Reports

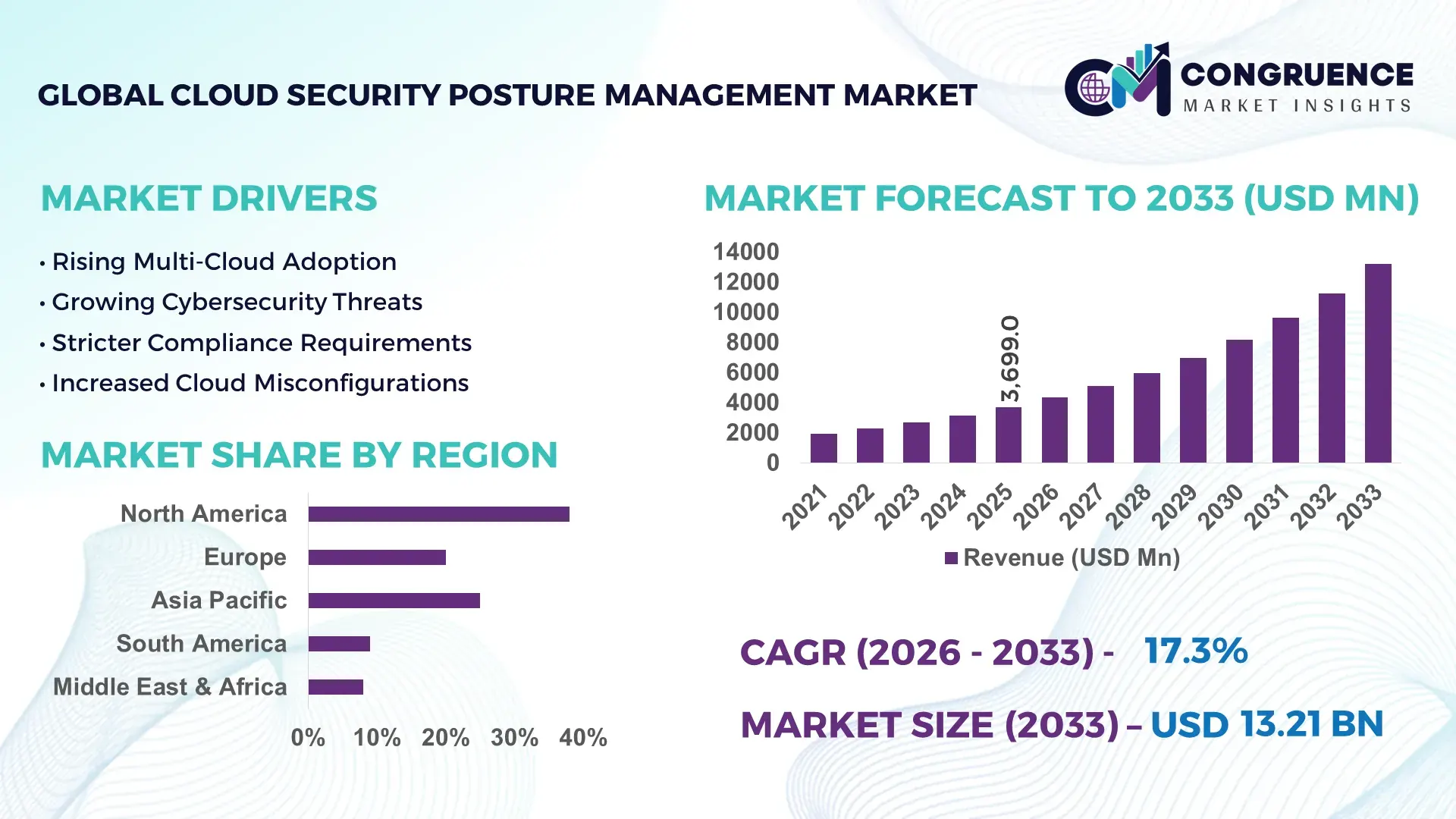

The Global Cloud Security Posture Management Market was valued at USD 3699 Million in 2025 and is anticipated to reach a value of USD 13212.57 Million by 2033 expanding at a CAGR of 17.25% between 2026 and 2033. Growth is accelerating due to multi-cloud workload expansion, stricter sovereign data compliance mandates, and rising AI-driven threat exposure across BFSI, healthcare, telecom, and public-sector cloud environments.

The United States dominates the global Cloud Security Posture Management market with nearly 38% share, supported by hyperscale cloud infrastructure, federal zero-trust modernization programs, and over USD 18 billion in enterprise cloud security spending during 2026. Financial services, defense, and healthcare organizations account for more than 46% of large-scale CSPM deployments, while automated compliance monitoring adoption exceeded 61% among Fortune 1000 enterprises. In comparison, Germany is strengthening sovereign cloud governance after escalating geopolitical cybersecurity concerns linked to critical infrastructure attacks across Europe, while India recorded over 34% annual growth in cloud-native security platform deployment driven by digital banking and SaaS expansion. Enterprises prioritizing unified posture visibility and automated remediation capabilities are securing faster audit readiness, lower breach exposure, and stronger multi-cloud governance efficiency.

Market Size & Growth: USD 3699 Million in 2025 to USD 13212.57 Million by 2033 at 17.25% growth, driven by enterprise-wide multi-cloud security consolidation and AI-powered compliance automation.

Top Growth Drivers: Multi-cloud adoption exceeded 72%, cloud compliance automation improved audit efficiency by 41%, and ransomware-led cloud misconfiguration incidents increased 29% globally.

Short-Term Forecast: By 2028, automated remediation tools are projected to reduce cloud configuration response time by 47% and lower manual security workload by 35%.

Emerging Technologies: AI-driven risk scoring, agentless scanning, and real-time Kubernetes posture management improved cloud threat detection accuracy by over 44% in enterprise deployments.

Regional Leaders: North America leads with USD 4.8 Billion potential, Europe exceeds USD 3.1 Billion through sovereign cloud expansion, and Asia-Pacific advances beyond USD 2.9 Billion due to fintech cloud migration.

Consumer/End-User Trends: Over 64% of enterprises now integrate CSPM platforms with DevSecOps pipelines to secure containerized and serverless workloads at deployment stage.

Pilot/Case Example: In 2026, a multinational banking modernization project reduced cloud misconfiguration exposure by 52% after implementing centralized posture management across hybrid environments.

Competitive Landscape: Leading vendors collectively control nearly 48% market share, with competition intensifying among platform-based cloud security providers and integrated cybersecurity suites.

Regulatory & ESG Impact: EU digital resilience policies and regional data residency mandates increased compliance-focused cloud security investments by 33% amid cross-border data governance pressure.

Investment & Funding: Global investment surpassed USD 5.4 Billion through cybersecurity acquisitions, AI-security partnerships, and regional cloud expansion across Asia-Pacific and Middle East markets.

Innovation & Future Outlook: Predictive posture analytics, autonomous remediation engines, and unified CNAPP integration are accelerating enterprise transition toward proactive cloud risk orchestration.

Advanced CSPM platforms are increasingly embedding runtime threat intelligence with infrastructure-as-code scanning, enabling enterprises to identify misconfigurations before deployment. Enterprises adopting unified cloud security operations reduced false-positive investigation cycles by nearly 31% during 2026, while regulated industries accelerated demand for policy-based remediation workflows integrated directly into DevSecOps and hybrid cloud governance frameworks.

Cloud Security Posture Management is becoming a strategic control layer for enterprises managing distributed cloud infrastructure, AI workloads, and compliance-heavy operations. As governments tighten digital sovereignty policies and enterprises accelerate hybrid cloud modernization, CSPM platforms are shifting from security tools to operational governance systems. In 2026, more than 68% of large enterprises operate across three or more cloud environments, increasing demand for centralized posture visibility and automated remediation. Financial institutions and healthcare providers are prioritizing cloud risk orchestration after repeated supply-chain cyber incidents exposed third-party configuration vulnerabilities and delayed compliance audits.

Modern AI-enabled CSPM platforms reduce cloud misconfiguration response time by nearly 45% compared with legacy manual assessment models while lowering false-positive investigation workloads by over 30%. The United States leads in large-scale enterprise deployment through integrated zero-trust frameworks, whereas Singapore and the UAE are rapidly expanding cloud-native security investments to support smart infrastructure and digital public services. Over the next three years, automated policy enforcement adoption is expected to exceed 70% among regulated industries managing containerized and serverless applications.

A major telecommunications operator in Japan recently consolidated over 12 cloud security monitoring systems into a unified CSPM environment, reducing audit preparation cycles by 40% and improving policy compliance consistency across multi-cloud assets. Vendors are responding through AI-security partnerships, sovereign cloud integrations, and platform-based expansion strategies focused on infrastructure resilience and operational automation. Enterprises that align CSPM investments with DevSecOps modernization and regulatory governance objectives are strengthening competitive positioning while improving long-term cloud scalability and risk management efficiency.

Rapid enterprise migration toward multi-cloud infrastructure is accelerating demand for centralized posture management and automated compliance monitoring. More than 71% of global enterprises now operate hybrid or multi-cloud architectures, while cloud misconfiguration incidents increased by 28% during the past year due to fragmented visibility across workloads and APIs. In the United States, federal zero-trust directives and stricter healthcare data governance rules are pushing organizations to integrate continuous compliance scanning into DevSecOps pipelines. This operational pressure is driving vendors to expand AI-based remediation capabilities and real-time policy orchestration tools. Cybersecurity providers are also forming infrastructure partnerships with hyperscale cloud operators to improve workload visibility, shorten incident response cycles, and reduce manual audit preparation by nearly 35%, strengthening enterprise cloud governance efficiency.

Interoperability limitations between legacy enterprise systems and modern cloud-native security platforms continue to slow CSPM deployment scalability. Nearly 43% of large organizations still operate mission-critical workloads on legacy infrastructure, creating fragmented visibility across hybrid environments. In Germany and Japan, strict data localization frameworks and industry-specific compliance standards increase integration timelines by over 25% for regulated sectors such as manufacturing and banking. Enterprises also face operational pressure from rising cloud monitoring costs and duplicated security tooling across disconnected environments. To reduce deployment friction, companies are localizing data-processing operations, consolidating vendors, and adopting agentless architecture models that simplify infrastructure onboarding. Strategic focus is shifting toward unified cloud governance frameworks capable of reducing operational overlap while maintaining regulatory alignment across distributed workloads.

AI-enabled automation and sovereign cloud adoption are creating high-value expansion opportunities for CSPM vendors targeting regulated industries and digital infrastructure projects. Automated remediation platforms are reducing cloud policy enforcement time by nearly 48%, while container security integration adoption surpassed 57% among enterprise DevSecOps teams in 2026. India and Saudi Arabia are expanding national cloud infrastructure investments to support digital banking, smart city deployments, and public-sector modernization, increasing demand for localized compliance monitoring tools. Vendors are investing in predictive risk analytics, runtime workload protection, and unified CNAPP integration to address complex hybrid cloud operations. A non-obvious growth area is sustainability-focused workload optimization, where intelligent posture management reduces redundant compute allocation and improves cloud resource efficiency by over 20% in high-density enterprise environments.

Long-term scalability remains constrained by shortages in cloud-native cybersecurity expertise and growing complexity in policy enforcement across distributed infrastructure. More than 52% of enterprises report difficulties managing real-time compliance across containerized workloads, while security operations teams handle nearly 3 times more cloud alerts than traditional on-premise environments. In the United Kingdom and Canada, evolving AI governance regulations are forcing organizations to redesign cloud security controls without disrupting operational continuity. The rapid expansion of edge computing and serverless applications is also increasing enforcement inconsistency across decentralized assets. Companies are responding through automated orchestration, managed security partnerships, and workforce upskilling investments focused on cloud governance engineering. Organizations that fail to standardize policy automation and cloud visibility frameworks risk slower deployment cycles, weaker compliance readiness, and reduced infrastructure resilience.

AI-Led Remediation Expansion Enterprises are accelerating adoption of AI-driven remediation engines to reduce cloud response latency and alert fatigue. Automated policy correction deployments increased by 46% during 2026, while false-positive investigation workloads declined by nearly 32% across large-scale hybrid environments. Financial institutions in the United States are restructuring security operations around autonomous orchestration workflows to support continuous compliance and faster incident prioritization. Vendors are expanding AI-security partnerships and embedding predictive analytics directly into cloud governance platforms to improve operational scalability.

Container Security Integration Surge Kubernetes and containerized workload growth are reshaping CSPM deployment priorities across telecom and SaaS infrastructure. More than 58% of enterprise DevSecOps teams now integrate posture management tools directly into CI/CD pipelines, reducing deployment misconfigurations by 37%. In India and Singapore, cloud-native application expansion is increasing demand for runtime posture monitoring and infrastructure-as-code scanning. Security vendors are consolidating CNAPP capabilities through acquisitions and unified platform strategies to simplify container governance and reduce fragmented security tooling.

Sovereign Cloud Compliance Focus Data residency mandates and digital sovereignty policies are driving localized CSPM deployment models. Germany and the UAE strengthened cloud governance frameworks during 2026, increasing enterprise demand for region-specific compliance automation by over 34%. Organizations handling regulated workloads are prioritizing localized monitoring architecture and encrypted workload visibility to avoid cross-border data exposure risks. Providers are responding through sovereign cloud alliances, regional data-processing hubs, and country-specific compliance templates aligned with evolving cybersecurity legislation.

Operational Consolidation Strategies Enterprises are reducing overlapping security infrastructure to improve visibility and lower operational complexity. Nearly 41% of multinational organizations consolidated multiple cloud monitoring tools into unified posture management environments during 2026, shortening audit preparation cycles by 29%. Labor shortages in cybersecurity operations are also accelerating demand for centralized governance dashboards and automated workflow integration. Vendors are scaling managed security partnerships and platform-based ecosystems to support enterprise-wide cloud governance while improving security team productivity and infrastructure resilience.

Risk Assessment Solutions dominate the Cloud Security Posture Management market due to their scalability across hybrid infrastructure, centralized visibility capabilities, and integration efficiency with SIEM and DevSecOps frameworks. More than 44% of large enterprises prioritize risk-based posture analytics to reduce cloud misconfiguration exposure and accelerate compliance readiness. Configuration Monitoring Tools remain widely deployed in mature enterprise environments because they support continuous asset visibility and policy enforcement across distributed workloads. However, Threat Detection Platforms are emerging as the fastest-growing segment, driven by AI-enabled anomaly detection and runtime workload protection adoption that improved incident response efficiency by nearly 36% during 2026. Identity and Access Management platforms are gaining traction through zero-trust security modernization, particularly within financial services and public-sector infrastructure. Compliance Management Tools continue expanding in Germany, Japan, and the UAE as stricter sovereign cloud mandates increase demand for automated audit reporting and region-specific governance controls. Vendors are strengthening competitive positioning through integrated CNAPP development, AI partnerships, and unified cloud governance architecture expansion.

Cloud Compliance Monitoring remains the leading application segment as enterprises prioritize continuous regulatory visibility across multi-cloud infrastructure and containerized workloads. More than 61% of regulated organizations integrated automated compliance workflows into cloud operations during 2026 to reduce manual audit preparation and policy enforcement delays. Security Automation is the fastest-growing application segment, driven by AI-enabled remediation and orchestration platforms that lowered cloud incident response time by nearly 42% compared with manual workflows. Threat Detection continues gaining operational relevance within telecom and SaaS environments managing real-time cloud-native applications and API-heavy ecosystems. Vulnerability Management adoption is also strengthening as enterprises integrate posture management with runtime workload scanning to reduce exploit exposure. Data Protection and Risk Management applications remain strategically important for healthcare and banking institutions handling sensitive cross-border information. Companies are expanding automation capabilities, embedding posture analytics into DevSecOps pipelines, and scaling unified governance platforms to improve compliance consistency and operational resilience across hybrid cloud environments.

BFSI represents the leading end-user segment due to high transaction volumes, stringent regulatory obligations, and extensive dependence on hybrid cloud infrastructure for digital banking operations. More than 66% of large financial institutions implemented continuous cloud posture monitoring across customer-facing workloads during 2026 to reduce compliance gaps and third-party exposure risks. Healthcare is emerging as the fastest-growing end-user category as hospitals and digital care providers accelerate cloud migration for patient analytics and telehealth systems, increasing demand for automated data governance and workload visibility tools. IT and Telecom companies continue expanding CSPM deployment through large-scale containerized infrastructure modernization and 5G service integration. Government agencies are strengthening sovereign cloud governance capabilities following critical infrastructure cybersecurity incidents, while Manufacturing and Retail sectors increasingly adopt posture management tools to secure IoT-connected operations and omnichannel commerce systems. Vendors are targeting these sectors through industry-specific compliance templates, flexible subscription models, and strategic hyperscaler partnerships focused on operational continuity and scalable cloud governance.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.4% between 2026 and 2033.

Enterprise-Scale Zero-Trust Modernization Accelerates Deployment

North America maintains leadership in Cloud Security Posture Management through high enterprise cloud density, advanced cybersecurity infrastructure, and large-scale zero-trust modernization initiatives. The region contributes nearly 38% of global deployment activity, supported by strong adoption across BFSI, healthcare, defense, and telecom sectors. More than 64% of Fortune 1000 enterprises integrated automated cloud compliance monitoring into hybrid infrastructure operations during 2026. Regulatory pressure around critical infrastructure resilience and third-party SaaS governance is also increasing investment in unified CNAPP and AI-enabled remediation platforms. Strategic partnerships between hyperscale cloud providers and cybersecurity vendors are strengthening workload visibility and accelerating automated policy enforcement across containerized and multi-cloud environments.

United States Market Outlook: The United States leads regional deployment through extensive enterprise cloud migration, mature cybersecurity spending patterns, and rapid AI infrastructure expansion. Large financial institutions and federal agencies are prioritizing automated posture governance following increased API-related security exposure across cloud-native environments. More than 61% of enterprise security teams in the country adopted integrated DevSecOps security orchestration during 2026, while hyperscale cloud operators expanded sovereign workload protection capabilities to support regulated industries and defense-linked digital infrastructure modernization.

Sovereign Cloud Governance Reshapes Security Architecture

Europe is strengthening its Cloud Security Posture Management position through digital sovereignty regulations, cross-border compliance enforcement, and industrial cybersecurity modernization. The region accounts for approximately 27% of global CSPM deployment concentration, with Germany, France, and the United Kingdom leading enterprise implementation activity. Stricter cloud governance frameworks increased demand for automated compliance validation and localized data monitoring by over 33% during 2026. Financial services and manufacturing organizations are prioritizing region-specific policy enforcement tools to maintain operational continuity across distributed cloud infrastructure. Security vendors are expanding regional cloud-processing partnerships and encrypted workload visibility solutions to align with evolving European cybersecurity legislation and critical infrastructure protection requirements.

Germany Market Outlook: Germany remains the region’s strongest operational hub due to advanced industrial digitization, strict enterprise compliance requirements, and high manufacturing cloud integration levels. Automotive, industrial automation, and banking sectors are accelerating deployment of AI-driven posture monitoring platforms to secure connected production environments and sensitive operational technology assets. Nearly 49% of large enterprises in Germany expanded sovereign cloud security investments during 2026 to address cross-border data governance complexity and improve resilience across hybrid industrial infrastructure systems.

Cloud-Native Expansion Drives Rapid Adoption

Asia-Pacific is emerging as the fastest-scaling Cloud Security Posture Management market due to aggressive digital infrastructure expansion, fintech modernization, and large-scale cloud-native application deployment. The region represents nearly 24% of global implementation activity, with India, China, Japan, and Singapore driving enterprise cloud security transformation. More than 58% of regional enterprises expanded containerized workload operations during 2026, increasing demand for runtime posture management and infrastructure-as-code scanning capabilities. Telecom providers and digital banking operators are investing heavily in AI-enabled security automation to improve compliance efficiency and reduce operational downtime. Cloud security vendors are expanding local partnerships, managed services, and sovereign compliance capabilities to support rising enterprise demand across rapidly digitizing economies.

India Market Outlook: India is strengthening its strategic position through rapid SaaS ecosystem growth, large-scale digital banking expansion, and aggressive public cloud adoption among mid-sized enterprises. Financial institutions and IT service providers are prioritizing automated compliance monitoring to manage high-volume API-driven cloud operations and customer data governance requirements. More than 34% annual growth in cloud-native workload deployment during 2026 accelerated enterprise investment in AI-enabled threat visibility, DevSecOps integration, and unified posture management platforms supporting scalable hybrid infrastructure environments.

Financial Sector Digitization Expands Security Demand

South America is witnessing rising Cloud Security Posture Management adoption through banking digitization, e-commerce infrastructure growth, and expanding hybrid cloud deployment across enterprise operations. The region contributes nearly 6% of global market activity, with Brazil and Chile leading cloud governance modernization initiatives. More than 41% of large enterprises increased cloud compliance automation spending during 2026 to address ransomware exposure and fragmented security visibility across third-party SaaS environments. Infrastructure limitations and uneven cybersecurity workforce availability continue creating deployment complexity for mid-sized organizations. Vendors are responding through managed cloud security partnerships, localized service delivery models, and lower-complexity posture monitoring platforms designed for regional enterprise scalability and operational flexibility.

Brazil Market Outlook: Brazil dominates regional demand through advanced digital banking infrastructure, expanding retail cloud adoption, and strong enterprise modernization activity. Financial institutions and telecom operators are integrating posture management platforms into centralized cybersecurity operations to improve compliance efficiency and cloud risk visibility. During 2026, enterprise adoption of automated cloud governance tools increased by nearly 37% as organizations responded to stricter data protection enforcement and growing operational dependence on hybrid cloud environments supporting digital consumer services.

Digital Infrastructure Investments Accelerate Modernization

Middle East & Africa is expanding Cloud Security Posture Management deployment through smart city programs, sovereign cloud investments, and public-sector digital transformation initiatives. The region accounts for approximately 5% of global implementation activity, with the UAE and Saudi Arabia leading cloud governance modernization. Government-backed digital infrastructure projects increased enterprise demand for automated compliance monitoring and encrypted workload visibility by over 31% during 2026. Financial services, energy, and telecom sectors are prioritizing AI-enabled posture management to secure high-volume cloud operations and interconnected infrastructure assets. Vendors are establishing regional cybersecurity partnerships and localized cloud-processing environments to support sovereign data governance and improve operational resilience across critical infrastructure systems.

United Arab Emirates Market Outlook: The UAE is positioning itself as a regional cloud security hub through advanced smart infrastructure deployment, strong hyperscale cloud partnerships, and aggressive public-sector digitization programs. Banking, aviation, and government organizations are accelerating investment in unified cloud governance platforms to support sovereign data protection objectives and AI-driven operational systems. More than 46% of enterprise cloud transformation projects initiated during 2026 incorporated automated posture management and continuous compliance monitoring capabilities from the initial deployment stage.

Global cybersecurity leaders including Palo Alto Networks, Check Point Software Technologies, Fortinet, Trend Micro, and CrowdStrike compete directly with cloud-native specialists and platform-integrated security providers focused on AI-enabled posture governance. The top five players collectively control nearly 49% of market activity through broad cloud ecosystem integration, automated remediation capabilities, and enterprise-scale compliance orchestration. Competition is increasingly shaped by detection speed, multi-cloud visibility, deployment flexibility, and policy automation efficiency, with AI-driven remediation reducing incident response workloads by over 35% in advanced enterprise deployments. Major vendors are expanding through hyperscaler partnerships, CNAPP consolidation strategies, and sovereign cloud integration programs targeting regulated industries. Regional providers in India, Israel, and the UAE are differentiating through localized compliance customization and lower deployment complexity. Consolidation pressure remains strong as enterprises reduce overlapping security tooling. Winning requires scalable automation, unified workload visibility, deep DevSecOps integration, and operational alignment with evolving regulatory governance frameworks globally.

Palo Alto Networks

Check Point Software Technologies

Fortinet

Trend Micro

CrowdStrike

Microsoft

IBM

Cisco Systems

Wiz

Orca Security

Rapid7

Tenable

SentinelOne

Qualys

March 2025 – Google announced a USD 32 billion acquisition agreement for Wiz to strengthen multi-cloud security capabilities, while Wiz maintained support across AWS and Azure environments, intensifying hyperscale cloud security competition globally. Source: reuters.com

July 2025 – Wiz expanded its Wiz Integration Network beyond 200 integrations, accelerating cloud-native interoperability and automated posture management workflows, enabling enterprises to reduce fragmented security tooling and improve operational coordination across hybrid infrastructures. Source: wiz.io

September 2025 – Check Point and Wiz launched an integrated CNAPP and cloud network security solution delivering AI-powered prevention with real-time visibility, strengthening unified remediation capabilities for enterprises managing complex multi-cloud application environments. Source: checkpoint.com

April 2026 – Palo Alto Networks expanded hybrid multicloud security integration with Nutanix, enabling automated Layer 7 visibility and AI workload protection while supporting scalable zero-trust enforcement across distributed enterprise infrastructure environments. Source: paloaltonetworks.com

AI-driven remediation, agentless scanning, and unified CNAPP architecture are reshaping Cloud Security Posture Management operations across hybrid and multi-cloud environments. Enterprises deploying automated posture orchestration reduced cloud misconfiguration response time by nearly 45% compared with legacy manual assessment workflows. More than 61% of regulated organizations integrated continuous compliance validation into DevSecOps pipelines during 2026, accelerating audit readiness and reducing operational friction. Integrated CSPM and DSPM deployment is also improving sensitive data visibility across distributed workloads and API-connected infrastructure.

Emerging technologies including runtime Kubernetes protection, infrastructure-as-code scanning, and identity-centric posture analytics are expanding enterprise security coverage. AI-powered risk prioritization platforms lowered false-positive investigation workloads by over 30%, while automated policy enforcement improved cloud governance efficiency by nearly 38%. Enterprises in the United States, Singapore, and Germany are prioritizing unified visibility across cloud infrastructure, identities, and workloads to support zero-trust modernization. Vendors competing through open integration ecosystems and predictive analytics capabilities are gaining stronger positioning among large-scale telecom, BFSI, and healthcare operators.

Between 2026 and 2028, AI security governance, autonomous remediation engines, and cloud-native workload protection will become operationally critical as enterprises expand generative AI infrastructure and containerized applications. Organizations implementing integrated posture management and runtime protection frameworks are expected to reduce manual compliance processing by over 40% while improving deployment consistency across distributed environments. Competitive advantage will increasingly depend on scalable automation, workload intelligence, and seamless integration across code, cloud, identity, and data governance operations.

The Cloud Security Posture Management Market report delivers strategic analysis across key solution categories including Risk Assessment Solutions, Compliance Management Tools, Threat Detection Platforms, Identity and Access Management, and Configuration Monitoring Tools. The study evaluates operational deployment trends across Cloud Compliance Monitoring, Security Automation, Risk Management, Data Protection, and Vulnerability Management applications. More than 60% of enterprise cloud security investments are concentrated within automated governance and AI-enabled remediation capabilities, reflecting rapid transition toward unified multi-cloud security operations.

The report covers major end-user sectors including BFSI, Healthcare, IT and Telecom, Government, Retail, and Manufacturing across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It assesses enterprise adoption behavior, infrastructure modernization trends, sovereign cloud developments, and cloud-native workload expansion between 2026 and 2033. Strategic insights include competitive positioning, deployment scalability, partnership activity, DevSecOps integration, compliance automation, and emerging CNAPP ecosystem evolution supporting investment planning, expansion strategy, and operational decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3699 Million |

|

Market Revenue in 2033 |

USD 13212.57 Million |

|

CAGR (2026 - 2033) |

17.25% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Palo Alto Networks, Check Point Software Technologies, Fortinet, Trend Micro, CrowdStrike, Microsoft, IBM, Cisco Systems, Wiz, Orca Security, Rapid7, Tenable, SentinelOne, Qualys |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |