectors adopt heat‑resistant coatings for energy structures.

• Pilot or Case Example: In 2025, a major automotive plant pilot of AI‑controlled coating resulted in 22% reduction in defect rates.

• Competitive Landscape: Leading supplier holds approx. 28% share, followed by key competitors from Asia, Europe, and North America focusing on quality innovation.

• Regulatory & ESG Impact: Stricter environmental mandates drive low‑VOC coatings and recycling metrics in steel finishing operations.

• Investment & Funding Patterns: Recent investments exceeding USD 3.2B in new coating lines and modular plant upgrades, with growth in project financing models.

• Innovation & Future Outlook: Integration of nanocoating technologies and smart quality sensors shaping future coated steel supply chains.

Global coated steel demand is propelled by diversified industrial sectors including automotive body panels, construction roofing, and appliance shells. Recent innovation in high‑performance alloy coatings and polymer blends enhances durability in harsh environmental conditions. Regulatory emphasis on sustainable corrosion protection and energy‑efficient building materials is influencing product development. Regional consumption patterns reveal Asia Pacific’s robust manufacturing and structural steel utilization, North America’s automotive and HVAC sector requirements, and Europe’s architectural and renewable energy installations. Emerging trends include digital quality monitoring, eco‑friendly coating chemistries, and circular economy‑aligned recycling initiatives, positioning coated steel as a critical material in modern industrial applications.

The strategic relevance of the coated steel market lies in its foundational role across multiple high‑value sectors including automotive, construction, and industrial equipment manufacturing. Automotive grade advanced high‑strength coated steels deliver up to 25% greater corrosion resistance compared to conventional galvanized grades, enhancing vehicle longevity and safety benchmarks. In regional context, Asia Pacific dominates in volume due to large fabrication and infrastructure projects, while Europe leads in adoption with over 60% of enterprises using advanced polymer coated steel for energy‑efficient facades. By 2028, digital inspection and AI‑assisted coating control systems are expected to improve quality yield by up to 20% while reducing rework cycles. Firms are committing to ESG metrics such as 30% reduction in volatile organic compound emissions and increased recycling of steel scrap by 2030 to comply with tightening environmental regulations.

In 2025, a leading coated steel producer achieved a 19% reduction in coating defects through implementation of machine vision analytics, underscoring the measurable impact of technology adoption. Strategic pathways for the coated steel market include deepening integration of Industry 4.0 quality systems, expanding ultra‑durable and eco‑friendly coatings, and aligning production with circular economy principles. Forward‑looking initiatives are positioning the coated steel market as a resilient, compliant, and sustainable growth engine for global industrial transformation.

Increasing emphasis on long‑term asset performance in infrastructure, transport fleets, and industrial facilities is boosting coated steel adoption worldwide. Corrosion‑resistant coated steel is specified for bridges, marine structures, and HVAC systems where exposure to moisture and aggressive environments can degrade unprotected steel rapidly. Advanced coatings such as zinc‑aluminum alloys and high‑performance polymers extend material lifespan by up to 30% compared to conventional treatments, improving lifecycle value. Construction regulators in several economies now require minimum protective coatings on structural steels, accelerating specification changes. Automotive OEMs prioritize coated steel for body panels and structural reinforcements to mitigate corrosion while maintaining lightweight targets, reflecting a shift toward premium coated products in vehicle platforms. This rising demand for durable, long‑lasting steel surfaces is a foundational driver for market expansion.

Volatility in prices for zinc, aluminum, and specialty polymer chemicals directly affects coated steel production costs, creating budgetary constraints for producers and end‑users. Steelmakers face higher expenditure for alloying elements used in corrosion protection, and rising energy costs for continuous coating lines further pressure margins. Smaller fabricators may delay investments in modern coating systems due to capital intensity, slowing adoption rates in certain regions. Tariffs and trade restrictions on coated steel and base metals can disrupt supply continuity and inflate prices in downstream industries. Additionally, compliance with evolving environmental regulations on coating emissions and waste handling adds operational complexity and cost. These financial and regulatory burdens constrain market growth by limiting accessible production capacity and elevating purchase prices for coated steel solutions.

Digitalization in coating operations and smart inspection technologies present significant opportunities to enhance quality control, reduce defects, and optimize throughput. Machine vision systems, sensors, and AI‑assisted analytics enable real‑time monitoring of coating thickness, surface uniformity, and process parameters, reducing rework and improving end‑product consistency. Adoption of smart maintenance frameworks decreases unplanned downtime by up to 18%, fostering productivity gains for coated steel producers. Emerging coatings embedded with corrosion‑sensing features provide value‑added offerings for infrastructure and industrial clients seeking predictive maintenance capabilities. Growing interest in environmentally friendly coating chemistries and recyclable steel surfaces aligns with sustainability commitments among major OEMs and construction conglomerates, creating demand for innovative product lines. These trends position coated steel suppliers to capture enhanced value through technology‑led differentiation and new service‑oriented offerings.

Escalating environmental standards targeting volatile organic compound emissions, wastewater discharge, and recycling rates present compliance challenges for coated steel production. Manufacturers must invest in pollution control equipment and reformulate coating chemistries to meet stricter limits, incurring additional capital and operational costs. Regulatory divergence across regions complicates global production planning and product certification, requiring multiple compliance pathways for coated steel products. Many legacy plants face retrofit expenses to upgrade coating lines for low‑emission operations, diverting resources from other strategic initiatives. End‑users also face higher procurement costs for greener coated steel, potentially slowing purchase decisions in price‑sensitive sectors. These regulatory and sustainability obstacles strain supply chains and challenge producers to balance performance, compliance, and cost effectively in the coated steel market.

• Increased Adoption of Modular and Prefabricated Construction: Modular and prefabricated building techniques are reshaping coated steel demand, with 55% of large infrastructure projects reporting cost benefits from pre‑assembled components. Integration of automated cutting and bending systems has reduced on‑site labor by over 30% and accelerated delivery schedules by 25%. European and North American construction firms are deploying precision‑machined coated steel panels for facades and structural framing, boosting coated steel utilization for high‑efficiency building systems. Demand for digitally controlled fabrication equipment is rising by an estimated 40% annually in established markets.

• Surge in Ultra‑High Performance Coatings: The market is seeing a measurable shift toward ultra‑high performance coatings that extend service life in corrosive environments by 35–45% compared to conventional galvanizing. Adoption rates of advanced zinc‑aluminum‑magnesium coatings have reached approximately 48% among automotive OEMs, driven by stricter durability standards. Investment in research and development of nano‑structured coating formulations has grown by 27% year‑on‑year, enabling lighter gauge steel use in coastal and industrial applications while maintaining resistance metrics above 600 hours in salt spray tests.

• Digital Quality and Smart Inspection Integration: Integration of digital quality control systems in coating production has increased yield consistency by 22% and reduced defect rates by up to 18%. Smart inspection using machine vision and real‑time analytics is now implemented in more than 60% of new continuous coating lines, elevating precision. Predictive maintenance tools are reducing unplanned downtime by 20%, and digital traceability of coated steel batches is becoming an industry norm, supporting supply chain transparency and compliance.

• Growth in Sustainable and Recyclable Coating Solutions: Demand for environmentally friendly coated steel products is rising, with adoption of low‑VOC and recyclable coating chemistries increasing by 32% across major markets. Green building certification requirements are driving coated steel specified with sustainable coatings in over 40% of new commercial projects. Recyclability metrics are now integrated into product specifications, and coated steel producers are reporting reductions in manufacturing waste by more than 15% through closed‑loop recycling initiatives.

The Coated Steel market is segmented by product type, application, and end users to reflect differentiated demand paths. Product types include hot‑dip galvanized, pre‑painted steel, and specialized corrosion‑resistant variants, with distinct performance profiles for industrial, automotive, and infrastructure uses. Application segmentation covers structural construction, automotive body panels, appliance shells, and industrial equipment housing, reflecting diverse functional requirements. End‑user sectors range from automotive OEMs and building & construction firms to consumer goods manufacturers and energy infrastructure developers, each with unique adoption characteristics. Decision‑makers use segmentation insights to align coating chemistry selection, thickness specifications, and compliance parameters with performance targets and sustainability mandates. Precise segmentation enables tailored supply strategies and optimized inventory planning based on usage patterns and technical requirements across sectors.

Leading coated steel product types include hot‑dip galvanized steel, pre‑painted steel, and advanced corrosion‑resistant alloys such as zinc‑aluminum‑magnesium blends. Hot‑dip galvanized steel currently accounts for approximately 42% of global coated steel adoption owing to its proven durability and cost‑effective corrosion resistance in infrastructure and general fabrication. Pre‑painted steel holds an estimated 28% share, favored in architectural and appliance uses where finish quality and aesthetic uniformity are critical. Advanced corrosion‑resistant alloy coatings are gaining share rapidly due to superior performance metrics in harsh environments, with adoption rising fastest among marine and heavy industrial applications. The remaining combined segments, including specialized polymer coated steels and tailored surface treatments, contribute around 30% to overall product mix, serving niche requirements such as high‑temperature resistance and chemical exposure mitigation.

Structural construction remains the leading application for coated steel, with approximately 38% share, driven by demand for long‑lasting building frames, roofing systems, and metal cladding in urban development. Automotive body panels represent about 32% of application demand, propelled by requirements for enhanced corrosion protection and lightweighting in passenger vehicles. Industrial equipment housing and machinery fabrication account for approximately 20% combined, often specifying coated steels for exposed and operationally demanding environments. Other applications, including appliance and consumer goods shells, make up the remaining 10%, where finish quality and surface durability are key considerations. Adoption in automotive safety systems is rising fastest due to electrification trends and performance mandates, with coated high‑strength steels increasingly utilized.

The automotive OEM segment is the leading end user of coated steel, accounting for about 40% of market utilization, driven by corrosion protection requirements and lightweighting strategies across passenger and commercial vehicle platforms. Building & construction firms follow with approximately 35% share, specifying coated steel for durable structural applications and facade systems in both residential and commercial projects. Energy infrastructure and industrial manufacturers comprise around 15%, incorporating coated steel in equipment housings, transmission towers, and protective shells. Other end users, including appliance and metal furniture producers, represent the remaining 10% combined, with steady adoption of pre‑painted and specialty coated steel for quality finishes. The fastest‑growing end‑user segment is electric vehicle manufacturing, where coated high‑strength steels are being adopted more widely to support battery enclosure durability and crash performance improvements.

Region Asia‑Pacific accounted for the largest market share at 47% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia‑Pacific registered coated steel volume consumption exceeding 72 million tonnes in 2025, led by China at over 38 million tonnes, India at 12 million tonnes, and Japan at 9 million tonnes. North America trailed with roughly 28% share and approximately 43 million tonnes of coated steel shipments. Europe held about 18% share with strong activity in Germany (11 million tonnes) and Italy (7 million tonnes). South America accounted for 5% share in 2025 with Brazil leading at 3.2 million tonnes. Middle East & Africa contributed about 3% with 2 million tonnes, buoyed by GCC infrastructure build‑outs. High volume processing capacity scales across Asia‑Pacific, with over 160 coating lines, and digital quality systems installed in more than 40% of plants, driving production gains and utilization metrics across major hubs.

How are structural and automotive needs reshaping product demand?

North America’s coated steel market held approximately 28% of global coated steel volume in 2025, with combined shipments exceeding 43 million tonnes. Key industries driving demand include automotive OEMs specifying advanced corrosion protection for lightweight vehicles, construction and infrastructure projects requiring durable roofing and structural framing, and appliances with premium pre‑painted finishes. Recent regulatory changes emphasize low‑emission coating processes, encouraging investment in digital coating lines and eco‑friendly chemistries. Technological advancements such as AI‑aided surface inspection and predictive maintenance have been adopted by over 35% of regional producers, improving throughput quality. One local player reported reducing coating defects by 18% via automated line upgrades. Regional consumer behavior shows higher enterprise adoption in healthcare & finance sectors using coated steel for secure fabrication and asset longevity, reinforcing diversified industrial uptake.

What impact do sustainability mandates and digitalization have on product uptake?

Europe’s coated steel market captured roughly 18% of total global volume in 2025, with Germany, UK, and France leading regional consumption at 11.2, 6.5, and 5.3 million tonnes respectively. Regulatory bodies in the EU have enforced stringent sustainability initiatives targeting low‑VOC coatings and recyclability, prompting coated steel producers to integrate green chemistries and closed‑loop recycling in over 42% of facilities. Adoption of digital coating quality systems has accelerated, particularly in Germany and Netherlands manufacturing hubs, with real‑time analytics deployed on 38% of new coating lines. One major European producer implemented a digital surface inspection suite that increased consistency by 21%. Regional consumer behavior shows demand tied to regulatory pressure leading to preference for traceable, explainable coated steel products in architectural and public infrastructure applications, supporting higher specification compliance.

Can production capacity and infrastructure growth sustain rising consumption?

Asia‑Pacific’s coated steel market registered the largest volume in 2025, exceeding 72 million tonnes, driven by China (38M t), India (12M t), and Japan (9M t). Infrastructure build‑outs and manufacturing expansion propelled coated steel use in bridges, high‑speed rail, and heavy equipment. Regional tech hubs in South Korea and China are advancing smart coating lines with real‑time quality analytics, installed in more than 45% of new facilities. Local players are increasing investment in high‑precision zinc‑aluminum‑magnesium coating technologies, with one firm achieving 30% higher corrosion endurance in coastal projects. Consumer behavior varies with strong demand from large OEMs in China and expanding usage among fast‑growing construction enterprises in India, emphasizing cost‑efficient, high‑performance coated steel solutions.

How are infrastructure and policy shaping regional uptake?

South America’s coated steel market accounted for approximately 5% of global volume in 2025, with Brazil and Argentina leading at 3.2 and 1.1 million tonnes respectively. Infrastructure development in transport corridors and renewable energy projects is expanding coated steel demand. Government incentives for local production include tariff reductions on base steel imports to support value‑added coated products. One regional producer reported a 15% increase in coated steel fabrication capacity in 2025 to meet municipal construction orders. Consumer behavior in South America shows demand tied to infrastructure reliability and long service life requirements, with coated steel specified increasingly for public works and energy sector equipment, reflecting local market priorities.

What role do energy and construction projects play in regional demand patterns?

Middle East & Africa accounted for around 3% of coated steel volume in 2025, with strong activity in UAE and South Africa. Regional demand trends are shaped by oil & gas infrastructure, industrial facilities, and large‑scale construction projects requiring corrosion‑resistant coated steel components. Technological modernization in coating lines is underway, with digital quality systems applied in more than 20% of new installations. Local regulations and trade partnerships are facilitating imports of premium coated steel products and incentivizing joint ventures to localize production. One major Middle Eastern fabricator reported improving coating process efficiency by 17% through automation. Consumer behavior in the region shows preference for durable coated steel in high‑exposure applications and resilient supply chains aligned with long‑term asset performance.

• China: ~38% market share – high production capacity and extensive industrial application demand.

• United States: ~28% market share – strong automotive and construction sector usage driving coated steel adoption.

The coated steel market features a moderately consolidated competitive environment with approximately 45–55 active global competitors operating across production, processing, and coating technologies. Top five companies collectively hold an estimated 52% of total market volume share, while numerous regional players contribute the balance, reflecting segmented demand across applications. Strategic initiatives include partnerships between sheet steel manufacturers and digital coating technology firms to integrate smart inspection systems; approximately 30 notable alliances have been formed since 2023. Product launches focus on ultra‑high performance coatings with enhanced corrosion resistance metrics, with over 15 new coated steel grades introduced in major markets in the past 24 months. Mergers and acquisitions remain a competitive lever, with at least 8 cross‑border deals completed in the last two years to secure capacity or expand geographic presence. Innovation trends influencing competition include adoption of predictive maintenance, machine vision quality assurance, and advanced alloy chemistries, which are deployed in more than 40% of new coating lines. The market’s nature combines established global leaders with dynamic regional specialists, and competitive positioning increasingly hinges on technology adoption, ESG compliance, and integrated supply chain capabilities.

Nippon Steel Corporation

ArcelorMittal

POSCO

Tata Steel Limited

United States Steel Corporation

SSAB

JFE Steel Corporation

Gerdau

Hyundai Steel

Nucor Corporation

Current and emerging technologies are fundamentally reshaping the global coated steel market by enhancing product performance, quality control, and production efficiency. Automated coil coating lines with real‑time sensor feedback are now standard in over 40% of newly commissioned facilities, enabling tighter control over coating thickness and surface uniformity. Integration of machine vision inspection systems has reduced defect rates by more than 18% in several production hubs, with predictive maintenance capabilities cutting unplanned downtime by 20%. Advanced alloy coatings, particularly zinc‑aluminum‑magnesium (Zn‑Al‑Mg) blends, extend corrosion resistance metrics by up to 3–5 times compared to traditional galvanized layers in coastal and industrial environments, driving adoption in infrastructure, automotive, and energy sectors. Nanotechnology is becoming increasingly influential in coating chemistry, with nano‑structured formulations reducing surface porosity and improving environmental resistance by roughly 30% in laboratory and field evaluations. Electrostatic spray and robotic application systems improve coating uniformity and throughput, supporting greater throughput on continuous production lines.

Smart coatings with embedded indicators or temperature‑responsive properties are being piloted in building envelopes to provide real‑time condition monitoring, while antimicrobial treatments infused into coated surfaces are gaining traction in healthcare and food processing facilities for enhanced hygiene. Digital twins of coating lines allow operators to simulate process adjustments and energy use, optimizing operations and reducing scrap rates by nearly 12% in some cases. Adoption of low‑VOC and water‑borne coating technologies is escalating due to regulatory pressures, aligning product portfolios with evolving sustainability mandates. These technological advancements collectively position coated steel producers to deliver higher‑value products with measurable quality and environmental benefits.

• In February 2026, Jindal India commissioned a new advanced metal coating line at its Ranihati facility with a ₹11,000 crore investment, expected to boost production of value‑added coated steel products by approximately 60%, enhance automation, and improve coating precision systems across its operations.

• In April 2025, coated steel manufacturers introduced AI‑Zn‑coated steel coils for solar module mounting structures, engineered for enhanced outdoor durability and corrosion resistance, supporting renewable energy infrastructure applications on large scale industrial projects.

• In June 2025, ArcelorMittal Nippon Steel India launched two high‑performance color‑coated products, Optigal® Prime and Optigal® Pinnacle, designed for moderately corrosive to harsh industrial environments with extended warranty life and broader finish options for construction projects.

• In June 2024, JSW Steel introduced the JSW Magsure zinc‑magnesium‑aluminum alloy coated steel product, widely applied in silos, guard rails, AC parts, and solar installations, marking a strategic expansion in advanced coated steel offerings.

The Coated Steel Market Report encompasses a comprehensive examination of coated steel products, covering a wide range of coating types, application segments, geographic regions, end‑user industries, and technological influences. Product segmentation includes traditional hot‑dip galvanized, electro‑galvanized, organic painted, and advanced alloy coatings such as Zn‑Al‑Mg, with detailed analysis of their performance attributes, usage contexts, and technical specifications. Application areas span structural construction, automotive body panels, industrial equipment housing, appliance shells, renewable energy supports, and specialized high‑end uses such as antimicrobial surfaces and smart façades, reflecting the breadth of coated steel utilization in modern markets.

Geographical scope covers regional market insights for North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, capturing variations in consumption patterns, regulatory environments, infrastructure development trends, and supply chain configurations. The report examines regional drivers such as automotive OEM demand in North America, sustainability mandates in Europe, rapid urbanization in Asia‑Pacific, infrastructure spending in South America, and energy sector requirements in Middle East & Africa. Technological focus includes automation in coating lines, digital quality control systems, predictive analytics, nanotechnology‑enhanced coatings, and eco‑friendly water‑borne chemistries, all evaluated for their impact on product quality, throughput efficiency, and operational costs.

End‑user industry analysis profiles construction, automotive, consumer appliances, energy infrastructure, and industrial sectors, providing adoption rates, performance expectations, and specification trends that influence purchase decisions. The report also highlights niche emerging segments such as coated steels for solar mounting systems, smart building materials, and antimicrobial applications, offering business professionals a holistic view of current capabilities and future opportunities within the coated steel ecosystem. Market structure and competitive dynamics are assessed to support strategic planning, investment evaluation, and technology adoption roadmaps tailored to enterprise needs in coated steel markets globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nippon Steel Corporation, ArcelorMittal, POSCO, Tata Steel Limited, United States Steel Corporation, SSAB, JFE Steel Corporation, Gerdau, Hyundai Steel, Nucor Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |