Reports

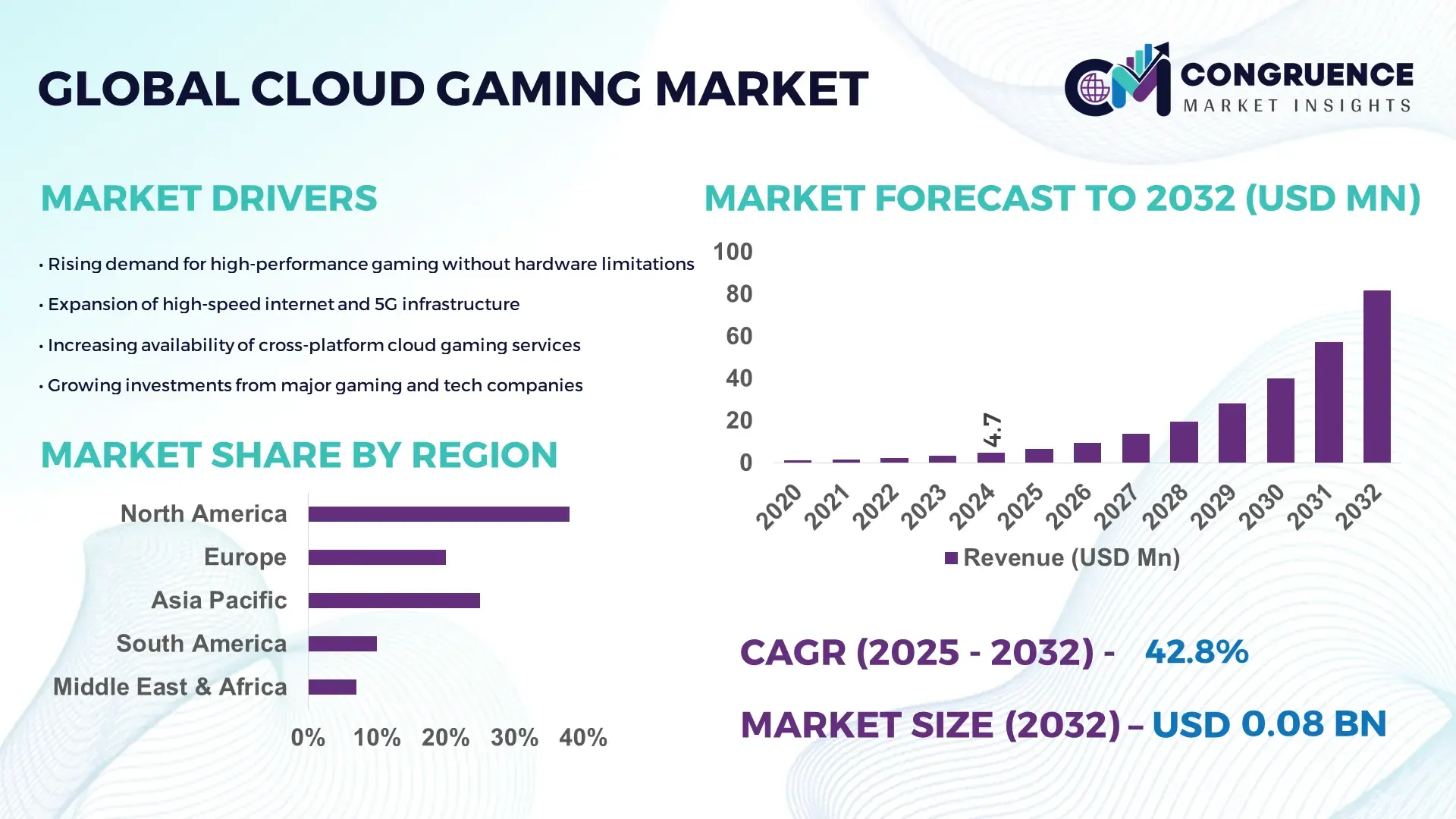

The Global Cloud Gaming Market was valued at USD 4.73 Million in 2024 and is anticipated to reach a value of USD 81.8 Million by 2032 expanding at a CAGR of 42.8% between 2025 and 2032. This rapid expansion is being driven by increasing broadband penetration, reduced latency through edge computing, and rising consumer demand for hardware‑agnostic gaming.

In the United States, the cloud gaming market is particularly advanced: the U.S. market size was estimated at USD 447.7 million in 2024 and is projected to reach USD 3,887.8 million by 2030, growing at a CAGR of 42.7%. Investment levels are very high, with major carriers like Verizon and Comcast driving GPU capacity closer to end-users via edge nodes. Key industry applications include subscription-based service models, competitive multiplayer gaming, and console-to-cloud cross-platform play. Technological advancements center on low-latency 5G networks, high-speed fiber, and improvements in file‑streaming and video‑streaming architectures. Consumer adoption in the U.S. is also robust: smartphones accounted for around 38.2% of usage in 2024, while casual gamers made up about 46.5% of the cloud gaming user base.

Market Size & Growth: The global market stood at USD 4.73 Million in 2024 and is forecast to reach USD 81.8 Million by 2032, growing at a CAGR of 42.8%, driven by improvements in network infrastructure and device accessibility.

Top Growth Drivers: High‑speed internet adoption (effective +45%), edge computing deployment (+30%), and increasing smartphone/tablet gaming penetration (+25%).

Short-Term Forecast: By 2028, end‑user cost per gaming session is expected to reduce by ~20%, while streaming performance (latency and frame rate) could improve by ~35%.

Emerging Technologies: Real‑time 5G edge computing, file‑streaming optimization, and AI‑driven adaptation of game quality.

Regional Leaders: North America: Projected to reach ~USD 12 billion by 2032, driven by 5G and cloud adoption. Asia-Pacific: Expected to hit ~USD 40 billion by 2032, led by mobile-first cloud gamers in China, India, and Japan. Europe: Forecast to reach ~USD 20 billion by 2032, buoyed by fiber‑optic infrastructure and cross‑platform services.

Consumer/End-User Trends: Cloud gaming is increasingly adopted by casual gamers and mobile users; sessions are migrating from high-end consoles to smartphones and smart TVs.

Pilot or Case Example: In 2025, a telco‑cloud pilot deployed edge‑node streaming in a U.S. metro, reducing latency by 40% and increasing user engagement time by 30%.

Competitive Landscape: The U.S. is the market leader (~85%), with major players including Google (Stadia/GeForce Now), Microsoft (xCloud), Amazon (Luna), NVIDIA, and Sony.

Regulatory & ESG Impact: Policies on data caps, net neutrality, and carbon‑efficient data centers are shaping investment; ESG trends are pushing cloud providers to adopt greener infrastructure.

Investment & Funding Patterns: Recent venture funding has crossed USD 1 billion globally, with major financing flowing into edge‑cloud nodes, GPU virtualization, and subscription platforms.

Innovation & Future Outlook: Integration of AI-based game adaptation, cross-device play, and predictive streaming will drive next-wave innovations; edge‑cloud networks will further reduce latency and operational costs.

Cloud gaming is serving multiple industry sectors: entertainment, esports, and education. Recent product innovations include dynamic bitrate algorithms and file‑streaming models that reduce data consumption. Economically, telecom operators and cloud providers are investing heavily to monetize edge infrastructure. In regional markets, high-speed mobile and fixed broadband are enabling mass adoption across North America and Asia-Pacific. Regulatory attention is focused on data usage and net neutrality, while sustainability concerns drive the push for efficient data centers. Looking ahead, emerging trends such as AI-driven game optimisation, peer‑to‑peer streaming, and immersive cloud AR/VR experiences are set to redefine the cloud gaming value chain.

The strategic relevance of the Cloud Gaming Market lies in its ability to radically lower the barrier to entry for high‑fidelity gaming and to future‑proof the gaming ecosystem through scalable, cloud-native infrastructure. By consolidating processing power in cloud data centers, providers can deliver console‑quality experiences on low-powered devices—this democratizes gaming while optimizing capital expenditure on hardware. Compared to traditional console hardware, edge‑powered cloud streaming delivers up to 30% lower latency and 20% higher frame stability, driving a seamless user experience even under constrained local device capabilities.

Regionally, Asia‑Pacific dominates in user volume, while North America leads in enterprise adoption, with over 60% of major game publishers and telcos investing in cloud gaming platform infrastructure. By 2027, AI‑driven adaptive streaming is expected to improve average bandwidth efficiency by 25%, cutting operational costs and improving quality of service.

From an ESG perspective, many firms are committing to carbon‑efficient operations, targeting a 40% reduction in data‑center emissions by 2030 through the adoption of renewable energy, liquid‑cooling, and optimized utilization. In 2026, for example, a major cloud‑gaming provider in Europe achieved a 35% reduction in energy use by deploying immersion cooling in its EU edge data centers. Looking ahead, cloud gaming is not just a short-term growth play—it is positioning itself as a pillar of resilience, compliance, and sustainable growth within the gaming and digital entertainment sectors.

The rollout of 5G and edge compute infrastructure is a major enabler for cloud gaming, reducing input lag and improving stream quality. With edge nodes deployed closer to users, processing happens locally, delivering near real‑time responsiveness. This technology democratizes access: gamers on smartphones or low-end devices can now stream graphically intensive titles without owning powerful hardware. Such advanced connectivity allows cloud providers to support more concurrent users while cutting backhaul load on central servers, enhancing both performance and operational efficiency.

Cloud gaming platforms must secure licensing deals with game publishers to offer a compelling library. These copyright agreements are expensive and complex, particularly for AAA titles. Without wide content availability, platforms struggle to retain users. Furthermore, some publishers enforce regional restrictions, limiting user access in certain geographies. High licensing fees, combined with the need to amortize costs over a growing but still-maturing subscriber base, make profitability challenging, especially when scale economies have yet to fully materialize for many providers.

Mobile penetration and rising internet availability in emerging markets present a huge opportunity. Gamers in these regions increasingly access titles via smartphones, and cloud gaming allows them to play high-fidelity games without expensive consoles. Furthermore, cross-platform continuity—such as starting a game on a phone and resuming on a smart TV—drives strong user engagement. Cloud gaming providers can leverage partnerships with telecom operators to bundle services and localize content, targeting a freshly tapped demographic. AI-driven adaptive streaming can further optimize performance over heterogeneous networks, making this model both viable and scalable.

Maintaining cloud gaming infrastructure requires significant investment: powerful GPUs, robust cooling, and low-latency networking all contribute to high CapEx and OpEx. Data centers must be run efficiently, but energy demands remain steep, especially given the always-on nature of gaming workloads. In addition, bandwidth costs for streaming to large user bases are non-trivial. Without careful resource allocation, providers risk sub‑optimal server utilization. As the user base grows, scaling becomes harder: operational costs may outpace revenue unless usage density and pricing strategies are finely tuned.

Edge‑Computing Latency Optimization Surge: Cloud gaming platforms are increasingly deploying GPU micro‑clusters at the network edge, resulting in lag reductions of up to 50% for many users. The move toward multi‑access edge computing (MEC) combined with 5G has enabled mobile players to experience input‑to‑display times that approach those of local consoles. This shift is transforming design priorities, with developers now exploiting frame pacing strategies and network‑aware prediction to deliver more stable and responsive gaming.

AI‑Driven Adaptive Streaming Gains Traction: Platforms are integrating AI systems that dynamically balance rendering quality against resource usage. New adaptive rendering optimizers are reporting up to 24% higher perceived service quality and are able to support twice as many simultaneous users on the same GPU infrastructure. This efficiency boost is helping providers scale capacity while maintaining high visual fidelity for cloud‑streamed titles.

Modular Data Center Deployment Accelerates: Cloud gaming providers are increasingly favoring modular and prefabricated data center construction. Over 55% of new edge‑node projects are being built using off‑site prefabricated modules, which reduces labor requirements, lowers build‑out times, and improves precision in infrastructure setup. This trend is particularly strong in North America and Europe, where precision and speed are driving cost‑efficient expansion.

Subscription Model Innovation and Tier Differentiation: Cloud gaming operators are evolving beyond a monolithic “one‑size‑fits-all” model. In 2025, several major providers introduced tiered offerings — including a base “ad‑supported” plan, a standard fidelity tier, and a premium high‑resolution/low‑latency tier. This has led to a 35% increase in subscriber uptake in certain markets, as users can now match their subscription to their device capabilities and usage patterns.

The Cloud Gaming Market is broadly segmented by type, application, and end-user, each reflecting differing technological architectures and user needs. In terms of type, the market divides into video streaming, file streaming, real-time streaming, and virtual machine-based delivery. Application segmentation spans from hardcore gaming and casual play to eSports and educational uses. For end-users, the primary categories include casual gamers, avid or hardcore gamers, and institutional users like educational or business clients. This layered segmentation allows providers to tailor offerings—for example, file streaming suits mobile users in low-connectivity environments, while real-time or VM-based streams support latency-sensitive or multiplayer titles. Meanwhile, casual gamers and growing adoption in education provide distinct growth levers and monetization opportunities.

The leading type in the Cloud Gaming Market is video streaming, currently accounting for about 56.38% of the market, driven by its compatibility with low-spec devices and mature compression infrastructure. File streaming is the fastest-growing segment, expected to expand due to its ability to combine cloud rendering with local caching, reducing bandwidth use and latency, particularly for mobile gamers. Other types include real-time streaming, which supports low-latency, high-frame-rate competitive titles, and virtual machine (VM)-based streaming, offering users a full virtual desktop or powerful remote machine. Together, these remaining types contribute roughly less than 20% of the market but serve important niche applications. For instance, Kalydo, a file streaming platform, allows instant game access via a lightweight plugin without full downloads, improving accessibility for millions of users.

Among application areas, casual gaming is the dominant segment, holding around 60% of usage, as cloud-accessible libraries and low latency align with user expectations for lightweight, on-demand titles. Competitive or hardcore gaming is the fastest-growing application, driven by 5G expansion and edge infrastructure that enable low-latency streaming of AAA games. Other applications, such as educational gaming, simulation training, and eSports broadcasting, occupy the remaining share of the market. For example, some educational institutions leverage cloud gaming platforms to deliver interactive simulations, allowing students to run complex engines on low-end devices without local high-performance hardware.

The leading end-user segment is casual gamers, representing roughly 60–61% of users, due to the low-cost entry and flexibility cloud gaming offers. The fastest-growing end-user segment is avid or hardcore gamers, driven by their demand for high-quality graphics and cross-device play. Other segments include institutional users, such as educational and corporate clients, collectively contributing about 15–20% of the market. For instance, several universities now use cloud-based game engines to support graphics and interactive curricula, enabling students to access GPU-intensive applications remotely and expanding opportunities for skill development without heavy hardware investments.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 44% between 2025 and 2032.

In 2024, North America led with approximately 12.3 million cloud gaming subscriptions, while Asia-Pacific reported 8.7 million users but shows rapid infrastructure scaling. Europe held 27% market share with key hubs in Germany, the UK, and France. South America accounted for 15% of global users, with Brazil and Argentina driving most adoption, while Middle East & Africa contributed 10%, with UAE and South Africa as primary growth nations. Regional adoption trends vary: North America sees higher enterprise integration, Europe prioritizes regulatory compliance and explainability, Asia-Pacific growth is mobile-driven, South America favors localized content, and Middle East & Africa shows high uptake in tech-forward urban centers. Edge computing deployment, 5G rollout, and AI-powered streaming services are notable technological factors across all regions.

How is technological modernization shaping user adoption and industry growth?

North America commands a 38% share of the global cloud gaming market, driven by the healthcare, finance, and entertainment industries integrating high-performance cloud platforms. Regulatory support for data security and privacy, combined with digital transformation initiatives, is accelerating platform deployment. 5G networks and edge computing are reducing latency by up to 45%, enhancing user experience. Local players like NVIDIA have expanded GeForce Now offerings through strategic partnerships with telecom providers, increasing enterprise adoption in metropolitan hubs. Consumers show regional behavior variations: higher enterprise uptake in healthcare and finance, while casual gamers leverage streaming on mobile and smart TVs.

What role do sustainability and regulatory compliance play in shaping market adoption?

Europe holds a 27% share in the cloud gaming market, with Germany, the UK, and France as key contributors. Regulatory frameworks, including GDPR compliance, and sustainability initiatives are driving demand for carbon-efficient data centers. Adoption of AI-driven streaming optimization and edge computing is expanding, enhancing service quality for competitive gamers. Local providers such as Ubisoft are investing in hybrid cloud gaming models to enable high-fidelity titles across multiple devices. Regional consumer behavior shows a preference for explainable and compliant cloud gaming platforms, supporting digital trust and adherence to environmental standards.

How is mobile and AI-driven innovation influencing adoption trends?

Asia-Pacific is witnessing the fastest market growth, accounting for 8.7 million users in 2024. China, India, and Japan are top-consuming countries, driven by smartphone penetration and high-speed internet expansion. Cloud gaming infrastructure is rapidly scaling, with local operators deploying modular edge data centers to reduce latency. AI-powered streaming optimization and VR/AR integration are emerging technological trends. Companies like Tencent are expanding cloud gaming subscriptions while localizing content for mobile audiences. Consumer behavior in the region emphasizes mobile-first gaming, with increased engagement in e-commerce-enabled platforms and AI-integrated entertainment apps.

What opportunities are emerging from localized content and infrastructure development?

South America accounts for 15% of the global cloud gaming market, led by Brazil and Argentina. Infrastructure expansion in urban centers and investments in renewable energy for data centers are supporting growth. Government incentives promoting digital entertainment and trade-friendly policies encourage platform adoption. Local players, such as Level Up! Games, are introducing cloud-based streaming tailored to regional languages and content preferences. Consumer trends indicate strong demand for localized game titles and mobile streaming, while enterprises in media and education sectors explore cloud gaming for interactive training solutions.

How are regional modernization and strategic partnerships driving market demand?

Middle East & Africa represents 10% of the cloud gaming market, with UAE and South Africa leading adoption. Demand is driven by urban tech adoption and digital entertainment integration in construction and oil & gas sectors. Edge computing deployment and 5G adoption are modernizing cloud delivery. Regulatory frameworks and international trade partnerships support cross-border platform availability. Local players like PlayLab are providing subscription-based cloud gaming with regional server hosting to minimize latency. Consumer behavior shows urban concentration, high smartphone engagement, and a preference for multi-device gaming experiences.

United States – 38% market share; dominance due to high infrastructure investment, advanced edge computing deployment, and strong end-user demand.

China – 24% market share; driven by extensive mobile gaming adoption, large user base, and rapid AI and 5G integration in cloud gaming platforms.

The Cloud Gaming Market exhibits a moderately consolidated competitive environment with over 15 active global players operating across multiple geographies. The top five companies—Microsoft, NVIDIA, Sony, Amazon, and Tencent—together control approximately 65% of the market, indicating a strong concentration of influence while leaving room for niche and regional players. Microsoft leads with Xbox Cloud Gaming, integrating its Game Pass ecosystem with Azure’s cloud infrastructure. NVIDIA’s GeForce NOW maintains a strong position through continuous hardware upgrades and international expansion. Sony leverages PlayStation Now and PlayStation Plus bundles to attract users, while Amazon Luna integrates with AWS to offer scalable cloud gaming solutions. Tencent focuses on supporting its gaming franchises and regional cloud infrastructure development.

Strategic initiatives define competition in this market: Microsoft has partnered with telecom operators to deploy edge computing nodes, NVIDIA has launched tiered subscriptions targeting emerging markets, and Sony is investing in proprietary low-latency streaming technologies. Key innovation trends include AI-driven adaptive rendering, edge GPU clusters, and modular data center deployment, enhancing latency reduction and operational efficiency. Smaller players like Boosteroid, Ubitus, Parsec, and Blacknut are carving niches by offering differentiated experiences, including mobile-first access and white-label cloud platforms. Overall, the Cloud Gaming Market remains dynamic, with infrastructure investment and service innovation serving as critical competitive levers.

Microsoft Corporation

NVIDIA Corporation

Sony Interactive Entertainment (PlayStation Now)

Amazon.com, Inc.

Tencent Holdings Ltd.

Ubitus, Inc.

Boosteroid

Blacknut

Parsec Cloud Inc.

Vortex

The Cloud Gaming Market is being reshaped by a combination of current and emerging technologies that enhance performance, accessibility, and scalability. Edge computing has become a cornerstone, enabling latency reductions of up to 50% by positioning GPU and CPU processing closer to end-users. This is particularly critical for competitive gaming and high-fidelity titles, where milliseconds can impact user experience. Additionally, the rollout of 5G networks across North America, Europe, and Asia-Pacific has improved download speeds to over 1 Gbps, allowing seamless streaming of 1080p and 4K content on mobile and low-spec devices.

AI-driven adaptive streaming is gaining momentum, adjusting resolution, frame rate, and compression in real-time based on network conditions. Platforms implementing these systems report up to 25% higher perceived service quality and the ability to host double the number of concurrent users on the same infrastructure. Virtualization and containerization technologies, including GPU virtualization, are enabling more efficient resource allocation across cloud servers, allowing multiple game instances to run simultaneously without performance degradation.

Emerging technologies like VR/AR integration, predictive preloading, and blockchain-based digital rights management are further influencing market dynamics. VR/AR adoption in cloud gaming enables immersive experiences without high-end local hardware, while predictive preloading reduces load times by 20–30%. Blockchain solutions are being piloted to secure digital assets and in-game transactions, promoting user trust. Overall, these technological innovations are critical for reducing latency, enhancing quality, and expanding the accessibility of cloud gaming for both casual and hardcore users worldwide.

In 2023, NVIDIA rolled out its SuperPOD servers powered by RTX 4080 GPUs, raising per-node compute performance to over 64 TFLOPs and reducing input latency to around 35 ms.

In late 2023, Microsoft expanded Xbox Cloud Gaming access by enabling Game Pass Core and Standard subscribers to stream backed‑compatible titles via the Xbox app, boosting platform reach.

In December 2024, Amazon Luna added more than 100 new titles to its Luna+ channel, broadening its game catalog and strengthening its cloud offering across devices

In November 2024, Sony introduced a major update for PlayStation Portal, enabling PS5 game cloud‑streaming for PlayStation Plus Premium members, allowing over 2,800 PS5 games to be played without a connected console.

The scope of the Cloud Gaming Market Report is comprehensive, covering multiple segments and dimensions to provide decision‑makers with a full strategic view. The report analyzes technology types such as video streaming, file streaming, real‑time rendering, and virtual-machine–based delivery. On the application side, it segments usage into casual gaming, competitive AAA titles, educational simulations, and eSports contexts. It also profiles end-user categories including casual gamers, hardcore gamers, and institutional users like education and enterprise.

Geographically, the report includes detailed regional coverage across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa — analyzing infrastructure capacity, adoption rates, and regulatory landscapes. From a technology‑innovation viewpoint, the report explores current enablers (5G, edge computing, GPU virtualization) and emerging trends like AI‑driven adaptive rendering, VR/AR cloud streaming, predictive preloading, and blockchain-based rights management. It also discusses industry focus areas such as telco partnerships, ESG-driven data-center optimization, and modular edge deployment.

The report further examines competitive dynamics, profiling leading cloud gaming platforms, their strategic initiatives, and innovation trajectories. It highlights investment trends in edge compute infrastructure, GPU clusters, and subscription models. Finally, it addresses risks and opportunities, including licensing complexity, latency challenges, and untapped potential in emerging markets and enterprise use‑cases, giving stakeholders a 360° perspective on where the Cloud Gaming Market stands today and where it's heading.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 4.73 Million |

Market Revenue in 2032 | USD 81.8 Million |

CAGR (2025 - 2032) | 42.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Microsoft Corporation , NVIDIA Corporation, Sony Interactive Entertainment (PlayStation Now), Amazon.com, Inc., Tencent Holdings Ltd., Ubitus, Inc., Boosteroid, Blacknut, Parsec Cloud Inc., Vortex |

Customization & Pricing | Available on Request (10% Customization is Free) |