Reports

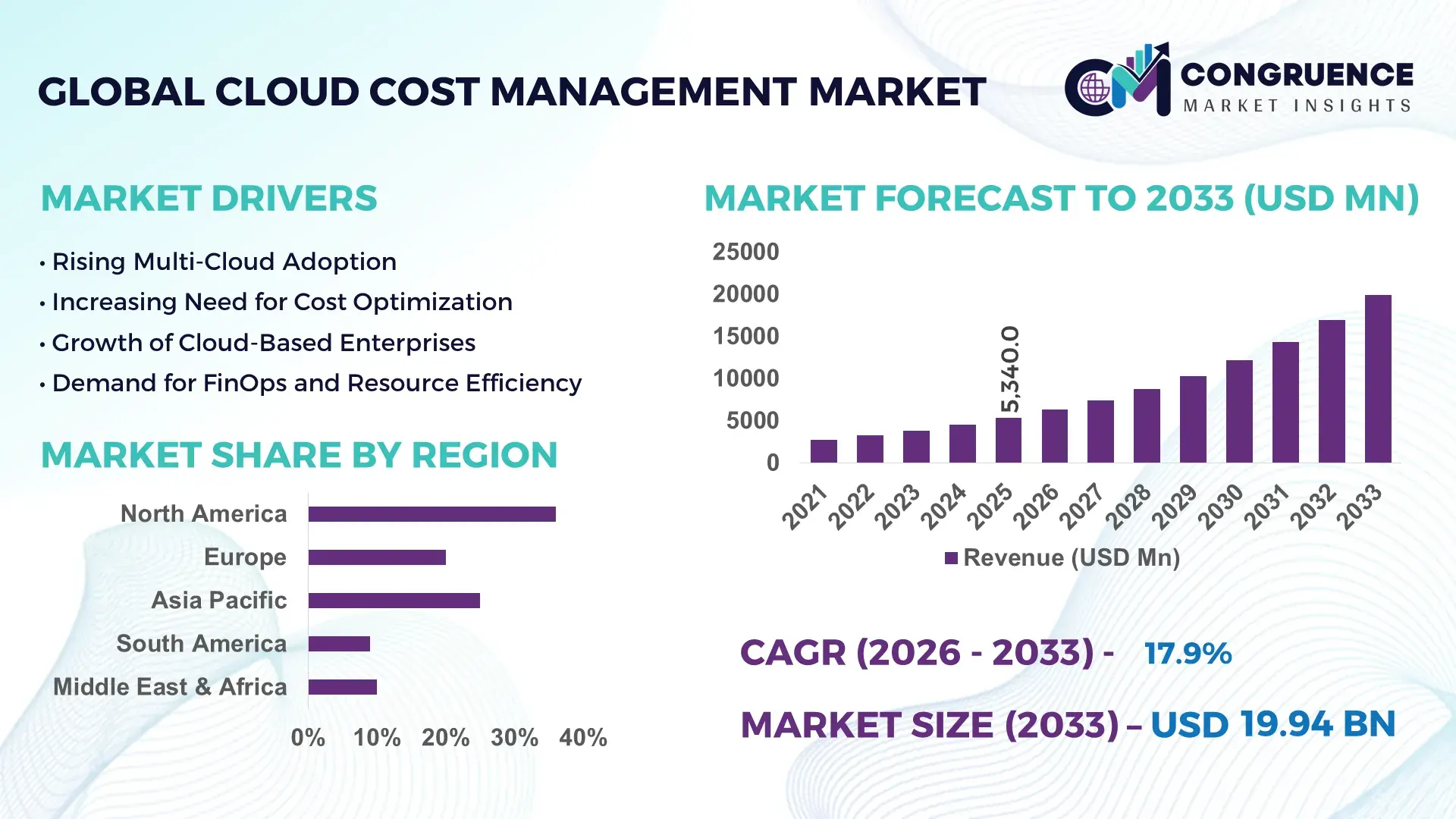

The Global Cloud Cost Management Market was valued at USD 5340 Million in 2025 and is anticipated to reach a value of USD 19936.62 Million by 2033 expanding at a CAGR of 17.9% between 2026 and 2033. Enterprise FinOps adoption, AI-driven workload optimization, and rising multi-cloud governance mandates are accelerating deployment of advanced cloud cost management platforms across BFSI, telecom, healthcare, and large-scale SaaS environments.

The United States dominates the global cloud cost management market with nearly 38% platform adoption share, supported by hyperscale cloud infrastructure, over USD 90 billion in enterprise cloud optimization spending, and strong FinOps integration across banking and AI workloads in 2026. Compared with Germany’s 11% enterprise deployment concentration in regulated manufacturing and automotive sectors, U.S. organizations report 27% faster cloud resource utilization tracking. Ongoing geopolitical pressure on data sovereignty and cross-border compliance is further increasing regional cloud expenditure visibility requirements.

Organizations prioritizing automated cloud financial governance, workload rightsizing, and real-time usage analytics are gaining measurable operational control and stronger infrastructure budgeting resilience in competitive digital economies.

Market Size & Growth: USD 5340 Million in 2025 to USD 19936.62 Million by 2033 at 17.9% CAGR, driven by enterprise FinOps automation and multi-cloud expansion.

Top Growth Drivers: AI workload optimization demand rose 34%, Kubernetes cost visibility adoption increased 29%, and hybrid cloud governance deployment expanded 31% in 2026.

Short-Term Forecast: By 2027, enterprises using automated cloud cost platforms are projected to reduce infrastructure overspending by 22% and improve workload efficiency by 26%.

Emerging Technologies: AI-based anomaly detection, predictive analytics, and container cost allocation tools improved cloud resource accuracy by nearly 30% across advanced enterprise environments.

Regional Leaders: North America exceeds USD 7.8 billion with FinOps maturity growth, Asia-Pacific approaches USD 5.2 billion through hyperscale expansion, and Europe crosses USD 4.6 billion under stricter compliance mandates.

Consumer/End-User Trends: Around 64% of large enterprises actively monitor multi-cloud spending daily, while 48% integrate cloud financial analytics directly into DevOps workflows.

Pilot/Case Example: In 2026, a global telecom operator reduced idle cloud compute costs by 33% after deploying AI-driven workload scheduling and automated budgeting controls.

Competitive Landscape: Leading vendors collectively control nearly 42% market share, with competition intensifying among enterprise cloud optimization, observability, and FinOps platform providers.

Regulatory & ESG Impact: Carbon-aware cloud allocation strategies lowered infrastructure energy waste by 18% as European compliance frameworks tightened operational reporting standards.

Investment & Funding: More than USD 4.3 billion entered cloud governance, observability, and optimization platforms through enterprise partnerships and strategic AI infrastructure investments.

Innovation & Future Outlook: Real-time autonomous cloud optimization and policy-driven financial orchestration are reshaping high-growth enterprise infrastructure management strategies globally.

Cloud cost management solutions are expanding rapidly across AI infrastructure, containerized workloads, SaaS governance, and hybrid cloud operations as enterprises push for tighter financial accountability. Advanced automation tools now improve cloud spend visibility by nearly 28% while reducing unused compute allocation in large-scale environments. Rising regional data localization policies and cross-border compliance requirements are also increasing demand for centralized cloud financial governance, setting the stage for deeper strategic optimization initiatives across global enterprises.

Cloud cost management platforms have become strategically critical as enterprises shift from cloud expansion to cloud efficiency, governance, and workload accountability. Rising AI infrastructure consumption, stricter data sovereignty frameworks, and enterprise-wide FinOps adoption are reshaping investment priorities across digital infrastructure ecosystems. In 2026, nearly 62% of large enterprises operate across three or more cloud environments, increasing demand for centralized spending visibility and automated optimization. Infrastructure modernization programs in the United States and Japan are further accelerating deployment of policy-based cloud financial management systems within telecom, BFSI, and healthcare sectors.

AI-enabled cloud cost optimization tools now reduce idle compute expenditure by nearly 30% compared with legacy spreadsheet-based monitoring models while improving workload allocation accuracy by 24%. North America leads in advanced automation deployment, whereas India and Southeast Asia are scaling rapidly through cloud-native startups and managed service partnerships. Over the next two years, enterprises are expected to increase automated budget enforcement integration by more than 35% as GPU-intensive AI workloads continue expanding operational complexity.

A global retail enterprise in 2026 integrated Kubernetes cost analytics with real-time workload scheduling, lowering cross-cloud resource waste by 21% within nine months. Vendors are responding through hyperscaler alliances, AI optimization investments, and FinOps-as-a-service expansion models. Organizations capable of combining cloud governance, automation, and predictive financial intelligence will secure stronger operational resilience and long-term infrastructure competitiveness.

Rapid enterprise migration toward AI-intensive and multi-cloud environments is accelerating demand for advanced cloud cost management solutions. In 2026, over 58% of global enterprises increased FinOps budget allocation to improve cloud utilization efficiency, while automated workload optimization reduced unnecessary compute spending by nearly 27%. Large-scale AI model training environments in the United States and South Korea are significantly increasing GPU resource monitoring requirements, forcing enterprises to adopt real-time cloud financial governance platforms. This operational pressure is driving partnerships between cloud observability providers and hyperscale infrastructure companies to deliver integrated analytics and predictive spending controls. Companies deploying automated rightsizing and container cost allocation tools are achieving faster budgeting cycles and stronger infrastructure accountability, creating measurable operational advantages in high-consumption digital ecosystems.

Fragmented cloud billing structures and inconsistent usage visibility continue limiting deployment efficiency across enterprise environments. Nearly 41% of organizations operating across multiple cloud providers report delayed cost attribution accuracy, while 33% struggle with workload-level financial tracking inside containerized infrastructures. Germany’s manufacturing sector faces additional compliance-related reporting burdens due to evolving data governance regulations, increasing operational auditing costs for cloud-intensive environments. Vendor-specific pricing architectures and incompatible monitoring frameworks also complicate unified cloud financial management strategies. To reduce exposure, enterprises are increasingly adopting third-party observability platforms, negotiating longer-term infrastructure contracts, and localizing sensitive workloads within compliant cloud zones. Companies unable to standardize cross-cloud cost governance risk lower infrastructure efficiency, inconsistent budget forecasting, and weakened operational scalability during AI-driven workload expansion.

Autonomous cloud optimization platforms are creating high-value opportunities across regulated and compute-intensive industries. AI-driven anomaly detection systems now improve cloud utilization efficiency by nearly 32%, while predictive budgeting engines reduce overprovisioned infrastructure allocation by approximately 25%. In India, financial institutions and digital commerce operators are accelerating deployment of policy-based cloud governance frameworks to manage rapidly growing transaction environments. Emerging carbon-aware workload orchestration technologies are also gaining traction as enterprises target infrastructure energy reduction and ESG-aligned operations. Vendors are investing in industry-specific FinOps modules, sovereign cloud partnerships, and AI-integrated analytics ecosystems to strengthen enterprise adoption. A major untapped opportunity lies in mid-sized enterprises transitioning from manual cloud monitoring to automated governance systems, where operational savings and deployment visibility remain significantly underpenetrated.

Scaling cloud cost management systems across hybrid architectures remains a major operational challenge for enterprises managing distributed workloads. Around 46% of organizations report integration complexity between cloud observability, security, and financial governance platforms, while nearly 39% face shortages of skilled FinOps and cloud optimization professionals. Japan’s advanced manufacturing and automotive sectors are experiencing deployment delays due to legacy infrastructure dependencies and fragmented workload orchestration frameworks. Increasing cybersecurity scrutiny surrounding cloud financial telemetry and API-level integrations is also raising long-term operational risk exposure. Enterprises are responding through internal cloud governance academies, AI-assisted automation investments, and strategic partnerships with managed cloud service providers. Companies that fail to standardize scalable optimization frameworks risk inconsistent cloud governance, rising infrastructure inefficiencies, and weakened competitiveness in AI-driven digital operating environments.

• AI-Led Spend Governance Expansion AI-driven cloud financial governance platforms are replacing static monitoring systems as enterprises prioritize real-time optimization and predictive workload control. In 2026, nearly 57% of Fortune 1000 companies integrated AI-based anomaly detection into cloud budgeting workflows, reducing unnecessary compute allocation by 26%. U.S.-based telecom operators are restructuring cloud operations around automated policy engines to manage rising GPU infrastructure consumption. Vendors are accelerating partnerships with hyperscale cloud providers to deliver integrated FinOps automation and faster cross-platform visibility.

• Kubernetes Cost Visibility Acceleration Containerized infrastructure management is becoming a central operational trend as Kubernetes deployments expand across banking, SaaS, and digital commerce environments. More than 49% of enterprises now track container-level cloud expenditure compared with 31% two years earlier, improving workload allocation efficiency by 22%. Germany’s industrial cloud modernization programs are increasing demand for granular cost attribution tools inside hybrid architectures. Companies are responding through embedded observability analytics, unified dashboards, and automated resource rightsizing frameworks to improve deployment consistency and operational transparency.

• Carbon-Aware Cloud Optimization Rise Sustainability-linked cloud optimization is moving into mainstream enterprise procurement strategies as regulatory reporting pressure intensifies. In Japan and France, enterprises deploying carbon-aware workload scheduling reduced infrastructure energy waste by nearly 18% while improving server utilization efficiency by 14%. Cloud cost management vendors are embedding emissions tracking and ESG-linked financial analytics into operational dashboards. A less visible shift involves procurement teams integrating sustainability metrics directly into cloud vendor selection, forcing providers to redesign workload placement and data center utilization strategies.

• FinOps Integration Across Departments Cloud financial management is expanding beyond IT teams into procurement, finance, and operations departments to strengthen enterprise-wide infrastructure accountability. Around 61% of large enterprises now run cross-functional FinOps governance models, accelerating budget response time by 24% and improving forecasting accuracy by 19%. India’s digital banking and e-commerce sectors are rapidly scaling centralized cloud governance programs amid rising transaction workloads. Companies are increasing investments in integrated ERP-cloud analytics platforms and workforce training to align operational spending decisions with real-time infrastructure performance data.

Cost Optimization remains the leading segment within the cloud cost management market due to its direct impact on infrastructure efficiency, workload performance, and operational budgeting control. In 2026, nearly 46% of enterprises prioritized automated optimization tools to reduce idle compute spending and improve resource utilization across multi-cloud environments. Organizations deploying AI-driven optimization engines reported up to 28% lower unnecessary cloud expenditure compared with manual governance models. Cost Monitoring continues to hold strong adoption across mature enterprises requiring real-time visibility and compliance tracking, while Billing Analytics is gaining traction in sectors managing highly distributed cloud consumption patterns.

Budget Management is emerging as the fastest-growing segment as enterprises integrate cloud spending directly into financial planning and operational forecasting workflows. Resource Management platforms are also expanding rapidly in telecom and AI-intensive environments where workload balancing and GPU allocation efficiency have become operational priorities. Vendors are responding through predictive analytics integration, automated policy controls, and cloud-native dashboard expansion. Investment priorities are increasingly shifting toward unified optimization suites capable of combining monitoring, allocation, and financial governance within a single operational framework.

Multi-Cloud Management dominates application demand as enterprises increasingly operate across complex distributed cloud ecosystems requiring centralized governance and cost visibility. In 2026, nearly 63% of large enterprises managed workloads across three or more cloud platforms, increasing deployment demand for unified financial monitoring and optimization systems. Organizations using integrated multi-cloud governance tools improved cross-platform resource visibility by 29% while reducing redundant provisioning activities by approximately 21%. IT Cost Control remains widely adopted across mature enterprises focused on budgeting discipline and infrastructure accountability within hybrid operating environments.

Usage Analytics is emerging as the fastest-growing application as AI workloads, container orchestration, and real-time digital services intensify demand for granular cloud consumption intelligence. Resource Allocation platforms are also expanding rapidly within telecom and digital commerce sectors where automated workload balancing has become operationally critical. Financial Planning tools are evolving from static reporting systems into predictive infrastructure budgeting platforms integrated with enterprise ERP ecosystems. Companies are accelerating automation deployment, API integration, and AI-assisted forecasting capabilities to strengthen operational efficiency and reduce unpredictable cloud expenditure volatility.

IT and Telecom remains the dominant end-user segment due to extensive cloud infrastructure dependency, large-scale distributed workloads, and continuous digital service expansion. In 2026, telecom and SaaS enterprises accounted for nearly 39% of enterprise cloud optimization deployments as rising data traffic and AI-driven operations intensified infrastructure monitoring requirements. Companies within this segment achieved up to 27% faster workload allocation efficiency through automated cloud governance systems. BFSI continues expanding strongly as regulatory compliance, transaction-intensive workloads, and cybersecurity integration increase demand for real-time cloud financial visibility and operational control.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and digital health providers modernize patient data infrastructure and AI-assisted diagnostics environments. Retail enterprises are scaling usage analytics and dynamic workload management platforms to support omnichannel commerce operations, while manufacturing firms increasingly deploy resource optimization tools within connected industrial systems. Government agencies are also strengthening adoption through sovereign cloud modernization initiatives and compliance-focused infrastructure governance programs. Vendors are responding with industry-specific pricing models, verticalized analytics platforms, and strategic partnerships tailored to regulated operational environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.6% between 2026 and 2033.

North America continues leading the cloud cost management market through mature hyperscale cloud ecosystems, advanced FinOps implementation, and large-scale enterprise cloud optimization programs. The region represented nearly 38% of global deployment activity in 2025, driven by strong adoption across telecom, BFSI, SaaS, and AI infrastructure environments. Enterprises are increasingly deploying automated workload optimization systems that improve infrastructure utilization efficiency by nearly 25% while reducing unnecessary compute allocation. Strategic partnerships between enterprise software providers and hyperscale cloud operators are accelerating deployment of integrated budgeting analytics, container visibility, and AI-assisted governance platforms. Canada and the United States are also strengthening sovereign cloud modernization initiatives to improve operational transparency and compliance-driven cloud management capabilities.

United States Market Outlook: The United States remains the largest operational hub for cloud cost management deployment due to extensive enterprise cloud infrastructure and rising AI workload consumption. More than 64% of Fortune 1000 companies actively use centralized FinOps governance frameworks integrated across multi-cloud environments. Telecom operators and digital commerce companies are investing heavily in predictive budgeting systems, GPU allocation optimization, and AI-based anomaly detection to improve infrastructure efficiency. Strong hyperscaler presence and enterprise cloud modernization programs continue reinforcing the country’s technology leadership.

Europe is strengthening cloud cost management adoption through stricter data governance requirements, sustainability-focused infrastructure modernization, and enterprise-wide compliance integration. The region accounted for approximately 26% of enterprise cloud governance deployments in 2025, led by Germany, France, and the United Kingdom. Organizations are increasingly implementing carbon-aware workload orchestration systems that reduce infrastructure energy waste by nearly 18% while improving workload allocation visibility. Regulatory frameworks focused on operational resilience and sovereign data control are driving demand for centralized financial governance platforms. Technology vendors are expanding localized deployment partnerships and sovereign cloud integration strategies to address enterprise concerns regarding compliance, workload transparency, and operational accountability.

Germany Market Outlook: Germany leads the European market through its advanced industrial digitalization ecosystem and strong enterprise cloud modernization programs. Nearly 48% of large manufacturing companies now deploy hybrid cloud governance systems integrated with operational analytics and cybersecurity frameworks. Automotive and industrial engineering enterprises are increasingly using cloud optimization technologies to support AI-driven simulation environments and connected production systems. Germany’s enterprise compliance standards and industrial automation investments continue strengthening demand for advanced cloud financial governance platforms.

Asia-Pacific is emerging as the fastest-scaling market due to aggressive cloud-native enterprise adoption, expanding digital commerce ecosystems, and accelerating AI infrastructure deployment. The region represented nearly 24% of global cloud governance implementation activity in 2025, with India, China, Japan, and Singapore leading deployment momentum. Enterprises across banking, telecom, and e-commerce sectors are rapidly adopting automated cloud optimization systems to manage rising multi-cloud complexity and transaction-intensive workloads. Multiple hyperscale infrastructure projects launched during 2026 increased enterprise cloud workload capacity by more than 30%, intensifying demand for predictive budgeting and real-time resource allocation platforms. Vendors are strengthening regional partnerships and localized service ecosystems to support rapidly expanding enterprise cloud modernization requirements.

India Market Outlook: India is becoming a strategic growth center due to rapid SaaS expansion, large-scale digital public infrastructure, and increasing enterprise cloud adoption. More than 52% of large digital enterprises now utilize automated cloud monitoring and optimization systems across multi-cloud environments. BFSI and e-commerce companies are accelerating investment in AI-based cloud governance platforms to improve workload scalability and transaction efficiency. Expanding data center investments and national digital transformation initiatives continue supporting long-term enterprise cloud management deployment.

South America is witnessing steady cloud cost management adoption as enterprises modernize legacy infrastructure and expand cloud-enabled service delivery operations. The region contributed nearly 7% of global enterprise cloud governance deployment activity in 2025, with Brazil and Chile leading modernization initiatives. Financial institutions and telecom operators are increasingly implementing automated cost monitoring systems to improve workload efficiency by approximately 19% and strengthen operational visibility. However, uneven cloud infrastructure maturity and inconsistent connectivity standards continue limiting deployment scalability across smaller enterprise environments. Technology providers are responding through localized support partnerships, governance training programs, and cloud optimization services tailored to mid-sized enterprises and regulated sectors.

Brazil Market Outlook: Brazil dominates the regional market through its large banking ecosystem, expanding enterprise cloud infrastructure, and accelerating digital transformation initiatives. Nearly 44% of major enterprises in the country operate hybrid cloud environments requiring centralized workload governance and financial monitoring capabilities. Banking and telecom companies are increasingly deploying AI-enabled cloud optimization platforms to manage rising transaction processing and cybersecurity integration requirements. Expanding regional data center investments continue improving enterprise cloud deployment capacity across the country.

The Middle East & Africa market is expanding steadily through government-backed digital transformation programs, sovereign cloud infrastructure investments, and enterprise modernization initiatives. The region represented approximately 5% of global cloud governance deployment activity in 2025, with the United Arab Emirates and Saudi Arabia leading operational adoption. Large-scale smart city programs and public-sector infrastructure modernization projects are increasing demand for centralized cloud financial management and workload optimization systems. Enterprises implementing AI-assisted resource monitoring platforms improved infrastructure allocation efficiency by nearly 17% across telecom and government environments. Vendors are strengthening compliance-focused deployment partnerships and localized service ecosystems to support rapidly evolving digital infrastructure requirements.

United Arab Emirates Market Outlook: The United Arab Emirates is positioning itself as a regional cloud governance hub through advanced digital infrastructure investments and enterprise modernization initiatives. More than 46% of large enterprises in the country have integrated multi-cloud governance systems into financial planning and operational workflows. Banking, aviation, and government organizations are increasingly investing in automated cloud optimization platforms to improve workload visibility and compliance management. Expanding hyperscale data center capacity and national AI adoption strategies continue accelerating enterprise cloud governance deployment.

The cloud cost management market is highly competitive, led by VMware, Flexera, IBM, Apptio, CloudHealth, and Harness, while hyperscaler-native optimization platforms compete aggressively against independent FinOps and observability vendors. The top five players collectively account for nearly 54% of enterprise deployments through integrated automation, predictive analytics, and multi-cloud governance capabilities. Competition is primarily based on AI-driven optimization accuracy, workload visibility depth, deployment speed, and enterprise integration flexibility. Advanced automation platforms are reducing idle cloud expenditure by nearly 30%, while integrated financial governance dashboards improve infrastructure budgeting efficiency by approximately 24%.

Companies are expanding through hyperscaler partnerships, acquisition-led platform consolidation, and industry-specific optimization suites targeting telecom, BFSI, healthcare, and SaaS environments. Independent vendors are increasingly differentiating through GPU workload optimization, Kubernetes cost analytics, and carbon-aware cloud governance capabilities. Rising integration complexity, enterprise compliance requirements, and long deployment cycles are creating strong entry barriers for emerging participants. Companies capable of delivering scalable automation, predictive financial intelligence, and seamless ecosystem interoperability are securing stronger competitive positioning across enterprise cloud infrastructure environments.

VMware

Flexera

IBM

Apptio

Harness

CloudHealth Technologies

CloudCheckr

Spot by NetApp

Densify

Nutanix

Broadcom

Oracle

SAP

ServiceNow

AI-powered cloud financial governance platforms are becoming the core technology layer across enterprise multi-cloud environments. In 2026, nearly 61% of large enterprises deployed automated anomaly detection and predictive budgeting engines to improve infrastructure visibility and workload accountability. Advanced AI optimization tools reduce idle compute expenditure by approximately 28% while improving allocation accuracy by 24% compared with legacy spreadsheet-based monitoring systems. Companies integrating FinOps platforms directly into DevOps workflows are achieving faster budget enforcement and stronger operational transparency across Kubernetes, GPU, and containerized infrastructures.

Emerging technologies such as autonomous workload orchestration, Kubernetes cost analytics, and carbon-aware cloud optimization are reshaping operational decision-making. Around 49% of enterprises now use container-level cloud tracking platforms, improving workload efficiency by nearly 22%. API-driven integration between ERP systems, observability tools, and cloud governance platforms is accelerating deployment speed and enabling real-time infrastructure forecasting. Telecom and BFSI enterprises are scaling AI-assisted optimization frameworks to manage rising transaction-intensive workloads and complex hybrid cloud architectures.

Between 2026 and 2028, disruptive technologies including generative AI-driven forecasting, self-healing infrastructure optimization, and policy-based cloud automation will intensify competitive differentiation. Enterprises deploying predictive optimization engines are expected to improve cloud utilization efficiency by over 30% while reducing manual governance intervention significantly. Vendors investing aggressively in GPU optimization, sovereign cloud integration, and automated compliance orchestration will secure stronger enterprise adoption as cloud infrastructure complexity continues accelerating.

November 2025 – Apptio, an IBM company, launched Cloudability Governance and Kubecost 3.0 with integrated Terraform-based FinOps automation and GPU optimization capabilities. The platform improved Kubernetes resource visibility and automated container rightsizing efficiency by nearly 30%, strengthening enterprise AI workload governance and multi-cloud financial control. Source: Apptio

March 2026 – Flexera released its 2026 State of the Cloud Report, revealing that 81% of enterprises now actively use generative AI while cloud waste increased to 29% due to AI-driven infrastructure demand. The findings accelerated enterprise investment in centralized FinOps governance and cloud accountability frameworks globally. Source: Flexera

March 2026 – Flexera One expanded its Cloud Cost Optimization platform with unified AWS and Azure savings estimation dashboards and advanced anomaly alerting capabilities. The deployment enabled enterprises to evaluate cross-cloud optimization opportunities through a single analytics environment, improving infrastructure decision speed and cloud commitment visibility significantly. Source: Flexera One Documentation

November 2025 – IBM Apptio deepened integration with HashiCorp Terraform through Cloudability Governance, embedding policy enforcement and real-time cost estimation directly into infrastructure-as-code workflows. The integration improved provisioning visibility and proactive cloud budgeting controls, helping enterprises reduce deployment inefficiencies across complex hybrid cloud environments. Source: TechTarget

The Cloud Cost Management Market Report provides detailed analysis across cost monitoring, cost optimization, budget management, billing analytics, and resource management segments while evaluating operational adoption patterns across multi-cloud management, IT cost control, resource allocation, financial planning, and usage analytics applications. The study covers deployment trends across IT and telecom, BFSI, healthcare, retail, manufacturing, and government sectors, with nearly 60% of enterprise demand concentrated in multi-cloud governance and AI-intensive infrastructure environments. The report also assesses emerging technologies including AI-driven optimization, Kubernetes analytics, predictive budgeting, and carbon-aware workload orchestration.

The report delivers strategic insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting infrastructure modernization, enterprise cloud governance adoption, and regional deployment concentration trends between 2026 and 2033. It evaluates competitive positioning, enterprise investment strategies, platform integration capabilities, and operational efficiency priorities influencing vendor expansion. Coverage includes cloud-native governance frameworks, sovereign cloud initiatives, hybrid infrastructure optimization, and evolving FinOps deployment models supporting long-term business planning and enterprise cloud transformation strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5340 Million |

|

Market Revenue in 2033 |

USD 19936.62 Million |

|

CAGR (2026 - 2033) |

17.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

VMware, Flexera, IBM, Apptio, Harness, CloudHealth Technologies, CloudCheckr, Spot by NetApp, Densify, Nutanix, Broadcom, Oracle, SAP, ServiceNow |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |