Reports

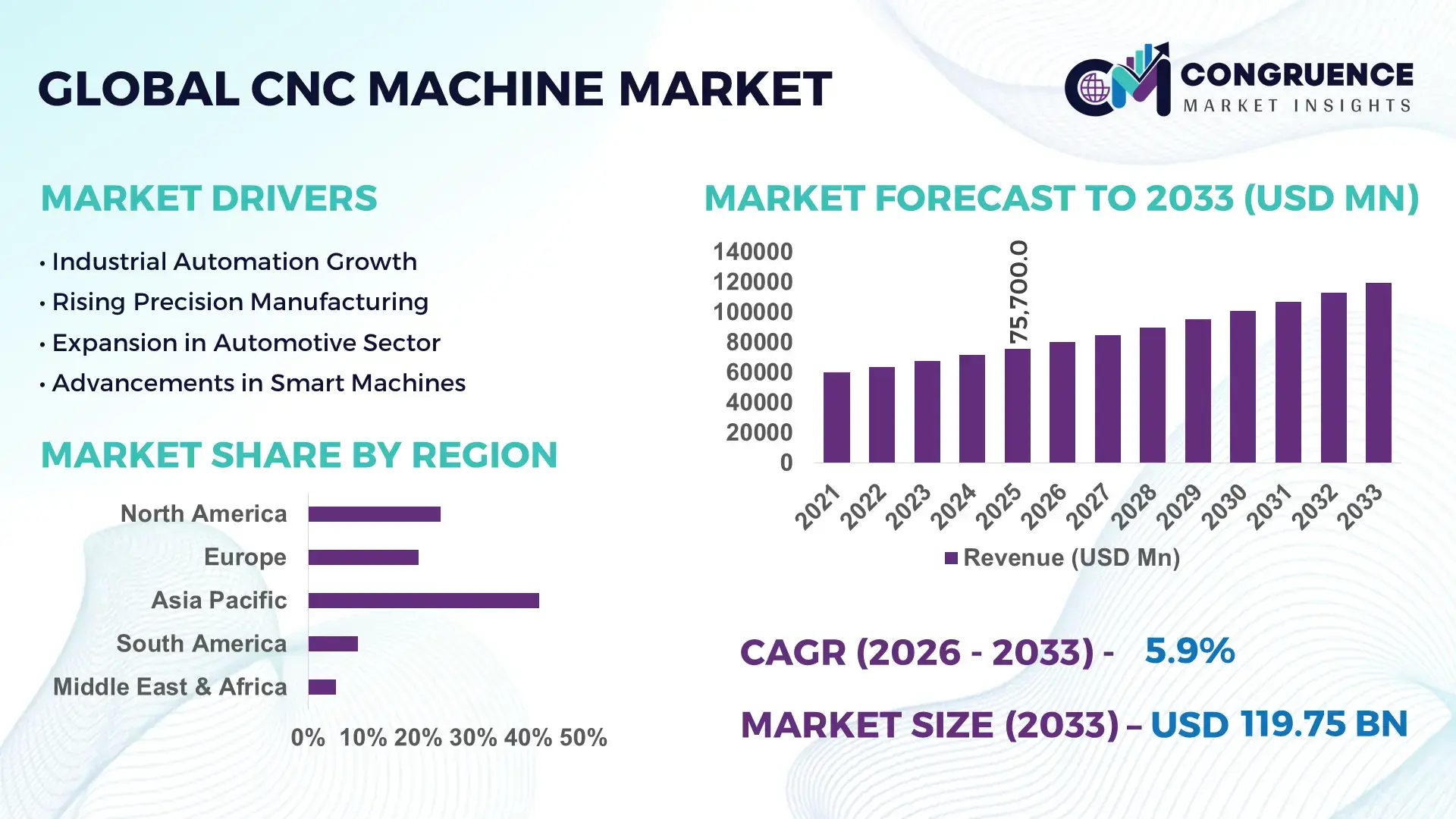

The Global CNC Machine Market was valued at USD 75699.96 Million in 2025 and is anticipated to reach a value of USD 119746.65 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033.

The expansion is being driven by accelerated adoption of multi-axis machining and AI-enabled process optimization, delivering 18–25% higher production efficiency in precision manufacturing environments. Between 2024 and 2026, global supply chain realignment and increased localization of manufacturing under policy frameworks such as industrial reshoring initiatives have intensified investments in advanced CNC infrastructure.

China remains the dominant market, accounting for approximately 32% of global CNC machine production capacity, supported by over USD 12 billion in annual manufacturing investments and strong demand from automotive and electronics sectors. Japan follows with nearly 18% share, driven by high-precision machining exports and robotics integration exceeding 40% of CNC installations. Germany contributes around 14%, leveraging Industry 4.0 adoption with over 55% of factories utilizing interconnected CNC systems. Compared to conventional machining, advanced CNC systems reduce material waste by up to 20% while improving throughput consistency by over 30%, reinforcing their competitive advantage. Strategically, manufacturers prioritizing automation integration and regional production alignment are positioned to secure cost efficiencies and long-term supply resilience.

Market Size & Growth: USD 75.7B (2025) to USD 119.7B (2033) at 5.9%, driven by 22% rise in automated manufacturing adoption globally

Top Growth Drivers: Automation integration (+28%), EV component manufacturing (+24%), aerospace precision demand (+19%)

Short-Term Forecast: By 2028, machining cycle times drop by 17% due to AI-based toolpath optimization

Emerging Technologies: AI-driven CNC, 5-axis machining, digital twin integration improving efficiency by 20–30%

Regional Leaders: Asia-Pacific USD 52B, Europe USD 28B, North America USD 24B; Asia leads with 35% faster factory automation rollout

Consumer/End-User Trends: Automotive and electronics sectors account for 48% CNC usage, with 26% shift toward high-speed machining

Pilot/Case Example: 2025 EV plant deployment improved production efficiency by 21% and reduced downtime by 15%

Competitive Landscape: Top players hold ~38% share; key companies include DMG Mori, Mazak, Haas, Okuma, Makino

Regulatory & ESG Impact: Energy-efficient CNC systems cut power consumption by 18% under stricter industrial emission norms

Investment & Funding: Over USD 9B invested globally in smart manufacturing upgrades, with strong public-private partnerships

Innovation & Future Outlook: Hybrid manufacturing and additive-CNC integration improve design flexibility by 25%

Automotive and aerospace sectors collectively contribute approximately 46% of total CNC machine demand, followed by electronics at nearly 22%, reflecting high reliance on precision machining. Recent innovations include AI-based predictive maintenance reducing machine downtime by 20% and adaptive control systems enhancing tool life by 15%. Asia-Pacific leads demand growth with over 40% share, while North America shows a 12% increase in high-end CNC adoption amid supply chain diversification. The shift toward fully automated smart factories signals a transition toward integrated manufacturing ecosystems, setting the stage for strategic capacity expansion decisions.

The CNC machine market is accelerating into a core battleground for industrial competitiveness, where precision, automation, and digital integration directly determine production economics and supply chain control. As global manufacturing shifts toward high-mix, low-volume production, CNC systems are transforming from standalone equipment into intelligent, interconnected assets that optimize throughput and reduce variability. This transformation is intensifying capital allocation toward advanced machining platforms, particularly in sectors demanding micron-level accuracy.

A major structural shift is emerging from supply chain regionalization and stricter industrial efficiency mandates, forcing manufacturers to localize production while maintaining global quality benchmarks. AI-enabled CNC systems improve efficiency by 28% while reducing operational costs by 18% compared to legacy programmable machines, fundamentally reshaping cost structures. Asia-Pacific leads in production volume with over 40% share, while Europe leads in adoption of smart CNC integration with over 55% of facilities deploying connected machining ecosystems.

In the next 2–3 years, cycle time reduction of 15–20% and defect rate declines of 12% will redefine operational KPIs across precision manufacturing. ESG-driven upgrades are delivering 17% lower energy consumption, providing both compliance advantages and direct cost savings. A 2025 aerospace manufacturing deployment achieved 19% productivity improvement through real-time machining analytics, reinforcing measurable ROI. Investment is shifting aggressively toward automation, digital twins, and hybrid machining capabilities, with manufacturers expanding capacity and forming strategic technology partnerships. Competitive advantage now hinges on how effectively companies integrate intelligence, scale precision, and align production with evolving global supply dynamics.

The rapid shift toward automated and precision-driven manufacturing is forcing widespread CNC machine adoption, driven by a 30% increase in demand for high-accuracy components across automotive, aerospace, and electronics sectors. Global supply chain restructuring, particularly post-2024, has intensified nearshoring strategies, increasing regional CNC deployment by 22% in key manufacturing hubs. This demand surge is directly tied to the need for consistent quality, reduced human error, and scalable production systems. The cause is clear: manufacturers require faster turnaround and precision at scale. The impact is a measurable 20% improvement in production efficiency and up to 18% reduction in scrap rates. In response, companies are accelerating capital investments, expanding multi-axis machining capacity, and forming strategic partnerships with automation and software providers. This shift is not incremental; it is fundamentally redefining manufacturing economics and forcing competitors to modernize or lose cost competitiveness.

Despite strong demand, the CNC machine market is constrained by high upfront capital costs and dependency on critical components such as precision ball screws and advanced controllers, which account for nearly 35% of total machine cost. Fluctuations in raw material prices, particularly specialty alloys, have increased production costs by 12–15%, directly impacting pricing strategies and adoption rates among small and mid-sized manufacturers. A key real-world constraint is the concentration of high-end component manufacturing in limited geographies, creating supply bottlenecks and lead time extensions of up to 20%. This directly affects scalability and delays industrial expansion projects. Companies are mitigating these risks by diversifying supplier bases, entering long-term procurement contracts, and investing in localized component manufacturing. Additionally, some manufacturers are exploring modular CNC designs to reduce cost barriers and improve flexibility, but the transition remains capital-intensive and strategically complex.

The integration of AI, IoT, and digital twin technologies is unlocking new growth pathways, with smart CNC adoption increasing by over 25% across advanced manufacturing facilities. Emerging markets in Southeast Asia and Latin America are witnessing a 20% rise in CNC deployment, driven by industrial expansion and favorable manufacturing policies. These regions offer cost advantages and untapped demand, creating a strong expansion opportunity for global players. A key innovation shift is hybrid manufacturing, combining additive and subtractive processes, delivering up to 23% material savings and enhanced design flexibility. This creates a non-obvious advantage by enabling complex component production with reduced waste and shorter development cycles. Companies are actively investing in R&D, building digital ecosystems, and expanding regional footprints to capture this growth. Strategic positioning now focuses on technology leadership and ecosystem integration rather than standalone machine sales.

The CNC machine market faces critical execution challenges, particularly in workforce skill gaps and infrastructure readiness, which are limiting optimal utilization rates by nearly 18%. Advanced CNC systems require highly skilled operators and programmers, yet training pipelines are not keeping pace with technological advancement, creating a persistent capability gap. Additionally, integration complexity with existing manufacturing systems increases deployment timelines by 15–20%, slowing digital transformation initiatives. Energy infrastructure limitations in emerging markets further constrain high-performance CNC operations, especially where stable power supply is inconsistent. These challenges directly impact long-term scalability and operational consistency. To remain competitive, companies are investing heavily in workforce upskilling programs, automation interfaces that reduce human dependency, and strategic partnerships with software and training providers. Solving these execution barriers is essential for sustaining growth, as failure to align technology with operational capability risks underutilization and diminished return on investment.

35% surge in AI-enabled CNC deployment is reshaping shop-floor execution. Manufacturers are integrating AI-driven toolpath optimization and predictive maintenance, reducing machine downtime by 20% and improving throughput by 18%. This shift is happening through retrofitting existing systems and deploying smart controllers in new installations. The business impact is immediate: lower operational disruptions and tighter production cycles. Companies are scaling software partnerships and embedding analytics into core machining workflows to sustain efficiency gains.

28% increase in multi-axis machining adoption is redefining precision manufacturing. Five-axis and hybrid CNC systems are replacing conventional three-axis machines, cutting setup time by 25% and improving component accuracy by 30%. This transition is driven by demand for complex geometries in aerospace and medical components. Firms are restructuring production lines and investing in advanced tooling to capture higher-margin projects, while also reducing manual intervention across operations.

22% shift toward regionalized production is optimizing supply chain resilience. Post-2024 supply chain disruptions have forced manufacturers to localize CNC operations, reducing lead times by 18% and logistics costs by 12%. Asia continues to lead volume manufacturing, while North America and Europe are accelerating domestic capacity expansion. Companies are establishing regional machining hubs and forming local supplier networks to stabilize production continuity.

19% rise in CNC-as-a-service models is transforming capital allocation strategies. Instead of heavy upfront investments, firms are adopting subscription-based machining access, reducing capital expenditure by 15% and improving asset utilization by 20%. This non-obvious shift is enabling small and mid-sized manufacturers to access high-end CNC capabilities. Providers are expanding service portfolios and building platform-based ecosystems, redefining how machining capacity is consumed and monetized.

The CNC machine market is segmented by type, application, and end-user, each reflecting distinct demand patterns and strategic priorities. CNC milling and turning machines dominate type-based demand due to their scalability and broad industrial use, while laser cutting and EDM technologies are gaining traction in specialized, high-precision applications. By application, automotive and metal fabrication account for over 50% of total demand, driven by high-volume production needs, while aerospace and precision engineering are expanding due to complexity requirements. End-user demand is heavily concentrated in automotive and industrial manufacturing, contributing nearly 55%, though electronics and medical device industries are rapidly increasing adoption. Demand is shifting toward high-precision, automated, and digitally integrated CNC systems, as companies prioritize efficiency, reduced downtime, and localized production capabilities. This segmentation highlights where investments are scaling and where innovation is redefining competitive advantage.

CNC Milling Machines dominate the market with approximately 38% share, driven by their versatility, high precision, and compatibility with multi-axis configurations, making them essential across automotive, aerospace, and industrial manufacturing. Their structural advantage lies in handling complex geometries with 20–25% higher efficiency compared to traditional machining setups. CNC Laser Cutting Machines are the fastest-growing segment, expanding at over 26% adoption growth, fueled by demand for high-speed, non-contact cutting processes that reduce material waste by 18% and improve edge quality.

CNC Turning Machines maintain strong relevance with around 22% share, particularly in mass production of cylindrical components, though they face gradual displacement in complex applications by advanced milling systems. CNC Grinding, EDM, and other specialized machines collectively account for nearly 18%, serving niche applications requiring ultra-precision and fine surface finishing. Demand is clearly shifting toward flexible, high-speed systems, prompting manufacturers to expand multi-axis milling capacity and invest in laser-based technologies. The strategic implication is clear: companies focusing on advanced, adaptable machining platforms are capturing higher-value production opportunities while reducing operational constraints.

Automotive Parts Manufacturing leads with approximately 34% share, driven by high-volume production requirements and the increasing complexity of EV components, which demand precision machining and consistency. The sector benefits from CNC-driven automation, delivering up to 22% faster production cycles and 15% lower defect rates. Aerospace Components is the fastest-growing application, with over 27% growth in CNC adoption, fueled by demand for lightweight, high-precision parts and strict quality standards.

Metal Fabrication and Tool & Die Making together contribute nearly 28%, supporting foundational industrial processes, while Precision Engineering holds a critical niche in high-accuracy components. A clear shift is occurring from volume-driven automotive manufacturing toward precision-focused aerospace and engineering applications. Companies are adapting by deploying advanced CNC systems, enhancing quality control, and investing in high-speed machining technologies. This transition signals a move toward higher-margin, lower-volume production models, where precision and reliability define competitive advantage.

The Automotive Industry remains the leading end-user, accounting for nearly 32% of CNC machine demand due to its scale, continuous production cycles, and reliance on precision components. However, Aerospace & Defense is the fastest-growing segment, expanding at over 25% adoption growth, driven by increasing demand for complex, high-performance parts and stringent quality standards.

Industrial Manufacturing and Electronics Industry together contribute approximately 38%, with electronics showing a 19% rise in CNC adoption due to miniaturization and precision requirements. The Medical Device Industry is emerging as a high-value segment, leveraging CNC machining for intricate, compliance-driven production. A clear contrast exists between automotive’s volume-driven demand and aerospace’s precision-focused growth trajectory. Companies are targeting these segments through customized CNC solutions, flexible pricing models, and strategic partnerships to address specific operational needs. The implication is decisive: future demand is shifting toward high-precision, innovation-driven industries, requiring manufacturers to align product offerings with specialized requirements.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific dominates in production volume and cost-efficient manufacturing, supported by over 45% of global CNC installations and strong export-driven ecosystems. Europe holds around 27% share, leading in high-precision machining and advanced automation adoption exceeding 55% across industrial facilities. North America, with nearly 21% share, is accelerating due to reshoring initiatives and a 23% increase in smart factory investments. Supply chain localization and industrial policy shifts are redefining regional dynamics, pushing companies to rebalance production footprints. Strategically, firms are aligning investments toward Asia for scale, Europe for innovation, and North America for resilient expansion.

How is advanced manufacturing adoption reshaping industrial competitiveness?

North America accounts for approximately 21% of global CNC machine demand, driven by aerospace, defense, and EV manufacturing sectors requiring high-precision machining. A key structural force is reshoring, with over 25% of manufacturers relocating production to reduce supply chain risks. This is accelerating digital transformation, with smart CNC adoption rising by 28% and automation integration improving production efficiency by 18%. Companies are expanding capacity, including a 15% increase in domestic machining facilities since 2024. Enterprises prioritize reliability, speed, and digital integration over cost alone, favoring advanced multi-axis systems. The region remains a strategic investment hub as companies seek supply chain control, technological leadership, and consistent production quality.

What is driving compliance-led transformation in precision manufacturing?

Europe contributes nearly 27% of the global CNC machine market, with Germany, Italy, and Switzerland leading high-precision manufacturing. Stringent ESG and energy efficiency regulations are shaping demand, with over 60% of manufacturers adopting energy-optimized CNC systems to meet compliance targets. This has resulted in a 17% reduction in industrial energy consumption across advanced facilities. Operationally, Industry 4.0 integration is accelerating, with 55% of CNC systems connected to digital production networks. Companies are investing in sustainable machining technologies and automation upgrades to maintain competitive positioning. Enterprise buyers prioritize compliance, quality, and long-term efficiency, making Europe a region where regulatory pressure directly drives innovation and operational excellence.

How is large-scale manufacturing accelerating precision machining demand?

Asia-Pacific leads the CNC machine market with over 42% share, anchored by China, Japan, and South Korea as global manufacturing powerhouses. The region benefits from strong supply chain ecosystems, accounting for nearly 50% of global CNC production capacity. Rapid industrialization and export-driven manufacturing are driving a 24% increase in CNC deployment across automotive and electronics sectors. Execution-level shifts include mass adoption of automated machining lines and localized production scaling, reducing lead times by 20%. Companies are investing heavily in capacity expansion, with industrial clusters increasing output by 18% since 2024. Enterprises prioritize cost efficiency and production speed, making Asia-Pacific critical for large-scale manufacturing and global supply continuity.

What is shaping industrial modernization and adoption patterns?

South America holds approximately 5% of the global CNC machine market, with Brazil and Argentina leading regional demand. Growth is driven by automotive and metal fabrication sectors, contributing to a 16% increase in CNC adoption over the past two years. However, infrastructure limitations and high equipment import costs, rising by nearly 12%, constrain rapid scalability. Companies are responding by focusing on localized production and incremental technology upgrades, improving operational efficiency by 14%. Enterprises exhibit strong price sensitivity, prioritizing cost-effective and durable CNC solutions over advanced automation. This region presents a balanced opportunity, where steady demand growth is offset by structural constraints, requiring targeted and cost-conscious investment strategies.

How are industrial diversification efforts influencing machining demand?

The Middle East & Africa region contributes around 5% of global CNC machine demand, led by the UAE, Saudi Arabia, and South Africa. Demand is primarily driven by oil & gas, construction, and infrastructure sectors, with CNC adoption increasing by 18% in project-based manufacturing. Government-led industrial diversification initiatives are accelerating investments, with over 20% growth in manufacturing infrastructure projects. Execution-level shifts include increased adoption of automated machining systems to support large-scale construction and energy projects. Companies are forming partnerships and expanding regional capabilities, improving production efficiency by 15%. Enterprises prioritize reliability and project scalability, positioning this region as an emerging strategic market driven by infrastructure transformation.

China – 32% share in CNC Machine Market: Dominates due to large-scale manufacturing capacity, strong domestic demand, and integrated supply chain ecosystems

Japan – 18% share in CNC Machine Market: Leads with advanced precision engineering, high automation adoption, and strong export-oriented CNC production

The CNC machine market is defined by intense competition between global technology leaders such as DMG Mori, Mazak, Okuma, Makino, and Haas, and a growing base of regional manufacturers competing on cost efficiency and localized supply. The top five players collectively control approximately 38% of the market, leveraging advanced automation, product innovation, and global distribution networks. Competition is primarily based on technology differentiation, pricing efficiency, and delivery speed, with AI-enabled systems improving productivity by up to 25% and reducing downtime by 20%.

Global OEMs are focusing on high-end, multi-axis machines and digital integration, while regional players are capturing mid-range demand through cost-competitive offerings. Strategic moves include capacity expansion, cross-border partnerships, and vertical integration to secure critical components and reduce lead times by 15%. The competitive landscape is shifting toward technology-driven differentiation, with digital machining ecosystems redefining value creation. High capital requirements and technological complexity act as key entry barriers. Winning in this market requires continuous innovation, operational agility, and the ability to deliver precision at scale while maintaining cost competitiveness.

DMG Mori

Mazak Corporation

Okuma Corporation

Makino Milling Machine Co., Ltd.

Haas Automation, Inc.

Doosan Machine Tools

FANUC Corporation

Siemens AG

Bosch Rexroth AG

Hardinge Inc.

Hurco Companies, Inc.

GF Machining Solutions

AI-driven CNC systems are redefining machining precision and operational control, with real-time toolpath optimization improving efficiency by 28% and reducing scrap rates by 18%. Adoption has crossed 35% in advanced manufacturing facilities, particularly in aerospace and automotive sectors. Integration with IoT-enabled sensors allows predictive maintenance, cutting downtime by 20% and enabling uninterrupted production cycles. This directly strengthens cost control and throughput consistency, giving early adopters a measurable competitive edge.

Multi-axis machining and digital twin integration are emerging as critical technologies, with five-axis CNC systems improving machining accuracy by 30% compared to traditional three-axis setups while reducing setup time by 25%. Deployment levels have reached nearly 40% in high-precision industries. Digital twins simulate machining processes, reducing prototyping costs by 15% and accelerating production validation. These technologies are enabling manufacturers to handle complex geometries while optimizing resource utilization and minimizing rework.

Hybrid manufacturing, combining additive and subtractive processes, represents a disruptive shift, delivering material savings of up to 23% and reducing production lead times by 20%. Though currently adopted by around 18% of high-end facilities, it is expanding rapidly due to demand for lightweight and complex components. Between 2026 and 2028, these integrated systems will redefine production flexibility and customization, benefiting technology-driven manufacturers that prioritize innovation and advanced capabilities over cost-led competition.

January 2026 – DMG Mori launched an AI-integrated CNC platform with real-time analytics, improving machining efficiency by 22% and reducing downtime by 18%. This innovation strengthens smart factory adoption and enhances precision manufacturing competitiveness. [AI Integration Push]

September 2025 – Mazak Corporation expanded its manufacturing facility capacity by 15% in North America to support rising demand for multi-axis CNC systems, improving regional supply responsiveness and reducing lead times significantly. [Capacity Expansion]

March 2025 – FANUC Corporation introduced advanced CNC automation solutions integrating robotics, increasing production speed by 20% and reducing labor dependency by 17%. This supports large-scale industrial automation and cost optimization strategies. [Automation Upgrade]

June 2024 – Siemens AG partnered with industrial manufacturers to deploy digital twin-enabled CNC solutions, reducing prototyping costs by 16% and accelerating product development cycles. This collaboration strengthens digital manufacturing ecosystems. [Digital Twin Alliance]

This report delivers comprehensive coverage of the CNC machine market by analyzing five core machine types, five major application areas, and five key end-user industries, alongside detailed regional insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It incorporates critical technologies such as AI-enabled machining, multi-axis systems, digital twins, and hybrid manufacturing, with adoption levels exceeding 35% in advanced facilities. The report also captures emerging niches, including CNC-as-a-service models and high-precision medical device machining, reflecting evolving industry dynamics.

The analytical depth includes evaluation of over 12 leading companies, with benchmarking based on market share, technology integration, and operational efficiency improvements of 15–30%. It further assesses demand distribution patterns, with automotive and industrial manufacturing contributing over 50% of usage, while aerospace and electronics show adoption increases above 20%. The report provides forward-looking insights for 2026–2033, focusing on digital transformation, localized production strategies, and automation scaling.

Strategically, it supports decision-making by identifying high-growth segments, technology investment priorities, and regional expansion opportunities. It enables stakeholders to optimize capital allocation, strengthen competitive positioning, and align with shifting manufacturing ecosystems driven by precision, efficiency, and digital integration.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 75699.96 Million |

|

Market Revenue in 2033 |

USD 119746.65 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DMG Mori, Mazak Corporation, Okuma Corporation, Makino Milling Machine Co., Ltd., Haas Automation, Inc., Doosan Machine Tools, FANUC Corporation, Siemens AG, Bosch Rexroth AG, Hardinge Inc., Hurco Companies, Inc., GF Machining Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |