Reports

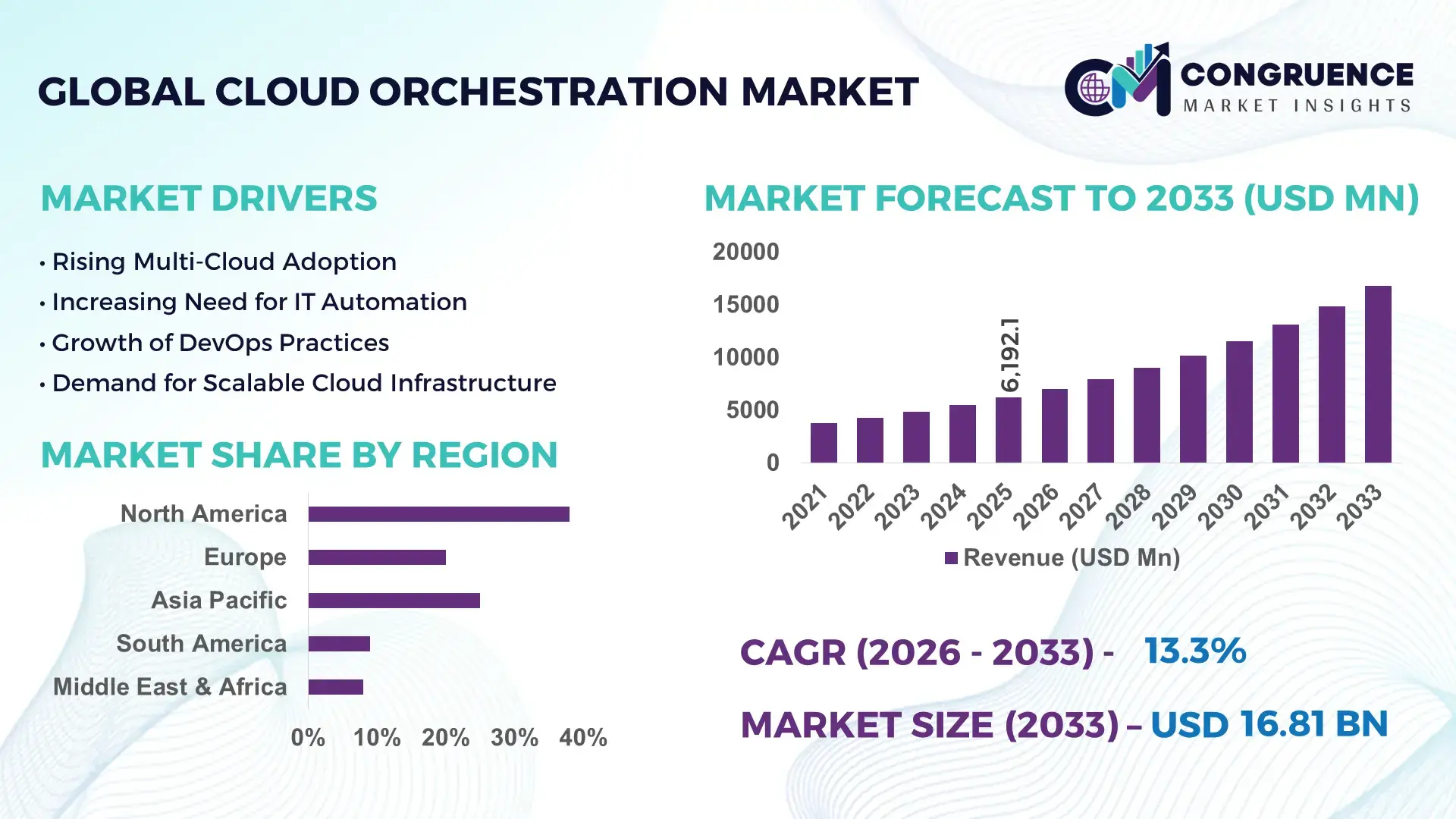

The Global Cloud Orchestration Market was valued at USD 6192.13 Million in 2025 and is anticipated to reach a value of USD 16814.32 Million by 2033 expanding at a CAGR of 13.3% between 2026 and 2033. The expansion is primarily driven by the rapid enterprise shift toward automated multi-cloud infrastructure management and the growing complexity of large-scale digital workloads.

The United States remains the most influential country in the cloud orchestration landscape due to its large-scale hyperscale infrastructure, enterprise cloud adoption, and continuous investment in automation technologies. The country hosts over 5,300 data centers, accounting for nearly 40% of global hyperscale capacity. Enterprise cloud adoption in the U.S. exceeds 94%, with more than 70% of large organizations deploying hybrid or multi-cloud environments that rely on orchestration platforms to automate provisioning and workload scaling. Investments in cloud-native technologies and Kubernetes-based orchestration systems surpassed USD 20 billion in enterprise IT budgets in 2024. Major industry applications include financial services automation, healthcare data orchestration, telecom network management, and large-scale retail e-commerce platforms handling millions of transactions per hour.

• Market Size & Growth: The cloud orchestration market reached USD 6192.13 million in 2025 and is projected to reach USD 16814.32 million by 2033, expanding at a 13.3% CAGR due to accelerating enterprise adoption of automated cloud infrastructure management and scalable digital workloads.

• Top Growth Drivers: Multi-cloud adoption (68%), IT automation demand (54%), and DevOps integration expansion (47%).

• Short-Term Forecast: By 2028, automated cloud orchestration platforms are expected to reduce infrastructure deployment time by 45% and improve workload performance efficiency by 32%.

• Emerging Technologies: AI-driven infrastructure automation, Kubernetes-based container orchestration, and policy-driven multi-cloud governance frameworks.

• Regional Leaders: North America projected to exceed USD 7200 million by 2033 with strong enterprise cloud automation adoption; Europe expected to reach USD 4300 million driven by regulatory-compliant cloud frameworks; Asia-Pacific projected near USD 3800 million due to expanding hyperscale data center infrastructure.

• Consumer/End-User Trends: Banking, telecommunications, healthcare, and e-commerce sectors increasingly deploy orchestration platforms to automate container workloads, manage hybrid infrastructure, and reduce operational complexity.

• Pilot or Case Example: In 2024, a large telecom operator implemented AI-based cloud orchestration across 120+ network functions, reducing service deployment time by 38% and improving network uptime by 21%.

• Competitive Landscape: The market leader holds approximately 19% share, followed by major competitors offering enterprise-grade cloud automation, container orchestration, and hybrid cloud management platforms.

• Regulatory & ESG Impact: Data sovereignty regulations and sustainable IT initiatives are pushing organizations to optimize energy-efficient cloud operations, targeting up to 30% reduction in data center energy usage by 2030.

• Investment & Funding Patterns: Global investment in cloud automation and orchestration technologies surpassed USD 9 billion in recent enterprise IT modernization initiatives, including venture-backed DevOps automation platforms.

• Innovation & Future Outlook: Cloud orchestration platforms are increasingly integrating AI-driven workload optimization, zero-touch provisioning, and automated policy enforcement to support next-generation digital infrastructure.

Cloud orchestration solutions are widely deployed across multiple industry sectors including BFSI, telecommunications, retail, healthcare, and government IT infrastructure. The BFSI sector contributes nearly 28% of enterprise orchestration deployments due to high-volume digital transaction management and compliance-driven automation needs. Telecommunications accounts for roughly 21% of adoption as network virtualization and 5G infrastructure require automated service orchestration. Recent technological innovations include AI-powered workload placement, autonomous cloud management tools, and integrated security orchestration frameworks. Regulatory frameworks focused on data localization and cyber resilience are also shaping enterprise investment decisions. Growing regional cloud consumption in Asia-Pacific and the Middle East is further accelerating demand for scalable orchestration platforms capable of managing complex hybrid cloud ecosystems.

The strategic importance of the cloud orchestration market is expanding as organizations increasingly depend on automated infrastructure management to support complex digital ecosystems. Enterprises deploying advanced Kubernetes orchestration frameworks report up to 40% faster application deployment compared to traditional manual cloud provisioning methods. In comparison, modern AI-driven orchestration engines deliver nearly 35% operational efficiency improvement compared to legacy infrastructure management tools.

North America dominates in infrastructure deployment volume due to its extensive hyperscale cloud ecosystem, while Asia-Pacific leads in enterprise adoption growth with nearly 61% of large organizations implementing hybrid cloud automation strategies. By 2028, AI-enabled predictive cloud orchestration is expected to reduce infrastructure downtime by approximately 28% while improving workload optimization accuracy by more than 30%.

Sustainability considerations are also shaping enterprise strategies, with organizations committing to reduce data center energy consumption by nearly 25% by 2030 through intelligent workload orchestration and automated resource allocation. In 2024, a large European financial services firm implemented AI-powered cloud orchestration across its hybrid infrastructure, achieving a 33% improvement in resource utilization and a 22% reduction in operational overhead. These developments position the cloud orchestration market as a critical pillar supporting resilient digital infrastructure, regulatory compliance, and long-term sustainable enterprise technology growth.

The expansion of multi-cloud and hybrid cloud deployments is significantly increasing demand for advanced cloud orchestration platforms. More than 76% of large enterprises now operate workloads across multiple cloud providers, creating a need for automated management systems capable of coordinating resources, applications, and networking services. Cloud orchestration platforms enable organizations to automate deployment pipelines, manage containerized applications, and optimize infrastructure usage across distributed environments. In sectors such as telecommunications and financial services, orchestration tools help manage thousands of microservices and container instances simultaneously. Enterprises adopting orchestration-based automation have reported up to 40% improvement in deployment efficiency and nearly 30% reduction in manual IT operations, making orchestration a fundamental technology in modern cloud infrastructure management.

Despite its benefits, cloud orchestration adoption faces challenges related to security, compliance, and integration complexity. Many enterprises operate legacy IT environments that require extensive customization to integrate with modern orchestration frameworks. Security risks also increase when workloads are distributed across multiple cloud platforms, making policy enforcement and access management more complex. Nearly 48% of enterprise IT leaders report concerns regarding configuration errors and automation mismanagement that could expose sensitive data or disrupt critical services. Additionally, compliance regulations related to data sovereignty and cross-border data transfers require strict governance controls, increasing implementation complexity. These factors can slow adoption among organizations with highly regulated infrastructure environments.

Artificial intelligence and machine learning technologies are opening significant opportunities for the cloud orchestration market by enabling predictive infrastructure management and autonomous workload optimization. AI-powered orchestration platforms can analyze real-time system data to automatically allocate resources, detect anomalies, and optimize application performance across hybrid cloud environments. Enterprises deploying AI-enabled orchestration solutions report up to 35% improvement in infrastructure efficiency and nearly 25% reduction in operational costs. With global enterprise data volumes expected to surpass 180 zettabytes by the end of the decade, intelligent orchestration systems will become essential for managing large-scale digital workloads, making AI-driven automation a major growth catalyst for next-generation cloud infrastructure platforms.

Implementing large-scale cloud orchestration systems requires specialized expertise in container management, automation frameworks, and distributed infrastructure operations. However, a global shortage of skilled cloud engineers and DevOps specialists remains a significant challenge. Industry studies indicate that more than 60% of enterprises struggle to recruit professionals with advanced Kubernetes and cloud automation skills. Additionally, orchestration platforms often involve complex configuration processes, requiring organizations to redesign existing IT workflows and governance models. Managing orchestration across multiple cloud providers can also create operational complexity related to compatibility, performance monitoring, and service integration. These challenges can slow deployment timelines and increase operational costs for organizations transitioning toward fully automated cloud infrastructure environments.

• Rapid Expansion of Kubernetes-Based Automation Platforms: Kubernetes-driven orchestration frameworks are becoming the backbone of enterprise cloud infrastructure. More than 72% of organizations deploying containerized applications now rely on Kubernetes orchestration tools to automate workload management and scaling. Enterprise IT environments managing over 500 microservices increasingly use orchestration layers to automate container deployment, health monitoring, and traffic routing. In large-scale cloud infrastructures, Kubernetes-based orchestration has improved deployment efficiency by nearly 40% while reducing manual configuration tasks by approximately 35%. Financial services and telecommunications companies managing distributed applications across multiple data centers are among the fastest adopters, using orchestration systems to manage thousands of container workloads simultaneously across hybrid and multi-cloud environments.

• Integration of Artificial Intelligence for Autonomous Cloud Operations: AI-driven cloud orchestration is emerging as a transformative trend, enabling predictive resource allocation and automated workload optimization. Approximately 61% of enterprise cloud operations teams are integrating AI-enabled orchestration tools to manage infrastructure complexity and detect performance anomalies. Advanced machine learning algorithms can analyze millions of infrastructure metrics every hour to predict system failures and optimize resource allocation. Organizations deploying AI-enabled orchestration platforms report up to 32% improvement in workload efficiency and nearly 27% reduction in operational downtime. Autonomous orchestration capabilities are particularly valuable for large enterprises operating global cloud networks with more than 1,000 virtual machines and container clusters that require continuous optimization and automated policy enforcement.

• Growth of Multi-Cloud Governance and Policy Automation: The expansion of multi-cloud infrastructure strategies is driving demand for advanced governance capabilities within cloud orchestration platforms. Nearly 78% of global enterprises now operate workloads across two or more cloud environments, requiring centralized orchestration tools to enforce security policies, automate compliance, and manage resource allocation. Cloud orchestration platforms capable of managing infrastructure across three or more providers have improved IT governance efficiency by approximately 34%. Large enterprises deploying multi-cloud orchestration frameworks report up to 29% faster compliance auditing and 31% improvement in infrastructure provisioning speed. Regulatory requirements in industries such as banking and healthcare are accelerating adoption of policy-driven orchestration tools designed to ensure data protection and operational transparency across distributed cloud environments.

• Increasing Adoption of Serverless and Event-Driven Orchestration Architectures: Serverless orchestration frameworks are gaining traction as organizations shift toward event-driven computing models. More than 49% of enterprises deploying cloud-native applications are integrating serverless orchestration technologies to automate application workflows and reduce infrastructure overhead. Event-driven orchestration allows systems to automatically trigger tasks based on real-time events, enabling faster response times and improved application scalability. Companies implementing serverless orchestration architectures report nearly 28% improvement in application responsiveness and up to 22% reduction in infrastructure resource consumption. The trend is particularly visible in digital commerce, real-time analytics, and streaming services, where millions of event-driven transactions must be processed every minute without manual infrastructure management.

The cloud orchestration market is segmented based on deployment type, application areas, and key end-user industries. In terms of type, hybrid cloud orchestration platforms are widely adopted due to their ability to integrate on-premise infrastructure with public cloud environments, accounting for over 46% of enterprise deployments. Public cloud orchestration solutions are expanding rapidly as organizations migrate workloads to scalable cloud platforms. Application segmentation highlights IT automation, application lifecycle management, and infrastructure provisioning as the primary use cases, with IT automation representing nearly 38% of total deployments. From an end-user perspective, banking, telecommunications, healthcare, retail, and government sectors dominate adoption, collectively representing more than 70% of enterprise demand as organizations seek automated infrastructure management to support large-scale digital operations.

The cloud orchestration market includes several deployment types such as public cloud orchestration, private cloud orchestration, and hybrid cloud orchestration platforms. Hybrid cloud orchestration currently leads the market with approximately 46% of adoption as enterprises increasingly integrate on-premise infrastructure with public cloud services to maintain flexibility, security control, and operational scalability. Hybrid environments allow organizations to orchestrate workloads across distributed infrastructures while maintaining data sovereignty and compliance, which is particularly important for financial institutions and government agencies. Public cloud orchestration accounts for nearly 34% of the market and represents the fastest-growing deployment type, expanding at an estimated CAGR of around 16%. Growth is driven by rising enterprise migration to hyperscale public cloud platforms that require automated orchestration to manage container workloads, microservices, and large-scale application deployments. Private cloud orchestration platforms maintain a specialized role, representing roughly 20% of adoption, particularly within sectors requiring strict data governance such as healthcare and defense.

Cloud orchestration technologies are widely used across several application areas including IT process automation, infrastructure provisioning, application lifecycle management, and workload scheduling. IT automation currently represents the largest application segment, accounting for approximately 38% of deployments. Enterprises increasingly rely on orchestration platforms to automate routine infrastructure tasks such as resource provisioning, monitoring, and configuration management, which can reduce manual IT workload by nearly 40%. Infrastructure provisioning follows closely with nearly 29% of total adoption as organizations deploy orchestration tools to automatically allocate compute resources, storage capacity, and network services across hybrid and multi-cloud environments. Application lifecycle management is the fastest-growing application segment, expanding at an estimated CAGR of about 17%, driven by DevOps practices and continuous integration pipelines that require automated deployment and testing environments.

Other applications such as workload scheduling, disaster recovery orchestration, and compliance automation collectively contribute nearly 33% of market deployments. These applications enable organizations to maintain operational continuity and optimize infrastructure efficiency.

The cloud orchestration market is strongly driven by demand from industries managing complex digital infrastructures. The banking, financial services, and insurance (BFSI) sector leads the market with approximately 28% adoption due to the need for automated infrastructure management capable of supporting high-volume digital transactions and regulatory compliance requirements. Large financial institutions process millions of transactions per day and rely on orchestration platforms to manage distributed applications, ensure security policies, and maintain operational continuity. The telecommunications sector represents around 23% of market demand and is the fastest-growing end-user segment, expanding at an estimated CAGR of about 18%. Telecom operators increasingly deploy orchestration tools to manage network virtualization, 5G infrastructure, and large-scale containerized applications supporting digital communication services.

Healthcare, retail, and government organizations collectively account for nearly 49% of remaining adoption. Healthcare providers use orchestration platforms to manage electronic health record systems and telemedicine applications, while retail companies rely on automated infrastructure to support high-traffic e-commerce platforms and real-time inventory analytics.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2026 and 2033.

North America hosts more than 3,000 enterprise cloud automation deployments across finance, telecom, and healthcare industries, with over 72% of large enterprises operating hybrid cloud environments that rely on orchestration platforms. Europe represents nearly 27% of global adoption, supported by strict data governance frameworks and increasing use of containerized enterprise applications across more than 1,500 enterprise cloud infrastructure projects. Asia-Pacific contributes approximately 24% of global deployments, driven by expanding hyperscale data center capacity exceeding 650 facilities across China, Japan, India, and Singapore. South America and Middle East & Africa collectively represent 11% of market activity, supported by rising investments in digital infrastructure, telecom network virtualization, and government-led cloud modernization programs.

How Is Enterprise Automation Accelerating Cloud Infrastructure Management Across Advanced Digital Economies?

North America holds approximately 38% share of the cloud orchestration market, supported by strong enterprise adoption across banking, healthcare, telecommunications, and e-commerce sectors. Over 74% of large enterprises in this region operate hybrid or multi-cloud infrastructures that require orchestration platforms to manage containerized workloads. Government-backed digital modernization programs and strict cybersecurity regulations have further accelerated enterprise adoption. Technological advancement is led by large-scale Kubernetes deployments and AI-driven infrastructure automation across more than 1,200 hyperscale data center facilities. A major local technology provider has recently expanded its orchestration platform to support automated deployment across more than 10,000 container clusters, enabling enterprises to reduce manual infrastructure management. Consumer behavior in this region reflects high enterprise cloud automation adoption, particularly within financial institutions and healthcare IT infrastructure.

How Are Data Governance Frameworks Transforming Enterprise Cloud Automation Strategies?

Europe accounts for nearly 27% of the global cloud orchestration market, with key demand concentrated in Germany, the United Kingdom, and France, which collectively represent more than 60% of regional enterprise deployments. Strict regulatory frameworks including data sovereignty and digital compliance policies have increased enterprise demand for automated orchestration tools capable of managing secure hybrid infrastructures. Over 65% of enterprises in Western Europe operate containerized applications requiring orchestration systems for automated resource allocation. Regional initiatives focused on sustainable data center operations have also encouraged cloud optimization technologies. A leading European cloud technology firm recently deployed orchestration tools supporting over 3,500 enterprise workloads across regulated industries. Regional enterprise behavior indicates strong demand for governance-driven orchestration platforms designed to ensure regulatory compliance and secure data management.

How Is Digital Infrastructure Expansion Reshaping Automated Cloud Management?

Asia-Pacific ranks as the third-largest regional market, representing nearly 24% of global cloud orchestration adoption with more than 650 large-scale data centers supporting enterprise digital infrastructure. Major consuming countries include China, India, and Japan, which collectively account for more than 70% of regional enterprise cloud deployments. Rapid growth of e-commerce platforms, mobile applications, and AI-powered digital services is accelerating the need for automated cloud infrastructure management. Innovation hubs in cities such as Bangalore, Tokyo, and Shenzhen are leading development of cloud-native applications requiring scalable orchestration frameworks. A regional cloud technology company recently introduced orchestration software capable of managing over 500 enterprise container clusters across hybrid infrastructure environments. Consumer behavior across this region reflects strong demand driven by digital commerce, mobile platforms, and large-scale application ecosystems.

What Factors Are Accelerating Digital Infrastructure Automation Across Emerging Cloud Ecosystems?

South America represents approximately 6% of the global cloud orchestration market, with Brazil and Argentina emerging as the primary adoption centers. Brazil alone accounts for nearly 55% of regional enterprise cloud deployments, driven by expanding digital banking and media streaming platforms. Infrastructure modernization programs across telecom and financial sectors are increasing demand for automated cloud management tools capable of orchestrating distributed workloads. Governments in several countries are supporting digital transformation through cloud adoption incentives and data localization initiatives. A regional telecommunications technology provider recently implemented orchestration frameworks managing more than 120 network services across hybrid infrastructure. Consumer behavior trends indicate strong adoption driven by digital media platforms, multilingual applications, and localized content delivery networks.

How Are Digital Transformation Initiatives Accelerating Enterprise Cloud Automation?

The Middle East & Africa region accounts for nearly 5% of global cloud orchestration deployments, with major adoption occurring in the United Arab Emirates, Saudi Arabia, and South Africa. Rapid digital transformation initiatives in oil & gas, government services, and financial technology sectors are expanding demand for automated infrastructure management tools. More than 180 large enterprise cloud infrastructure projects are currently underway across the region, many requiring orchestration systems to manage containerized applications. National digital economy strategies and smart city initiatives are accelerating investments in advanced cloud infrastructure. A regional technology provider recently deployed orchestration solutions supporting over 250 enterprise workloads across government cloud platforms. Consumer behavior in this region shows growing reliance on digital public services, fintech applications, and large-scale enterprise data management systems.

United States – 34% Cloud Orchestration market share: Strong enterprise cloud adoption, presence of over 5,000 data centers, and extensive deployment of hybrid cloud infrastructure across finance, healthcare, and telecommunications sectors.

China – 16% Cloud Orchestration market share: Rapid expansion of hyperscale cloud infrastructure and large-scale digital platforms supporting millions of cloud-based applications across e-commerce, fintech, and digital services industries.

The cloud orchestration market is characterized by moderate consolidation with strong competition among more than 70 active technology vendors offering enterprise automation, container orchestration, and hybrid cloud management platforms. The top five companies collectively account for nearly 52% of the global market presence, supported by extensive enterprise software ecosystems and large cloud infrastructure platforms. Leading companies are investing heavily in AI-driven orchestration capabilities, Kubernetes automation tools, and integrated DevOps frameworks to strengthen their market positioning.

Strategic partnerships between cloud platform providers and enterprise software firms have increased significantly, with more than 40 collaboration agreements announced between 2023 and 2025 focused on hybrid infrastructure management and cloud automation. Product innovation remains a central competitive factor, with vendors introducing orchestration solutions capable of managing over 10,000 container instances within a single enterprise environment. Several companies are also integrating advanced features such as automated compliance monitoring, predictive infrastructure scaling, and zero-touch deployment technologies.

Mergers and acquisitions have become a major strategy in the industry, particularly involving cloud automation startups specializing in AI-driven infrastructure management. In addition, the growing adoption of open-source orchestration platforms has intensified competition, encouraging vendors to differentiate through enterprise-grade security, automation capabilities, and advanced workload optimization features.

Microsoft

IBM

Cisco Systems

VMware

Red Hat

Hewlett Packard Enterprise

Amazon Web Services

Google Cloud

BMC Software

Oracle Corporation

ServiceNow

Flexera Software

Micro Focus

CloudBolt Software

Morpheus Data

Cloud orchestration technologies are rapidly evolving to support highly distributed and automated digital infrastructure. One of the most significant advancements is the widespread adoption of Kubernetes-based orchestration frameworks, with over 70% of enterprises managing containerized workloads through Kubernetes clusters. Modern orchestration platforms can coordinate thousands of containers simultaneously while automating workload scheduling, network configuration, and infrastructure scaling.

Artificial intelligence and machine learning are increasingly integrated into orchestration systems to enable predictive infrastructure management. AI-powered orchestration tools can analyze more than 1 million operational metrics per hour to detect anomalies, forecast resource demand, and automatically allocate computing resources. Organizations implementing AI-driven orchestration report up to 30% improvement in infrastructure utilization and a reduction of nearly 25% in operational incidents.

Another technological shift involves the integration of Infrastructure as Code (IaC) frameworks, allowing enterprises to deploy entire cloud environments through automated scripts. More than 65% of DevOps teams now rely on IaC-based orchestration platforms to manage hybrid and multi-cloud environments. Edge computing integration is also expanding, with orchestration platforms now capable of managing workloads across over 10,000 distributed edge nodes, supporting real-time analytics, IoT applications, and large-scale digital services.

• In May 2025, Microsoft expanded its Azure Kubernetes Service capabilities with advanced automated node scaling and integrated policy-based orchestration management, enabling enterprises to manage over 1,000 containerized workloads across hybrid cloud environments with improved deployment speed and infrastructure efficiency. Source: www.microsoft.com

• In September 2024, VMware introduced enhanced orchestration capabilities within its VMware Aria Automation platform, enabling automated provisioning and lifecycle management across multi-cloud environments. The platform now supports orchestration for more than 500 application services and integrates AI-driven workload optimization tools. Source: www.vmware.com

• In March 2025, IBM strengthened its hybrid cloud automation portfolio by expanding Red Hat OpenShift orchestration features with advanced multi-cluster management capabilities, enabling enterprises to orchestrate container deployments across more than 200 distributed environments while improving workload resilience and infrastructure visibility. Source: www.ibm.com

• In November 2024, Oracle enhanced its cloud infrastructure orchestration services by introducing automated resource orchestration across distributed Kubernetes clusters, enabling enterprise clients to manage thousands of containerized workloads with unified governance, security policies, and automated infrastructure scaling. Source: www.oracle.com

The Cloud Orchestration Market Report provides a comprehensive analysis of the global ecosystem supporting automated cloud infrastructure management. The report examines key market segments including orchestration types such as public cloud, private cloud, and hybrid cloud environments, with hybrid orchestration platforms representing more than 45% of enterprise deployments due to their ability to integrate distributed IT infrastructures.

Application coverage includes IT automation, infrastructure provisioning, application lifecycle management, and workload orchestration across multi-cloud environments. IT automation accounts for nearly 38% of enterprise deployments as organizations increasingly automate routine infrastructure operations to reduce manual intervention and improve system efficiency.

The geographic scope includes detailed analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 30 major cloud infrastructure markets and over 70 enterprise technology vendors operating within the ecosystem. The report also evaluates emerging technologies shaping the industry, including AI-driven orchestration platforms, Infrastructure as Code frameworks, container orchestration systems, and edge computing integration supporting over 10,000 distributed cloud nodes.

In addition, the report assesses industry demand across key sectors such as banking, telecommunications, healthcare, retail, and government digital infrastructure, which collectively account for more than 70% of enterprise cloud orchestration deployments globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

13.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft, IBM, Cisco Systems, VMware, Red Hat, Hewlett Packard Enterprise, Amazon Web Services, Google Cloud, BMC Software, Oracle Corporation, ServiceNow, Flexera Software, Micro Focus, CloudBolt Software, Morpheus Data |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |