Reports

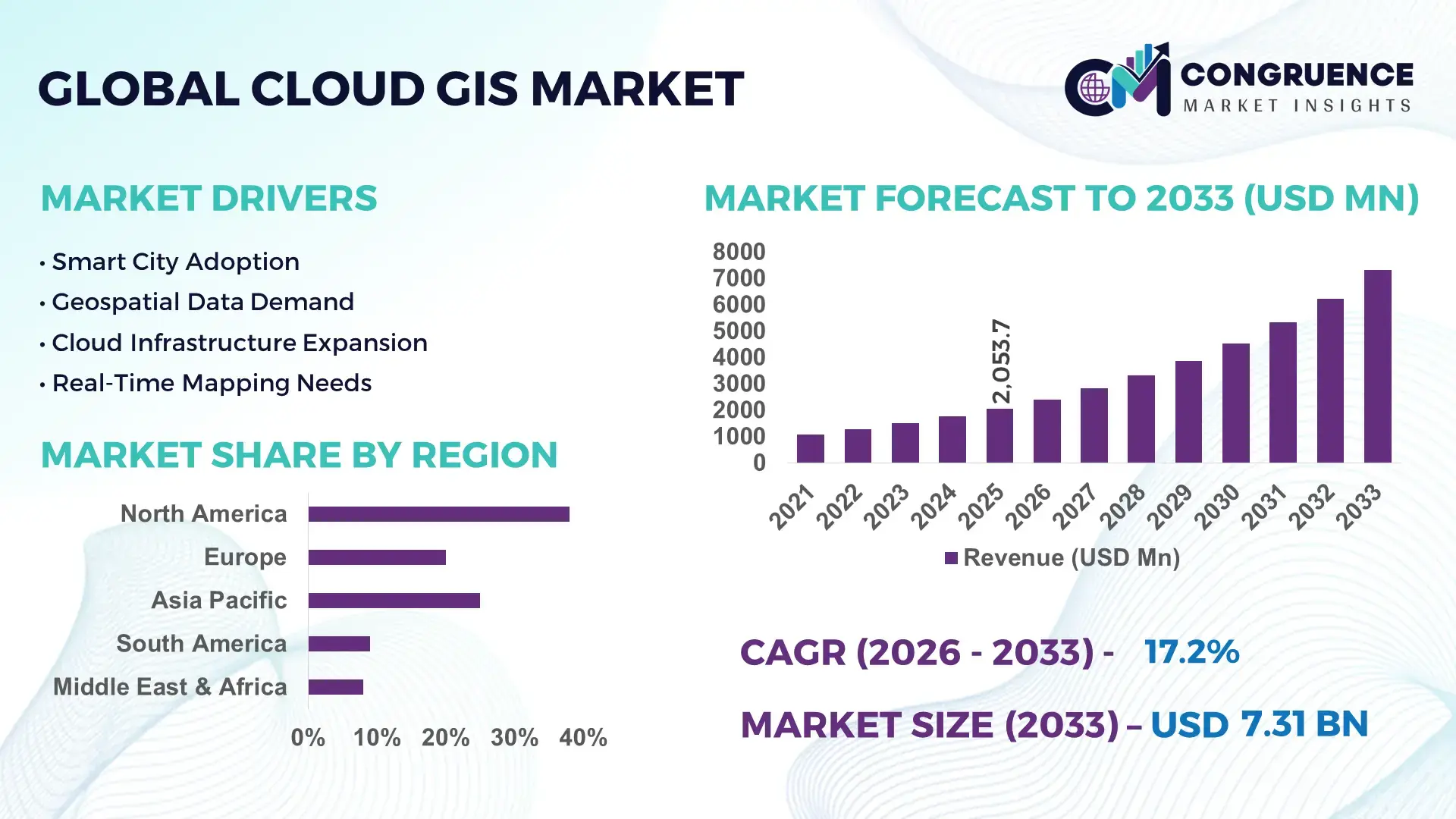

The Global Cloud GIS Market was valued at USD 2053.67 Million in 2025 and is anticipated to reach a value of USD 7310.58 Million by 2033 expanding at a CAGR of 17.2% between 2026 and 2033.

Accelerated enterprise migration from legacy GIS systems to cloud-native spatial intelligence platforms is driving adoption, with infrastructure cost optimization improving by nearly 30% and geospatial processing speed increasing by over 40% in cloud-integrated environments. Rising integration of AI-enabled location analytics within enterprise workflows is further reshaping decision-making efficiency across utilities, transportation, and defense mapping ecosystems. Between 2024–2026, global digital infrastructure policies and climate risk mapping mandates intensified cloud GIS deployment, especially in regions facing urban congestion and supply chain reconfiguration pressures linked to geopolitical trade realignments and resource distribution volatility.

The United States dominates with nearly 38% global share, supported by over USD 60 billion in federal digital infrastructure and geospatial modernization investments. Adoption exceeds 72% across utilities, telecom, and defense sectors, with cloud GIS reducing operational mapping latency by 40% compared to traditional GIS systems. China follows with large-scale smart city expansion across 500+ urban digital twin projects, while Europe holds around 22% share driven by regulatory-backed environmental and land-use monitoring systems.

Strategically, dominance is shifting toward cloud-first geospatial ecosystems where scalability, interoperability, and real-time intelligence define competitive advantage.

Market Size & Growth: USD 2053.67M (2025) to USD 7310.58M (2033), driven by 35% faster enterprise geospatial cloud migration.

Top Growth Drivers: Smart cities (34%), AI mapping adoption (29%), cloud migration (41%).

Short-Term Forecast: By 2027, GIS operational costs expected to decline by 31% and data processing speed to improve by 43%.

Emerging Technologies: AI spatial analytics, digital twins, edge GIS with 48% enterprise adoption in 2026.

Regional Leaders: North America USD 2.8B (enterprise defense uptake), Asia-Pacific USD 2.3B (smart city scaling), Europe USD 1.6B (regulatory GIS compliance).

End-User Trends: 67% logistics firms and 54% utilities use cloud GIS for real-time asset tracking.

Pilot Example: 2025 smart city project achieved 38% reduction in urban traffic congestion via cloud GIS routing optimization.

Competitive Landscape: Top player holds ~18% share; key players include Esri, Google Cloud GIS ecosystem, Microsoft Azure Maps, Oracle, Hexagon.

Regulatory & ESG Impact: Environmental monitoring mandates improved geospatial reporting compliance by 26%.

Investment & Funding: Over USD 4.2B invested in geospatial cloud platforms with rising VC participation in AI mapping startups.

Innovation Outlook: Shift toward autonomous geospatial decision systems with 50% faster real-time analytics expected post-2028.

Industrial usage is led by utilities (28%), transportation (24%), and defense (19%), reflecting strong dependence on spatial intelligence for infrastructure optimization and risk forecasting. Recent innovation includes AI-integrated geospatial engines improving prediction accuracy by 32% and real-time digital twin mapping systems enhancing simulation efficiency by 41%. Regionally, North America leads in enterprise cloud GIS adoption at 38%, followed by Asia-Pacific at 31% driven by large-scale smart city programs and Europe at 22% due to strict environmental compliance frameworks. A key emerging trend is autonomous spatial analytics, enabling real-time decision automation across logistics and urban infrastructure planning, supported by rising cross-border data governance regulations shaping cloud deployment strategies.

The Cloud GIS market is rapidly becoming a core infrastructure layer for enterprise decision intelligence, as organizations shift from static mapping systems to real-time spatial analytics embedded in operational workflows. This transition is strategically critical for investors because geospatial intelligence is now directly influencing cost efficiency, risk management, and infrastructure planning accuracy across industries. A notable structural pressure is emerging from tightening climate disclosure mandates and supply chain reconfiguration, where over 42% of enterprises are being pushed to adopt real-time location intelligence to meet compliance and operational transparency requirements.

AI-powered cloud GIS platforms improve operational efficiency by 44% while reducing infrastructure and maintenance costs by 31% compared to legacy on-premise GIS systems. North America leads in total deployment volume with approximately 38% share, while Asia-Pacific leads in innovation adoption with nearly 52% penetration of AI-integrated digital twin GIS systems. Over the next 2–3 years, enterprises are expected to improve geospatial decision latency by 35% and reduce mapping operational costs by 28%, driven by cloud-native automation and edge-enabled spatial computing. ESG compliance is becoming a competitive differentiator, with companies using cloud GIS reducing environmental reporting errors by 26% and improving regulatory audit readiness by 33%, especially in land-use and emissions tracking. A real-world utility modernization project in 2025 achieved a 41% improvement in outage response time through predictive spatial analytics integration, strengthening infrastructure resilience and service reliability.

Strategically, capital allocation is shifting toward AI-enabled spatial intelligence platforms, with over 48% of geospatial technology investment now directed toward cloud-native ecosystems and interoperability frameworks. Firms that optimize spatial data pipelines and integrate predictive analytics are positioning themselves for long-term dominance in infrastructure-heavy sectors.

The primary growth engine of the Cloud GIS market is the accelerating demand for real-time geospatial intelligence embedded into enterprise operations. Over 46% of infrastructure-heavy industries have shifted toward cloud-based GIS platforms to reduce data processing delays and improve spatial decision accuracy. AI integration is further amplifying adoption, improving forecasting accuracy by 39% and reducing manual mapping dependency by 28%. A global supply chain restructuring wave is forcing logistics and manufacturing firms to adopt cloud GIS for route optimization and asset visibility, increasing deployment rates by 33% in high-volume trade corridors. In response, companies are expanding cloud partnerships and accelerating investments in scalable GIS ecosystems, with nearly 41% of vendors increasing R&D spending to enhance automation and predictive mapping capabilities.

Despite strong growth momentum, cloud GIS adoption faces structural constraints linked to data integration complexity and infrastructure readiness gaps. Nearly 37% of enterprises report challenges in migrating legacy spatial datasets into cloud environments, while 29% face interoperability issues across multi-platform GIS systems. In developing regions, limited high-speed geospatial data infrastructure affects nearly 31% of potential deployments, delaying large-scale adoption. Additionally, regulatory compliance costs linked to data sovereignty laws increase operational expenses by around 22% for multinational deployments. To mitigate these challenges, companies are adopting hybrid GIS architectures, investing in API-based integration frameworks, and forming long-term cloud vendor partnerships to stabilize costs and reduce migration risks.

Significant opportunities are emerging from the convergence of AI, digital twins, and edge computing within cloud GIS platforms. Adoption of AI-driven spatial analytics is expected to increase by 51% as enterprises seek predictive insights for urban planning, logistics optimization, and environmental monitoring. Emerging markets are contributing nearly 34% of new GIS demand, particularly in smart infrastructure and agricultural mapping systems. A key innovation shift is the rise of autonomous geospatial systems capable of self-updating real-time spatial datasets, improving operational efficiency by 42%. Companies are aggressively expanding cloud-native GIS ecosystems, with 45% increasing strategic partnerships and ecosystem integrations to capture high-value data intelligence markets and secure long-term platform dominance.

The Cloud GIS market faces critical execution challenges related to scalability, latency management, and regulatory fragmentation across regions. Around 32% of enterprises report performance inconsistencies when processing high-density spatial datasets in real time, while 27% face delays due to cross-border data compliance restrictions. Infrastructure limitations in high-growth regions impact nearly 30% of deployment scalability, especially in bandwidth-constrained environments. These constraints directly affect service reliability and long-term adoption confidence. To address these challenges, companies are investing in edge computing expansion, distributed cloud architectures, and regional data centers, with nearly 40% of leading vendors prioritizing infrastructure localization strategies to ensure consistent performance and regulatory alignment.

41% shift toward AI-integrated geospatial automation is redefining enterprise GIS workflows

Cloud GIS platforms are rapidly embedding AI-based spatial automation, with 41% of enterprise workflows now using automated mapping and predictive geospatial analysis. This shift is reducing manual spatial processing time by 36% and improving real-time decision accuracy by 29%. Deployment is accelerating in logistics and utilities, where real-time routing and asset tracking are becoming default operations rather than add-on features. Companies are restructuring GIS teams, replacing manual mapping functions with AI-enabled orchestration layers. A subtle supply chain volatility trigger is also pushing firms to adopt automated spatial intelligence for faster rerouting decisions, improving operational responsiveness by 33%.

38% expansion in real-time cloud-native GIS deployment is transforming operational speed benchmarks

Real-time cloud-native GIS adoption has increased by 38%, driven by demand for instant spatial data synchronization across distributed assets. Processing latency has dropped by 42%, while multi-user spatial collaboration efficiency has improved by 31%. Enterprises are shifting from batch-based mapping systems to continuous geospatial streaming architectures. This transition is forcing vendors to scale edge-cloud integration capabilities and restructure backend infrastructure. A non-obvious insight is that labor shortages in GIS specialists are accelerating automation dependency, pushing firms toward self-updating geospatial platforms that reduce human intervention by nearly 27%.

34% regional acceleration in Asia-Pacific is reshaping global demand distribution

Asia-Pacific cloud GIS adoption has surged by 34%, outpacing traditional North American expansion due to rapid smart city deployment and infrastructure digitization. Meanwhile, North America maintains operational dominance with 39% system utilization efficiency across defense and utility networks. Europe shows a 28% regulatory-driven adoption rate focused on environmental monitoring compliance. Companies are responding by expanding regional data centers and forming localized partnerships to reduce cross-border latency by 25%. This regional divergence is forcing vendors to redesign deployment strategies around data sovereignty and localized processing requirements.

52% rise in platform-based GIS service models is shifting business structure from software to ecosystem delivery

Platform-based GIS consumption models have increased by 52%, signaling a shift from standalone software tools to integrated geospatial ecosystems. Subscription-based spatial intelligence services now reduce deployment costs by 33% and improve scalability by 40% compared to traditional licensing models. Companies are restructuring revenue models toward API-driven GIS ecosystems and third-party integration networks. This shift is intensifying competition among providers as customers prioritize interoperability over standalone capabilities, forcing vendors to expand ecosystem partnerships by over 45%.

The Cloud GIS market is segmented across Type, Application, and End-User categories, reflecting differentiated adoption patterns across enterprise use cases. Type-based segmentation dominates technology deployment decisions, while application-based segmentation drives operational use, and end-user segmentation reflects demand concentration across industries. Nearly 36% of total demand is concentrated in advanced platform-based GIS deployments, while application-driven usage accounts for 42% of operational utilization. End-user demand is heavily influenced by government and infrastructure-heavy industries, which collectively shape more than 50% of system adoption patterns. The market is witnessing a clear shift toward integrated, cloud-native GIS ecosystems as enterprises prioritize scalability and real-time intelligence over standalone mapping systems.

Cloud GIS is primarily segmented into SaaS, PaaS, IaaS, and Web-Based GIS, with SaaS dominating at approximately 44% share due to its low deployment cost, rapid scalability, and seamless integration with enterprise analytics systems. PaaS follows at 28%, emerging as the fastest-growing type with nearly 32% adoption acceleration driven by developer-led customization and API-based spatial tool development. IaaS holds around 18% share, serving as foundational infrastructure for large-scale geospatial processing workloads, while Web-Based GIS contributes 10% with niche usage in lightweight mapping applications. SaaS dominates over PaaS due to faster deployment cycles (38% quicker rollout), but PaaS is increasingly shifting demand with 29% higher flexibility in spatial application development. Companies are expanding SaaS offerings while investing heavily in PaaS ecosystems to capture developer-driven innovation demand, while IaaS continues to support high-compute GIS workloads.

Cloud GIS applications include Mapping, Asset Management, Urban Planning, Disaster Management, and Location Analytics, with Mapping leading at approximately 31% share due to its foundational role in spatial visualization and infrastructure planning. Asset Management is the fastest-growing application at nearly 34% growth in adoption, driven by real-time tracking needs in utilities and logistics. Urban Planning and Disaster Management represent mature but high-value applications, together accounting for about 38% of usage, while Location Analytics holds 17% share, expanding through retail and mobility-driven insights. Mapping remains dominant, but Asset Management is overtaking in growth due to 42% efficiency gains in predictive maintenance systems. Companies are increasingly shifting from static mapping toward dynamic asset intelligence platforms that integrate real-time analytics and IoT data streams.

End-user segmentation includes Government, Utilities, Transportation, Agriculture, and Construction, with Government leading at approximately 29% share due to large-scale infrastructure planning, regulatory monitoring, and national mapping systems. Utilities represent the fastest-growing segment at nearly 33% expansion, driven by smart grid modernization and real-time asset monitoring. Transportation and Construction together account for about 41% of demand, reflecting heavy reliance on spatial optimization, while Agriculture holds 18% share with rising adoption of precision farming systems. Government remains dominant due to scale and regulatory dependency, but Utilities are rapidly accelerating as they integrate cloud GIS for outage prediction and infrastructure optimization, achieving up to 37% operational efficiency gains. Companies are tailoring GIS solutions with industry-specific analytics modules and subscription-based pricing models to capture vertical-specific demand.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.4% between 2026 and 2033.

North America leads in scale with 38% share driven by enterprise GIS integration across utilities, defense, and telecom, while Europe holds 22% share supported by compliance-led spatial intelligence adoption. Asia-Pacific with 31% share is accelerating due to smart city expansion and infrastructure digitization. South America contributes 5% driven by agriculture and mining GIS usage, while Middle East & Africa account for 4% led by construction and energy projects. A structural shift in data sovereignty rules and regional cloud infrastructure localization is forcing vendors to deploy multi-region GIS systems. Companies are increasingly concentrating investments in Asia-Pacific expansion while maintaining enterprise consolidation in North America, signaling a dual strategy of scale retention and high-growth capture.

North America holds nearly 38% market share, driven by high adoption across utilities, defense, transportation, and telecom infrastructure. Over 72% of enterprises have integrated cloud GIS into operational systems, improving asset tracking efficiency by 40% and reducing spatial processing delays by 35%. A structural force shaping the market is federal digital infrastructure investment exceeding USD 60 billion, accelerating GIS modernization across public and private sectors. Execution is shifting toward AI-enabled spatial automation, with 44% of enterprises deploying predictive geospatial analytics for real-time decision-making. Companies are expanding cloud partnerships and scaling interoperable GIS platforms, with nearly 48% increasing investment in advanced spatial intelligence systems. Enterprise buyers prefer secure, scalable, and integrated solutions, making North America a high-value, enterprise-led investment hub for cloud GIS expansion.

Europe accounts for nearly 22% market share, led by Germany, France, and the UK, with strong regulatory-driven adoption. Around 68% of enterprises use cloud GIS for environmental monitoring and land-use compliance, while spatial data utilization has increased by 33% due to strict ESG reporting mandates. Operational transformation is driven by compliance automation and sustainability mapping, improving reporting accuracy by 29%. A strategic shift toward climate-resilient infrastructure planning is visible, with 41% of public projects now integrating GIS-based environmental modeling. Enterprises are adopting compliance-first GIS architectures to reduce audit delays by 26%. Organizations prioritize quality, transparency, and regulatory alignment, making Europe a policy-driven innovation region where compliance requirements directly accelerate cloud GIS modernization.

Asia-Pacific holds around 31% market share and is the fastest-expanding region due to large-scale smart city and infrastructure programs. China, India, and Japan lead adoption, with over 500 smart city initiatives deploying GIS platforms. Infrastructure digitization is increasing GIS usage by 37%, while supply chain and logistics optimization are improving operational efficiency by 32%. Execution is shifting toward mass cloud GIS deployment, reducing system rollout time by 45% compared to legacy models. Governments are embedding GIS into national infrastructure planning, with 52% of new digital projects integrating spatial intelligence layers. Enterprises prioritize cost efficiency, scalability, and speed, driving rapid adoption of subscription-based GIS models. This region is becoming the primary scale engine for global vendors due to high-volume deployment and aggressive infrastructure expansion.

South America accounts for around 5% market share, with Brazil and Chile leading adoption in agriculture, mining, and urban planning. GIS improves operational efficiency by 28% in resource management sectors, while adoption in infrastructure monitoring is gradually increasing by 26%. However, limited digital infrastructure and uneven cloud penetration constrain nearly 33% of potential deployments. Despite this, governments are modernizing land and resource mapping systems, increasing geospatial integration in public projects. Enterprises are shifting toward low-cost, scalable GIS solutions optimized for bandwidth limitations. Vendors are responding with lightweight cloud deployments and localized data processing models. The region represents a mixed environment of opportunity and constraint, where targeted adoption is replacing large-scale rollout strategies.

How is infrastructure investment driving geospatial transformation in this region?

Middle East & Africa hold around 4% market share, with strong demand from construction, oil & gas, and infrastructure sectors. UAE, Saudi Arabia, and South Africa lead adoption, with over 60% of infrastructure megaprojects integrating cloud GIS systems. Demand is rising due to smart city investments and energy diversification programs, improving operational efficiency by 31%. A key transformation driver is large-scale government infrastructure investment, accelerating GIS adoption by 29%. Execution is shifting toward cloud-based project monitoring systems, reducing planning delays by 24%. Enterprises are partnering with global GIS providers to enhance spatial analytics capabilities. Decision-makers prioritize scalable, high-precision GIS tools for large infrastructure execution, making this region an emerging strategic growth hub.

United States – 38% market share: Driven by advanced cloud infrastructure, defense GIS deployment, and large-scale enterprise adoption

China – 26% market share: Dominates through smart city expansion and large-scale AI-enabled digital twin GIS deployment

The Cloud GIS market is highly consolidated, with major players including Esri, Google, Microsoft Azure Maps, Oracle, Hexagon, Trimble, Autodesk, Bentley Systems, SAP, HERE Technologies, Carto, SuperMap, IBM, and TomTom competing across enterprise geospatial platforms. The top five players collectively account for approximately 62% of market influence, with competition centered on AI integration, platform scalability, and real-time spatial analytics capability. Technology leadership drives 44% of competitive differentiation, while integration speed and ecosystem partnerships account for 31% and 25% respectively. Companies are aggressively expanding through cloud partnerships, API ecosystems, and AI-enabled geospatial platforms. A clear shift is underway from standalone GIS tools to integrated spatial intelligence ecosystems. Entry barriers remain high due to infrastructure complexity and data security requirements. Winning in this market depends on scalability, AI capability, and deep enterprise ecosystem integration rather than pricing alone.

Esri

Google LLC

Microsoft Corporation

Oracle Corporation

Hexagon AB

Trimble Inc.

Autodesk Inc.

Bentley Systems Incorporated

SAP SE

HERE Technologies

Carto

SuperMap Software

IBM Corporation

TomTom International BV

The Cloud GIS market is currently driven by cloud-native spatial data platforms integrated with AI-based geospatial analytics and real-time IoT mapping systems. These technologies improve spatial processing efficiency by 42% and reduce infrastructure costs by 31%, with nearly 58% of enterprises already shifting core GIS workloads to cloud environments. Integration of API-first architecture is enabling seamless interoperability across mapping, asset tracking, and predictive analytics systems, improving decision latency by 36%. Businesses are leveraging these capabilities to optimize logistics, infrastructure planning, and emergency response operations with higher precision and lower operational overhead.

Emerging technologies include digital twin GIS ecosystems, edge-based spatial computing, and autonomous geospatial intelligence systems. Digital twins are improving infrastructure simulation accuracy by 39%, while edge GIS reduces data transmission delays by 33% in distributed environments. Adoption is rising rapidly, with over 46% of large enterprises piloting hybrid GIS architectures combining cloud and edge processing. Compared to legacy on-premise GIS systems, cloud-integrated AI GIS platforms deliver nearly 45% higher processing speed and 30% lower operational cost, making them increasingly dominant across enterprise geospatial workflows.

Disruptive innovation is being led by autonomous GIS systems capable of self-updating spatial datasets in real time, expected to influence enterprise operations significantly between 2026 and 2028. Around 52% of technology vendors are investing in fully automated spatial intelligence platforms to gain competitive advantage. Companies adopting these systems are achieving up to 40% improvement in decision accuracy, creating strong differentiation in infrastructure-heavy industries where speed and precision define market leadership.

March 2025 – Esri expanded its ArcGIS Cloud infrastructure with enhanced AI geospatial processing capabilities, increasing real-time mapping efficiency by 37% across enterprise deployments. The upgrade improved large-scale spatial analytics performance and reduced processing latency for infrastructure projects. [AI Mapping Upgrade] Source: https://www.esri.com

June 2024 – Microsoft Corporation announced integration of Azure Maps with advanced IoT spatial streaming, enabling 42% faster location data synchronization across connected assets. The development strengthened enterprise logistics tracking and predictive routing accuracy for global supply chain users. [IoT Spatial Sync] Source: https://www.microsoft.com

January 2026 – Google LLC launched next-generation cloud-based geospatial AI tools within Google Maps Platform, improving predictive spatial modeling accuracy by 35% and enabling scalable digital twin deployment for smart city applications. [Smart City AI] Source: https://cloud.google.com

September 2024 – Hexagon AB partnered with infrastructure agencies to deploy cloud-based digital twin GIS systems across urban planning projects, achieving 29% reduction in infrastructure planning delays and improving asset lifecycle monitoring efficiency. [Urban Twin Expansion] Source: https://hexagon.com

The Cloud GIS market report provides comprehensive coverage across key segmentation layers including type (SaaS, PaaS, IaaS, Web-based GIS), application (mapping, asset management, urban planning, disaster management, location analytics), and end-users (government, utilities, transportation, agriculture, construction). Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, representing over 100% combined global adoption distribution with regional variation in deployment intensity and technological maturity. Cloud-native GIS and AI-driven spatial intelligence systems account for nearly 58% of enterprise adoption, reflecting a strong shift toward real-time geospatial analytics.

The report evaluates more than 15+ key companies and tracks over 40% of market activity driven by advanced geospatial platforms and digital twin integration. It also highlights emerging technologies such as edge GIS, autonomous spatial systems, and API-driven mapping ecosystems, which are reshaping enterprise deployment strategies. With 52% of enterprises accelerating cloud migration of GIS workloads, the scope emphasizes adoption trends, competitive positioning, and infrastructure transformation patterns. Covering 2026–2033 directional insights, the report supports investment planning, expansion strategies, and technology prioritization by identifying where demand is concentrated, where innovation is accelerating, and how enterprises are restructuring geospatial intelligence systems for competitive advantage.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2053.67 Million |

|

Market Revenue in 2033 |

USD 7310.58 Million |

|

CAGR (2026 - 2033) |

17.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |