Reports

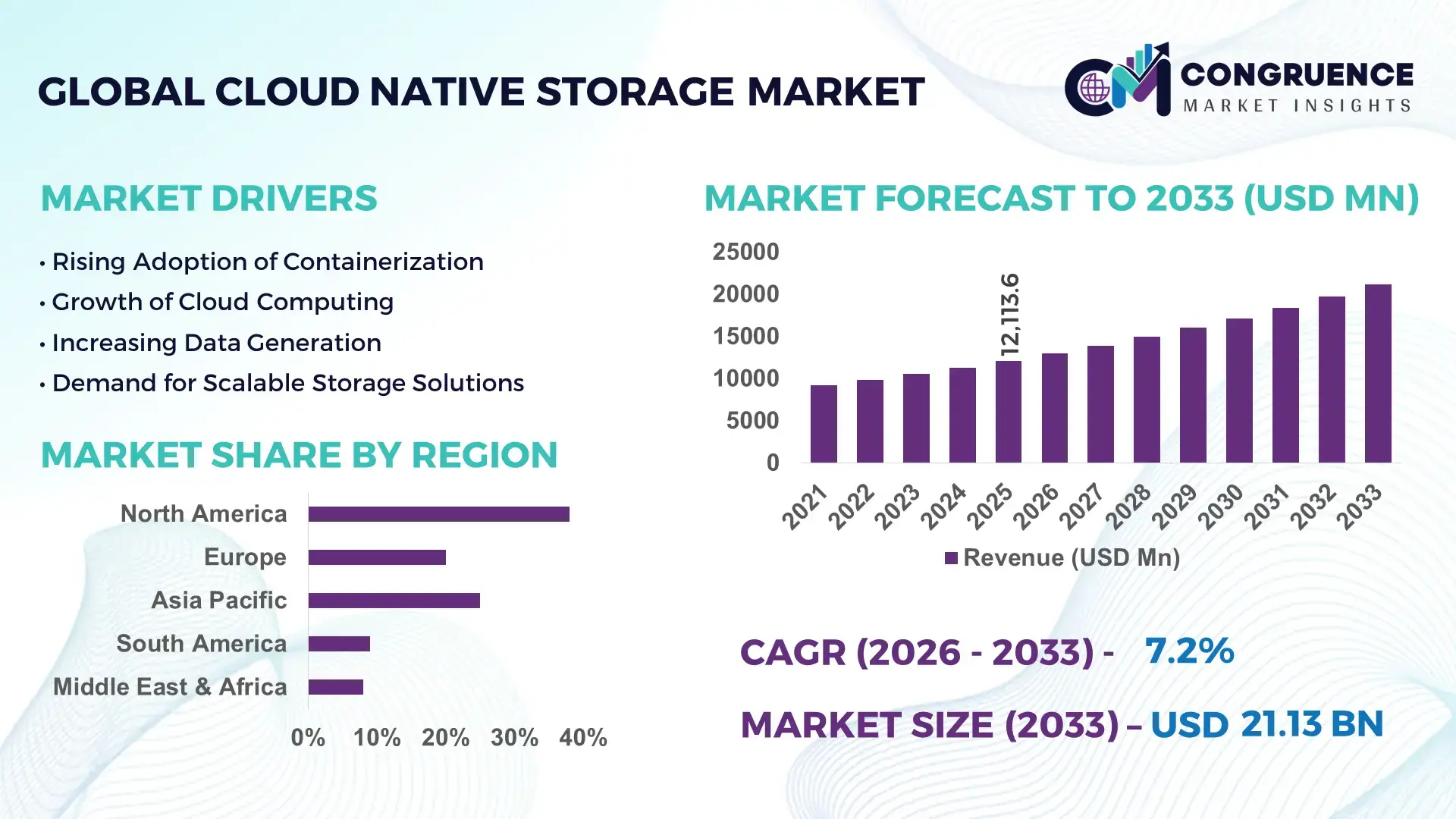

The Global Cloud Native Storage Market was valued at USD 12113.6 Million in 2025 and is anticipated to reach a value of USD 21126.69 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. The growth is primarily driven by the accelerating adoption of containerized applications and microservices architectures across enterprise IT environments.

The United States continues to dominate the cloud native storage market with advanced infrastructure and strong enterprise cloud adoption. Over 78% of large enterprises in the country have deployed Kubernetes-based environments, significantly boosting demand for scalable and persistent storage solutions. The country hosts more than 35% of global hyperscale data centers, with ongoing investments exceeding USD 50 billion annually in cloud infrastructure. Key sectors such as BFSI, healthcare, and e-commerce contribute significantly to adoption, with over 65% of organizations integrating cloud-native storage solutions for data-intensive workloads. Technological advancements, including software-defined storage and container storage interfaces, are widely implemented, enhancing operational efficiency and reducing latency by up to 40% in distributed environments.

Market Size & Growth: USD 12113.6 Million in 2025 to USD 21126.69 Million by 2033 at 7.2% CAGR, driven by increasing containerization and hybrid cloud deployments.

Top Growth Drivers: Kubernetes adoption rising by 72%, storage efficiency gains up to 45%, and enterprise cloud migration exceeding 68%.

Short-Term Forecast: By 2028, cloud-native storage solutions are expected to reduce operational costs by 30% and improve data processing speeds by 35%.

Emerging Technologies: Container Storage Interface (CSI), software-defined storage, and AI-driven data orchestration platforms are shaping the market.

Regional Leaders: North America projected at USD 8.5 Billion by 2033 with strong enterprise adoption; Asia-Pacific at USD 6.2 Billion driven by digital transformation; Europe at USD 4.9 Billion with regulatory-driven cloud integration.

Consumer/End-User Trends: BFSI and telecom sectors account for over 50% adoption due to high data throughput requirements and real-time analytics demand.

Pilot or Case Example: In 2024, a telecom provider reduced downtime by 42% through containerized storage deployment.

Competitive Landscape: Market leader holds approximately 28% share, followed by key players including major cloud and storage solution providers.

Regulatory & ESG Impact: Data localization policies and carbon-neutral data center initiatives are influencing adoption, with firms targeting 25% energy reduction by 2030.

Investment & Funding Patterns: Over USD 20 billion invested globally in cloud infrastructure and storage innovation projects in recent years.

Innovation & Future Outlook: Integration of AI-driven storage automation and edge computing is expected to redefine scalability and performance benchmarks.

Cloud native storage market growth is influenced by key sectors such as BFSI contributing nearly 28%, IT and telecom around 32%, and healthcare approximately 14% of total deployments. Recent innovations include persistent storage for Kubernetes clusters, NVMe-based cloud storage systems, and automated data lifecycle management tools. Regulatory frameworks focusing on data sovereignty and compliance are pushing enterprises toward region-specific storage solutions. Environmentally sustainable data centers and energy-efficient storage architectures are becoming priorities, particularly in Europe and Asia-Pacific. Increasing adoption of hybrid cloud strategies and edge computing solutions is further shaping consumption patterns, while future growth is expected to be driven by intelligent automation and real-time data analytics capabilities.

Cloud native storage has become a strategic cornerstone for enterprises transitioning toward digital-first, agile IT ecosystems. It enables scalable, resilient, and portable storage solutions that align with containerized workloads and microservices architecture. Organizations adopting container-native storage platforms report up to 50% faster deployment cycles compared to traditional storage systems. Kubernetes-based storage orchestration delivers 35% improvement in resource utilization compared to legacy storage architectures, significantly optimizing infrastructure costs.

North America dominates in volume due to extensive cloud infrastructure, while Asia-Pacific leads in adoption with over 62% of enterprises actively implementing cloud-native solutions for digital transformation initiatives. By 2028, AI-powered storage management systems are expected to improve workload efficiency by 40% through predictive analytics and automated resource allocation. Firms are committing to sustainability targets, including a 30% reduction in data center energy consumption by 2030 through optimized storage architectures and green computing practices.

In 2024, a leading cloud service provider in Japan achieved a 38% reduction in latency by deploying edge-integrated cloud native storage solutions, enabling faster data processing for real-time applications. Additionally, enterprises leveraging hybrid cloud-native storage models have reported up to 25% improvement in disaster recovery capabilities. The future pathway of the cloud native storage market lies in deeper integration with AI, edge computing, and multi-cloud ecosystems, positioning it as a critical enabler of resilience, regulatory compliance, and sustainable digital growth.

The widespread adoption of containerization technologies is a primary driver of the cloud native storage market. Over 75% of enterprises globally are deploying containerized applications, necessitating scalable and persistent storage solutions. Container orchestration platforms such as Kubernetes require dynamic storage provisioning, leading to increased demand for container-native storage systems. These systems enable seamless data portability, improved application performance, and efficient workload scaling. Enterprises implementing container-based storage architectures report up to 40% faster application deployment and 30% reduction in infrastructure overhead. Additionally, the growing popularity of DevOps practices and continuous integration pipelines is further accelerating adoption. Industries such as e-commerce, finance, and telecommunications are heavily investing in containerized environments to support high-volume, real-time data processing, thereby reinforcing the importance of cloud native storage solutions.

Data security and regulatory compliance remain significant restraints for the cloud native storage market. With increasing cyber threats, organizations are cautious about storing sensitive data in distributed cloud environments. Over 60% of enterprises cite data privacy concerns as a barrier to cloud-native adoption. Regulatory requirements such as data localization laws and strict compliance standards add complexity to storage deployment strategies. Managing encryption, access control, and data integrity across multi-cloud environments can increase operational challenges. Additionally, enterprises must invest in advanced security frameworks and monitoring tools, raising implementation costs. The lack of standardized security protocols across cloud platforms further complicates adoption. These challenges are particularly prominent in sectors like healthcare and banking, where data sensitivity and compliance requirements are stringent, slowing the pace of cloud native storage integration.

The rapid expansion of edge computing presents substantial growth opportunities for the cloud native storage market. With over 50 billion connected devices expected globally, data generation at the edge is increasing exponentially. Cloud native storage solutions enable efficient data processing closer to the source, reducing latency by up to 45%. Industries such as manufacturing, autonomous vehicles, and smart cities are leveraging edge-integrated storage to support real-time analytics and decision-making. The integration of cloud native storage with edge infrastructure enhances scalability and ensures seamless data synchronization across distributed environments. Additionally, advancements in lightweight storage solutions and micro data centers are enabling cost-effective deployments. As enterprises increasingly adopt edge computing to enhance operational efficiency, the demand for flexible and high-performance storage solutions is expected to grow significantly.

Integration complexities with existing legacy systems present a major challenge for the cloud native storage market. Many enterprises still rely on traditional storage infrastructures that are not compatible with modern containerized environments. Transitioning to cloud native storage requires significant architectural changes, including data migration, application refactoring, and system integration. These processes can increase implementation time by up to 35% and require specialized technical expertise. Additionally, interoperability issues between different cloud platforms and storage solutions create operational inefficiencies. Enterprises must also address compatibility concerns with legacy applications that were not designed for distributed environments. The lack of standardized frameworks for seamless integration further complicates adoption. These challenges often lead to increased costs and slower deployment timelines, hindering the widespread adoption of cloud native storage solutions across traditional enterprise environments.

• Accelerated Kubernetes-Based Storage Adoption: Kubernetes-native storage integration has surged significantly, with over 72% of enterprises deploying container orchestration platforms now relying on persistent storage frameworks. This trend is driven by the need for scalable and dynamic workload management, with organizations reporting up to 40% improvement in deployment efficiency and 33% reduction in provisioning time. Cloud-native storage platforms supporting Container Storage Interface (CSI) standards have increased by 60% across enterprise environments, enhancing interoperability and automation capabilities in multi-cloud infrastructures.

• Expansion of Edge-Integrated Storage Architectures: The integration of cloud native storage with edge computing is gaining strong momentum, with nearly 48% of enterprises deploying edge storage solutions to support real-time analytics. These systems have reduced latency by up to 45% and improved data processing speeds by 38% in sectors such as manufacturing and telecommunications. The number of edge-enabled micro data centers has increased by over 35% globally, reflecting a growing demand for localized data processing and storage resilience in distributed environments.

• AI-Driven Storage Optimization and Automation: Artificial intelligence is increasingly embedded in cloud native storage platforms, with over 58% of enterprises implementing AI-based data management tools. These solutions deliver up to 37% improvement in storage utilization and reduce manual intervention by 42%. Automated workload balancing and predictive analytics have enabled organizations to achieve up to 30% lower operational overhead. AI-enabled anomaly detection systems are also improving data security by identifying potential threats with 28% greater accuracy compared to traditional monitoring tools.

• Rising Demand for Sustainable and Energy-Efficient Storage Systems: Sustainability initiatives are reshaping storage infrastructure strategies, with approximately 65% of data center operators prioritizing energy-efficient cloud-native storage solutions. Advanced storage architectures are delivering up to 32% reduction in power consumption and 27% lower carbon emissions. Adoption of liquid cooling and energy-optimized storage hardware has increased by 29%, particularly in Europe and Asia-Pacific, where regulatory frameworks emphasize environmental compliance and green IT practices.

The cloud native storage market segmentation reflects a structured approach across types, applications, and end-user industries, enabling targeted adoption strategies. By type, container-native storage and software-defined storage dominate due to their flexibility and scalability in dynamic environments. Application-wise, data-intensive workloads such as analytics, DevOps, and backup solutions are key drivers, with analytics accounting for over 35% of deployments. From an end-user perspective, IT and telecom sectors lead adoption with more than 30% share, followed by BFSI and healthcare industries. Increasing adoption of hybrid cloud environments, coupled with growing demand for real-time data processing, is influencing segmentation dynamics. Enterprises are prioritizing storage solutions that offer interoperability, high availability, and compliance capabilities, shaping a competitive and innovation-driven market landscape.

Cloud native storage solutions are categorized into container-native storage, software-defined storage, and object storage systems. Container-native storage leads the segment, accounting for approximately 46% of adoption due to its seamless integration with Kubernetes environments and ability to provide persistent storage for containerized applications. Software-defined storage holds around 32% share, offering flexibility and centralized management across hybrid cloud ecosystems. Object storage solutions, while accounting for 22%, are gaining traction for unstructured data storage and scalability needs. Container-native storage is also the fastest-growing segment, expanding at an estimated CAGR of 9.1%, driven by increasing enterprise adoption of microservices architectures and container orchestration platforms. The demand for real-time data processing and portability is further accelerating its growth. Other storage types collectively contribute to nearly 54% of the market, highlighting the diversified deployment strategies across industries.

The application landscape of cloud native storage includes data analytics, backup and disaster recovery, DevOps, and content management systems. Data analytics emerges as the leading application, holding approximately 38% share due to the exponential growth of structured and unstructured data. Backup and disaster recovery account for around 27%, driven by the need for data resilience and business continuity. DevOps applications contribute nearly 20%, while other applications collectively represent 15% of the market. Backup and disaster recovery is the fastest-growing application segment, with an estimated CAGR of 8.7%, supported by increasing cyber threats and stringent data protection requirements. Organizations are prioritizing cloud-native storage to ensure rapid recovery and minimal downtime.

End-user segmentation in the cloud native storage market is led by IT and telecommunications, accounting for approximately 34% of total adoption due to high data throughput requirements and continuous service delivery demands. BFSI follows with around 26%, leveraging cloud-native storage for secure transaction processing and regulatory compliance. Healthcare contributes approximately 16%, driven by the need for real-time patient data access and analytics. Other sectors, including retail, manufacturing, and government, collectively account for 24% of the market. The healthcare sector is the fastest-growing end-user segment, expanding at an estimated CAGR of 8.9%, fueled by increasing adoption of digital health technologies and electronic health records. IT and telecom continue to dominate, but emerging industries are rapidly integrating cloud-native storage to support digital transformation initiatives.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America benefits from over 65% enterprise cloud adoption and more than 40% of global hyperscale data center capacity, supporting large-scale deployment of cloud native storage platforms. Europe follows with approximately 27% market share, driven by regulatory-led cloud adoption and over 55% enterprise compliance-driven deployments. Asia-Pacific holds around 24% share but is rapidly expanding due to digital transformation, with over 62% of enterprises adopting hybrid cloud solutions. South America accounts for nearly 6% share, supported by growing telecom infrastructure and a 28% increase in cloud investments. The Middle East & Africa region contributes approximately 5%, with over 30% growth in data center expansion projects and increasing adoption in sectors such as oil & gas and smart city initiatives.

How are advanced enterprise cloud ecosystems accelerating next-generation storage adoption?

North America holds approximately 38% of the global cloud native storage market, supported by strong adoption across BFSI, healthcare, and IT sectors, which collectively account for over 60% of regional demand. The region benefits from more than 70% enterprise penetration of containerized applications, significantly driving storage requirements. Government initiatives promoting cloud-first strategies and data security compliance frameworks have accelerated adoption. Technological advancements such as AI-driven storage orchestration and software-defined storage are improving efficiency by up to 35%. A key regional player has expanded its container-native storage capabilities to support over 10,000 enterprise clients, enhancing workload scalability and reducing latency by 30%. Consumer behavior reflects high reliance on secure, compliant storage solutions, particularly in finance and healthcare industries, where real-time data access and regulatory compliance are critical.

What factors are shaping secure and compliant storage transformation strategies?

Europe accounts for approximately 27% of the global cloud native storage market, with major contributions from Germany, the United Kingdom, and France, which together represent over 65% of regional demand. Strict regulatory frameworks focusing on data protection and sovereignty have driven over 58% of enterprises to adopt compliant cloud-native storage solutions. Sustainability initiatives targeting a 30% reduction in carbon emissions have also influenced storage infrastructure decisions. The region has seen a 33% increase in adoption of energy-efficient storage technologies and hybrid cloud systems. A leading regional technology provider has implemented green data storage solutions, reducing energy consumption by 25% across enterprise deployments. Consumer behavior is heavily influenced by regulatory requirements, leading to increased demand for secure, transparent, and explainable storage solutions across industries such as finance and government.

How is rapid digital expansion transforming scalable storage ecosystems?

Asia-Pacific ranks as the fastest-growing region, accounting for approximately 24% of global market volume, with China, India, and Japan contributing over 70% of regional demand. The region has witnessed a 60% increase in cloud infrastructure investments, driven by digital transformation initiatives and expanding e-commerce ecosystems. Over 65% of enterprises are adopting cloud-native architectures to support mobile applications and real-time analytics. Technological hubs are driving innovation, with more than 40% of startups focusing on cloud-based solutions. A regional cloud service provider recently expanded its storage infrastructure to support over 8,000 enterprises, improving data processing efficiency by 34%. Consumer behavior is influenced by mobile-first usage patterns and growing demand for scalable, cost-effective storage solutions, particularly in sectors such as retail, fintech, and telecommunications.

What role do evolving telecom and digital services play in storage adoption?

South America holds around 6% of the global cloud native storage market, with Brazil and Argentina accounting for nearly 70% of regional demand. The region has experienced a 25% increase in telecom infrastructure investments, driving the need for scalable storage solutions. Government policies supporting digital transformation and cross-border data exchange have encouraged adoption, with over 40% of enterprises transitioning to cloud-based systems. The energy sector and media industries are key contributors, leveraging cloud-native storage for data-intensive applications. A regional telecom provider has deployed cloud-native storage solutions across its network, reducing downtime by 28% and improving service delivery efficiency. Consumer behavior is closely tied to digital media consumption and localized content delivery, increasing demand for flexible and high-performance storage systems.

How are digital infrastructure investments enabling scalable storage ecosystems?

The Middle East & Africa region accounts for approximately 5% of the global cloud native storage market, with the UAE and South Africa contributing over 55% of regional demand. Rapid digital transformation initiatives, including smart city projects, have driven a 30% increase in cloud infrastructure investments. The oil & gas and construction sectors are major adopters, utilizing cloud-native storage for real-time data monitoring and analytics. Governments are implementing policies to support digital economies, with over 35% of enterprises adopting cloud-based solutions. A regional technology firm has introduced advanced storage platforms that improve data processing efficiency by 32%. Consumer behavior reflects increasing reliance on digital services and mobile applications, driving demand for scalable and secure storage infrastructure across various industries.

United States Cloud Native Storage Market – 38% share: High enterprise cloud adoption exceeding 78% and extensive hyperscale data center infrastructure.

China Cloud Native Storage Market – 18% share: Rapid digital transformation and over 65% enterprise adoption of cloud-native technologies supporting large-scale deployments.

The cloud native storage market is characterized by a moderately consolidated yet innovation-driven competitive landscape, with over 60 active global and regional players competing across enterprise and cloud segments. The top five companies collectively account for approximately 54% of the market, reflecting a strong concentration of technological expertise and infrastructure capabilities. Market leaders are focusing on expanding container-native storage offerings, with over 70% of major vendors integrating Kubernetes-compatible solutions into their portfolios. Strategic partnerships and collaborations have increased by 35%, enabling companies to enhance interoperability across multi-cloud environments. Product innovation remains a key differentiator, with nearly 50% of firms investing in AI-driven storage management and automation technologies. Mergers and acquisitions have risen by 22%, aimed at strengthening capabilities in edge computing and hybrid cloud storage. Additionally, companies are prioritizing sustainability, with over 40% implementing energy-efficient storage solutions. Competitive positioning is increasingly defined by scalability, performance optimization, and compliance capabilities, making innovation and strategic alliances critical for long-term market success.

NetApp

Dell Technologies

Hewlett Packard Enterprise (HPE)

IBM Corporation

Pure Storage

VMware

Red Hat

Portworx

StorageOS

Robin.io

Scality

MinIO

SUSE

Cloud native storage technologies are rapidly evolving to support containerized workloads, microservices architectures, and distributed computing environments. One of the most influential advancements is the widespread adoption of the Container Storage Interface (CSI), now implemented in over 70% of Kubernetes deployments, enabling seamless integration between storage systems and orchestration platforms. CSI-based architectures have improved provisioning efficiency by approximately 35% while reducing manual configuration overhead by nearly 40%.

Software-defined storage (SDS) continues to gain traction, accounting for more than 60% of enterprise deployments due to its flexibility and ability to decouple hardware from storage management. SDS solutions are enabling organizations to achieve up to 30% better resource utilization and 25% reduction in storage costs through centralized control and automation. Additionally, NVMe-over-Fabrics (NVMe-oF) technology is being increasingly deployed, delivering latency reductions of up to 50% and significantly enhancing data throughput for high-performance applications such as AI analytics and real-time processing.

Artificial intelligence and machine learning are being integrated into cloud native storage platforms, with over 55% of enterprises adopting AI-driven storage optimization tools. These systems provide predictive analytics for workload balancing, resulting in up to 38% improvement in storage efficiency and 32% reduction in downtime. Edge-native storage is also emerging as a critical innovation, with nearly 45% of organizations deploying edge storage nodes to support low-latency applications, reducing data processing delays by up to 42%.

Furthermore, multi-cloud and hybrid cloud storage architectures are becoming standard, with over 65% of enterprises adopting cross-cloud storage strategies to enhance redundancy and avoid vendor lock-in. Advances in data encryption, zero-trust security frameworks, and automated lifecycle management are further strengthening the reliability and compliance of cloud native storage systems, making them essential for modern enterprise infrastructure.

• In November 2025, NetApp expanded its Astra Control platform with advanced Kubernetes data management capabilities, enabling enterprises to automate application-aware data protection across hybrid cloud environments. The update improved workload mobility and reduced backup recovery times by up to 30%. Source: www.netapp.com

• In April 2025, Dell Technologies introduced enhancements to its PowerFlex software-defined storage platform, integrating Kubernetes-native support and automation features. The upgrade enabled enterprises to scale storage resources dynamically, improving operational efficiency by approximately 35% in containerized environments. Source: www.delltechnologies.com

• In September 2024, VMware announced updates to its Tanzu portfolio, strengthening its cloud native storage capabilities with improved container storage orchestration and multi-cloud compatibility. The enhancements allowed enterprises to streamline Kubernetes deployment workflows and increase infrastructure utilization by over 25%. Source: www.vmware.com

• In February 2024, Pure Storage launched an updated version of Portworx Enterprise with enhanced data security and ransomware protection features. The release introduced automated backup and disaster recovery capabilities, reducing system downtime by up to 40% for mission-critical applications. Source: www.purestorage.com

The cloud native storage market report provides a comprehensive analysis of a rapidly evolving digital infrastructure segment, covering multiple dimensions of technology, deployment models, and industry applications. The scope includes detailed segmentation across storage types such as container-native storage, software-defined storage, and object-based storage systems, collectively representing over 90% of modern enterprise deployments. The report also examines application areas including data analytics, DevOps, backup and disaster recovery, and content management, which together account for more than 80% of storage utilization across industries.

Geographically, the report spans key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering over 95% of global cloud infrastructure deployments. It highlights regional variations in adoption, with enterprise cloud penetration exceeding 70% in developed markets and rapidly increasing in emerging economies. The analysis also incorporates industry-specific insights, focusing on sectors such as IT and telecommunications, BFSI, healthcare, retail, and manufacturing, which together contribute over 85% of market demand.

Technological coverage includes emerging innovations such as AI-driven storage automation, NVMe-based architectures, edge-native storage solutions, and hybrid multi-cloud ecosystems. The report further explores regulatory and compliance frameworks impacting deployment strategies, including data sovereignty and cybersecurity requirements. Additionally, it evaluates infrastructure trends such as the expansion of hyperscale data centers, which have grown by more than 30% globally in recent years. This structured scope ensures that decision-makers gain a holistic understanding of market dynamics, technological advancements, and strategic opportunities within the cloud native storage ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NetApp, Dell Technologies, Hewlett Packard Enterprise (HPE), IBM Corporation, Pure Storage, VMware, Red Hat, Portworx, StorageOS, Robin.io, Scality, MinIO, SUSE |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |