Reports

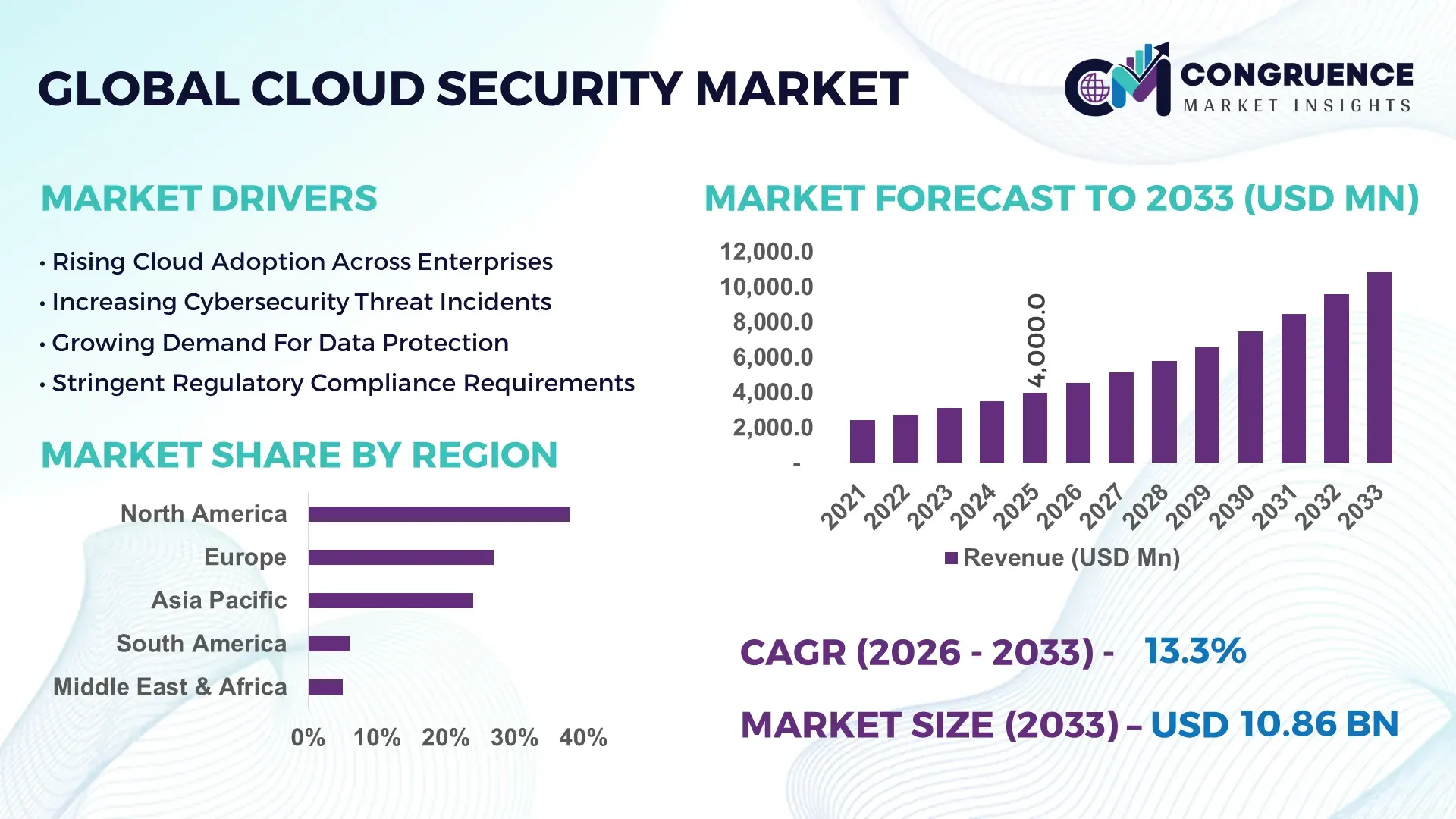

The Global Cloud Security Market was valued at USD 4,000.0 Million in 2025 and is anticipated to reach a value of USD 10,861.7 Million by 2033 expanding at a CAGR of 13.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing enterprise migration to hybrid and multi-cloud environments, necessitating advanced threat detection and compliance solutions.

In the United States, the Cloud Security Market demonstrates strong technological maturity supported by over 92% enterprise cloud adoption across large organizations. The country hosts more than 35% of global hyperscale data centers, with investments exceeding USD 75 billion annually in cloud infrastructure and cybersecurity capabilities. Key applications span BFSI, healthcare, and defense, where over 68% of organizations deploy zero-trust architectures and AI-based threat intelligence platforms. Additionally, more than 60% of Fortune 500 companies have integrated cloud-native security tools such as CNAPP and CASB solutions, while automation-driven security operations have reduced incident response time by approximately 40%, highlighting strong technological advancement and operational efficiency.

Market Size & Growth: USD 4,000.0 Million in 2025, projected to reach USD 10,861.7 Million by 2033 at 13.3% CAGR, driven by rising cyberattack frequency and cloud adoption.

Top Growth Drivers: 72% enterprise cloud adoption, 65% increase in ransomware incidents, 58% rise in remote workforce security needs.

Short-Term Forecast: By 2028, automated cloud security solutions expected to reduce breach response time by 45%.

Emerging Technologies: AI-driven threat detection, Zero Trust Architecture, Cloud-Native Application Protection Platforms (CNAPP).

Regional Leaders: North America (~USD 4.5 Billion by 2033), Asia-Pacific (~USD 3.2 Billion), Europe (~USD 2.6 Billion); APAC shows fastest enterprise onboarding.

Consumer/End-User Trends: BFSI and healthcare sectors account for over 55% of demand due to compliance-heavy workloads.

Pilot or Case Example: In 2025, a global bank reduced cloud security incidents by 38% using AI-driven anomaly detection.

Competitive Landscape: Market leader holds ~18% share, followed by IBM, Cisco, Palo Alto Networks, and Check Point.

Regulatory & ESG Impact: Over 70% enterprises aligning with GDPR, HIPAA, and ESG cybersecurity mandates.

Investment & Funding Patterns: Over USD 20 billion invested globally in cloud security startups and infrastructure in recent years.

Innovation & Future Outlook: Integration of AI, edge security, and quantum-resistant encryption shaping long-term evolution.

Cloud Security Market is driven by BFSI (32%), healthcare (21%), and IT & telecom (18%) sectors, supported by increasing zero-trust deployment and AI-driven threat intelligence. Regulatory mandates such as GDPR and data localization laws are accelerating adoption, while North America leads consumption and Asia-Pacific shows rapid enterprise onboarding growth. Emerging trends include CNAPP integration and automation-led security orchestration, positioning the market for scalable and resilient digital infrastructure expansion.

The Cloud Security Market holds critical strategic importance as enterprises increasingly transition toward digital-first business models and distributed cloud environments. Organizations are prioritizing security frameworks such as Zero Trust Architecture, which delivers nearly 35% improvement in breach prevention compared to traditional perimeter-based security models. Additionally, AI-powered security analytics platforms are reducing threat detection time by over 50%, enabling proactive risk mitigation across complex cloud infrastructures.

From a regional perspective, North America dominates in volume due to its large-scale enterprise deployments, while Asia-Pacific leads in adoption with over 64% of enterprises accelerating cloud-first strategies. This divergence highlights both maturity and expansion opportunities across global markets. By 2028, AI-driven security automation is expected to reduce operational security costs by nearly 30%, improving efficiency and scalability for enterprises managing hybrid environments.

Compliance and ESG considerations are increasingly shaping market strategies, with firms committing to measurable cybersecurity resilience targets such as 40% reduction in breach-related emissions and energy-efficient data protection systems by 2030. In 2025, a leading U.S. financial institution achieved a 42% reduction in security incidents through implementation of AI-based behavioral analytics, demonstrating the tangible impact of advanced security frameworks.

Looking ahead, the Cloud Security Market is poised to serve as a foundational pillar for digital resilience, regulatory compliance, and sustainable enterprise growth, supported by continuous innovation in automation, encryption, and intelligent threat detection technologies.

The Cloud Security Market is characterized by rapid technological evolution, increasing cyber threats, and expanding enterprise reliance on cloud computing ecosystems. Organizations across industries are adopting multi-cloud and hybrid cloud strategies, with over 75% of enterprises operating in multi-cloud environments, thereby increasing the complexity of securing distributed workloads. The demand for advanced solutions such as Cloud Access Security Brokers (CASB), Secure Access Service Edge (SASE), and Cloud-Native Application Protection Platforms (CNAPP) is rising significantly.

Moreover, regulatory compliance requirements such as GDPR, HIPAA, and regional data protection laws are influencing purchasing decisions, with more than 68% of enterprises prioritizing compliance-driven security investments. The market is also witnessing a surge in AI-based threat detection systems, which have demonstrated up to 60% faster anomaly detection compared to traditional systems. Additionally, the growing number of IoT-connected devices, exceeding 15 billion globally, is further intensifying the need for scalable cloud security frameworks. Overall, the market is driven by innovation, regulatory mandates, and increasing digital transformation initiatives across industries.

The increasing frequency and sophistication of cyberattacks are a primary driver of the Cloud Security Market. Global ransomware incidents have increased by over 65% in recent years, with cloud-based environments becoming a major target due to their scalability and accessibility. More than 70% of enterprises have reported at least one cloud security breach, prompting organizations to invest heavily in advanced security solutions. AI-driven threat detection systems are now capable of identifying anomalies with up to 95% accuracy, significantly reducing potential damage. Additionally, phishing attacks targeting cloud credentials have risen by 45%, further highlighting vulnerabilities in cloud ecosystems. Enterprises are responding by deploying multi-factor authentication, encryption protocols, and zero-trust frameworks, which have reduced unauthorized access incidents by approximately 50%. The growing need to safeguard sensitive data and ensure business continuity is therefore driving widespread adoption of cloud security technologies.

Despite strong growth, integration challenges remain a significant restraint for the Cloud Security Market. Organizations often operate across multiple cloud platforms, with over 60% using hybrid or multi-cloud environments, leading to fragmented security architectures. Integrating diverse security tools across platforms can increase operational complexity by nearly 40%, resulting in inefficiencies and gaps in threat visibility. Additionally, legacy IT infrastructure poses compatibility issues, with around 48% of enterprises reporting difficulties in aligning traditional systems with modern cloud security frameworks. The shortage of skilled cybersecurity professionals further compounds this challenge, as over 3.5 million positions remain unfilled globally. Misconfigurations in cloud environments, responsible for nearly 30% of security incidents, highlight the risks associated with improper integration. These challenges can delay deployment timelines and increase costs, limiting the full-scale adoption of advanced cloud security solutions across enterprises.

AI-driven automation presents significant growth opportunities within the Cloud Security Market by enhancing operational efficiency and threat intelligence capabilities. Automated security platforms can reduce incident response times by up to 70%, enabling organizations to address threats in real time. More than 55% of enterprises are actively investing in AI-based security tools to improve detection accuracy and reduce manual intervention. Additionally, predictive analytics powered by machine learning can identify potential vulnerabilities before exploitation, reducing breach risks by approximately 40%. The increasing adoption of DevSecOps practices, implemented by over 50% of organizations, is further driving demand for integrated security solutions across the software development lifecycle. Emerging technologies such as autonomous security operations centers (SOCs) and behavior-based analytics are creating new revenue streams and expanding market scope. These innovations are enabling organizations to build scalable, adaptive, and resilient cloud security infrastructures.

Evolving regulatory requirements present a major challenge for the Cloud Security Market, as organizations must comply with diverse and frequently changing data protection laws across regions. Over 80 countries have implemented data localization regulations, requiring enterprises to store and process data within specific geographic boundaries. Compliance costs have increased by nearly 25% for multinational organizations managing cross-border operations. Additionally, regulatory frameworks such as GDPR impose strict penalties, with fines reaching up to 4% of global turnover for non-compliance. The complexity of maintaining compliance across multiple jurisdictions is further intensified by the rapid pace of technological change, making it difficult for organizations to keep security policies updated. Furthermore, approximately 62% of enterprises report challenges in aligning cloud security practices with regulatory requirements, leading to delays in deployment and increased risk exposure. These factors collectively hinder seamless market expansion.

Rapid Adoption of Zero Trust Security Models: Over 68% of enterprises have adopted Zero Trust frameworks, reducing unauthorized access incidents by nearly 50%. Organizations implementing identity-based access controls report a 35% improvement in threat prevention efficiency, particularly in finance and healthcare sectors where data sensitivity is critical.

Surge in AI-Powered Threat Detection Systems: Approximately 61% of cloud security platforms now integrate AI capabilities, enabling real-time anomaly detection with up to 95% accuracy. Enterprises leveraging AI-driven tools have observed a 45% reduction in false positives, significantly improving security operations efficiency.

Expansion of Multi-Cloud Security Strategies: More than 75% of enterprises operate in multi-cloud environments, increasing demand for unified security solutions. Organizations adopting integrated security platforms report a 30% improvement in visibility across cloud assets and a 25% reduction in misconfiguration risks.

Growth in Cloud-Native Security Platforms (CNAPP): Adoption of CNAPP solutions has increased by 52%, driven by the need to secure containerized and serverless environments. These platforms enable end-to-end workload protection, reducing vulnerability exposure by nearly 40% while improving compliance monitoring efficiency by 33%.

The Cloud Security Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across industries and technologies. Organizations are increasingly selecting integrated security solutions that align with their cloud infrastructure strategies, with over 70% preferring unified platforms over standalone tools. Type segmentation highlights a shift toward advanced solutions such as identity and access management and data security, driven by rising cyber threats and compliance requirements.

Application-wise, sectors such as BFSI, healthcare, and IT & telecom dominate usage due to high data sensitivity and regulatory pressures. Over 60% of enterprises in these industries prioritize cloud security investments to ensure data protection and operational continuity. End-user segmentation reveals strong demand from large enterprises, which account for the majority of deployments due to complex IT environments, while small and medium enterprises are rapidly increasing adoption through scalable and cost-effective solutions. Overall, segmentation reflects a dynamic market driven by technological innovation, regulatory compliance, and industry-specific security requirements.

The Cloud Security Market by type includes Identity and Access Management (IAM), Data Security, Network Security, Endpoint Security, Application Security, and Others. Among these, Identity and Access Management leads the segment, accounting for approximately 34% of total adoption due to its critical role in managing user authentication and enforcing zero-trust policies. IAM solutions are widely implemented across enterprises to control access across distributed cloud environments, especially with over 70% of organizations adopting multi-cloud strategies. Data Security follows with nearly 26% share, driven by increasing regulatory compliance requirements and rising incidents of data breaches. Network Security and Application Security collectively contribute around 28%, focusing on securing cloud infrastructure and application layers. Endpoint Security remains niche but relevant, especially with the rise in remote workforce environments. The fastest-growing segment is Application Security, expanding at an estimated CAGR of 15.2%, driven by the rapid adoption of cloud-native applications, containers, and DevSecOps practices. Organizations are prioritizing application-layer protection to mitigate vulnerabilities in modern software development pipelines. The remaining segments collectively account for approximately 12% of the market, addressing specialized use cases such as workload protection and security analytics.

The Cloud Security Market by application includes BFSI, Healthcare, IT & Telecom, Retail & E-commerce, Government, and Others. BFSI leads the segment with approximately 32% share due to the high sensitivity of financial data and strict regulatory compliance requirements. Financial institutions increasingly deploy encryption, identity management, and AI-based threat detection systems to mitigate risks associated with digital transactions and online banking. Healthcare accounts for nearly 21% share, driven by the need to secure electronic health records and patient data. IT & Telecom contributes around 19%, as cloud infrastructure providers and telecom operators adopt advanced security frameworks to protect large-scale networks. Retail & E-commerce and Government sectors together account for approximately 20%, focusing on customer data protection and national cybersecurity initiatives. The fastest-growing application is Retail & E-commerce, expanding at a CAGR of 16.1%, supported by the surge in digital transactions and online platforms. In 2025, more than 42% of enterprises globally reported deploying cloud security solutions for customer experience platforms, while over 58% of consumers preferred brands with strong data protection policies.

The Cloud Security Market by end-user includes Large Enterprises and Small & Medium Enterprises (SMEs). Large enterprises dominate the segment with approximately 64% share due to their complex IT infrastructures and higher exposure to cyber threats. These organizations invest heavily in advanced cloud security solutions such as zero-trust frameworks, AI-driven analytics, and integrated security platforms to protect large-scale operations. SMEs account for around 36% of the market, increasingly adopting cloud security solutions due to the availability of scalable and cost-effective services. The rise in cyberattacks targeting smaller businesses, with over 43% of attacks focused on SMEs, has accelerated adoption rates. The fastest-growing segment is SMEs, expanding at an estimated CAGR of 14.7%, driven by digital transformation initiatives and increasing awareness of cybersecurity risks. In 2025, more than 48% of SMEs globally reported adopting cloud-based security solutions, while 61% of enterprises emphasized automation in security operations.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2026 and 2033.

The market demonstrates strong regional variation, with North America driven by high enterprise cloud adoption exceeding 90% among large organizations and widespread deployment of zero-trust frameworks across sectors such as BFSI and healthcare. Europe follows with approximately 27% share, supported by strict regulatory frameworks such as GDPR and increasing investments in data protection technologies. Asia-Pacific holds around 24% share, with countries like China, India, and Japan witnessing rapid cloud infrastructure expansion and over 65% enterprise adoption rates. South America and the Middle East & Africa collectively contribute about 11%, with increasing digital transformation initiatives and government-led cybersecurity programs driving adoption. Regional growth is also influenced by rising cyber threats, with over 70% of organizations globally reporting cloud-related security incidents, emphasizing the need for advanced security solutions across all regions.

North America holds approximately 38% of the Cloud Security Market, driven by strong enterprise adoption across industries such as BFSI, healthcare, and IT. Over 92% of large organizations in the region utilize cloud platforms, creating high demand for advanced security solutions. Regulatory frameworks such as HIPAA and CCPA have increased compliance-driven investments, with more than 70% of enterprises prioritizing data protection initiatives. Technological advancements such as AI-driven threat detection and zero-trust architecture are widely adopted, with over 65% of enterprises implementing automated security solutions. A key player, Palo Alto Networks, has expanded its cloud-native security offerings, enabling enterprises to secure multi-cloud environments more effectively. Consumer behavior in the region reflects higher enterprise adoption, particularly in healthcare and finance, where data sensitivity is critical. Additionally, over 60% of organizations report improved operational efficiency through integrated cloud security platforms.

Europe accounts for approximately 27% of the Cloud Security Market, driven by strong regulatory enforcement and increasing digital transformation initiatives. Key markets such as Germany, the UK, and France lead adoption, with over 68% of enterprises implementing cloud-based solutions. Regulatory bodies enforcing GDPR have significantly influenced market growth, with more than 75% of organizations prioritizing compliance-driven security investments. The adoption of emerging technologies such as AI and encryption-based security solutions is rising, with nearly 58% of enterprises integrating advanced threat detection systems. A notable regional player, SAP, has enhanced its cloud security portfolio to support enterprise compliance requirements across Europe. Consumer behavior reflects strong demand for explainable and compliant security solutions, with regulatory pressure driving innovation and adoption.

Asia-Pacific represents around 24% of the Cloud Security Market and ranks as the fastest-growing region in terms of adoption. Countries such as China, India, and Japan are leading consumption, with enterprise cloud adoption exceeding 65% in major economies. Infrastructure expansion is significant, with over 40% increase in regional data center capacity and rising investments in digital transformation initiatives. Technology hubs in India and Southeast Asia are fostering innovation in AI-driven security solutions, with over 55% of enterprises adopting automated security platforms. A key regional player, Trend Micro, is actively developing advanced cloud security solutions tailored for regional enterprises. Consumer behavior indicates growth driven by e-commerce and mobile-based applications, with over 70% of digital transactions requiring secure cloud environments.

South America accounts for approximately 6% of the Cloud Security Market, with Brazil and Argentina leading regional adoption. The region is witnessing increasing demand for cloud security solutions driven by digital transformation initiatives across banking, retail, and government sectors. Infrastructure development is accelerating, with over 45% of enterprises adopting cloud platforms to enhance operational efficiency. Government incentives and trade policies are encouraging cybersecurity investments, particularly in Brazil where national digitalization programs are expanding rapidly. A local player, Stefanini, is enhancing its cloud security offerings to support enterprise adoption. Consumer behavior reflects demand tied to media, fintech, and language localization platforms, with over 52% of businesses prioritizing data protection strategies.

The Middle East & Africa region contributes approximately 5% of the Cloud Security Market, driven by increasing adoption of cloud technologies across industries such as oil & gas, construction, and finance. Countries like the UAE and South Africa are leading growth, with over 48% enterprise cloud adoption rates. Technological modernization is evident, with governments investing in smart city initiatives and digital infrastructure. Over 50% of organizations in the region are implementing cybersecurity frameworks to protect critical infrastructure. A regional player, DarkMatter, is focusing on advanced cybersecurity solutions tailored for government and enterprise sectors. Consumer behavior indicates rising awareness of cybersecurity, with increasing demand for secure cloud solutions across industries.

United States – 34% Market share: Strong enterprise adoption, high cloud infrastructure investment, and advanced cybersecurity frameworks drive the Cloud Security Market.

China – 18% Market share: Rapid digital transformation, expanding data center infrastructure, and strong government-backed cloud initiatives support growth.

The Cloud Security Market is moderately fragmented, with over 120 active global and regional players competing across various solution categories such as IAM, CASB, CNAPP, and SASE platforms. The top five companies collectively account for approximately 42% of the market, indicating a mix of consolidation and competitive diversity. Leading players are focusing on strategic partnerships, acquisitions, and product innovation to strengthen their market position.

For instance, major companies are investing heavily in AI-driven threat detection and automation, with over 60% of new product launches incorporating machine learning capabilities. Partnerships between cloud service providers and cybersecurity firms have increased by nearly 35%, enabling integrated and scalable security solutions for enterprises. Additionally, mergers and acquisitions activity has risen by 28%, reflecting the need for portfolio expansion and technological advancement.

Innovation remains a key competitive factor, with companies prioritizing zero-trust architecture, encryption technologies, and cloud-native security platforms. The market also shows strong competition in pricing and service differentiation, particularly among mid-sized vendors targeting SMEs. Overall, the competitive landscape is dynamic, driven by continuous innovation, strategic collaborations, and increasing demand for comprehensive cloud security solutions.

Amazon Web Services (AWS)

Google Cloud

IBM

Cisco Systems

Palo Alto Networks

Check Point Software Technologies

Fortinet

Trend Micro

McAfee

CrowdStrike

Zscaler

Sophos

Broadcom

The Cloud Security Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, machine learning, and cloud-native architectures. AI-powered threat detection systems are now capable of analyzing over 1 million events per second, improving anomaly detection accuracy by up to 95%. These systems significantly reduce false positives by nearly 45%, enhancing operational efficiency for security teams.

Zero Trust Architecture is becoming a foundational technology, with over 68% of enterprises adopting identity-based access controls to eliminate implicit trust within networks. Additionally, Secure Access Service Edge (SASE) frameworks are gaining traction, integrating networking and security functions into a unified platform, improving network visibility by approximately 30%.

Cloud-Native Application Protection Platforms (CNAPP) are emerging as a comprehensive solution, combining workload protection, compliance monitoring, and vulnerability management. Over 52% of organizations are adopting CNAPP solutions to secure containerized and serverless environments. Encryption technologies are also evolving, with quantum-resistant encryption gaining attention as a future-proof security measure.

Automation and orchestration tools are enabling security operations centers (SOCs) to respond to threats in real time, reducing response times by up to 70%. These technologies are reshaping the cloud security landscape, enabling scalable, efficient, and resilient security frameworks for enterprises worldwide.

• In April 2026, Microsoft announced the general availability of container security capabilities within its Defender for Cloud platform for Azure Government, enabling U.S. federal agencies to secure Kubernetes workloads with advanced threat protection, vulnerability assessment, and compliance monitoring across hybrid environments. Source: www.microsoft.com

• In November 2025, Microsoft introduced a native integration between Defender for Cloud and GitHub Advanced Security, enabling developers to access runtime threat intelligence directly within development workflows, improving vulnerability remediation efficiency and enabling continuous protection from code to deployment environments.

• In December 2025, Palo Alto Networks and Google Cloud expanded their strategic partnership to deliver end-to-end AI-powered cloud security solutions, integrating Prisma AIRS with Google Cloud infrastructure to secure AI workloads, developer tools, and hybrid multicloud environments across more than 75 joint integrations.

• In October 2025, Palo Alto Networks launched Prisma AIRS 2.0 and Cortex Cloud 2.0, integrating AI-driven security automation trained on over 1.2 billion real-world security incidents, enabling enterprises to detect vulnerabilities faster and manage risks across multi-cloud environments through a unified cloud command center.

The Cloud Security Market Report provides a comprehensive analysis of key industry segments, technologies, and regional dynamics shaping the global market landscape. The report covers multiple solution types including identity and access management, data security, network security, application security, and emerging cloud-native protection platforms. These segments collectively address over 90% of enterprise cloud security requirements, reflecting the broad scope of solutions analyzed.

The report evaluates applications across major industries such as BFSI, healthcare, IT & telecom, retail, and government, which together account for more than 80% of cloud security deployments globally. It also highlights adoption trends among large enterprises and SMEs, with enterprise-level deployments representing the majority due to complex infrastructure requirements.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional variations in adoption, regulatory frameworks, and technological advancements. Over 70% of global enterprises are included in the study scope, ensuring robust market representation.

Additionally, the report explores emerging technologies such as AI-driven security, zero-trust architecture, SASE, and quantum-resistant encryption, which are expected to shape future market developments. It also includes insights into investment patterns, innovation trends, and competitive strategies adopted by key market players, providing a holistic view for decision-makers and industry professionals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,000.0 Million |

| Market Revenue (2033) | USD 10,861.7 Million |

| CAGR (2026–2033) | 13.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft Corporation; Amazon Web Services, Inc.; Google LLC; IBM Corporation; Cisco Systems, Inc.; Palo Alto Networks, Inc.; Check Point Software Technologies Ltd.; Fortinet, Inc.; Trend Micro Incorporated; McAfee Corp.; CrowdStrike Holdings, Inc.; Zscaler, Inc.; Sophos Ltd.; Broadcom Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |

p