Reports

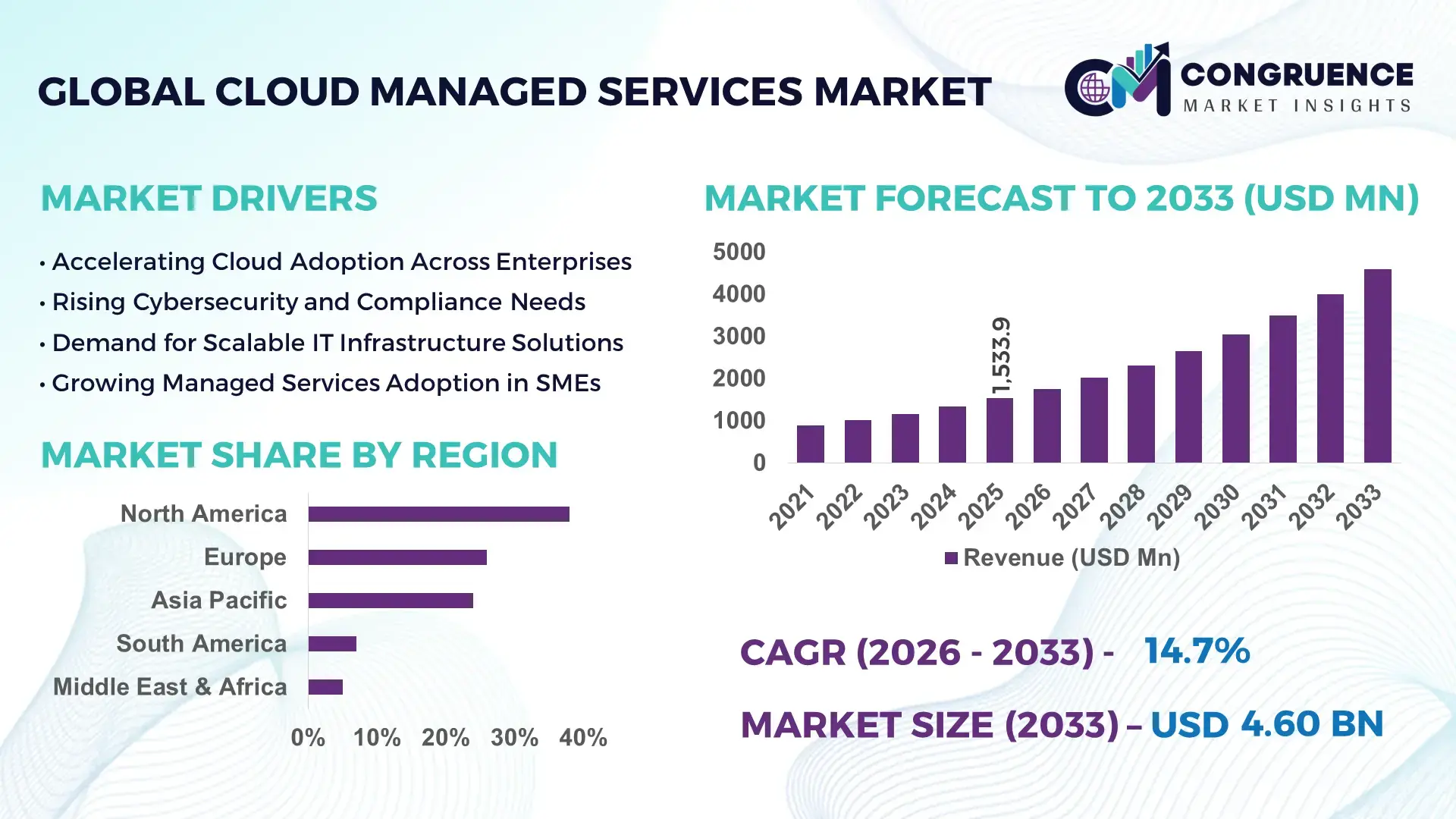

The Global Cloud Managed Services Market was valued at USD 1,553.9 Million in 2025 and is anticipated to reach a value of USD 4,595.2 Million by 2033 expanding at a CAGR of 14.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by accelerating enterprise cloud migration strategies, rising demand for hybrid IT management, and increasing cybersecurity complexities across digital infrastructures.

The United States represents the dominant country in the Cloud Managed Services Market, supported by its advanced hyperscale data center ecosystem and high enterprise cloud penetration. The country hosts over 2,700 data centers, accounting for more than 40% of global hyperscale infrastructure capacity. Enterprise cloud adoption exceeds 94% among large organizations, with over 65% operating in multi-cloud environments. Annual enterprise cloud spending in the U.S. surpassed USD 180 billion in 2025, with managed security, cloud optimization, and DevOps automation among the fastest-growing segments. Key industry applications include BFSI, healthcare, retail, and federal government modernization programs. AI-driven monitoring, automated incident response, and infrastructure-as-code adoption have improved operational efficiency by nearly 30% across major enterprises.

Market Size & Growth: Valued at USD 1,553.9 Million in 2025 and projected to reach USD 4,595.2 Million by 2033, expanding at 14.7% CAGR; growth is fueled by rapid hybrid cloud integration and cybersecurity outsourcing.

Top Growth Drivers: 72% enterprise multi-cloud adoption rate, 48% rise in managed security service demand, 35% IT cost optimization achieved through outsourced cloud management.

Short-Term Forecast: By 2028, automated cloud management platforms are expected to reduce operational overhead by 27% and improve workload performance efficiency by 22%.

Emerging Technologies: AI-driven observability platforms, Kubernetes-based orchestration, Zero Trust security frameworks, and Infrastructure-as-Code automation.

Regional Leaders: North America projected to reach USD 1,850 Million by 2033 driven by BFSI modernization; Europe to exceed USD 1,200 Million supported by GDPR-driven compliance outsourcing; Asia-Pacific to surpass USD 1,050 Million due to 60% SME cloud adoption acceleration.

Consumer/End-User Trends: BFSI contributes nearly 28% of managed cloud deployments, healthcare 18%, IT & telecom 24%, with 68% enterprises preferring bundled managed security services.

Pilot or Case Example: In 2024, a large U.S. healthcare network achieved 32% downtime reduction and 25% faster incident resolution using AI-enabled managed cloud monitoring.

Competitive Landscape: Accenture holds approximately 14% share, followed by IBM, Tata Consultancy Services, Capgemini, and Infosys.

Regulatory & ESG Impact: Data localization mandates and carbon neutrality goals have pushed 41% enterprises to adopt energy-efficient cloud optimization tools.

Investment & Funding Patterns: Over USD 22 billion invested globally in managed cloud infrastructure and automation platforms in 2024, with strong venture backing for AI-based operations startups.

Innovation & Future Outlook: Integration of AI Ops, edge-cloud management, and predictive analytics is expected to enhance uptime reliability beyond 99.99% service-level agreements.

Cloud Managed Services Market adoption is led by BFSI (28%), IT & telecom (24%), healthcare (18%), and retail (12%), reflecting diversified demand patterns. Recent innovations include AI-powered FinOps tools and automated compliance monitoring platforms. Regulatory drivers such as data protection frameworks and carbon-neutral IT commitments are shaping procurement strategies. North America and Asia-Pacific exhibit strong consumption growth, while hybrid-cloud orchestration and edge computing management are emerging as long-term transformation pillars for enterprise IT ecosystems.

The Cloud Managed Services Market holds strong strategic relevance as enterprises transition from capital-intensive IT infrastructures to agile, service-oriented digital ecosystems. Organizations are prioritizing cloud governance, cybersecurity resilience, and workload optimization to enhance operational continuity. AI-driven cloud monitoring delivers 35% faster anomaly detection compared to traditional rule-based IT management systems, while automated remediation tools reduce manual intervention by nearly 40%. These measurable efficiency gains position managed services as a critical enabler of enterprise-scale digital transformation.

North America dominates in deployment volume due to high enterprise IT spending, while Asia-Pacific leads in adoption growth rate, with nearly 62% of mid-sized enterprises accelerating managed multi-cloud strategies. BFSI and healthcare sectors are embedding managed services into regulatory compliance frameworks, ensuring data sovereignty and encryption standards alignment.

By 2028, AI-powered FinOps platforms are expected to reduce cloud overspending by 30% through predictive workload scaling and cost governance analytics. Firms are committing to ESG-linked IT improvements, including 25% reduction in data center energy consumption by 2030 through workload optimization and carbon-aware scheduling technologies.

In 2025, a leading U.S. financial institution achieved a 29% reduction in infrastructure downtime and 21% faster digital product deployment cycles after implementing AI-based managed cloud orchestration. As automation, compliance integration, and sustainability metrics converge, the Cloud Managed Services Market will remain a foundational pillar of resilience, regulatory alignment, and sustainable enterprise growth.

The Cloud Managed Services Market dynamics are shaped by rapid enterprise digitalization, increasing hybrid cloud complexity, and growing cybersecurity exposure. Over 70% of enterprises now operate across multiple cloud environments, creating demand for centralized monitoring, governance, and cost optimization services. Regulatory mandates such as data localization and sector-specific compliance standards have increased outsourcing of cloud security management. Additionally, rising edge deployments and IoT integrations are expanding workload distribution, necessitating advanced orchestration platforms. Automation, AI Ops, and predictive analytics are redefining service-level agreements, pushing uptime benchmarks beyond 99.9%. Competitive intensity remains high, with service providers differentiating through vertical specialization, bundled managed security offerings, and ESG-driven optimization capabilities.

Over 72% of enterprises globally operate in multi-cloud environments, managing workloads across at least two public or hybrid cloud platforms. This shift has increased operational complexity by nearly 45%, prompting demand for unified monitoring and governance frameworks. Managed service providers deliver centralized dashboards, automated scaling, and integrated security controls that reduce incident response times by up to 30%. Furthermore, 68% of IT leaders report improved cost visibility after adopting managed cloud optimization tools. The proliferation of SaaS applications and containerized workloads has also driven Kubernetes management outsourcing, particularly among BFSI and telecom enterprises handling high transaction volumes exceeding 10 million daily operations.

Data localization laws across more than 60 countries require enterprises to store sensitive information within national boundaries, increasing infrastructure fragmentation. Nearly 38% of multinational corporations report operational inefficiencies due to cross-border compliance restrictions. Additionally, regulatory audits have increased by 25% in heavily regulated sectors such as healthcare and finance, elevating compliance management costs. Integration challenges between legacy IT systems and modern cloud platforms further slow deployment cycles, with 42% of enterprises citing compatibility issues as a barrier. These regulatory and technical constraints complicate standardized service delivery models across regions.

AI-driven cloud automation platforms can reduce manual IT workload by nearly 40% and improve predictive fault detection accuracy to 85%. As enterprises deploy over 50% of workloads in containerized environments, automated orchestration and self-healing systems create new revenue streams for managed service providers. Edge computing expansion, projected to support 75% of enterprise data processing outside centralized data centers, also presents opportunities for distributed cloud management solutions. SMEs, accounting for 60% of new cloud migrations in Asia-Pacific, represent a rapidly expanding client base seeking bundled managed infrastructure and cybersecurity solutions.

Cyberattacks targeting cloud environments increased by 28% in the past year, with ransomware incidents impacting nearly 37% of medium-to-large enterprises. Advanced persistent threats require continuous monitoring and zero-trust architecture integration, raising operational costs for service providers. The shortage of certified cloud security professionals, estimated at over 3 million globally, further intensifies service delivery constraints. Additionally, managing hybrid infrastructures spanning on-premises and multi-cloud ecosystems increases configuration errors by up to 23%, exposing enterprises to compliance and performance risks. These challenges demand continuous innovation and workforce upskilling.

AI-Driven Operations Achieving 35% Faster Incident Resolution: Enterprises adopting AI Ops platforms report 35% faster anomaly detection and 28% lower unplanned downtime. Automated ticketing and root-cause analysis reduce mean time to resolution from 4.5 hours to under 3 hours in complex multi-cloud ecosystems.

Surge in Managed Security Integration with 48% Adoption Growth: Demand for bundled managed security services increased by 48% year-over-year, with 67% enterprises implementing zero-trust architectures. Multi-factor authentication deployments rose by 42%, strengthening compliance alignment.

Hybrid and Multi-Cloud Orchestration Expanding to 70% Enterprises: Over 70% of organizations manage workloads across hybrid infrastructures, driving 31% efficiency improvement through centralized governance dashboards and automated scaling frameworks.

ESG-Focused Cloud Optimization Reducing Energy Use by 25%: Enterprises integrating carbon-aware workload scheduling achieved up to 25% reduction in data center energy consumption. Nearly 41% of firms now include sustainability metrics in cloud procurement decisions, aligning IT modernization with environmental performance goals.

The Cloud Managed Services Market segmentation reflects diversified enterprise demand across service types, industry applications, and end-user categories. By type, organizations increasingly prioritize managed infrastructure, managed security, managed network, managed mobility, and managed communication services to address hybrid-cloud complexity. Managed infrastructure and security together account for more than 55% of deployments due to rising cyber threats and workload migration initiatives. By application, BFSI, IT & telecom, healthcare, retail, and manufacturing dominate adoption patterns, driven by compliance mandates and digital customer engagement strategies. Industry data indicates that over 70% of enterprises operating multi-cloud environments outsource at least one critical management function. From an end-user standpoint, large enterprises contribute the majority of adoption, but SMEs are rapidly expanding due to scalable subscription models and 60%+ cloud-first policies in emerging markets. This structured segmentation highlights how operational resilience, regulatory compliance, and automation efficiency shape procurement decisions across verticals.

The Cloud Managed Services Market by type includes Managed Infrastructure Services, Managed Security Services, Managed Network Services, Managed Mobility Services, and Managed Communication & Collaboration Services. Managed Infrastructure Services currently account for approximately 34% of total adoption, as enterprises migrate mission-critical workloads to hybrid and multi-cloud environments requiring 24/7 monitoring and automated orchestration. Managed Security Services follow with nearly 28% share, reflecting a 48% increase in enterprise cybersecurity outsourcing amid a 28% rise in cloud-targeted cyberattacks. However, Managed Security Services are the fastest-growing segment, expanding at an estimated 16.9% CAGR, driven by zero-trust implementation and regulatory audit requirements across more than 60 jurisdictions. Managed Network Services and Managed Communication Services together contribute around 26% of deployments, particularly in telecom and distributed enterprise ecosystems managing high-bandwidth data traffic. Managed Mobility Services remain niche but relevant, representing roughly 12% share, supporting remote workforce device management and endpoint security.

By application, BFSI leads the Cloud Managed Services Market with approximately 28% share, driven by high transaction volumes exceeding 10 million daily digital banking interactions and strict data encryption mandates. IT & Telecom accounts for nearly 24%, supported by 5G infrastructure expansion and edge workload orchestration. Healthcare holds around 18% share, reflecting increasing adoption of HIPAA-compliant managed hosting and AI-assisted monitoring platforms. While BFSI dominates, healthcare is the fastest-growing application segment, expanding at an estimated 17.4% CAGR due to digital patient record integration and telehealth infrastructure scaling. Retail and manufacturing collectively contribute approximately 20% share, leveraging managed services for omnichannel platforms and predictive maintenance systems. In 2025, more than 41% of global enterprises reported piloting AI-integrated Cloud Managed Services for customer experience optimization. Additionally, 58% of digital-native firms indicated improved SLA compliance after outsourcing cloud operations management.

Large enterprises represent the leading end-user segment in the Cloud Managed Services Market, accounting for approximately 64% of total adoption due to complex multi-cloud environments and higher IT budgets. Over 75% of Fortune 1000 companies outsource at least one cloud management function. SMEs hold about 36% share but are the fastest-growing segment, expanding at an estimated 18.2% CAGR, fueled by subscription-based pricing models and simplified managed infrastructure bundles. SMEs in Asia-Pacific report more than 60% cloud-first strategies, accelerating third-party management adoption. Industry-wise, BFSI enterprises account for nearly 28% of managed service consumption, IT & telecom 24%, healthcare 18%, and retail 12%, with remaining sectors collectively contributing 18%. In 2025, approximately 44% of mid-sized enterprises globally reported increased reliance on managed cloud providers for cybersecurity compliance. Furthermore, 62% of enterprises adopting hybrid cloud frameworks indicated improved operational resilience after outsourcing monitoring and automation functions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.9% between 2026 and 2033.

North America’s leadership is supported by over 2,700 operational data centers and enterprise cloud penetration exceeding 90%, with nearly 70% of large organizations running multi-cloud strategies. Europe holds approximately 26% share, driven by stringent data protection frameworks and more than 65% enterprise hybrid-cloud integration. Asia-Pacific accounts for nearly 24% of total demand, fueled by 60%+ SME cloud-first policies across India and Southeast Asia. South America contributes around 7%, with Brazil representing over 45% of regional consumption. The Middle East & Africa region captures close to 5% share, supported by national digital transformation programs in the UAE and Saudi Arabia. Globally, more than 72% of enterprises outsource at least one cloud management function, and over 41% prioritize managed security services, reflecting regionally diverse yet technology-driven growth dynamics.

North America holds approximately 38% of the global Cloud Managed Services Market share, supported by strong enterprise IT spending and advanced digital infrastructure. The BFSI sector contributes nearly 30% of regional demand, followed by healthcare at 22% and IT & telecom at 25%. Regulatory frameworks such as data privacy mandates and federal cybersecurity modernization programs have pushed over 68% of enterprises to integrate managed security and compliance monitoring tools. Technological advancements include AI-driven IT operations, container orchestration platforms, and zero-trust network implementations, with 74% of enterprises deploying hybrid cloud governance models. Accenture, a major regional player, has expanded AI-powered cloud management centers across multiple U.S. cities, enhancing automated monitoring capabilities for Fortune 500 clients. Consumer behavior reflects high enterprise adoption in healthcare and finance, where more than 80% of large institutions rely on third-party managed cloud partners for mission-critical operations.

Europe accounts for approximately 26% of the global Cloud Managed Services Market share, with Germany, the United Kingdom, and France collectively contributing over 60% of regional demand. Regulatory bodies enforcing GDPR compliance have led to 71% of enterprises adopting managed cloud security and data governance services. Sustainability initiatives targeting 55% carbon reduction by 2030 have further accelerated demand for energy-optimized cloud management platforms. Over 63% of European enterprises utilize hybrid-cloud environments, and AI-based workload optimization adoption has grown by 34% in the past two years. Capgemini, headquartered in France, has expanded sovereign cloud and managed cybersecurity solutions across EU markets to address localization requirements. Regional consumer behavior reflects regulatory-driven procurement, where nearly 69% of enterprises prioritize explainable AI monitoring and transparent compliance reporting in managed cloud contracts.

Asia-Pacific represents roughly 24% of the global Cloud Managed Services Market and ranks second in total deployment volume. China, India, and Japan account for over 65% of regional consumption, with India reporting more than 60% SME cloud-first adoption. Infrastructure expansion includes over 500 new hyperscale data center projects announced across the region in recent years. Manufacturing, e-commerce, and fintech sectors are key demand generators, collectively contributing more than 50% of managed service utilization. Tata Consultancy Services has strengthened regional capabilities by deploying AI-enabled cloud monitoring hubs supporting over 1,000 enterprise clients. Regional behavior indicates strong growth driven by e-commerce platforms and mobile-based enterprise applications, with 58% of mid-sized firms outsourcing infrastructure management to reduce operational complexity and improve uptime beyond 99.9%.

South America contributes approximately 7% of the global Cloud Managed Services Market, with Brazil accounting for nearly 45% of regional demand, followed by Argentina and Chile. Financial services and media industries collectively represent over 40% of managed cloud utilization. Government-backed digital banking initiatives and tax incentives for technology modernization have encouraged 52% of enterprises to shift toward hybrid-cloud models. Regional infrastructure investments include expanded fiber connectivity and data center projects supporting cross-border digital services. A leading Brazilian IT services provider has implemented managed security platforms for over 200 financial institutions, improving cyber incident response times by 27%. Consumer behavior reflects demand tied to media streaming, fintech applications, and language-localized platforms, particularly among urban enterprises seeking scalable IT operations.

The Middle East & Africa region holds close to 5% of the global Cloud Managed Services Market share, with the UAE, Saudi Arabia, and South Africa leading adoption. Oil & gas, government services, and construction sectors contribute nearly 48% of regional demand. National transformation programs such as Vision 2030 initiatives have accelerated cloud adoption across public-sector entities, with over 55% of government departments deploying managed cloud solutions. Technological modernization includes smart city deployments and AI-based infrastructure monitoring platforms. A UAE-based technology firm recently launched a sovereign managed cloud platform supporting over 300 enterprise clients with localized data hosting. Regional consumer behavior reflects growing demand for secure, locally hosted cloud environments, particularly among government-backed infrastructure and energy enterprises prioritizing data sovereignty and cybersecurity compliance.

United States – 34% Market Share: It leads due to high enterprise cloud penetration, extensive hyperscale infrastructure, and strong BFSI and healthcare demand.

Germany – 9% Market Share: It is driven by industrial digitalization, strict data protection regulations, and strong adoption of hybrid-cloud governance across manufacturing and automotive sectors.

The Cloud Managed Services Market exhibits a moderately fragmented structure, with more than 150 active global and regional service providers competing across infrastructure management, cybersecurity, DevOps automation, and hybrid-cloud orchestration. The top five companies collectively account for approximately 46% of the global market share, indicating strong brand consolidation among tier-one IT service providers, while mid-sized and niche firms compete through vertical specialization and regional customization.

Large multinational players focus on integrated end-to-end cloud lifecycle management, combining advisory, migration, optimization, and managed security services under unified service-level agreements exceeding 99.99% uptime benchmarks. Over 60% of leading vendors have expanded AI-driven operations (AIOps) capabilities since 2023, embedding predictive analytics and automated remediation tools to reduce incident response times by 30–40%. Strategic initiatives include hyperscaler partnerships, sovereign cloud launches, and acquisitions targeting cybersecurity and FinOps startups. In the past two years, more than 25 strategic acquisitions have been completed globally to strengthen managed detection and response (MDR) capabilities.

Competitive differentiation increasingly centers on zero-trust frameworks, carbon-aware workload optimization, and industry-specific compliance modules. Approximately 58% of enterprise contracts now include bundled managed security components, intensifying rivalry in high-value verticals such as BFSI and healthcare. Pricing models are evolving toward outcome-based and consumption-aligned contracts, reflecting growing enterprise demand for cost transparency and performance accountability.

Capgemini

Infosys

Wipro

HCLTech

Cognizant

NTT DATA

DXC Technology

Fujitsu

Atos

Rackspace Technology

Tech Mahindra

Unisys

Kyndryl

The Cloud Managed Services Market is being reshaped by rapid advancements in AI-driven automation, container orchestration, edge-cloud integration, and zero-trust cybersecurity architectures. AI Ops platforms now analyze over 500 million events per day in large enterprise environments, reducing false-positive alerts by nearly 35% and cutting mean time to resolution by up to 40%. Machine learning–based predictive analytics models are capable of identifying infrastructure anomalies with accuracy rates exceeding 85%, improving workload stability and SLA adherence.

Containerization technologies such as Kubernetes are deployed in over 60% of enterprise cloud-native applications, prompting demand for managed orchestration services capable of handling auto-scaling, policy enforcement, and multi-cluster governance. Infrastructure-as-Code (IaC) tools have reduced manual configuration efforts by 30%, accelerating deployment cycles from weeks to days.

Edge computing integration is another transformative trend, with nearly 50% of enterprise data expected to be processed outside centralized data centers. Managed service providers are investing in distributed monitoring frameworks that maintain 99.9%+ uptime across hybrid and edge deployments.

Cybersecurity innovation remains critical, as 67% of enterprises are implementing zero-trust architectures supported by continuous identity verification and encryption key lifecycle management. Additionally, carbon-aware scheduling algorithms are enabling organizations to lower data center energy consumption by up to 25%, aligning operational performance with ESG targets.

• In October 2025, Bharti Airtel entered a strategic partnership with International Business Machines (IBM) to bolster its Airtel Cloud platform by integrating IBM’s AI-ready infrastructure and hybrid cloud solutions, enabling regulated industries like banking, healthcare, and government to scale AI workloads more efficiently across multi-cloud and edge environments. This initiative expands cloud service resilience and compliance for enterprise customers. Source: www.ibm.com

• In October 2025, IBM announced a strategic partnership with Anthropic to integrate Claude LLM models into IBM’s enterprise software portfolio, enhancing AI governance, security, and productivity within hybrid cloud deployments. The collaboration aims to accelerate development of secure, enterprise-ready AI applications embedded within cloud services. Source: www.ibm.com

• In August 2025, Capgemini signed an agreement to acquire Cloud4C, a hybrid cloud and sovereign cloud managed services provider, strengthening its automation-driven platform capabilities and expanding its AI-ready operations and compliance frameworks across global client portfolios. This strategic acquisition enhances Capgemini’s cloud migration and end-to-end management offerings. Source: www.capgemini.com

• In April 2025, Accenture expanded its collaboration with Amazon Web Services (AWS) to accelerate AI-powered cloud modernization in the public sector, defense, and national security organizations, enhancing cloud transformation capabilities with AWS technologies and driving broader adoption of cloud-native innovation frameworks. Source: www.newsroom.accenture.com

The Cloud Managed Services Market Report provides a comprehensive evaluation of service types, deployment models, enterprise sizes, and vertical-specific adoption patterns across five major regions and over 20 key countries. The scope covers managed infrastructure, managed security, managed network, managed mobility, and managed communication services, representing more than 90% of outsourced cloud management demand globally.

The report analyzes applications across BFSI (28%), IT & telecom (24%), healthcare (18%), retail (12%), manufacturing, government, and energy sectors, highlighting operational, compliance, and automation-driven use cases. It further examines enterprise segmentation, where large enterprises contribute 64% of demand while SMEs account for 36%, with strong uptake in emerging economies.

Technological coverage includes AI Ops, Kubernetes orchestration, Infrastructure-as-Code frameworks, zero-trust security, edge-cloud management, and ESG-driven workload optimization tools. The geographic scope spans North America (38% share), Europe (26%), Asia-Pacific (24%), South America (7%), and Middle East & Africa (5%), detailing infrastructure density, digital transformation maturity, and sector-specific adoption trends.

Additionally, the report addresses competitive benchmarking across more than 150 active vendors, assessing service capabilities, innovation pipelines, and partnership ecosystems. Emerging niches such as sovereign cloud, FinOps management, and carbon-aware cloud scheduling are incorporated to provide forward-looking strategic insight for technology investors, service providers, and enterprise decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,553.9 Million |

| Market Revenue (2033) | USD 4,595.2 Million |

| CAGR (2026–2033) | 14.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Accenture; IBM; Tata Consultancy Services (TCS); Capgemini; Infosys; Wipro; HCLTech; Cognizant; NTT DATA; DXC Technology; Fujitsu; Atos; Rackspace Technology; Tech Mahindra; Unisys; Kyndryl |

| Customization & Pricing | Available on Request (10% Customization Free) |