Reports

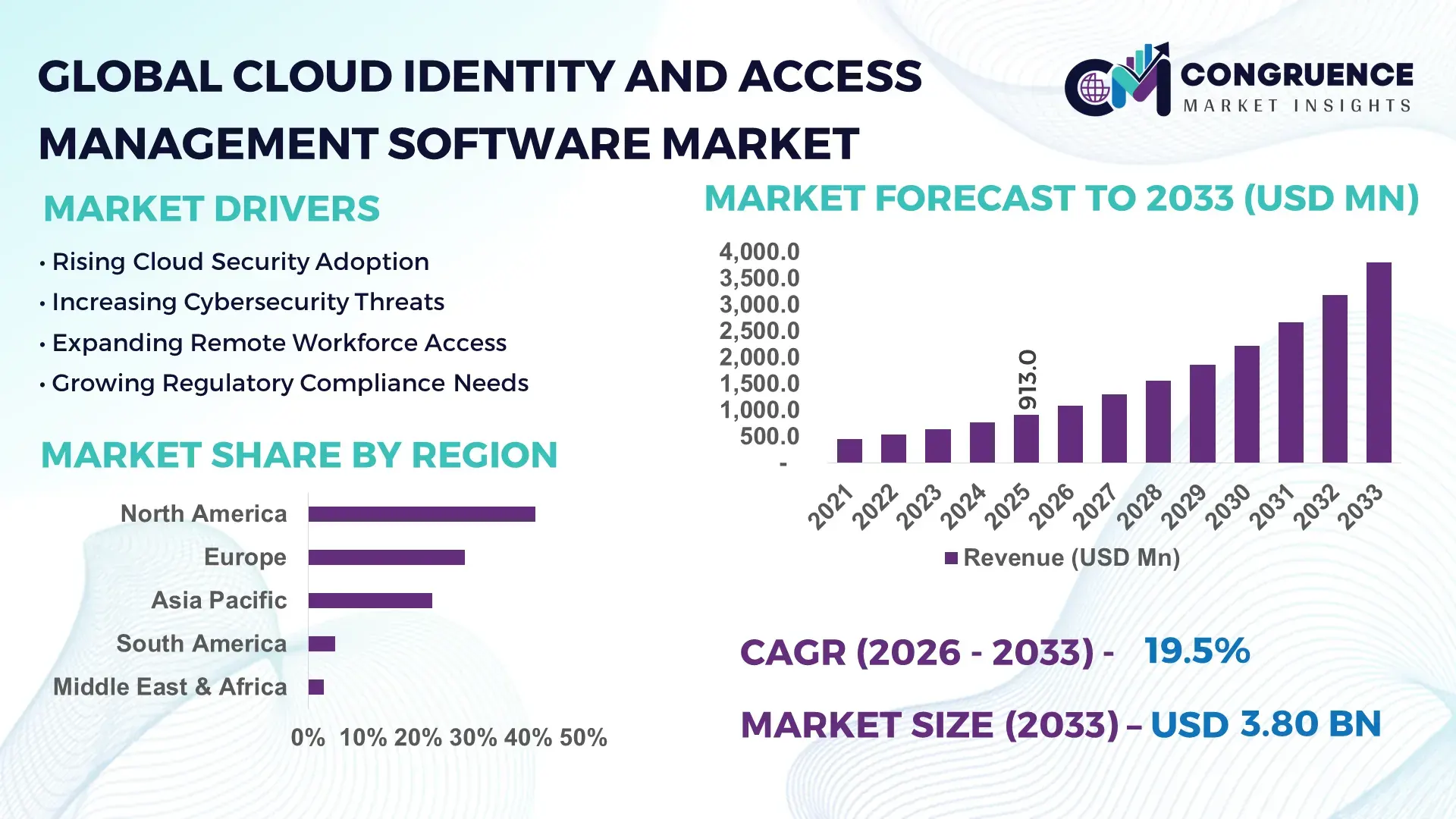

The Global Cloud Identity and Access Management Software Market was valued at USD 913.0 Million in 2025 and is anticipated to reach a value of USD 3,801.9 Million by 2033 expanding at a CAGR of 19.52% between 2026 and 2033. The market is accelerating as enterprises rapidly deploy passwordless authentication, Zero Trust security architectures, and AI-enabled identity governance to comply with evolving cybersecurity regulations and secure hybrid cloud environments.

The United States dominates the global Cloud Identity and Access Management Software Market with approximately 38% market share, supported by over 70% enterprise cloud adoption, multi-billion-dollar cybersecurity investments, and strong deployment across BFSI, healthcare, government, and technology sectors. Compared with Germany, where enterprise cloud adoption exceeds 52%, U.S. organizations lead in Zero Trust implementation following federal cybersecurity initiatives and Executive Order 14028, reinforcing large-scale identity modernization.

Organizations prioritizing AI-driven identity orchestration, regulatory compliance, and scalable cloud-native security platforms will secure stronger operational resilience and long-term competitive differentiation.

Market Size & Growth: USD 913.0 Million (2025) to USD 3,801.9 Million (2033) at 19.52%, driven by Zero Trust adoption.

Top Growth Drivers: Zero Trust (+48%), hybrid workforce (+42%), AI identity analytics (+35%).

Short-Term Forecast: By 2028, authentication costs decline 28% through cloud automation.

Emerging Technologies: AI identity analytics, passwordless authentication, and machine identity management reshape security.

Regional Leaders: North America (~USD 1.55B), Europe (~USD 0.98B), Asia-Pacific (~USD 0.87B) accelerate cloud deployment.

Consumer/End-User Trends: More than 68% of enterprises prioritize cloud-native IAM over legacy systems.

Pilot/Case Example: 2024 enterprise Zero Trust rollout reduced unauthorized access incidents by 45%.

Competitive Landscape: Microsoft leads with ~17% share alongside Okta, IBM, CyberArk, and Ping Identity.

Regulatory & ESG Impact: Identity automation reduces manual provisioning effort by nearly 40%, supporting compliance.

Investment & Funding: Over USD 6 billion invested globally in cybersecurity identity platforms and strategic partnerships.

Innovation & Future Outlook: AI copilots, decentralized identity, and machine identity security define the next competitive phase.

Cloud Identity and Access Management Software continues expanding across financial services, healthcare, manufacturing, and public-sector digital infrastructure as organizations strengthen identity-centric cybersecurity. AI-powered identity governance and passwordless authentication now improve access decision accuracy by nearly 35%, while stricter regulations and resilient cloud infrastructure strategies accelerate deployment. Machine identity management is emerging as the next major investment priority, setting the foundation for broader strategic transformation.

Cloud Identity and Access Management Software has become a strategic technology foundation as organizations modernize digital infrastructure, secure distributed workforces, and strengthen cyber resilience. Intensifying ransomware activity, expanding multi-cloud environments, and stricter regulations such as the NIS2 Directive and U.S. federal Zero Trust initiatives are reshaping enterprise security investment priorities. Identity security now directly influences business continuity, regulatory compliance, and competitive positioning.

Modern cloud-native IAM platforms automate identity lifecycle management and policy enforcement, reducing administrative effort by nearly 40% compared with legacy on-premises identity systems while improving provisioning speed by over 50%. North America continues leading enterprise-scale deployments through mature cloud ecosystems, whereas Asia-Pacific records faster implementation across financial services, telecommunications, and digital government programs supported by accelerating cloud adoption and infrastructure modernization.

Organizations increasingly deploy AI-enabled identity governance alongside privileged access management to secure employees, customers, and machine identities from a unified platform. Leading vendors are expanding strategic partnerships with cloud providers, cybersecurity firms, and system integrators to accelerate deployment and improve interoperability. Over the next two to three years, enterprises prioritizing automated identity intelligence, passwordless authentication, and scalable Zero Trust architectures will strengthen operational resilience, reduce security complexity, and establish durable competitive advantage in an increasingly digital business environment.

Enterprise migration toward Zero Trust security frameworks and cloud-native identity governance is fundamentally reshaping Cloud Identity and Access Management Software adoption. More than 70% of large enterprises now operate hybrid or multi-cloud environments, while over 65% of organizations prioritize identity as the primary security control for digital assets. In the United States, Executive Order 14028 continues driving federal Zero Trust implementation, accelerating commercial adoption across regulated industries. This structural shift reduces identity-related attack surfaces while strengthening compliance and operational resilience. Vendors are responding through AI-powered identity analytics, strategic cloud partnerships, and expansion of passwordless authentication portfolios. A notable operational advantage is the growing convergence of workforce and machine identity management, enabling unified policy enforcement and lower administrative complexity across distributed enterprise ecosystems.

Integration complexity with legacy identity systems remains a significant structural restraint for enterprise-scale deployments. Nearly 58% of organizations continue operating hybrid identity infrastructures, while approximately 45% report interoperability challenges between cloud IAM platforms and legacy enterprise applications. Germany's manufacturing sector illustrates this constraint, where long-established operational technology environments require extensive customization before cloud identity integration. These limitations increase deployment timelines, implementation costs, and governance complexity, particularly for highly regulated industries. Organizations are mitigating operational risks by adopting phased migration strategies, API-first identity architectures, regional cloud hosting, and long-term technology partnerships with system integrators. Companies emphasizing standardized identity frameworks and modular deployment models are achieving faster modernization while minimizing disruption to mission-critical business operations.

Rapid growth in connected devices, AI workloads, and automated infrastructure is creating substantial opportunities beyond traditional workforce identity management. Machine identities now outnumber human identities by more than 40:1, while approximately 60% of enterprises are increasing investment in automated identity governance. Singapore's Smart Nation initiatives and expanding digital public infrastructure demonstrate how decentralized identity ecosystems are gaining strategic importance. Organizations are investing in verifiable credentials, AI-driven identity lifecycle automation, and identity orchestration platforms to improve operational efficiency and reduce manual administration. Technology vendors are accelerating innovation through cloud alliances, developer ecosystems, and R&D focused on machine identity security. The strongest competitive advantage increasingly lies in securing non-human identities across rapidly expanding cloud-native environments.

Maintaining consistent identity governance across multi-cloud, SaaS, on-premises, and edge environments remains the industry's most demanding execution challenge. Around 75% of enterprises now operate multiple cloud platforms, while over 50% report shortages of skilled cybersecurity professionals capable of managing advanced identity ecosystems. Japan's expanding digital transformation initiatives highlight the operational pressure of integrating thousands of applications under unified identity policies without disrupting business continuity. Inconsistent access governance increases cyber risk, audit complexity, and operational overhead. Companies are addressing these challenges through AI-assisted policy automation, continuous identity verification, workforce upskilling, and strategic cybersecurity partnerships. Organizations that establish centralized identity governance with automated policy enforcement will strengthen long-term operational resilience and sustainable competitive positioning.

AI-Driven Identity Intelligence Enterprises are embedding AI into identity governance to automate anomaly detection, access certification, and risk-based authentication. More than 62% of large organizations now utilize AI-assisted identity analytics, while automated access reviews reduce administrative workloads by nearly 35%. Following stricter cyber regulations in the United States and Europe, vendors are expanding AI capabilities through acquisitions, cloud partnerships, and integrated security platforms, improving response speed and operational consistency.

Passwordless Authentication Expansion Passwordless authentication is rapidly replacing traditional credentials across enterprise environments. Nearly 58% of organizations have implemented or are deploying passwordless login methods, while phishing-related credential attacks decline by approximately 50% after deployment. Companies are scaling biometric authentication, FIDO2 standards, and hardware security keys to strengthen workforce security, reduce helpdesk costs, and streamline user onboarding across hybrid workplaces.

Machine Identity Management Growth Automated infrastructure, APIs, and connected workloads are accelerating demand for machine identity governance. Machine identities now exceed human identities by over 40:1, and nearly 55% of enterprises are centralizing certificate lifecycle management. Organizations are restructuring identity operations through automation platforms and cloud-native certificate management, improving application availability while minimizing security gaps across distributed digital ecosystems.

Integrated Security Platform Adoption Enterprises increasingly consolidate IAM with endpoint security, SIEM, and cloud security platforms to simplify operations. More than 60% of cybersecurity buyers now prefer integrated security ecosystems, reducing security management complexity by nearly 30%. Growing software supply-chain risks and evolving compliance obligations encourage strategic technology alliances, enabling vendors to deliver unified identity protection with faster deployment and lower operational overhead.

Cloud-Based solutions represent the leading segment, accounting for approximately 68% of deployments due to superior scalability, centralized administration, and seamless integration with SaaS applications, hybrid cloud environments, and Zero Trust architectures. Organizations increasingly prefer subscription-based cloud IAM to reduce infrastructure maintenance while enabling continuous security updates and rapid policy enforcement. Cloud-native platforms also accelerate onboarding and identity lifecycle management across distributed workforces. Vendors continue strengthening this segment through AI-powered identity analytics, strategic cloud partnerships, and broader passwordless authentication capabilities. Hybrid deployment is the fastest-growing segment as enterprises balance regulatory compliance with cloud modernization initiatives. Nearly 24% of large organizations continue operating mixed identity infrastructures requiring hybrid deployment models, particularly across financial institutions and government agencies. On-Premises solutions remain strategically important for organizations managing highly sensitive workloads, although modernization investments increasingly focus on cloud integration rather than infrastructure expansion. Vendors are prioritizing interoperability, API-based architecture, and migration services to support phased digital transformation while protecting existing enterprise investments.

User Authentication remains the dominant application, representing approximately 34% of enterprise deployments because every digital access request depends on secure identity verification. Organizations continue strengthening authentication through biometrics, passwordless login, adaptive access policies, and behavioral analytics to improve both security and user experience. Multi-Factor Authentication maintains widespread deployment across regulated sectors, while Single Sign-On improves workforce productivity by reducing authentication friction across multiple enterprise applications. Vendors continue integrating AI-based risk assessment to strengthen authentication accuracy and reduce credential compromise. Identity Governance & Administration is the fastest-growing application as enterprises automate identity lifecycle management, compliance reporting, and access certification. Nearly 61% of large enterprises now prioritize automated identity governance to reduce manual administrative effort and improve audit readiness. Privileged Access Management is also gaining strategic importance as organizations secure administrator accounts and machine identities supporting critical infrastructure. Technology providers are expanding unified identity platforms that combine authentication, governance, privileged access, and access analytics into integrated cloud security ecosystems.

BFSI represents the largest end-user segment, contributing nearly 29% of enterprise demand as financial institutions require continuous identity verification, fraud prevention, privileged access control, and regulatory compliance. Banks increasingly deploy AI-enabled authentication, behavioral analytics, and adaptive access policies to protect digital banking platforms while improving customer experience. Government and IT & Telecommunications organizations also maintain strong deployment levels due to national cybersecurity strategies, digital identity modernization, and large-scale cloud infrastructure investments supporting critical public and enterprise services. Healthcare is the fastest-growing end-user segment as hospitals and healthcare providers accelerate electronic health record protection and secure clinician access across connected care environments. Approximately 66% of healthcare organizations are expanding identity modernization programs to strengthen compliance and reduce ransomware exposure. Retail & E-commerce continues increasing investment to secure customer identities during omnichannel transactions, while Manufacturing strengthens machine identity management for connected industrial environments. Vendors are responding through industry-specific security frameworks, strategic cloud partnerships, and customized deployment models tailored to sector-specific compliance requirements.

North America accounted for the largest market share at 41.3% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.1% between 2026 and 2033.

North America remains the leading Cloud Identity and Access Management Software market, contributing approximately 41.3% of global demand in 2025 through advanced cloud infrastructure, mature cybersecurity ecosystems, and widespread enterprise digital transformation. Large-scale adoption across BFSI, healthcare, government, and technology sectors continues to strengthen regional leadership. More than 72% of large enterprises operate hybrid or multi-cloud environments, driving sustained investment in identity governance and passwordless authentication. Federal Zero Trust mandates in the United States continue accelerating enterprise deployment, while strategic alliances between cloud providers and cybersecurity vendors improve platform interoperability, AI-driven threat detection, and identity lifecycle automation across complex enterprise environments.

United States Market Outlook: The United States leads regional deployment through its concentration of global cloud providers, cybersecurity innovators, and highly regulated enterprise industries. More than 75% of Fortune 500 organizations have adopted advanced identity governance or Zero Trust initiatives, while continuous investment in AI-enabled cybersecurity platforms strengthens operational resilience. Federal modernization programs, strong cloud infrastructure, and expanding enterprise SaaS adoption continue encouraging organizations to replace legacy identity systems with cloud-native identity platforms supporting workforce, customer, and machine identities.

Europe maintains a strong market position through strict cybersecurity regulations, advanced enterprise digitization, and growing investment in secure cloud infrastructure. The region accounts for nearly 28.4% of global adoption, supported by financial services, manufacturing, healthcare, and public-sector modernization. More than 60% of large enterprises are integrating identity governance with cloud security strategies to comply with GDPR and NIS2 requirements. Vendors continue expanding regional cloud infrastructure, localized identity services, and compliance-focused security capabilities while strengthening partnerships with European system integrators to simplify enterprise deployment and regulatory reporting.

Germany Market Outlook: Germany serves as Europe's leading enterprise identity market through its advanced manufacturing sector, digital industrial infrastructure, and stringent cybersecurity compliance requirements. Approximately 58% of medium and large enterprises have accelerated cloud security modernization initiatives, integrating IAM with Industry 4.0 environments and critical manufacturing systems. Strong domestic technology investment and enterprise demand for secure hybrid-cloud operations continue positioning Germany as a strategic innovation hub for identity governance and industrial cybersecurity.

Asia-Pacific is the fastest-expanding regional market as governments and enterprises accelerate digital transformation, cloud migration, and national cybersecurity programs. The region contributes approximately 22.6% of global market activity, supported by expanding hyperscale data centers, digital banking, and e-government initiatives. Enterprise cloud adoption exceeds 65% across several developed Asia-Pacific economies, while investments in AI-powered cybersecurity and identity orchestration continue increasing. Technology vendors are expanding regional cloud availability, local partnerships, and managed security services to address rapidly growing enterprise demand across both developed and emerging digital economies.

China Market Outlook: China leads regional deployment through its extensive cloud infrastructure, expanding enterprise digitization, and strong domestic cybersecurity ecosystem. More than 70% of large digital enterprises have integrated cloud identity management into broader cloud security strategies, particularly across financial services, telecommunications, and e-commerce. Government-supported digital infrastructure programs and continuous investment in domestic cloud platforms continue strengthening enterprise identity modernization and large-scale cloud security deployment.

South America continues strengthening Cloud Identity and Access Management Software adoption as organizations modernize IT infrastructure and expand cloud-based business operations. The region represents approximately 4.9% of global demand, with financial institutions, telecommunications providers, and retail organizations driving implementation. Enterprise cloud migration has surpassed 48% among large organizations in several leading economies, increasing demand for centralized identity governance and privileged access management. Technology providers are expanding regional partnerships, managed security offerings, and cloud integration capabilities while addressing infrastructure disparities and cybersecurity skill shortages that influence deployment speed.

Brazil Market Outlook: Brazil remains the region's largest market due to its expanding financial technology ecosystem, large enterprise base, and accelerating cloud adoption. National data protection regulations continue encouraging organizations to strengthen identity governance and access controls. More than 55% of enterprise cybersecurity investment now supports cloud security modernization initiatives, prompting global IAM providers to expand local partnerships, cloud hosting capabilities, and managed identity services throughout the country.

The Middle East & Africa market is advancing through government-led digital transformation, cloud infrastructure expansion, and increasing investment in cybersecurity modernization. The region contributes roughly 2.8% of global demand, with financial services, energy, telecommunications, and public-sector organizations leading adoption. More than 50% of enterprise cloud modernization projects now include identity governance as a core security component. Cloud vendors and cybersecurity providers continue establishing regional data centers, technology alliances, and managed security operations to improve deployment capabilities while supporting national digital economy initiatives.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market development through advanced smart government initiatives, expanding hyperscale cloud infrastructure, and strong cybersecurity investment. Approximately 65% of government digital transformation projects incorporate advanced identity management capabilities to secure citizen services and critical infrastructure. Strategic partnerships between international cloud providers and domestic technology organizations continue accelerating enterprise deployment while positioning the UAE as a regional cybersecurity and cloud innovation hub.

Cloud Identity and Access Management Software competition is led by Microsoft, Okta, CyberArk, Ping Identity, and SailPoint, collectively controlling approximately 58% of the global market. Microsoft and Okta compete aggressively in workforce identity, while CyberArk and BeyondTrust dominate privileged access security. Ping Identity and SailPoint differentiate through enterprise federation and identity governance, challenging cloud-native innovators with deep integration capabilities. Competition centers on AI-driven identity analytics, Zero Trust architectures, and deployment speed, with automated identity workflows reducing administrative effort by nearly 40% and passwordless authentication lowering credential-based attacks by approximately 50%. Vendors strengthen positions through acquisitions, cloud partnerships, platform consolidation, and AI-powered identity orchestration rather than price competition alone. Identity security consolidation is accelerating as customers demand unified platforms instead of standalone tools. The primary entry barrier is enterprise-scale interoperability with complex legacy environments and regulatory compliance. Winning requires AI-enabled automation, seamless multi-cloud integration, rapid deployment, and comprehensive identity security spanning workforce, customer, and machine identities.

Okta

CyberArk

Ping Identity

SailPoint

IBM

Oracle

One Identity

BeyondTrust

Delinea

Saviynt

ForgeRock

JumpCloud

RSA Security

Cloud Identity and Access Management Software is rapidly evolving through AI-driven identity analytics, passwordless authentication, and machine identity security. More than 65% of large enterprises now deploy AI-assisted access governance to automate anomaly detection and identity lifecycle management, reducing manual administration by nearly 35%. Passwordless authentication based on FIDO2 and biometrics is replacing traditional credentials, cutting phishing-related compromise by approximately 50% while improving user productivity. Organizations integrating identity intelligence with Zero Trust security gain stronger operational resilience and faster incident response.

Traditional rule-based identity management is increasingly replaced by adaptive risk-based authentication and behavioral analytics. Compared with legacy identity platforms, AI-enabled cloud-native IAM improves access decision speed by nearly 45% while reducing provisioning delays by over 40%. Workforce identity, customer identity, and machine identity are converging into unified platforms, benefiting global enterprises managing hybrid cloud environments. Technology leaders such as Microsoft, Okta, CyberArk, and SailPoint continue expanding integrated identity ecosystems through AI innovation and strategic cloud partnerships.

Between 2026 and 2028, decentralized identity, verifiable credentials, and machine identity governance will reshape enterprise security architectures. More than 60% of digital transformation programs are expected to integrate identity orchestration with cloud security platforms, enabling automated compliance, stronger API protection, and scalable Zero Trust deployment. Organizations investing early in unified identity intelligence will gain measurable operational efficiency, lower cyber risk, and stronger competitive differentiation as AI-driven identities become standard across enterprise ecosystems.

February 2025 – CyberArk acquired Zilla Security to strengthen Identity Governance and Administration capabilities within its Identity Security Platform. The acquisition expanded governance automation and accelerated unified identity lifecycle management for enterprise customers. Measurable data: Integration adds modern cloud-native IGA capabilities to CyberArk's platform. Business impact: Strengthens end-to-end identity security portfolio. Source: www.cyberark.com

April 2025 – CyberArk introduced its Machine Identity Security platform to protect machine workloads across cloud, hybrid, and on-premises environments. Measurable data: Company research accompanying the launch highlighted machine identities growing substantially faster than human identities. Business impact: Expands enterprise protection for AI workloads and cloud-native applications.

November 2025 – Microsoft announced continued expansion of Microsoft Entra capabilities, including modernization of hybrid identity synchronization through cloud-native synchronization technologies. Measurable data: Migration targets enterprise-scale hybrid identity deployments while reducing on-premises management complexity. Business impact: Accelerates Zero Trust modernization across Microsoft customers.

January 2026 – Okta announced plans to expand its India engineering workforce by 50% to accelerate AI-driven identity security development. Measurable data: Workforce expansion of 50% supports deep technology and product engineering. Business impact: Strengthens global AI innovation capacity and product development.

This report provides comprehensive analysis of the Cloud Identity and Access Management Software Market across Cloud-Based, Hybrid, and On-Premises deployment models, covering applications including User Authentication, Identity Governance & Administration, Privileged Access Management, Single Sign-On, and Multi-Factor Authentication. It evaluates demand across BFSI, Healthcare, Government, IT & Telecommunications, Retail & E-commerce, Manufacturing, and other enterprise sectors. The study assesses market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, enterprise adoption patterns, and regional technology priorities.

The report examines competitive positioning of leading technology providers, emerging cloud-native innovators, and enterprise security specialists while analyzing AI-powered identity analytics, passwordless authentication, Zero Trust architectures, decentralized identity, and machine identity management. More than 65% enterprise cloud adoption and increasing identity-centric cybersecurity investments demonstrate accelerating digital transformation. Strategic insights support product development, investment planning, partnership evaluation, expansion strategies, competitive benchmarking, and long-term decision-making across evolving identity security ecosystems between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 913.0 Million |

| Market Revenue (2033) | USD 3,801.9 Million |

| CAGR (2026–2033) | 19.52% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft Corporation; Okta, Inc.; CyberArk Software Ltd.; Ping Identity Holding Corp.; SailPoint Technologies Holdings, Inc.; IBM Corporation; Oracle Corporation; One Identity LLC; BeyondTrust Corporation; Delinea Inc.; Saviynt Inc.; ForgeRock, Inc.; JumpCloud Inc.; RSA Security LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |