Reports

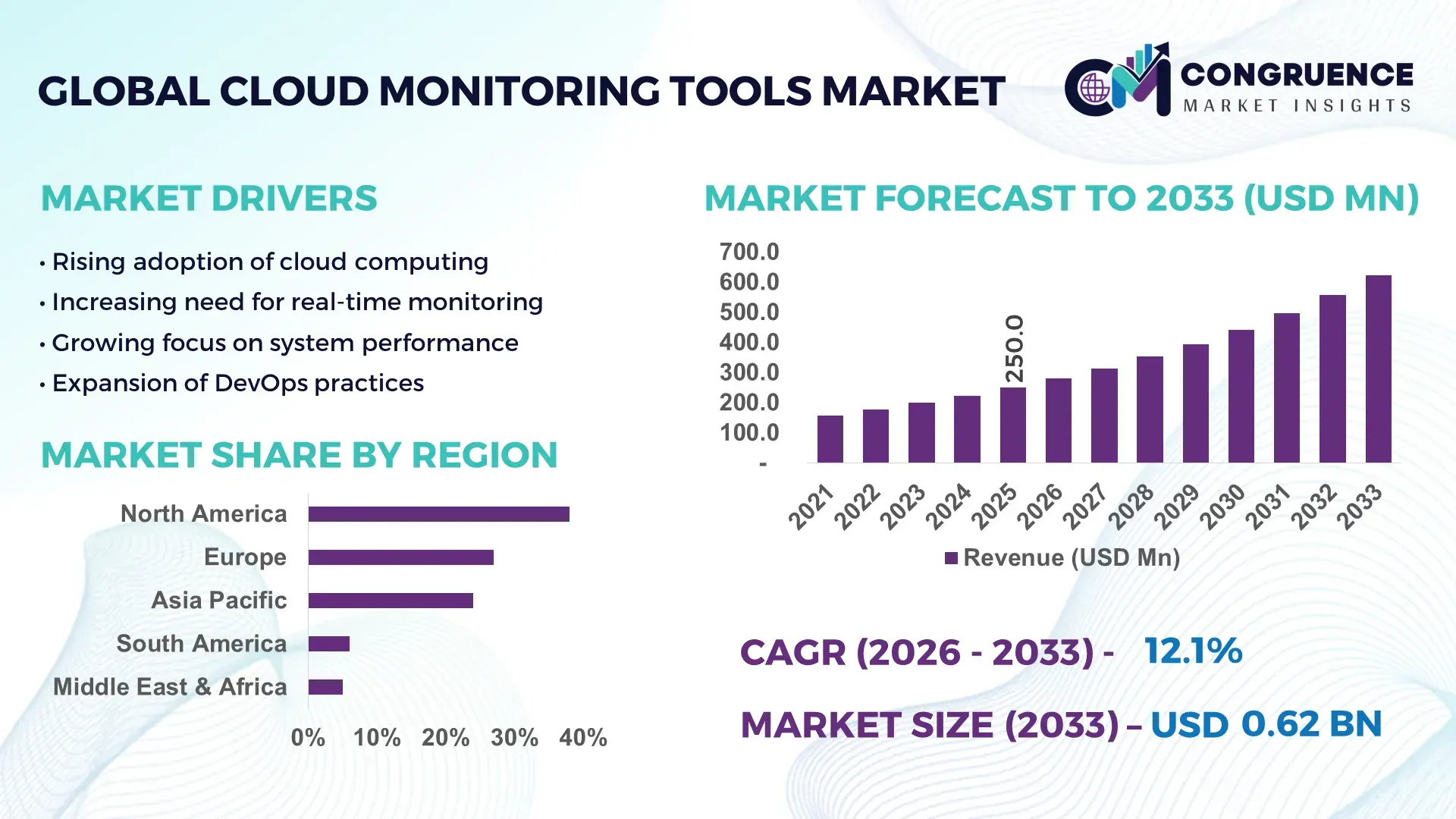

The Global Cloud Monitoring Tools Market was valued at USD 250.0 Million in 2025 and is anticipated to reach a value of USD 623.4 Million by 2033 expanding at a CAGR of 12.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. Increasing multi-cloud adoption and rising demand for real-time performance visibility are driving market expansion.

The United States leads the Cloud Monitoring Tools Market with strong enterprise cloud penetration exceeding 94% among large organizations and over 67% among SMEs. The country hosts more than 40% of global hyperscale data centers, supporting high demand for monitoring tools. Over 72% of enterprises deploy multi-cloud environments, increasing complexity and driving monitoring adoption. Key sectors such as BFSI, healthcare, and e-commerce contribute significantly, with BFSI alone accounting for nearly 28% of enterprise cloud monitoring tool usage. Investments in cloud infrastructure exceeded USD 120 billion annually, with continuous advancements in AI-driven observability, predictive analytics, and automated remediation enhancing system performance and reducing downtime by up to 35%.

Market Size & Growth: USD 250.0 Million in 2025, projected to reach USD 623.4 Million by 2033 at 12.1% CAGR, driven by increasing multi-cloud complexity.

Top Growth Drivers: Multi-cloud adoption (72%), DevOps integration (65%), automation efficiency gains (48%).

Short-Term Forecast: By 2028, enterprises may reduce downtime by 30% through AI-based monitoring.

Emerging Technologies: AI-driven observability, AIOps platforms, serverless monitoring tools.

Regional Leaders: North America (USD 220M by 2033), Europe (USD 160M), Asia-Pacific (USD 140M) with rapid cloud-native adoption trends.

Consumer/End-User Trends: BFSI and IT sectors account for over 55% combined usage, with growing SME adoption.

Pilot or Case Example: In 2025, a fintech firm reduced system downtime by 32% using AI-powered monitoring.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 major players intensifying innovation.

Regulatory & ESG Impact: Data compliance laws impact 60% of deployments, promoting secure monitoring tools.

Investment & Funding Patterns: Over USD 15 billion invested in cloud monitoring and observability platforms globally.

Innovation & Future Outlook: Integration of predictive analytics and autonomous monitoring shaping future deployments.

Cloud Monitoring Tools Market is influenced by IT & telecom (35%), BFSI (28%), healthcare (15%), and retail (12%). AI-enabled monitoring solutions improved anomaly detection accuracy by over 40%. Regulatory frameworks emphasizing data sovereignty are shaping deployment models. North America dominates consumption, while Asia-Pacific shows fastest adoption due to digital transformation initiatives. Increasing integration with DevOps and AIOps platforms is expected to drive long-term innovation and operational efficiency.

Cloud Monitoring Tools Market holds strategic importance as enterprises shift toward distributed cloud ecosystems and hybrid infrastructures. Organizations are increasingly adopting observability frameworks that combine logs, metrics, and traces to improve system visibility and resilience. AI-driven monitoring delivers 45% faster incident detection compared to traditional rule-based systems, significantly enhancing operational efficiency. The integration of AIOps platforms is enabling predictive maintenance and automated remediation, reducing human intervention by nearly 38%.

In terms of regional dynamics, North America dominates in volume, while Asia-Pacific leads in adoption with over 68% of enterprises accelerating cloud-first strategies. Europe is witnessing strong uptake driven by regulatory compliance requirements such as data localization mandates. By 2028, AI-enabled monitoring is expected to reduce system downtime by 35% while improving application performance by over 28%. Firms are committing to ESG metrics, including reducing IT-related carbon emissions by 25% through optimized resource utilization and energy-efficient cloud operations.

A comparative benchmark shows that AI-driven observability platforms deliver 40% improvement compared to traditional monitoring systems in anomaly detection and response time. In 2025, a major US-based enterprise achieved a 33% reduction in incident resolution time using automated monitoring tools integrated with DevOps pipelines. Looking forward, the Cloud Monitoring Tools Market is positioned as a core pillar of enterprise resilience, compliance readiness, and sustainable digital infrastructure growth.

The Cloud Monitoring Tools Market is evolving rapidly with the increasing complexity of cloud-native architectures, containerized applications, and hybrid IT environments. Enterprises are deploying advanced monitoring tools to gain visibility into distributed systems, ensuring uptime and performance optimization. Over 70% of organizations now use at least two cloud platforms, increasing the need for centralized monitoring solutions. The rise of microservices architecture has further intensified demand, as it requires granular monitoring of application components.

Automation and AI integration are key influencing factors, with over 60% of enterprises adopting AIOps solutions to enhance monitoring efficiency. Security concerns are also shaping market dynamics, as nearly 55% of organizations prioritize real-time threat detection within monitoring platforms. The demand for compliance-driven monitoring tools has increased by 42% due to stringent data protection regulations globally. Additionally, cost optimization is a major driver, with companies aiming to reduce cloud spending by 20–30% through efficient monitoring practices.

The growing adoption of multi-cloud environments is a major driver of the Cloud Monitoring Tools Market. Over 72% of enterprises operate in multi-cloud setups, creating challenges in managing performance, security, and cost across different platforms. Monitoring tools provide centralized visibility, enabling organizations to track system health and performance in real time. The rise of containerization technologies such as Kubernetes has increased monitoring complexity by over 50%, further driving demand. Additionally, DevOps adoption has surged by 65%, requiring continuous monitoring to support rapid deployment cycles. Organizations using advanced monitoring tools report up to 35% improvement in system uptime and 28% faster issue resolution. This growing need for efficiency and reliability is accelerating market expansion.

Despite strong growth potential, implementation complexity remains a significant restraint in the Cloud Monitoring Tools Market. Over 48% of enterprises report difficulties integrating monitoring tools with legacy systems and diverse cloud environments. The lack of standardized protocols across cloud providers creates interoperability challenges, increasing deployment time by up to 30%. Additionally, skilled workforce shortages impact adoption, with nearly 40% of organizations lacking expertise in managing advanced monitoring solutions. High initial setup efforts and configuration requirements also limit adoption among SMEs. Furthermore, data overload from monitoring tools can reduce operational efficiency, with companies reporting up to 25% increase in alert fatigue. These challenges hinder seamless deployment and slow overall market growth.

AI-driven observability presents significant opportunities in the Cloud Monitoring Tools Market. Over 60% of enterprises are investing in AIOps platforms to enhance predictive monitoring capabilities. AI-based tools can reduce incident detection time by 45% and improve root cause analysis accuracy by 38%. The increasing adoption of edge computing, expected to involve over 50% of enterprise data processing, is creating demand for decentralized monitoring solutions. Additionally, industries such as healthcare and finance are leveraging AI monitoring to ensure compliance and improve operational efficiency. Cloud-native businesses adopting AI-powered monitoring report up to 30% cost savings through resource optimization. These advancements are opening new growth avenues and expanding market potential.

Data security and compliance remain critical challenges in the Cloud Monitoring Tools Market. Over 55% of organizations cite data privacy concerns as a barrier to adopting cloud monitoring solutions. Regulations such as GDPR and regional data protection laws require strict compliance, increasing deployment complexity. Monitoring tools handling sensitive data must ensure encryption and secure access, which can increase operational costs by up to 20%. Additionally, cyber threats targeting cloud environments have increased by 35%, requiring continuous security monitoring. The lack of standardized security frameworks across cloud platforms further complicates implementation. Organizations must invest in secure monitoring infrastructures, making it challenging for smaller enterprises to adopt advanced solutions.

AI-driven anomaly detection adoption exceeds 60% across enterprises: Organizations are increasingly leveraging AI-based monitoring tools, with over 62% deploying machine learning algorithms to detect anomalies in real time. These systems improve detection accuracy by 40% and reduce false alerts by nearly 30%, enhancing operational efficiency and reducing manual intervention.

Container and Kubernetes monitoring usage surpasses 55% adoption rate: With containerized applications becoming mainstream, more than 57% of enterprises now monitor Kubernetes environments. This has improved application deployment efficiency by 35% while reducing system failures by approximately 22% in large-scale distributed environments.

Serverless and edge monitoring demand grows by over 45%: The rise of serverless computing and edge deployments has increased demand for specialized monitoring tools. Around 48% of organizations have adopted serverless monitoring, improving latency performance by 27% and enabling real-time data processing across distributed systems.

Integration with DevOps pipelines improves release cycles by 30%: Over 65% of DevOps teams integrate monitoring tools into CI/CD pipelines, leading to 30% faster deployment cycles and a 25% reduction in post-release issues. This trend is transforming monitoring from reactive to proactive system management.

The Cloud Monitoring Tools Market is segmented based on type, application, and end-user, each contributing uniquely to the overall ecosystem. Types include infrastructure monitoring, application performance monitoring (APM), network monitoring, and database monitoring, with APM leading adoption due to increasing demand for application visibility. Applications span across IT operations, security monitoring, and performance optimization, with IT operations holding the largest share due to widespread enterprise cloud adoption. End-users include BFSI, IT & telecom, healthcare, retail, and government sectors, with IT & telecom dominating usage due to high cloud dependency. Increasing demand for real-time monitoring, automation, and compliance-driven solutions is shaping segmentation trends. Enterprises are prioritizing integrated monitoring platforms to streamline operations and improve system reliability across distributed cloud environments.

Application Performance Monitoring (APM) leads the segment with approximately 38% share due to its critical role in ensuring application uptime and performance visibility. Infrastructure monitoring accounts for around 27%, while network monitoring contributes nearly 18%. APM dominance is driven by increasing reliance on cloud-native applications and microservices architecture. Infrastructure monitoring remains essential for managing compute and storage resources across cloud environments. The fastest-growing segment is AI-driven observability tools, expanding at an estimated CAGR of 14.5%, driven by demand for predictive analytics and automation. Database monitoring and log management tools together hold a combined share of approximately 17%, serving niche but essential use cases.

• In 2025, a global cloud provider deployed AI-based APM tools across 10,000+ applications, improving performance monitoring efficiency by 35% and reducing incident response time significantly.

IT operations dominate with a 42% share due to widespread enterprise cloud adoption and the need for continuous monitoring. Security monitoring accounts for 28%, reflecting rising cybersecurity concerns. Performance optimization applications contribute around 18%, while other applications collectively hold 12%. Security monitoring is the fastest-growing segment with a CAGR of approximately 13.2%, driven by increasing cyber threats and compliance requirements. In 2025, more than 41% of enterprises globally reported integrating monitoring tools into security frameworks. Additionally, over 58% of organizations prioritize real-time threat detection.

• In 2025, over 150 global enterprises implemented integrated monitoring platforms for security and IT operations, improving threat detection efficiency by 33%.

IT & telecom leads with a 36% share due to heavy reliance on cloud infrastructure. BFSI follows with 28%, driven by regulatory compliance needs. Healthcare and retail contribute 14% and 12% respectively, while other sectors account for 10%. Healthcare is the fastest-growing end-user segment with a CAGR of 13.8%, supported by increasing digital health adoption and data monitoring requirements. In 2025, over 45% of hospitals globally implemented cloud monitoring tools for patient data systems. Additionally, 52% of enterprises reported increased reliance on monitoring tools for operational continuity.

• In 2025, a large healthcare network implemented cloud monitoring across 200+ facilities, improving system uptime by 29% and reducing IT incidents significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.5% between 2026 and 2033.

North America benefits from high cloud adoption, with over 90% enterprise penetration, while Europe holds around 27% share driven by compliance-focused deployments. Asia-Pacific accounts for approximately 24%, supported by rapid digital transformation across China, India, and Japan. South America and Middle East & Africa collectively contribute 11%, with increasing investments in cloud infrastructure. Over 65% of enterprises in developed regions have adopted advanced monitoring tools, while emerging regions show adoption rates of 35–45%, indicating strong growth potential.

North America holds approximately 38% market share driven by strong cloud adoption across BFSI, healthcare, and IT sectors. Over 90% of large enterprises use cloud services, creating demand for advanced monitoring tools. Regulatory frameworks such as data protection laws and cybersecurity standards influence adoption. Technological advancements including AI-based monitoring and automation are widely implemented, improving system efficiency by over 30%. A major player in the region has introduced AI-driven monitoring platforms that reduce downtime significantly. Consumer behavior shows higher enterprise adoption in healthcare and finance, with over 70% of organizations prioritizing real-time monitoring solutions.

Europe accounts for approximately 27% of the market, with key countries including Germany, the UK, and France leading adoption. Regulatory frameworks such as GDPR drive demand for secure and compliant monitoring solutions. Around 65% of enterprises prioritize data governance in monitoring deployments. Emerging technologies such as AI and automation are increasingly integrated, improving efficiency by 25%. A regional cloud provider has launched compliance-focused monitoring tools tailored for regulated industries. Consumer behavior reflects strong demand for transparent and explainable monitoring solutions due to regulatory pressure.

Asia-Pacific holds around 24% market share and ranks as the fastest-growing region. China, India, and Japan are key contributors, with over 68% of enterprises adopting cloud-first strategies. Rapid expansion of digital infrastructure and e-commerce is driving demand. Innovation hubs in India and China are leading advancements in AI-based monitoring. A regional technology firm has deployed scalable monitoring tools supporting thousands of SMEs. Consumer behavior shows growth driven by mobile applications and cloud-native startups, with adoption rates increasing by over 40% in recent years.

South America accounts for approximately 6% of the market, with Brazil and Argentina leading adoption. Infrastructure modernization and digital transformation initiatives are key drivers. Over 45% of enterprises are adopting cloud-based solutions, increasing demand for monitoring tools. Government policies supporting IT infrastructure development are boosting adoption. A regional player has introduced cost-effective monitoring tools tailored for SMEs. Consumer behavior shows demand tied to media and localization services, with increasing adoption in digital content platforms.

Middle East & Africa holds around 5% share, with UAE and South Africa as key markets. Demand is driven by sectors such as oil & gas, construction, and finance. Over 50% of enterprises are investing in cloud modernization initiatives. Technological advancements including AI monitoring tools are being adopted gradually. Government-led digital transformation programs are supporting growth. A local provider has launched monitoring solutions tailored for energy sector applications. Consumer behavior shows increasing demand for scalable and secure monitoring solutions.

United States – 34% Market share: strong enterprise cloud adoption and high data center capacity

China – 18% Market share: rapid digital infrastructure expansion and growing enterprise cloud usage

The Cloud Monitoring Tools Market is moderately fragmented with over 50 active global and regional players competing across different segments. The top five companies collectively hold approximately 55% of the market share, indicating a semi-consolidated structure. Leading players focus on AI-driven observability, automation, and integration with DevOps pipelines to maintain competitive advantage. Strategic initiatives such as partnerships, mergers, and acquisitions are increasing, with over 20 major collaborations recorded in the past two years.

Product innovation remains a key competitive factor, with more than 60% of vendors investing in AI-based monitoring capabilities. Cloud-native solutions are gaining traction, with 70% of new product launches targeting hybrid and multi-cloud environments. Companies are also focusing on expanding regional presence, particularly in Asia-Pacific, where adoption rates are rising rapidly. Pricing strategies and subscription-based models are widely used, with over 65% of vendors offering SaaS-based monitoring solutions. The competitive landscape is expected to intensify as new entrants introduce innovative solutions and existing players enhance their technological capabilities.

Microsoft Azure

Google Cloud

IBM Corporation

Oracle Corporation

Cisco Systems Inc.

Datadog Inc.

New Relic Inc.

Dynatrace Inc.

Splunk Inc.

SolarWinds Corporation

LogicMonitor Inc.

PagerDuty Inc.

BMC Software Inc.

The Cloud Monitoring Tools Market is witnessing rapid technological evolution driven by advancements in AI, machine learning, and automation. AI-powered monitoring solutions are now used by over 60% of enterprises to enhance anomaly detection and predictive analytics. These tools improve system performance monitoring accuracy by approximately 40% and reduce downtime by up to 35%. AIOps platforms are gaining significant traction, enabling automated root cause analysis and reducing manual intervention by nearly 38%.

Container monitoring technologies are also expanding, with more than 55% of enterprises deploying Kubernetes-based environments. This has led to increased demand for specialized monitoring tools capable of tracking microservices and distributed applications. Serverless monitoring is another emerging trend, with adoption rates exceeding 45%, driven by the growth of cloud-native applications. These tools help improve application performance by 25–30% through real-time data analysis.

Edge computing integration is further influencing the market, with over 50% of enterprise data expected to be processed at the edge. Monitoring tools are evolving to support decentralized environments, ensuring low-latency performance and real-time insights. Additionally, integration with DevOps pipelines is enhancing deployment efficiency, with organizations reporting 30% faster release cycles. Advanced visualization tools and dashboards are improving data interpretation, enabling better decision-making. These technological advancements are positioning cloud monitoring tools as essential components of modern IT infrastructure.

• In June 2025, Datadog announced new AI-powered observability capabilities including AI Agent Monitoring, LLM Experiments, and AI Agents Console, enabling organizations to monitor agentic AI systems, test model performance, and improve deployment visibility across complex cloud environments. Source: www.datadoghq.com

• In June 2025, Datadog expanded its log management suite with Flex Frozen and Archive Search, allowing enterprises to optimize log storage, meet data residency requirements, and improve compliance for regulated industries such as healthcare and financial services.

• In December 2025, Datadog introduced Agent Builder and Secret Scanning capabilities, enabling AI agents to analyze monitoring data and automatically detect credential leaks in CI/CD pipelines, enhancing real-time security monitoring and automated threat prevention.

• In June 2025, Datadog enhanced platform interoperability by enabling native OpenTelemetry (OTel) metrics integration, allowing enterprises to unify observability data across cloud-native and third-party systems without additional configuration, improving monitoring consistency across hybrid environments.

The Cloud Monitoring Tools Market Report provides a comprehensive analysis of key segments including type, application, end-user, and regional markets. The report covers major product categories such as application performance monitoring, infrastructure monitoring, network monitoring, and database monitoring, highlighting their adoption trends and operational significance. Applications analyzed include IT operations, security monitoring, and performance optimization, each contributing to enterprise efficiency and system reliability.

The report evaluates end-user industries including IT & telecom, BFSI, healthcare, retail, and government, with detailed insights into adoption rates and usage patterns. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering a holistic view of regional dynamics and growth potential. The analysis includes over 20 countries, focusing on cloud adoption levels, infrastructure investments, and technological advancements.

Additionally, the report explores emerging technologies such as AI-driven monitoring, AIOps platforms, and edge computing integration. It also examines enterprise trends such as multi-cloud adoption, DevOps integration, and automation strategies. The scope includes analysis of competitive landscape, innovation trends, and regulatory frameworks shaping the market. The report is designed to support decision-makers with actionable insights, enabling strategic planning and investment decisions across the cloud monitoring ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 250.0 Million |

| Market Revenue (2033) | USD 623.4 Million |

| CAGR (2026–2033) | 12.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Amazon Web Services; Microsoft Azure; Google Cloud; IBM Corporation; Oracle Corporation; Cisco Systems Inc.; Datadog Inc.; New Relic Inc.; Dynatrace Inc.; Splunk Inc.; SolarWinds Corporation; LogicMonitor Inc.; PagerDuty Inc.; BMC Software Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |