Reports

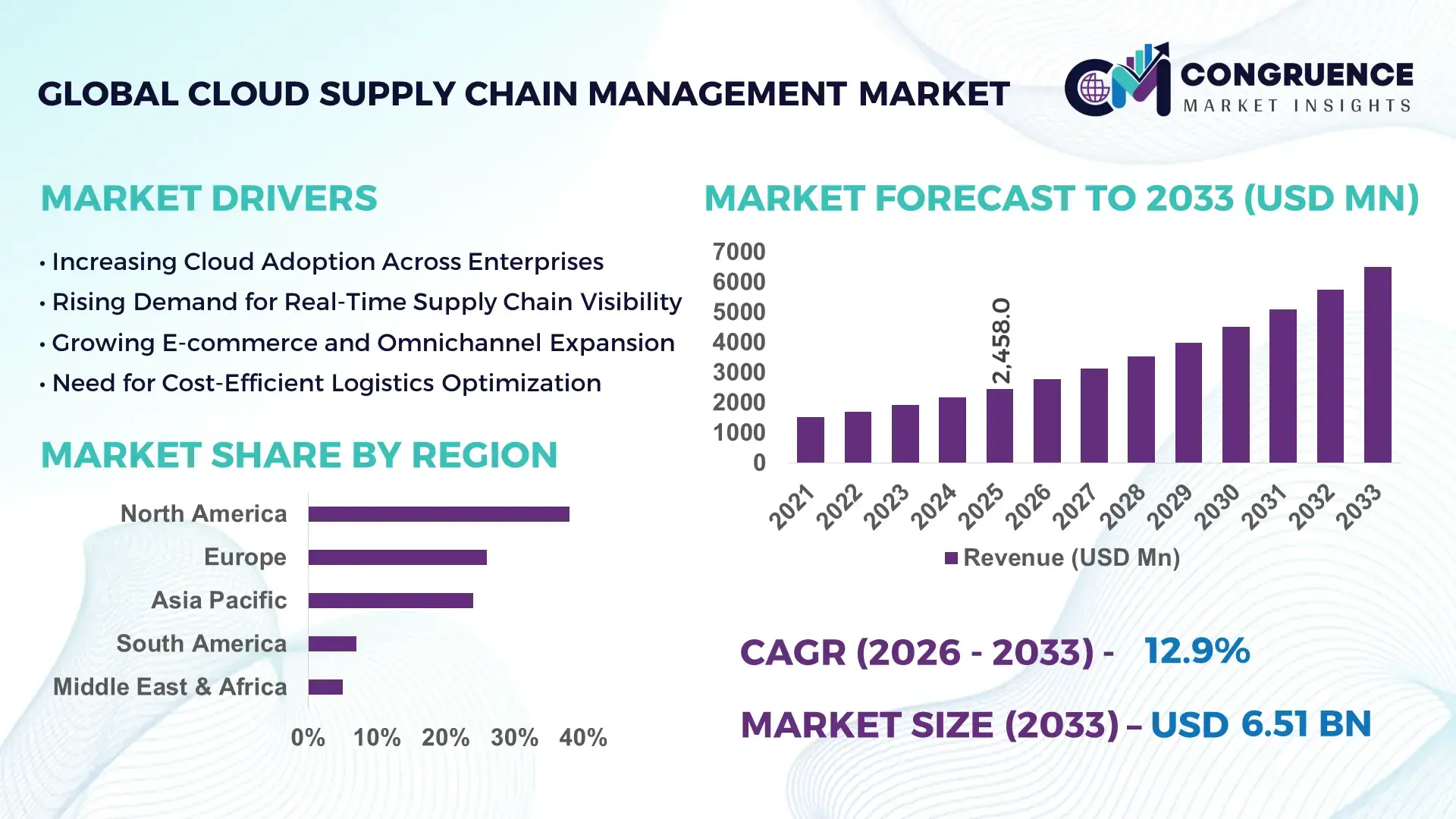

The Global Cloud Supply Chain Management Market was valued at USD 2,458.0 Million in 2025 and is anticipated to reach a value of USD 6,506.8 Million by 2033 expanding at a CAGR of 12.94% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising enterprise digitization, real-time inventory optimization needs, and integration of AI-driven predictive analytics into supply chain ecosystems.

The United States continues to dominate the Cloud Supply Chain Management Market in terms of enterprise deployment scale and technological innovation. Over 72% of large U.S. enterprises have adopted at least one cloud-based SCM module, while manufacturing and retail sectors account for more than 45% of enterprise implementations. The country hosts more than 40 major cloud data center clusters supporting logistics and ERP workloads, with hyperscale cloud infrastructure investments exceeding USD 80 billion annually. AI-enabled demand forecasting tools are integrated into over 60% of tier-1 retail supply chains, and automation-driven warehouse systems cover nearly 35% of large distribution centers nationwide.

Market Size & Growth: Valued at USD 2,458.0 Million in 2025, projected to reach USD 6,506.8 Million by 2033, expanding at 12.94% CAGR due to enterprise cloud migration and AI-based supply chain visibility tools.

Top Growth Drivers: 68% enterprise cloud adoption rate; 35% improvement in demand forecasting accuracy; 28% reduction in inventory holding costs.

Short-Term Forecast: By 2028, predictive analytics integration is expected to reduce logistics costs by 22% and improve order fulfillment rates by 18%.

Emerging Technologies: AI-driven digital twins, blockchain-based traceability, IoT-enabled real-time asset monitoring.

Regional Leaders: North America projected above USD 2.4 Billion by 2033 with high AI integration; Asia-Pacific exceeding USD 1.9 Billion driven by manufacturing digitization; Europe surpassing USD 1.4 Billion with strong ESG compliance adoption.

Consumer/End-User Trends: Over 64% of enterprises prioritize real-time supply visibility; 48% of mid-sized firms are shifting from on-premise ERP to SaaS SCM platforms.

Pilot or Case Example: In 2025, a global retailer implemented AI-based SCM, reducing stockouts by 26% and warehouse downtime by 19%.

Competitive Landscape: SAP holds approximately 21% market presence, followed by Oracle, Blue Yonder, Infor, and Manhattan Associates.

Regulatory & ESG Impact: Carbon disclosure mandates are pushing 40% of multinational firms to integrate emission-tracking modules within SCM systems.

Investment & Funding Patterns: Over USD 5 Billion invested in supply chain SaaS and AI platforms between 2023–2025, with rising venture capital focus on logistics analytics.

Innovation & Future Outlook: Integration of generative AI planning tools and autonomous procurement bots is reshaping predictive supply modeling and scenario simulation.

Cloud Supply Chain Management solutions are widely deployed across manufacturing (38% contribution), retail (27%), healthcare (14%), and logistics (12%). Increasing regulatory emphasis on traceability and carbon reporting, along with AI-enabled inventory optimization tools, is shaping adoption. Asia-Pacific demonstrates strong manufacturing-linked demand, while North America leads in SaaS-based transformation initiatives. Emerging digital twin technology and blockchain integration are strengthening transparency and resilience across global supply networks.

The Cloud Supply Chain Management Market holds strategic relevance as enterprises prioritize resilience, agility, and predictive planning capabilities. AI-powered supply chain orchestration platforms now deliver 30% faster disruption response compared to traditional ERP-based planning systems. Digital twin technology delivers 25% improvement in simulation accuracy compared to legacy spreadsheet-driven forecasting models, allowing enterprises to proactively mitigate risk exposure.

North America dominates in deployment volume, while Asia-Pacific leads in new enterprise adoption with over 58% of mid-sized manufacturers transitioning to SaaS-based SCM platforms. By 2028, AI-driven demand sensing tools are expected to reduce inventory buffers by 20% while improving service-level agreements by 15%. Firms are committing to ESG performance metrics such as 30% emission reduction in logistics operations by 2030 through carbon-optimized routing algorithms.

In 2025, a leading U.S.-based retailer achieved a 24% reduction in excess inventory through machine-learning-based replenishment automation. Over the next three years, blockchain-enabled supplier transparency is projected to improve compliance audit efficiency by 18%. As global trade complexity increases, the Cloud Supply Chain Management Market is positioned as a core enabler of operational resilience, compliance readiness, and sustainable growth across industries.

The Cloud Supply Chain Management Market is influenced by rapid digital transformation, globalization of trade networks, and the growing need for end-to-end supply visibility. Over 65% of multinational enterprises now consider supply chain digitization a board-level priority. The integration of IoT sensors, AI-based analytics, and SaaS ERP platforms has enhanced predictive maintenance accuracy by nearly 30% in logistics-intensive sectors. Increasing disruptions—from geopolitical shifts to climate events—have pushed enterprises to invest in scenario modeling platforms. Additionally, automation in warehousing has expanded by 32% globally, reinforcing the demand for centralized cloud-based coordination platforms capable of real-time analytics and multi-node optimization.

More than 70% of enterprises report challenges in multi-tier supplier monitoring, prompting rapid adoption of cloud-based dashboards and analytics tools. AI-driven SCM platforms improve forecast accuracy by 35% and reduce lead-time variability by 18%. Retailers implementing predictive demand sensing systems have reduced stockouts by 25%, while manufacturing firms report 22% lower procurement cycle times. The shift toward omnichannel commerce, representing over 45% of global retail transactions, further necessitates real-time inventory synchronization and cloud orchestration platforms.

Approximately 52% of enterprises cite data security as a primary barrier to cloud migration. Supply chain systems process sensitive procurement, supplier, and financial data, increasing exposure to cyber threats. Integration challenges between legacy ERP systems and SaaS-based SCM platforms result in 15–20% higher implementation timelines. Additionally, regulatory compliance requirements across regions add operational complexity, particularly in cross-border logistics operations.

AI-enabled demand forecasting improves accuracy by up to 40%, while predictive maintenance solutions reduce equipment downtime by 28%. Emerging markets in Asia-Pacific show over 55% adoption growth in SaaS supply chain platforms among mid-sized enterprises. Digital twin-based planning solutions can simulate over 10,000 supply scenarios in minutes, offering strategic planning capabilities that were previously unavailable in legacy systems.

Modern supply chains often involve more than 200 supplier nodes across multiple geographies. Managing regulatory compliance across different jurisdictions increases operational costs by nearly 12%. Additionally, fragmented data ecosystems reduce visibility efficiency by 17%, limiting real-time decision-making capabilities. Workforce skill gaps in AI and data analytics further constrain optimal platform utilization.

Rapid AI-Driven Demand Forecasting Adoption: Over 62% of large enterprises integrated AI-based forecasting tools in 2025, improving forecast precision by 35% and reducing excess inventory by 20%.

Expansion of Blockchain Traceability Networks: Nearly 38% of multinational supply chains adopted blockchain tracking modules, cutting audit processing time by 18% and improving supplier compliance accuracy by 22%.

Growth in Digital Twin Simulation Platforms: Digital twin adoption increased by 41% across logistics-intensive sectors, enabling 30% faster risk scenario modeling and 16% improvement in response planning efficiency.

Surge in SaaS-Based SCM Migration: Around 48% of mid-sized enterprises transitioned from on-premise systems to SaaS-based SCM platforms, achieving 27% reduction in IT infrastructure costs and 19% faster system deployment timelines.

The Cloud Supply Chain Management Market is segmented by type, application, and end-user industry. Cloud-based deployment models dominate enterprise transformation strategies, while AI-enabled analytics modules are expanding rapidly across retail and manufacturing sectors. Large enterprises account for over 60% of adoption due to complex multi-tier supply networks, while SMEs show accelerating transition toward SaaS-based subscription models. Application diversity—ranging from inventory management to transportation optimization—demonstrates strong cross-industry demand supported by digital trade growth and automation expansion.

The market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud deployment models. Public cloud solutions account for approximately 46% of adoption due to scalability and lower upfront infrastructure investment. Hybrid cloud models hold around 34%, preferred by enterprises requiring regulatory compliance and sensitive data protection. Private cloud contributes nearly 20%, largely in regulated industries such as healthcare and defense. Hybrid cloud is the fastest-growing segment, expanding at nearly 15% annually due to its flexibility in balancing security and scalability. Public cloud platforms remain dominant in retail and logistics due to rapid deployment advantages and integration capabilities with AI modules. Private cloud deployments are gaining niche traction in financial and pharmaceutical sectors where compliance mandates require localized data storage. SMEs increasingly prefer public cloud solutions due to subscription-based pricing, representing 52% of SME deployments. Public cloud solutions also demonstrate stronger integration with IoT sensors and AI-powered analytics tools, enabling 30% faster deployment cycles. Hybrid models enhance disaster recovery performance by 22%, making them attractive for multinational supply chain operations spanning multiple regions. Private cloud implementations often integrate advanced encryption standards, supporting 40% stronger data governance compliance in highly regulated environments.

Applications include Inventory Management, Transportation & Logistics Management, Procurement & Sourcing, Demand Planning & Forecasting, and Warehouse Management. Inventory Management leads with approximately 29% adoption share, driven by the need to reduce carrying costs and improve stock visibility. Demand Planning & Forecasting accounts for around 24%, while Transportation & Logistics Management contributes 21%. Demand Planning is the fastest-growing application, expanding at nearly 16% annually due to AI-driven predictive tools. Warehouse Management solutions are rising rapidly with automation integration, particularly in e-commerce hubs where order volumes increased by over 30% in the past three years. Procurement & Sourcing solutions represent nearly 14% share and are increasingly integrating supplier risk analytics modules. Transportation platforms leverage route optimization algorithms, improving delivery efficiency by 18% across large enterprises. Over 38% of global enterprises reported piloting advanced SCM analytics platforms for customer experience improvement in 2025. In addition, 44% of logistics providers adopted IoT-enabled tracking tools integrated with cloud SCM systems to enhance delivery transparency.

Manufacturing remains the leading end-user segment with approximately 38% adoption share due to complex supplier ecosystems and just-in-time production requirements. Retail accounts for 27%, followed by Healthcare (14%), Logistics & Transportation (12%), and Others (9%). Retail is the fastest-growing segment, expanding at nearly 17% annually, fueled by omnichannel commerce growth and dynamic inventory needs. Healthcare institutions increasingly adopt cloud SCM to manage pharmaceutical traceability, with 42% of large hospitals integrating digital procurement platforms. Manufacturing firms report 25% improvement in supplier coordination through AI-enabled SCM dashboards. Logistics companies utilize cloud-based transportation optimization tools to reduce fuel consumption by 12%. Around 45% of SMEs across Asia-Pacific implemented SaaS SCM tools between 2023 and 2025 to enhance export efficiency. Additionally, 39% of retail enterprises globally prioritize AI-driven replenishment automation to reduce stock imbalances.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2026 and 2033.

North America’s leadership is supported by over 72% enterprise cloud adoption across large organizations and more than 65% deployment penetration in retail and manufacturing supply networks. Europe follows with approximately 26% market share, driven by regulatory-driven digital traceability mandates impacting more than 40% of cross-border trade operations. Asia-Pacific holds nearly 24% share in 2025, with over 58% of mid-sized manufacturers transitioning to SaaS-based SCM systems. South America accounts for around 7%, primarily concentrated in Brazil and Argentina, where logistics modernization investments increased by 18% in 2024. The Middle East & Africa region contributes roughly 5%, with digital procurement platforms expanding across oil & gas and construction sectors, particularly in the UAE and South Africa, where over 35% of large enterprises are investing in AI-enabled supply chain visibility tools.

North America represents approximately 38% of the global Cloud Supply Chain Management Market share in 2025, supported by strong enterprise IT spending and mature cloud ecosystems. Manufacturing, retail, healthcare, and financial services are the primary demand drivers, collectively accounting for over 62% of deployments. Regulatory frameworks such as federal cybersecurity modernization initiatives and digital procurement standards have accelerated cloud transformation across public agencies. Over 70% of Fortune 1000 companies operate hybrid or multi-cloud SCM systems. Technological advancements include AI-driven predictive demand planning, blockchain-enabled traceability, and IoT-integrated logistics dashboards, improving operational visibility by nearly 30%. SAP America has expanded AI-enabled supply chain orchestration tools across major U.S. retailers, reducing stock imbalances by over 20%. Consumer behavior shows higher enterprise adoption in healthcare and finance, where over 55% of large institutions rely on cloud-based procurement automation to meet compliance standards.

Europe holds around 26% of the global market share, with Germany, the UK, and France representing more than 60% of regional deployments. Regulatory pressure from digital trade compliance frameworks and sustainability reporting requirements impacts nearly 45% of multinational enterprises operating in the region. Over 50% of European manufacturers have integrated AI-based inventory forecasting to reduce waste and improve supply continuity. Adoption of blockchain traceability systems has increased by 32% across food and pharmaceutical sectors to meet cross-border audit requirements. Companies such as SAP SE in Germany are enhancing cloud-based digital twin capabilities, enabling up to 25% faster supply disruption simulations. Consumer and enterprise behavior indicates strong demand for explainable AI systems, with nearly 48% of enterprises prioritizing transparency and ESG-aligned reporting tools within supply chain operations.

Asia-Pacific ranks second in market volume, accounting for approximately 24% share in 2025. China, India, and Japan are the top consuming countries, collectively contributing over 70% of regional deployments. The region supports more than 50% of global manufacturing output, driving demand for scalable SaaS-based SCM systems. E-commerce transactions increased by over 30% in key economies, necessitating advanced warehouse and logistics coordination tools. Innovation hubs in Singapore, Shenzhen, and Bengaluru are accelerating AI-driven supply planning integration. Alibaba Cloud has expanded intelligent logistics platforms supporting over 10 million SMEs, improving order fulfillment efficiency by 18%. Regional consumer behavior is heavily influenced by mobile-first platforms, with over 60% of SMEs preferring subscription-based cloud SCM tools for cost-effective scalability.

South America represents approximately 7% of global market share, led by Brazil and Argentina, which together account for nearly 65% of regional demand. Infrastructure modernization programs have increased logistics digitalization spending by 16% since 2024. The energy, agriculture, and retail sectors are key adopters, representing over 55% of deployments. Government-backed trade facilitation programs have reduced customs processing time by 14%, encouraging digital procurement integration. TOTVS, a Brazil-based enterprise software provider, has expanded cloud-based supply chain solutions for over 40,000 businesses, enhancing inventory synchronization efficiency by 19%. Regional demand patterns indicate supply chain investments are closely linked to export-driven industries and localized language customization requirements for digital platforms.

The Middle East & Africa accounts for nearly 5% of global share in 2025. The UAE and South Africa lead adoption, contributing over 60% of regional deployments. Oil & gas, construction, and retail sectors represent the largest demand clusters, with more than 48% of large enterprises investing in digital supply visibility platforms. Technological modernization initiatives, including smart port and free-trade zone digitization, have improved shipment tracking accuracy by 22%. Oracle’s regional cloud expansion initiatives support AI-based procurement automation across logistics hubs in Dubai, enhancing cross-border trade efficiency. Consumer behavior reflects increasing reliance on centralized cloud dashboards, with over 35% of enterprises integrating IoT-enabled fleet management tools to improve route optimization.

United States – 34% Market Share: It is supported by high enterprise digitization rates, over 70% large enterprise cloud adoption, and strong AI-driven logistics integration.

China – 19% Market Share: It's expansion is driven by large-scale manufacturing capacity, rapid e-commerce growth exceeding 30% annually, and strong government-backed digital infrastructure programs.

The Cloud Supply Chain Management Market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 54% of total market presence. Over 120 active technology vendors compete globally, ranging from enterprise SaaS providers to niche AI-based logistics analytics startups. Market leaders emphasize AI-driven predictive analytics, digital twin simulation, and blockchain traceability integration as core competitive differentiators.

Strategic initiatives between 2023 and 2025 include over 40 partnership agreements between cloud hyperscalers and logistics providers to enhance real-time data integration capabilities. Product innovation cycles have shortened by nearly 25%, reflecting rapid advancements in generative AI-enabled supply planning tools. Mergers and acquisitions activity increased by 18% in 2024 as larger enterprise software vendors acquired AI-focused startups to strengthen analytics portfolios.

Competitive positioning is shaped by vertical specialization, with some players focusing on retail optimization while others prioritize manufacturing orchestration. Nearly 60% of vendors now offer modular SaaS pricing models to capture SME demand. Innovation-led differentiation, integration capabilities, and ecosystem partnerships remain critical success factors influencing procurement decisions across multinational enterprises.

Infor

Manhattan Associates

Kinaxis

IBM

Salesforce

Microsoft

Epicor Software Corporation

JDA Software

E2open

Descartes Systems Group

Coupa Software

Advanced technologies are fundamentally reshaping the Cloud Supply Chain Management Market. Artificial Intelligence and Machine Learning algorithms improve demand forecasting accuracy by up to 40% and reduce stock imbalances by nearly 25%. Digital twin technology enables simulation of over 10,000 supply disruption scenarios within minutes, enhancing contingency planning efficiency by 30%.

Blockchain-based traceability systems are implemented across 38% of multinational food and pharmaceutical supply chains, improving compliance audit speed by 20%. IoT-enabled asset tracking devices have expanded across more than 45% of global logistics fleets, reducing shipment losses by 12%. Robotic Process Automation integration in procurement workflows reduces manual processing time by 35%.

Generative AI tools are emerging as strategic enablers, automating supplier negotiations and predictive replenishment modeling. Nearly 42% of large enterprises are piloting AI-based autonomous procurement assistants. Cloud-native microservices architectures now account for 50% of new deployments, enabling modular scalability and API-driven ecosystem integration. Edge computing adoption is rising in warehouse automation hubs, improving real-time decision latency by 18%. These technological advancements collectively strengthen operational resilience, regulatory compliance, and sustainability performance across global supply networks.

• In May2025, SAP SE unveiled a major expansion of its AI-powered innovations for network-centric supply chain management, including advanced guided execution for manufacturing and enhanced SAP Business Network capabilities that improve visibility, compliance workflows, and real-time emissions tracking across over 190 countries. These enhancements are designed to streamline production data handovers, integrate IoT device data, and enable autonomous planning through new Joule agents set for availability by year-end. Source: www.sap.com

• In October 2025, SAP announced SAP Supply Chain Orchestration, a new solution built on SAP Business Technology Platform that provides multi-tier risk detection, AI-driven impact analysis, and intelligent response actions ahead of disruptions, along with unified scenario simulations and enhanced logistics intelligence now being rolled out through early 2026. Source: www.sap.com

• In July 2025, Oracle Corporation launched Oracle Cloud SCM Advanced Inventory Management, adding embedded AI to streamline warehouse tasks, simplify inventory transactions, and accelerate order fulfillment with real-time automation that reduces manual intervention and enhances accuracy. Source: www.oracle.com

• In September 2025, Oracle introduced new AI-powered supply chain capabilities for healthcare organizations that enhance real-time visibility into medical inventories, automate procurement workflows, and boost operational efficiency for supply chain and patient care teams using Fusion Cloud Applications. Source: www.oracle.com

The Cloud Supply Chain Management Market Report provides comprehensive coverage of deployment models including public, private, and hybrid cloud systems, addressing over 100 enterprise solution configurations. The study evaluates applications such as inventory optimization, transportation management, procurement automation, warehouse orchestration, and demand forecasting across 5 major industry verticals.

Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing over 30 key national markets. The report assesses technology integration including AI, blockchain, IoT, robotic process automation, and digital twin platforms. More than 120 competitive vendors are benchmarked based on product innovation, deployment scale, and ecosystem partnerships.

The scope further examines SME versus large enterprise adoption patterns, where large enterprises represent over 60% of implementations while SMEs demonstrate accelerating SaaS uptake. Emerging niches such as carbon-tracking supply modules and autonomous procurement bots are also evaluated. This structured and data-driven scope enables decision-makers to assess operational priorities, regulatory impacts, digital transformation pathways, and long-term investment strategies within the Cloud Supply Chain Management Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,458.0 Million |

| Market Revenue (2033) | USD 6,506.8 Million |

| CAGR (2026–2033) | 12.94% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SAP SE; Oracle Corporation; Blue Yonder; Infor; Manhattan Associates; Kinaxis; IBM; Salesforce; Microsoft; Epicor Software Corporation; JDA Software; E2open; Descartes Systems Group; Coupa Software |

| Customization & Pricing | Available on Request (10% Customization Free) |