Reports

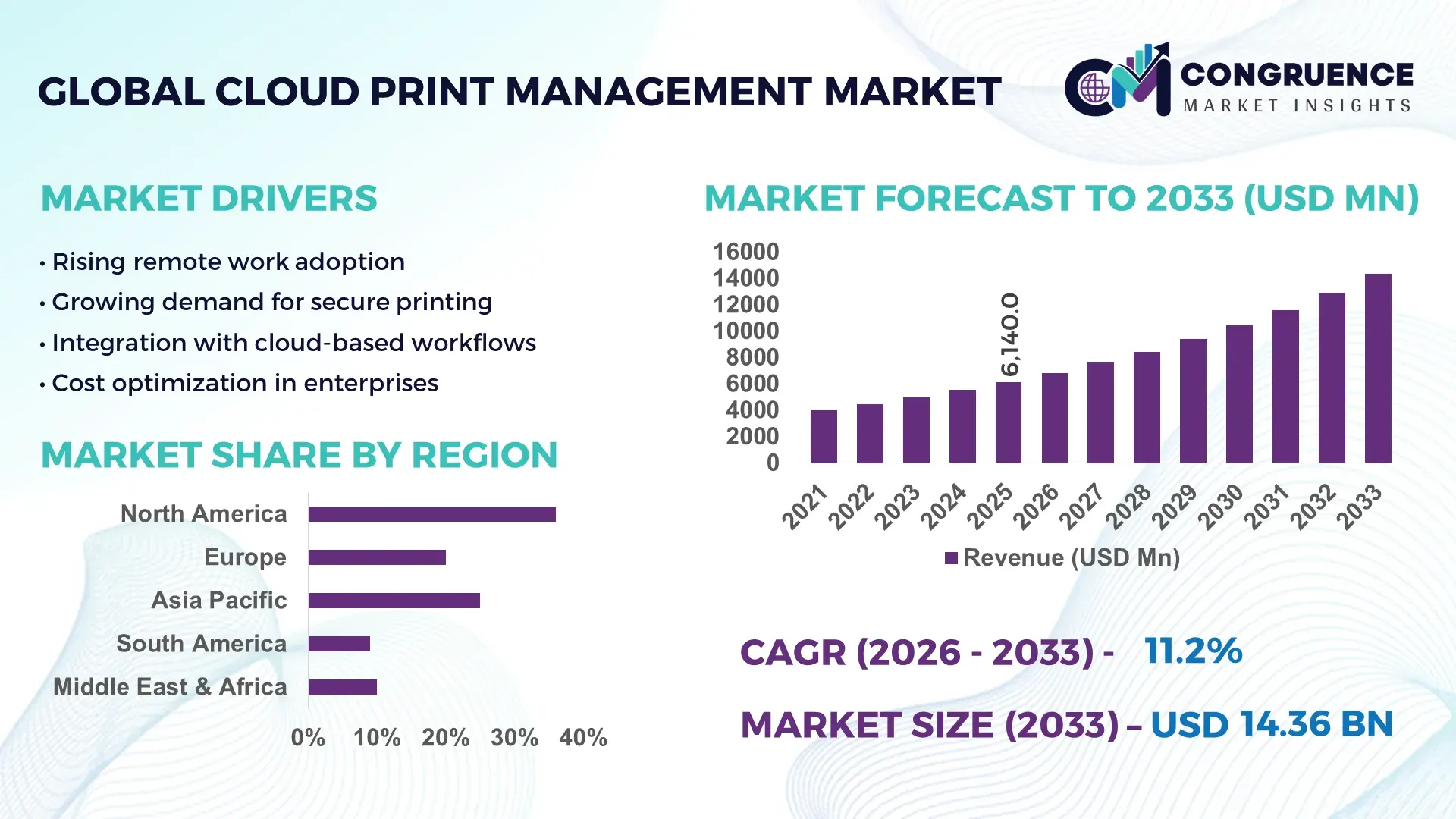

The Global Cloud Print Management Market was valued at USD 6140 Million in 2025 and is anticipated to reach a value of USD 14355.11 Million by 2033 expanding at a CAGR of 11.2% between 2026 and 2033. Growth is primarily driven by enterprise digital transformation and rising demand for secure, remote document infrastructure.

The United States represents the most technologically advanced national environment for cloud-based print infrastructure, supported by large-scale enterprise IT spending exceeding USD 1.4 trillion annually and strong SaaS adoption across more than 70% of medium and large organizations. Over 60% of enterprises have transitioned to hybrid or remote work models, increasing demand for centralized, cloud-controlled device fleets. Healthcare networks operate multi-site printing ecosystems integrating EHR-linked secure print release, while universities deploy cloud print portals serving campuses with 20,000+ users. Investments in zero-trust security, AI-driven usage analytics, and edge-connected IoT printers have accelerated modernization of over 45 million networked office devices nationwide, reinforcing advanced deployment maturity.

Market Size & Growth: USD 6140 Million in 2025, projected to reach USD 14355.11 Million by 2033, growing at 11.2% CAGR, fueled by hybrid work expansion and secure document digitization.

Top Growth Drivers: Cloud adoption 68%, document workflow efficiency improvement 45%, security risk reduction initiatives 52%.

Short-Term Forecast: By 2028, organizations are expected to achieve up to 30% print cost reduction and 25% improvement in device utilization efficiency.

Emerging Technologies: AI-based print analytics, zero-trust print security architecture, and IoT-enabled smart printer integration.

Regional Leaders: North America USD 5.2 Billion by 2033 driven by hybrid workforce adoption; Europe USD 4.1 Billion supported by compliance mandates; Asia-Pacific USD 3.6 Billion due to rapid SME cloud migration.

Consumer/End-User Trends: Enterprises prioritize centralized control, healthcare emphasizes compliance printing, and education adopts mobile campus printing platforms.

Pilot or Case Example: A 2024 enterprise deployment across distributed offices achieved 28% lower print volumes and 35% faster job authentication.

Competitive Landscape: Market leader holds approximately 18% share, followed by HP, Canon, Xerox, Ricoh, and Konica Minolta.

Regulatory & ESG Impact: Data protection laws and sustainability targets are accelerating adoption of secure release printing and paper reduction policies.

Investment & Funding Patterns: Over USD 900 Million invested recently in cloud document infrastructure, with growth in SaaS-based managed service financing.

Innovation & Future Outlook: Integration with digital workflow platforms, AI automation, and secure edge printing will define next-generation enterprise deployments.

Enterprise demand spans healthcare, education, BFSI, and government sectors, which collectively contribute over 65% of solution deployments due to strict data security and document traceability requirements. Innovations such as biometric release authentication, AI-powered print behavior analytics, and serverless print architecture are reshaping deployment models. Regulatory compliance frameworks, sustainability mandates targeting 20–30% paper reduction, and economic focus on IT cost optimization are driving modernization. North America and Europe show mature replacement cycles, while Asia-Pacific leads in new installations linked to SME digitization. Future growth is expected from integration with digital workflow ecosystems, intelligent automation, and secure edge-cloud printing convergence.

Cloud Print Management has evolved into a strategic IT control layer rather than a peripheral office function, aligning directly with enterprise cybersecurity, cost governance, and digital workplace transformation agendas. Organizations managing distributed workforces now oversee printer fleets exceeding 1 device per 8–10 employees, creating security exposure across millions of network endpoints. Cloud-native management frameworks enable centralized policy enforcement, real-time device telemetry, and encrypted job release, forming part of zero-trust architectures. AI-driven print analytics delivers 32% improvement in usage visibility compared to legacy on-premise print servers, enabling data-led policy optimization and waste reduction.

North America dominates in deployment volume due to extensive enterprise IT estates, while Western Europe leads in structured adoption, with over 58% of enterprises integrating cloud-controlled print environments within broader compliance frameworks. By 2028, AI-based device behavior analytics is expected to reduce unclaimed print jobs and consumable waste by 27%, directly improving operational efficiency KPIs. Sustainability mandates are reshaping procurement models, with firms committing to 30% paper consumption reduction by 2030 through rule-based printing, digital workflows, and automated duplex enforcement.

In 2024, a multinational financial institution in Germany achieved 35% reduction in print-related energy consumption through serverless print architecture and automated power management analytics. Looking forward, the Cloud Print Management Market is positioned as a core pillar of enterprise resilience, regulatory compliance readiness, and sustainable digital infrastructure modernization.

The global shift toward hybrid and remote work has fundamentally changed enterprise print infrastructure design. Over 60% of large organizations operate multi-location or home-based work structures, requiring secure access to document output beyond traditional office networks. Cloud Print Management enables policy enforcement, user authentication, and job routing across geographically dispersed environments without local server dependency. Enterprises managing more than 1,000 devices report up to 25% reduction in unauthorized print activity when secure release and identity-based controls are implemented. Educational institutions and healthcare systems with multi-site operations rely on cloud dashboards to monitor device utilization, toner levels, and service requirements in real time. This distributed visibility reduces manual oversight, improves compliance auditing, and supports consistent user experience regardless of location, making hybrid work enablement a primary structural growth catalyst.

Many enterprises continue operating aging printer fleets, with device lifecycles often extending beyond 6–8 years, limiting compatibility with modern cloud protocols. Integration with legacy ERP, document management, and authentication systems can require significant configuration and testing. Organizations with strict data sovereignty policies may hesitate to shift print data routing to cloud environments, even when encrypted, due to regulatory interpretation differences. Additionally, on-premise print servers still support mission-critical workflows in manufacturing and public administration settings, where downtime risks discourage rapid migration. IT teams face skill gaps in managing API integrations and cross-platform security policies, increasing implementation timelines. These technical and organizational complexities slow transition speed, especially among mid-sized enterprises lacking dedicated print governance expertise.

AI-based monitoring tools analyze device behavior, user patterns, and document flows to enable predictive maintenance and automated supply management. Enterprises deploying analytics-enabled solutions report up to 20% improvement in fleet utilization and significant reductions in emergency service calls due to proactive alerts. Automation of print policies—such as rule-based color restrictions, default duplex printing, and job routing to energy-efficient devices—supports sustainability objectives while lowering consumable usage. Integration with digital workflow platforms allows print to function as a controlled endpoint within automated document lifecycles, especially in legal, healthcare, and financial sectors where document traceability is critical. As organizations prioritize data-driven IT operations, AI-enhanced print governance presents a major efficiency and compliance optimization avenue.

Print devices are increasingly recognized as attack surfaces because they store cached documents, user credentials, and network configuration data. Regulatory frameworks such as data protection laws require secure handling of personally identifiable information, making print security a compliance-critical domain. Organizations must implement encryption, user authentication, audit logging, and firmware updates across large device fleets, often numbering in the thousands. Managing these controls consistently across multiple vendors and locations presents operational complexity. Security audits frequently reveal outdated firmware or misconfigured ports, exposing vulnerabilities. Additionally, incident response planning must now include print infrastructure, increasing governance overhead and requiring cross-functional coordination between IT security, compliance teams, and facilities management.

• Rapid Shift Toward Serverless Print Architectures Reducing Infrastructure Footprint: Enterprises are decommissioning traditional print servers at scale, with over 48% of large organizations migrating to fully serverless environments to minimize hardware dependency. This transition cuts on-premise print infrastructure by nearly 35%, lowers IT maintenance workloads by 28%, and accelerates multi-site deployment timelines by 40% compared to legacy server-based setups.

• Expansion of Zero-Trust Print Security Frameworks Across Enterprise Networks: Print devices are now included in broader cybersecurity programs, with 62% of enterprises implementing identity-based print authentication and encrypted job transmission. Secure release adoption has reduced unauthorized document access incidents by 31%, while automated firmware monitoring improves vulnerability response times by 45%, strengthening compliance with corporate data protection mandates.

• AI-Driven Usage Analytics Optimizing Fleet Performance and Sustainability Metrics: Advanced analytics platforms process device telemetry from fleets exceeding 1,000+ units, enabling organizations to lower consumable waste by 22% and reduce unnecessary color printing by 30% through policy automation. Predictive maintenance alerts have also decreased service interruptions by 26%, improving uptime consistency across distributed office networks.

• Integration with Digital Workflow Ecosystems Increasing Process Automation Levels: Over 54% of enterprises now connect print environments with cloud document management and collaboration platforms, enabling automated routing of scanned and printed outputs. Workflow-linked printing reduces manual document handling steps by 33% and shortens approval cycle times by 25%, particularly in regulated sectors such as finance, healthcare, and public administration.

The Cloud Print Management market demonstrates structured segmentation across solution types, enterprise applications, and industry end-user groups, reflecting how organizations modernize document output environments. Solution adoption is influenced by infrastructure scale, security posture, and workforce distribution. Enterprises with more than 500 employees typically manage fleets exceeding 120 networked devices, increasing reliance on centralized cloud platforms. Application segmentation reveals that security-led use cases now shape over 40% of deployment decisions, while workflow automation and cost control functions remain strong adoption pillars. End-user segmentation highlights higher penetration in regulated sectors where document traceability and audit compliance are critical operational requirements. Education and healthcare collectively manage millions of monthly print transactions across distributed campuses and facilities, reinforcing demand for cloud-based governance. Meanwhile, small and medium enterprises are increasingly entering the market as SaaS subscription models lower upfront deployment complexity. These segmentation dynamics indicate a shift from hardware-centric oversight toward analytics-driven, policy-controlled print ecosystems integrated with broader digital workplace infrastructure.

Cloud Print Management solutions are categorized into managed print services, print monitoring and analytics tools, security-focused print control platforms, mobile and remote printing solutions, and workflow/output management systems. Managed print services lead with approximately 34% adoption share, as large enterprises prefer bundled device oversight, predictive maintenance, and consumable optimization delivered via centralized cloud dashboards. Security-centric print control platforms represent the fastest-growing type, expanding at nearly 13% annually, driven by rising implementation of identity-based authentication, encrypted job routing, and zero-trust network frameworks.

Monitoring and analytics tools contribute roughly 18% of deployments, enabling fleet performance insights and usage-based optimization. Mobile and remote printing solutions hold near 16%, reflecting hybrid workforce trends where employees require secure output access outside traditional offices. Workflow and output management tools account for a combined 32%, serving sectors with document-intensive processes such as legal, healthcare, and finance.

Application segmentation shows document security and compliance management leading with about 38% usage share, as enterprises prioritize protection of confidential records and adherence to data handling regulations. Cost optimization and usage tracking represent the fastest-growing application area, advancing at approximately 12% annually, supported by analytics tools that reduce consumable waste and device overuse.

Device fleet management and monitoring account for nearly 22% of deployments, enabling IT teams to oversee thousands of endpoints from unified dashboards. Workflow automation contributes about 20%, particularly in sectors with structured approval cycles and document routing needs. Sustainability-focused print control initiatives make up roughly 20%, where automated duplex policies and color restrictions reduce paper consumption by up to 25% in enterprise settings.

Large enterprises form the leading end-user group with around 41% adoption, due to complex IT environments managing thousands of devices across multiple locations. Healthcare organizations represent the fastest-growing segment, expanding at nearly 14% annually, as hospitals integrate print governance with electronic health record systems to secure patient data and track document flows.

Educational institutions account for approximately 19% of deployments, supporting campus-wide mobile printing for student populations exceeding 10,000 users per institution. Government and public sector bodies represent about 17%, driven by document security mandates and centralized procurement models. Financial and legal service providers collectively hold near 23%, where confidential document handling and audit requirements are critical.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.1% between 2026 and 2033.

North America maintains a dense enterprise IT ecosystem with over 45 million networked office printers integrated into cloud-managed environments. Europe follows with nearly 28% share, driven by compliance-centric deployments across regulated industries. Asia-Pacific holds about 24% of installations, supported by SME digitalization and rapid office infrastructure expansion in urban technology corridors. South America represents close to 7%, while the Middle East & Africa collectively contribute approximately 5%, reflecting developing yet accelerating adoption. Enterprise fleets in mature markets average 1 printer per 9 employees, compared to 1 per 14 in emerging economies, indicating modernization headroom. Regional consumption patterns show that over 52% of deployments globally are linked to hybrid workforce enablement, while 31% align with security-led digital governance programs.

How are advanced enterprise IT ecosystems accelerating cloud-based document infrastructure modernization?

This region represents approximately 36% of global deployments, supported by strong enterprise digitization. Healthcare, financial services, education, and federal institutions drive demand, managing high-volume, compliance-sensitive documentation. Over 65% of large organizations operate centralized cloud dashboards for device fleets exceeding 500 units. Regulatory frameworks such as data privacy mandates and secure record retention policies encourage encrypted job release and identity-based authentication. Technological adoption includes AI-powered print analytics, zero-trust endpoint integration, and IoT-enabled fleet monitoring. One leading player, HP, has expanded subscription-based print security services integrating real-time threat detection across networked devices. User behavior shows preference for mobile-enabled, secure print release, particularly in healthcare and finance sectors where confidentiality standards are strict.

How are compliance mandates and sustainability initiatives reshaping enterprise print governance models?

Europe holds nearly 28% of market adoption, with Germany, the UK, and France leading deployments. Enterprises prioritize compliance with data protection and environmental governance rules, driving policy-based printing and audit trail integration. Over 58% of enterprises in regulated industries apply automated duplex policies to reduce paper consumption. Sustainability initiatives support device lifecycle optimization and recycling of consumables. Adoption of emerging technologies such as AI-driven usage analytics and secure cloud authentication is increasing across government and legal institutions. A regional technology provider, Canon Europe, has expanded cloud-connected monitoring tools supporting centralized fleet oversight across cross-border operations. Buyers demonstrate high sensitivity to regulatory accountability, favoring traceable, policy-controlled print environments.

What role does rapid SME digitization play in accelerating cloud-managed output environments?

Asia-Pacific ranks third in current volume but leads in expansion momentum, accounting for about 24% of installations. China, India, and Japan are the top consuming countries due to large enterprise populations and growing service sectors. Urban technology parks and smart office developments are integrating cloud-controlled device fleets from the outset. Regional innovation hubs emphasize mobile-first workflows, with over 55% of office workers accessing documents through mobile devices. Ricoh Asia Pacific has advanced cloud-based device analytics platforms to support distributed enterprise campuses. Consumer behavior reflects strong adoption of mobile and BYOD printing models, driven by fast-growing digital service industries and e-commerce operations.

How is enterprise modernization influencing demand for centralized document security systems?

This region contributes around 7% of global demand, with Brazil and Argentina as primary markets. Infrastructure modernization in financial services, education, and media sectors is encouraging cloud-managed print deployment. Over 40% of large organizations in urban business districts have migrated at least part of their device fleets to cloud oversight platforms. Government digitization programs and trade modernization initiatives are improving IT infrastructure reliability. Xerox Latin America has expanded managed services focusing on analytics-driven supply optimization. End-users show preference for cost-monitoring tools and mobile authentication systems, particularly among media companies handling multilingual document production.

How are digital transformation initiatives modernizing document infrastructure across high-growth economies?

The region represents roughly 5% of total installations but shows strong modernization efforts in the UAE and South Africa. Oil & gas, construction, and public sector digitization projects are integrating cloud-managed print control into broader smart infrastructure programs. Over 35% of enterprise deployments involve centralized authentication platforms supporting secure access across multiple facilities. Technology modernization trends include IoT-connected device fleets and remote monitoring systems for distributed operations. A regional integrator has deployed cloud print dashboards across government offices to standardize usage reporting. Consumer behavior emphasizes secure, multilingual document output and mobile authentication, especially in government and energy sectors.

United States – 31% share in the Cloud Print Management market, supported by large enterprise IT ecosystems and widespread hybrid workforce infrastructure.

Germany – 11% share in the Cloud Print Management market, driven by compliance-focused industries and strong adoption of secure, policy-controlled document systems.

The Cloud Print Management market exhibits a moderately fragmented structure with more than 40 active global and regional solution providers competing across managed services, security software, analytics platforms, and workflow integration tools. The top five vendors collectively account for approximately 52% of total deployments, indicating a competitive yet innovation-driven environment. Large multinational imaging and document technology firms leverage installed hardware bases exceeding 10 million devices globally to upsell cloud management subscriptions.

Competition increasingly centers on software differentiation rather than hardware dependency. Over 60% of new strategic initiatives focus on SaaS platform expansion, API integration with collaboration suites, and zero-trust security frameworks. Partnerships between print OEMs and cybersecurity firms have increased by 35% in the past two years to address endpoint vulnerabilities. Product innovation cycles have shortened to 12–18 months, with vendors releasing AI-powered analytics modules capable of reducing device downtime by up to 26%. Mergers and managed service acquisitions are also rising, particularly in North America and Europe, where providers seek to expand regional service coverage and enterprise account penetration. Competitive positioning now emphasizes subscription scalability, centralized analytics, and ESG-aligned print optimization capabilities.

HP Inc.

Canon Inc.

Xerox Holdings Corporation

Ricoh Company, Ltd.

Konica Minolta, Inc.

Lexmark International

Epson

Kyocera Document Solutions

PaperCut Software

Y Soft Corporation

PrinterLogic

UniPrint

Cloud-native architecture is redefining print infrastructure, with over 48% of large enterprises transitioning from on-premise print servers to multi-tenant SaaS platforms. Serverless print models reduce infrastructure footprint by up to 35% and cut deployment times by nearly 40% across distributed office environments. These platforms leverage encrypted job routing, centralized policy enforcement, and identity federation through SSO and multi-factor authentication, aligning print governance with zero-trust network strategies. Integration with cloud identity providers enables real-time user validation across fleets exceeding 1,000 devices, significantly strengthening endpoint security control.

Artificial intelligence and machine learning are increasingly embedded into analytics modules. AI-driven telemetry engines analyze device usage patterns, enabling up to 22% reduction in consumable waste and 26% fewer service interruptions through predictive maintenance alerts. Behavioral analytics also detect anomalous printing activity, supporting early identification of potential data exfiltration risks. Automation technologies enforce rule-based printing—such as duplex defaults and color restrictions—helping enterprises achieve paper reduction targets of 20–30%.

Edge and IoT connectivity advancements are enhancing device intelligence. Modern printers now function as network endpoints equipped with firmware monitoring and automated patch deployment, reducing vulnerability exposure windows by 45%. Mobile and BYOD printing technologies support secure access via encrypted QR or NFC-based authentication, addressing workforce mobility trends where over 55% of employees use mobile devices for document workflows. Integration with digital workflow and document management platforms allows automated routing of scanned outputs, reducing manual handling steps by 30% and improving process efficiency in regulated industries.

• In January 2025, Ricoh was positioned as a leader in the 2024 cloud managed print and document services landscape, recognized globally for portfolio breadth, implementation capabilities, and digital transformation support that enhances enterprise print infrastructure delivery and professional services coverage. (ricoh.com)

• In May 2025, Xerox was named a leader in the 2025 cloud print services landscape for its comprehensive cloud-centric portfolio, AI-enabled document capture innovations, and strategic acquisitions that expanded its managed print service capabilities for organizations of all sizes. (Xerox Newsroom)

• In June 2024, Canon launched its Canon Cloud Print Manager platform, enabling secure cloud printing across enterprise devices and locations, streamlining multi-site operations and enhancing remote document workflows for enterprise users globally.

• In January–March 2025, Xerox expanded its cloud print management offerings by integrating cloud-native managed print services into its Workplace Cloud platform, automating driver deployment, supplies logistics, and fleet maintenance to reduce on-premise infrastructure reliance.

The Cloud Print Management Market Report encompasses a comprehensive analysis of solution types, deployment models, regional distributions, technology influences, and industry-specific applications. It evaluates both software and services segments, detailing adoption across on-premise, public cloud, and hybrid cloud deployments, with segmentation by organization size from small and medium enterprises to large enterprises managing extensive device fleets. The report includes type-level insights covering managed print services, security-centric print control layers, mobile and remote printing platforms, and analytics-driven optimization tools.

Geographic scope spans major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level analysis highlighting consumption patterns, infrastructure maturity, and regulatory influences. Industry application categories incorporate document security and compliance, device monitoring and management, workflow automation, and sustainability-centered deployments. Technology trends examined include AI-based analytics, identity-led secure release systems, serverless print frameworks, and IoT-edge integrations supporting mobile and BYOD printing environments.

The report also addresses end-user verticals such as healthcare, education, financial services, government, retail, and legal services, profiling each segment’s specific adoption drivers, usage characteristics, and integration with broader digital workplace strategies. Further, it identifies niche growth opportunities arising from hybrid work enablement, ESG-aligned print governance models, and cross-platform collaboration tool integrations. Insights on competitive dynamics, recent product launches, and innovation trajectories complete the market’s strategic overview, tailored for decision-makers seeking actionable intelligence on evolving cloud-managed print ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

HP Inc., Canon Inc., Xerox Holdings Corporation, Ricoh Company, Ltd., Konica Minolta, Inc., Lexmark International, Epson, Kyocera Document Solutions, PaperCut Software, Y Soft Corporation, PrinterLogic, UniPrint |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |