Reports

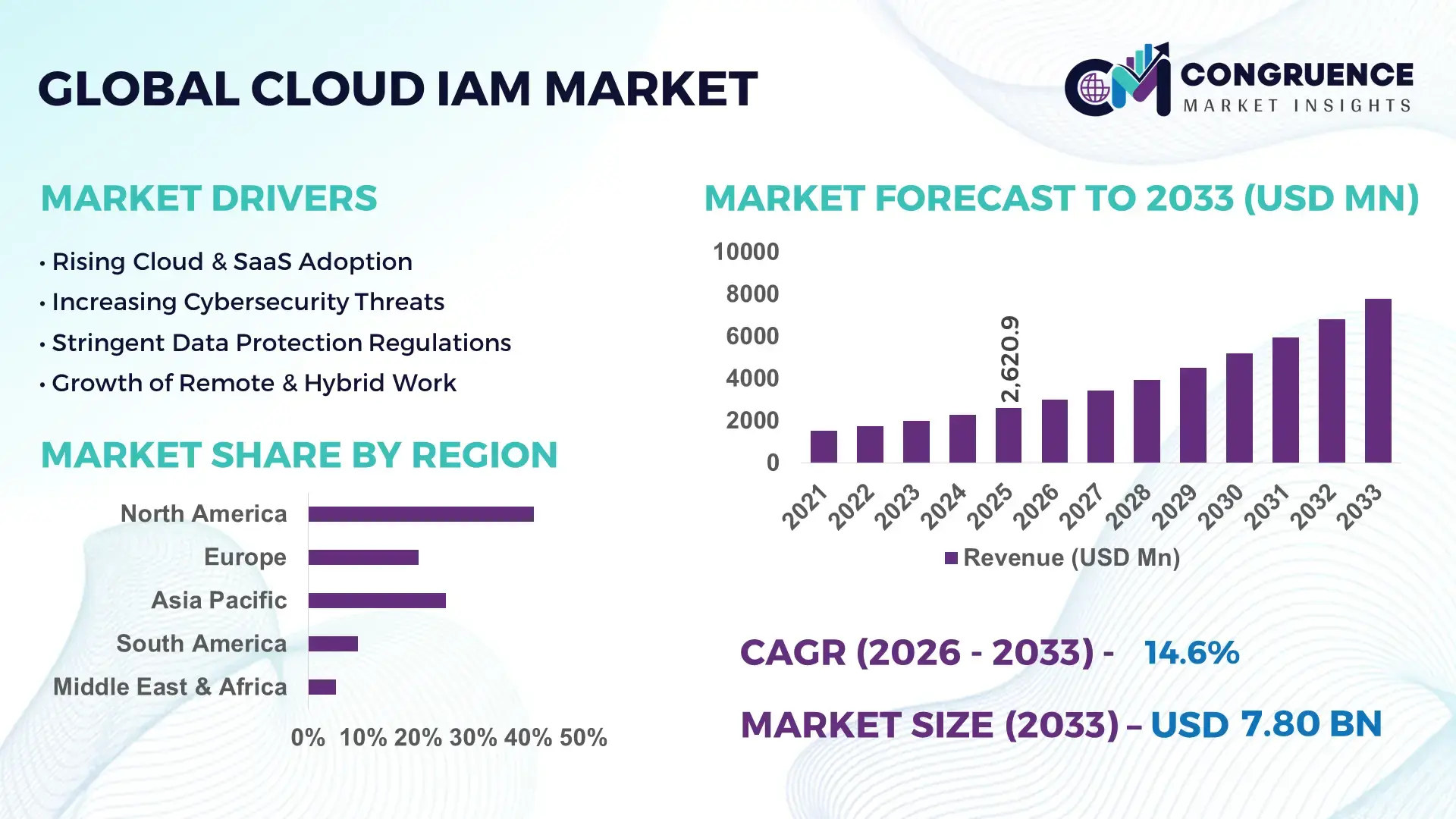

The Global Cloud IAM Market was valued at USD 2620.91 Million in 2025 and is anticipated to reach a value of USD 7797.03 Million by 2033 expanding at a CAGR of 14.6% between 2026 and 2033. The growth is primarily driven by increasing enterprise focus on secure digital identity management and regulatory compliance.

The United States remains a pivotal hub for Cloud IAM development, boasting extensive production capabilities and high investment levels in both startups and established cybersecurity firms. In 2024, over 65% of enterprise IT budgets in the country included cloud identity solutions, while adoption among mid-sized businesses exceeded 50%. Leading applications span financial services, healthcare, and government, with organizations implementing multi-factor authentication, identity governance, and zero-trust frameworks. Technological advancements, such as AI-driven identity analytics and adaptive authentication, are being integrated into large-scale enterprise deployments. The country also demonstrates robust regional adoption, with the Northeast and West Coast accounting for over 60% of deployments, highlighting concentrated innovation and early adoption trends.

Market Size & Growth: Valued at USD 2620.91 Million in 2025, projected to reach USD 7797.03 Million by 2033; CAGR of 14.6% driven by enterprise digital transformation and cybersecurity focus.

Top Growth Drivers: Cloud adoption acceleration 68%, regulatory compliance initiatives 55%, identity governance efficiency improvement 47%.

Short-Term Forecast: By 2028, organizations are expected to achieve 35% reduction in identity-related security incidents.

Emerging Technologies: AI-powered identity analytics, adaptive authentication, decentralized identity solutions.

Regional Leaders: United States USD 2800 Million, Europe USD 2100 Million, Asia-Pacific USD 1800 Million by 2033; U.S. shows high enterprise adoption, Europe emphasizes compliance-driven deployment, APAC growth fueled by fintech and cloud migration.

Consumer/End-User Trends: Financial services, healthcare, and government sectors drive adoption; increasing preference for cloud-native, scalable identity solutions.

Pilot or Case Example: In 2024, a U.S. banking consortium implemented AI-based adaptive authentication, reducing account breaches by 42% and downtime by 15%.

Competitive Landscape: Leading player: Okta (~25%), followed by Microsoft, IBM, Ping Identity, and SailPoint.

Regulatory & ESG Impact: GDPR, CCPA, and SOC 2 compliance drive market adoption; ESG initiatives promote secure and privacy-focused digital identity frameworks.

Investment & Funding Patterns: Over USD 1.2 Billion invested in 2024 across venture funding and strategic acquisitions for cloud IAM innovation.

Innovation & Future Outlook: Focus on AI integration, cloud-native IAM platforms, zero-trust adoption, and blockchain-based identity solutions shaping market evolution.

Cloud IAM adoption is expanding across banking, healthcare, government, and technology sectors, with enterprises increasingly prioritizing secure and automated identity management. Recent innovations include AI-driven behavioral analytics, passwordless authentication, and risk-based access control systems. Regulatory pressures such as GDPR and CCPA are enforcing stricter compliance, while economic drivers like cloud cost optimization are accelerating adoption. Regional growth trends indicate strong expansion in North America and APAC, driven by fintech, e-commerce, and large-scale cloud migration projects. Future outlook emphasizes enhanced interoperability, AI-assisted governance, and integration with emerging digital ecosystems, ensuring scalable, secure identity management solutions for complex enterprise environments.

The strategic relevance of the Cloud IAM Market lies in its ability to enable secure, scalable, and compliant identity management across diverse industries. Advanced AI-driven identity analytics delivers 40% improvement in threat detection compared to traditional rule-based access controls. North America dominates in volume, while Europe leads in adoption, with over 60% of enterprises implementing cloud-native IAM solutions. By 2028, adaptive authentication technologies are expected to reduce account compromise incidents by 35%, significantly improving enterprise security posture. Firms are committing to ESG improvements such as 20% reduction in digital identity-related energy consumption by 2030 through optimized cloud infrastructure. In 2024, a U.S.-based financial consortium achieved a 42% reduction in downtime by integrating AI-based behavioral analytics across its IAM platform. Strategic deployment of Cloud IAM ensures operational resilience by minimizing unauthorized access, enforcing regulatory compliance, and improving user experience through centralized identity governance. Looking forward, the Cloud IAM Market is poised to act as a pillar of resilient, compliant, and sustainable growth, supporting enterprises in navigating evolving digital ecosystems while embedding security and regulatory compliance at the core of business operations.

The escalating need for secure digital identity management is a primary driver of Cloud IAM adoption. In 2024, over 68% of global enterprises reported deploying cloud-based identity solutions to protect sensitive data and ensure compliance with regulations such as GDPR and CCPA. Multi-factor authentication and AI-based threat detection are increasingly implemented to prevent identity breaches, reducing potential financial losses by up to 35%. Cloud IAM enables centralized user access control and real-time monitoring, improving operational efficiency and minimizing security gaps. High adoption in sectors such as banking, healthcare, and government underscores the criticality of secure identity solutions. The integration of advanced analytics allows organizations to proactively detect anomalies and manage user privileges, fostering trust and enhancing user experience while reducing operational overhead and risk exposure.

Integration complexity with existing IT infrastructure remains a key restraint for Cloud IAM adoption. Enterprises with legacy systems often face challenges connecting older applications to modern IAM solutions, delaying deployment timelines. Surveys indicate that 42% of organizations experience integration issues, leading to increased operational costs and longer implementation cycles. Additionally, inconsistent security policies across hybrid environments can cause vulnerabilities, reducing the effectiveness of identity governance. Technical skill gaps among IT staff and resistance to process change further hinder widespread adoption. These limitations are particularly pronounced in industries with extensive on-premises legacy software, such as manufacturing and public sector institutions. Addressing these challenges requires substantial investment in training, middleware solutions, and phased implementation strategies to ensure seamless interoperability without compromising security or compliance.

AI-driven identity governance presents significant growth opportunities in the Cloud IAM Market. Advanced AI analytics can automate access certification, detect anomalous user behavior, and enforce adaptive authentication policies, reducing manual oversight by up to 50%. By 2027, predictive identity analytics is projected to improve threat detection rates by 40% for early adopters. Expansion into emerging markets, where cloud adoption is accelerating, also provides untapped potential, especially in fintech, healthcare, and e-commerce sectors. Organizations adopting AI-powered IAM are better positioned to comply with evolving data privacy regulations while optimizing operational efficiency. Additionally, the integration of blockchain-based identity solutions and decentralized authentication offers opportunities to enhance security and user control, creating new business models and service offerings. These innovations are poised to redefine enterprise identity management practices globally.

Rising cybersecurity threats and regulatory complexity remain significant challenges for the Cloud IAM Market. The increasing frequency of sophisticated cyberattacks, such as phishing, credential stuffing, and ransomware, forces enterprises to continuously update IAM protocols, increasing operational costs. Compliance with multiple overlapping regulations, including GDPR, CCPA, HIPAA, and ISO standards, adds layers of complexity for multinational organizations, often requiring specialized legal and technical expertise. In 2024, 38% of enterprises reported difficulties maintaining uniform access control policies across jurisdictions. Rapid technological changes, coupled with inconsistent adoption of cloud standards, exacerbate risk exposure and slow deployment. Addressing these challenges requires continuous investment in security technologies, staff training, and regulatory monitoring to ensure Cloud IAM solutions remain robust, compliant, and effective against evolving threats.

• Expansion of AI-Powered Authentication: AI-driven authentication solutions are transforming Cloud IAM practices, with over 62% of enterprises adopting AI-based risk scoring for user access. These systems detect anomalous behavior in real-time, reducing unauthorized access incidents by up to 45% and lowering manual identity verification tasks by 35%. Financial services and healthcare sectors are leading adoption due to sensitive data requirements.

• Growth of Passwordless and Biometric Solutions: Organizations are increasingly implementing passwordless authentication methods, including biometric verification, with 48% of large enterprises deploying at least one biometric system in 2024. Adoption has improved login efficiency by 30% and reduced credential-related security incidents by 28%, while improving end-user experience across mobile and cloud platforms.

• Surge in Multi-Cloud IAM Integration: Multi-cloud adoption has created a measurable demand for unified IAM solutions. Approximately 57% of global enterprises reported integrating IAM across at least two cloud providers, enabling centralized access control and reducing configuration errors by 40%. This trend is most pronounced in North America and APAC, where hybrid cloud deployments are prevalent.

• Adoption of Zero-Trust and Risk-Based Access Controls: Zero-trust frameworks and risk-based adaptive access policies are becoming standard, with 53% of organizations implementing continuous access evaluation in 2024. Enterprises using these models achieved a 38% decrease in security incidents and a 25% improvement in compliance adherence, particularly in sectors with strict regulatory oversight such as government and banking.

The Cloud IAM Market is structured around multiple dimensions including types, applications, and end-users, each reflecting evolving enterprise needs and technological adoption patterns. By type, solutions vary from identity governance and administration platforms to access management tools and privileged account management systems, enabling organizations to tailor security protocols. Application areas include enterprise security, regulatory compliance, IT operations, and customer identity management, with deployments reflecting sector-specific requirements. End-user adoption spans financial services, healthcare, government, and technology industries, with large enterprises demonstrating higher penetration, while SMEs are increasingly adopting cloud-based IAM solutions for scalability and compliance. Regional consumption patterns reveal North America leads in overall volume, while APAC shows rapid adoption driven by digital transformation initiatives. The segmentation analysis provides decision-makers with actionable insights on deployment strategies, prioritization of investment, and technology alignment to optimize identity and access management across organizations.

The Cloud IAM market encompasses several product types, including identity governance and administration (IGA), access management (AM), privileged access management (PAM), and identity-as-a-service (IDaaS) platforms. Identity governance and administration leads the market, accounting for 38% of adoption, due to its ability to centralize user lifecycle management and ensure compliance with regulations such as GDPR and CCPA. Access management follows closely with 28%, supporting secure authentication, single sign-on (SSO), and multi-factor authentication for enterprise users. The fastest-growing type is IDaaS, with adoption projected to surpass 20% by 2033, driven by cloud-native solutions, flexible subscription models, and rapid deployment capabilities. Privileged access management and other niche tools collectively contribute 14%, providing specialized security for critical systems.

Cloud IAM applications cover enterprise security, regulatory compliance, IT operations, and customer identity management (CIAM). Enterprise security remains the leading application, representing 40% of adoption, as organizations focus on preventing unauthorized access and protecting sensitive data. CIAM is the fastest-growing application, expected to reach 18% adoption by 2033, fueled by the rise of digital services, e-commerce, and personalized customer engagement strategies. Regulatory compliance applications hold 25% of market relevance, ensuring enterprises adhere to GDPR, HIPAA, and SOC 2 requirements, while IT operations management tools contribute 17%, optimizing administrative efficiency and user provisioning.

The leading end-user segment in the Cloud IAM market is large enterprises, accounting for 45% of adoption, due to complex IT environments and regulatory obligations. The fastest-growing end-user group is SMEs, projected to surpass 22% adoption by 2033, driven by scalable cloud platforms, subscription-based IDaaS solutions, and the need for secure remote work infrastructure. Other contributors include government agencies (18%) and technology firms (15%), leveraging IAM for compliance, access management, and security automation. Industry adoption rates are particularly high in banking (62%), healthcare (58%), and e-commerce (53%), reflecting sector-specific compliance and security needs.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15% between 2026 and 2033.

North America’s dominance is driven by widespread enterprise adoption, high cloud infrastructure investment exceeding USD 45 Billion in 2024, and regulatory compliance mandates across finance, healthcare, and government sectors. Asia-Pacific’s rapid expansion is fueled by emerging economies such as China, India, and Japan, which collectively represent over 55% of regional Cloud IAM deployments. Europe holds 28% market share, driven by GDPR compliance and advanced digital transformation initiatives, while South America and Middle East & Africa collectively contribute 18%, supported by fintech adoption and public sector modernization programs. Across all regions, identity governance, access management, and AI-based authentication solutions are witnessing measurable uptake, reflecting enterprises’ prioritization of security, regulatory compliance, and operational efficiency in multi-cloud environments.

How are enterprises leveraging cloud identity management for secure operations?

North America holds 41% of the Cloud IAM Market, reflecting high enterprise penetration across healthcare, banking, and government sectors. Regulatory initiatives such as CCPA and HIPAA compliance have accelerated deployment of AI-driven authentication and multi-factor access controls. Technological advancements, including adaptive authentication and zero-trust frameworks, are being integrated across large-scale cloud environments. Notable local players, such as Okta and Ping Identity, have launched identity governance solutions serving over 1,000 enterprise clients in 2024. Regional consumer behavior highlights higher adoption in healthcare and finance, with 62% of organizations implementing cloud-native IAM solutions, compared to 48% in other industries. The region also shows a preference for scalable subscription-based models, enabling rapid deployment and flexible access management.

How are European enterprises optimizing cloud identity solutions under regulatory pressure?

Europe accounts for 28% of the Cloud IAM Market, with Germany, UK, and France being the largest contributors. Strict regulatory frameworks like GDPR and ISO 27001 compliance drive demand for explainable Cloud IAM systems. Enterprises are increasingly adopting AI-powered access controls and identity analytics to enhance security and ensure audit readiness. Local players such as SAP and Micro Focus have introduced cloud-based identity governance platforms, facilitating secure employee and customer access for over 500 companies in 2024. Regional consumer behavior favors compliance-driven deployment, with organizations prioritizing solutions that support data privacy, traceable access logs, and automated reporting. Financial services, healthcare, and public institutions are the highest adopters, collectively representing over 60% of regional implementation.

What factors are driving the adoption of cloud-based identity management in APAC?

Asia-Pacific represents 23% of the Cloud IAM Market, with China, India, and Japan as top-consuming countries. Growth is supported by rapid digital transformation, mobile-first strategies, and expanding e-commerce ecosystems. Enterprises are investing in scalable cloud IAM platforms and AI-based adaptive authentication to secure sensitive data and optimize user access. Local players like Huawei and Alibaba Cloud have rolled out identity-as-a-service solutions to over 300 large enterprises in 2024. Regional consumer behavior is characterized by high adoption in fintech, technology, and telecom sectors, while government initiatives promoting digital ID infrastructure are further accelerating market penetration.

How are emerging enterprises adopting cloud identity solutions in South America?

South America holds 10% of the Cloud IAM Market, with Brazil and Argentina as primary contributors. Infrastructure modernization and growth in the energy and media sectors are boosting Cloud IAM adoption. Government incentives supporting digital transformation and cybersecurity initiatives have encouraged enterprises to implement AI-driven access management. Local companies such as TOTVS are offering identity governance solutions for over 200 organizations across financial services and education sectors. Regional consumer behavior shows heightened demand for solutions supporting language localization, secure mobile access, and compliance with emerging data privacy regulations.

What strategies are shaping the adoption of cloud identity solutions in MEA?

Middle East & Africa represents 8% of the Cloud IAM Market, with UAE and South Africa leading deployment. Growth is driven by oil & gas, construction, and public sector modernization, alongside government mandates for digital security. Technological modernization trends, including cloud-based adaptive authentication and zero-trust frameworks, are being implemented across enterprise environments. Local players such as Etisalat and Dimension Data are providing cloud IAM solutions to over 150 regional clients in 2024. Regional consumer behavior emphasizes enterprise adoption in government and energy sectors, with a focus on centralized access controls and regulatory compliance adherence.

United States – 38%: High production capacity, strong end-user demand in finance and healthcare, and early adoption of AI-driven IAM solutions.

China – 21%: Rapid digital infrastructure expansion, large enterprise adoption, and government-backed cloud identity initiatives.

The Cloud IAM market is moderately fragmented, with over 120 active competitors globally, ranging from specialized startups to established cybersecurity and cloud service providers. The top five companies—Okta, Microsoft, IBM, Ping Identity, and SailPoint—collectively hold approximately 62% of the market, indicating significant concentration among leading players. Competition is shaped by aggressive product innovation, including AI-driven adaptive authentication, passwordless access, and identity analytics platforms. Strategic initiatives such as partnerships with cloud service providers, mergers and acquisitions, and the launch of identity-as-a-service (IDaaS) solutions are common; for example, Microsoft expanded its identity management suite in 2024 to integrate advanced AI threat detection across Azure clients. Innovation trends are increasingly influencing market positioning, with companies investing in zero-trust frameworks, multi-cloud integration, and blockchain-based identity solutions. Emerging players are targeting SMEs and niche industry verticals, leveraging cost-effective, cloud-native solutions. Regional expansion is another key driver, with North America and Europe accounting for 69% of deployments, while APAC demonstrates rapid adoption, prompting incumbents to establish localized support centers and R&D hubs. Overall, competitive intensity is high, prioritizing technological differentiation, compliance-focused features, and scalable enterprise solutions.

Ping Identity

SailPoint

ForgeRock

OneLogin

RSA Security

NetIQ

Auth0

SecureAuth

Evidian

The Cloud IAM market is experiencing significant technological evolution, driven by the integration of advanced AI, machine learning, and cloud-native frameworks. AI-powered identity analytics is now deployed in over 58% of enterprises globally, enabling real-time monitoring of user behavior, detection of anomalous access patterns, and automated risk scoring. Adaptive authentication, including context-aware multi-factor authentication, is being implemented in 47% of financial institutions and healthcare organizations, significantly reducing account compromise incidents by up to 42%. Passwordless authentication technologies, such as biometric verification and cryptographic key-based access, are gaining traction, with 36% of global organizations adopting them in 2024 to improve login efficiency and reduce credential theft. Zero-trust architecture is becoming a core deployment strategy, with 53% of large-scale enterprises integrating continuous access verification to enforce least-privilege access policies.

Emerging technologies such as blockchain-based decentralized identity (DID) solutions are also influencing the Cloud IAM landscape, particularly in APAC and North America, where 14% of enterprises are piloting blockchain-enabled identity systems for secure cross-border transactions and supply chain verification. Cloud-native IAM platforms are increasingly preferred over on-premises systems, providing scalability, integration with multi-cloud environments, and rapid deployment capabilities. Technological innovation is further supported by automation in privileged access management, real-time compliance reporting, and identity lifecycle management. Enterprises adopting these technologies report measurable outcomes, including a 38% reduction in administrative overhead and a 29% improvement in compliance accuracy. Overall, technological advancements are central to enhancing security, operational efficiency, and regulatory adherence, positioning Cloud IAM as a critical enabler of enterprise resilience.

• In April 2024, Okta acquired Axiom Security to enhance its Privileged Access Management (PAM) capabilities, integrating Just-In-Time (JIT) access and automated review workflows across cloud and on-premises environments. The integration aims to improve risk mitigation across infrastructure such as GitHub, Snowflake, and PostgreSQL systems. (IT Pro)

• In March 2025, Microsoft expanded its partnership ecosystem by integrating Delinea into the Microsoft Security Store, enabling centralized privileged access management and AI-driven governance across hybrid cloud environments, enhancing Entra ID capabilities for large enterprise deployments.

• In June 2025, LoginRadius launched “Partner IAM,” a purpose-built solution for managing identities and access for external users in B2B SaaS ecosystems, targeting secure integrations for partners, resellers, and suppliers amid growing multi-tenant architecture demands. (LoginRadius)

• In late 2025, Okta announced plans to expand its India workforce by 50% by 2026 to accelerate AI-driven security innovation, focusing on deeptech engineering and product development to support global IAM product enhancements. (The Economic Times)

The Cloud IAM Market Report provides a comprehensive analysis of identity and access management solutions deployed in cloud environments, covering technological, application, and regional dimensions critical for strategic decision-making. The report examines product segments such as identity governance and administration, access management, privileged access management, CIAM solutions, and emerging decentralized identity frameworks, characterizing their operational roles and enterprise adoption patterns. It also highlights technology trends including AI-based adaptive authentication, passwordless access, zero-trust architectures, and federated identity systems used by organizations to manage secure access across workforce, partner, and customer identities. Geographic segmentation spans key regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—offering insights into regional infrastructure trends, regulatory impacts, and localized consumer behaviors that influence deployment strategies. The analysis includes application areas such as security operations, regulatory compliance, IT operations, and digital customer engagement, detailing how varied industry verticals like finance, healthcare, government, and technology tailor IAM solutions to their needs. The report further identifies niche segments like mobile-native IAM, biometric authentication platforms, and partner ecosystem identity solutions. Emerging topics include integration of IAM with broader cybersecurity frameworks, identity threat detection, and SaaS adoption patterns among SMEs. Designed for enterprise architects, CISOs, and industry leaders, the report offers actionable intelligence on competitive dynamics, technology benchmarking, and growth opportunities in secure cloud identity management.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 14.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Okta, Microsoft, IBM, Ping Identity, SailPoint, ForgeRock, OneLogin, RSA Security, NetIQ, Auth0, SecureAuth, Evidian |

Customization & Pricing | Available on Request (10% Customization is Free) |