Reports

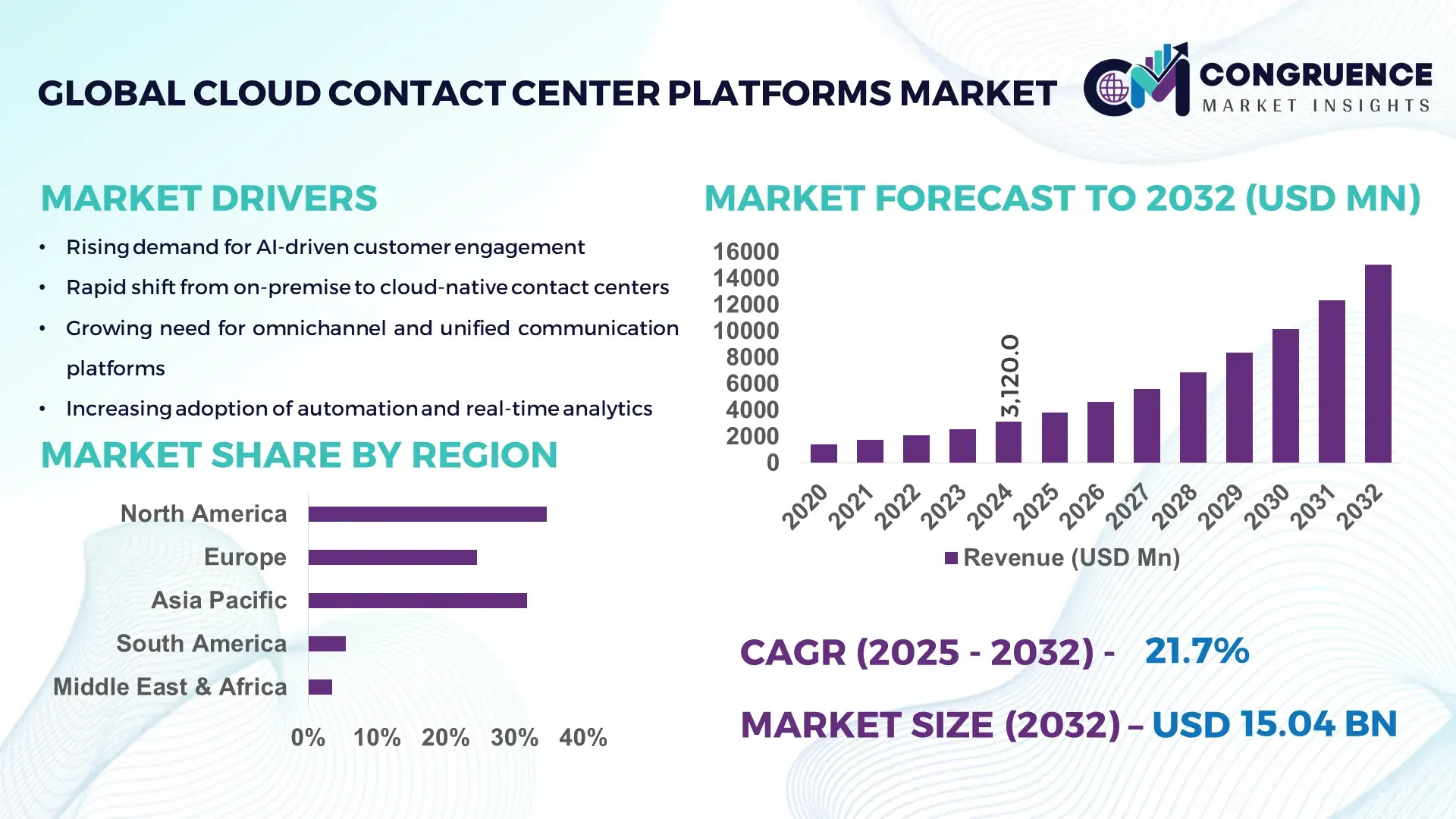

The Global Cloud Contact Center Platforms Market was valued at USD 3,120.0 Million in 2024 and is anticipated to reach a value of USD 15,043.0 Million by 2032 expanding at a CAGR of 21.73% between 2025 and 2032, according to an analysis by Congruence Market Insights. Due to accelerated enterprise migration to cloud-native customer experience stacks and AI-enabled automation is driving rapid adoption.

The United States remains the country that dominates the Cloud Contact Center Platforms Market. Production capacity for cloud contact center software and hosted services exceeds 1.2 million concurrent seats across major public-cloud regions, with enterprise investment levels surpassing USD 4.5 billion in platform modernisation in 2024 alone. Key industry applications include telecoms (accounting for ~28% of enterprise deployments), BFSI (24%), and e-commerce/retail (18%). Technological advancements include large-scale deployment of conversational AI (deployed in ~46% of new rollouts in 2024) and edge-enabled routing for latency-sensitive voice services (implemented by ~32% of tier-1 operators).

Market Size & Growth: Current market value USD 3,120.0 Million; projected value USD 15,043.0 Million; expected CAGR 21.73%; growth driven by cloud migration and AI automation.

Top Growth Drivers: Increased cloud adoption 48%, AI-driven automation efficiency 34%, omnichannel integration uplift 29%.

Short-Term Forecast: By 2028, average contact-center operating cost per contact expected to decline by 22%.

Emerging Technologies: Conversational AI, predictive routing, and edge-enabled voice services.

Regional Leaders: North America — projected USD 6,200M by 2032 (enterprise modernization-led), Asia-Pacific — USD 4,100M by 2032 (rapid digital adoption), Europe — USD 2,900M by 2032 (regulated deployments & telco integrations).

Consumer/End-User Trends: Enterprises favor self-service and blended-agent workflows; 55% of users prefer messaging channels for routine inquiries.

Pilot or Case Example: 2024 pilot of AI routing achieved 27% decrease in average handling time and 18% FCR improvement.

Competitive Landscape: Market leader ~26% share; key competitors include Five9, Genesys, NICE, Amazon Connect, and Cisco.

Regulatory & ESG Impact: Data-localization rules and energy-efficiency mandates accelerating on-prem→cloud shifts and green cloud procurement.

Investment & Funding Patterns: Recent private and strategic funding exceeded USD 2.1 billion, with rising project finance for platform modernization.

Innovation & Future Outlook: Trend toward composable CX stacks, tighter CRM-CC integrations, and AIops for real-time quality and compliance assurance.

The Cloud Contact Center Platforms Market is serving telecom, BFSI, retail, and healthcare sectors—telecom and BFSI dominate deployment volumes; innovations include conversational IVR, predictive analytics, and low-code integration tools. Regulatory, economic, and ESG drivers—data residency, digital transformation budgets, and green-cloud procurement—are accelerating cloud shifts while regional consumption favors APAC growth and North American scale deployments. Future trends point to composable, AI-centric CX stacks for resilient operations.

Cloud Contact Center Platforms are strategically central to enterprise CX transformation because they convert legacy voice-centric contact centers into data-driven, omnichannel operations that measurably improve KPIs and compliance posture. AI-driven routing and conversational AI enable automation of routine work—AI-driven routing delivers a 30% improvement compared to rule-based routing in average handling time and agent utilization. North America dominates in deployment volume, while Asia-Pacific leads in rapid enterprise adoption with ~42% of new cloud contact center rollouts in 2024. By 2027, conversational AI is expected to improve First Contact Resolution by approximately 18% and reduce repeat contacts by near-term operational redesigns. Firms are increasingly committing to ESG targets—many operators aim for a 15% reduction in data-center energy intensity by 2027 via green cloud contracts and workload scheduling. In a recent micro-scenario, a leading US telecom provider in 2024 achieved a 25% improvement in agent productivity and a 20% reduction in peak-period queuing by deploying predictive routing and elastic cloud scaling. Strategically, organisations will continue investing in open, composable CX stacks, embedded analytics, and AIops to convert real-time signals into capacity and quality decisions. This positions the Cloud Contact Center Platforms Market as a pillar of resilience, compliance, and sustainable growth for customer-centric enterprises.

The Cloud Contact Center Platforms Market is being reshaped by rapid cloud adoption, AI automation, and tighter regulatory expectations. Demand drivers include omnichannel customer expectations, the need for real-time analytics, and the shift from CAPEX to OPEX procurement models. Technology convergence—cloud telephony, CRM integration, and low-code orchestration—enables faster launch cycles: typical deployment lead times have fallen by an estimated 35% for greenfield cloud projects. Enterprises prioritise platform extensibility, security certifications (e.g., SOC2, ISO 27001), and vendor ecosystems that deliver pre-built connectors for CRM, workforce optimization, and quality assurance. Vendors are adding embedded AIops for anomaly detection and proactive capacity scaling. Competitive dynamics feature consolidation among platform specialists and hyperscalers offering managed contact-center services. Labour dynamics also influence platform choices: blended agent models and automation reduce routine task loads, enabling knowledge workers to focus on higher-value interactions. Overall, the market is moving from monolithic suites to modular, API-first architectures that support rapid innovation and measurable operational improvement across channels.

Omnichannel automation is a primary growth driver for the Cloud Contact Center Platforms Market because enterprises are integrating voice, SMS, chat, social, and messaging apps into unified interaction journeys. Adoption data indicate that 62% of new deployments in 2024 prioritized unified routing across at least three channels. Automation—conversational AI, bot-to-agent escalation, and automated post-call summarization—reduces agent workload and improves response times; pilots have reported up to 28% reductions in average handling time and 21% improvement in customer satisfaction scores. Enterprises also realize workforce efficiency through blended agent routing and intelligent scheduling: predictive analytics enable a 15–20% reduction in over-staffing while improving service-level attainment during peaks. Investment in omnichannel orchestration platforms and low-code integration toolkits is rising, enabling faster time-to-value and consistent CX across digital and voice touchpoints.

Legacy systems and complex integrations remain major restraints for the Cloud Contact Center Platforms Market. Many large enterprises retain on-prem telephony and proprietary middleware that require extensive reengineering: integration projects commonly consume 40–60% of migration budgets and extend timelines. Compliance and data-localization rules increase architectural complexity—implementing segmented data zones and hybrid deployments can add 12–18% to operational costs. Security and privacy requirements (encryption in transit and at rest, strict access controls, and audit trails) force additional tooling and professional services, slowing procurement cycles. Talent shortages for cloud-native CX engineering and AIops further impede rapid rollouts; organisations often experience a 20–30% skills gap between platform capabilities and in-house expertise, necessitating third-party managed services and training investments.

Integrating AIops and predictive analytics presents significant opportunities for the Cloud Contact Center Platforms Market by enabling proactive operations and capacity optimisation. AIops can detect usage anomalies, predict volume spikes, and automate scaling—reducing downtime risk and lowering cloud spend volatility; early adopters report up to 18% savings in cloud operating costs. Predictive contact routing and sentiment analysis boost resolution rates and improve agent coaching by surfacing high-value interactions; pilots show a 22% uplift in customer satisfaction when predictive insights guide agent interventions. There is also opportunity in industry-specific verticalisation—tailored modules for banking compliance workflows, healthcare consent handling, and telecom OSS/BSS integrations—each unlocking new enterprise procurement pools. Additionally, marketplaces for plug-and-play CX microservices enable faster innovation and recurring revenue for platform providers.

Escalating cloud costs and vendor lock-in pose substantial challenges to the Cloud Contact Center Platforms Market. Variable consumption models can lead to unpredictable monthly expenditures—some enterprises report 12–25% higher-than-expected cloud bills during initial scaling phases. Proprietary connectors and bespoke workflows increase switching costs: migration to alternate providers often requires re-engineering of integrations and retraining of staff. Regulatory demands for data locality and auditability can force hybrid topologies, increasing total cost of ownership by 10–20%. Further, interoperability gaps between different vendors’ APIs complicate omnichannel analytics and reporting, slowing enterprise governance. Finally, cybersecurity threats and the need for continuous patching create operational burdens that many enterprises address through managed services, adding to recurring expenses.

Conversational AI and Intent-driven Automation are accelerating: Conversational AI adoption rose to ~46% of new deployments in 2024, with intent-driven bots handling up to 40% of routine inquiries and reducing average handling time by 24%. Enterprises are implementing hybrid bot-to-agent flows to maintain quality while scaling self-service.

Composable, API-first Architectures enable rapid innovation: 58% of recent platform RFPs require API-first, modular components; this shift has cut time-to-deploy for new channels by nearly 35% and increased third-party microservice uptake by 47%.

AIops and Predictive Capacity Planning improve resiliency: AIops tooling is now present in ~33% of large deployments; predictive capacity models have reduced peak-period queue times by up to 22% and lowered unplanned scaling events by 19%.

Green Cloud and Compliance-driven Procurement is rising: 41% of enterprises now include sustainability metrics in vendor evaluations; energy-efficient cloud regions and contractual carbon-intensity SLAs are reducing data-center energy intensity targets by an average of 12–15% across recent procurements.

The Cloud Contact Center Platforms market is segmented across product types, deployment models, applications, and end-users, each reflecting distinct buyer priorities and deployment complexity. Product-type segmentation ranges from Automatic Call Distribution and omnichannel routing to analytics, workforce optimization, and AI-enabled automation modules; solution choices are increasingly influenced by integration capabilities with CRM, workforce systems, and compliance tooling. Deployment segmentation (public cloud, private cloud, hybrid) drives architectural choices—regulated industries favour hybrid models for data residency, while high-scale digital-first firms opt for public-cloud elasticity. Application segmentation covers customer service, telesales, technical support, and back-office orchestration, with each use case imposing unique SLAs and latency requirements. End-user segmentation spans telecom, BFSI, retail & e-commerce, healthcare, and public sector; enterprise buyers demand verticalised feature-sets (e.g., consent management for healthcare). Decision-makers prioritize extensibility, security certifications, and AIops for resiliency; procurement shifts toward OPEX consumption and vendor marketplaces for plug-in services. These segmentation lenses guide go-to-market, pricing, and product roadmaps for platform providers.

Automatic Call Distribution (ACD) and omnichannel routing platforms are the leading product type, accounting for approximately 24.1% of type-based deployments in 2024; ACD remains central because it standardises queuing, prioritisation, and SLA-driven routing across voice and digital channels. Analytics & reporting modules are the fastest-growing product segment—projected to expand at roughly 18.8% CAGR—driven by demand for real-time performance dashboards, speech/text analytics, and CX optimisation use cases. AI-enabled conversational engines and predictive routing modules are rapidly rising—conversational capabilities are being embedded into core platform stacks and are present in an increasing share of new rollouts. Other product types include workforce optimization (WFO) suites, quality management, IVR/voicebots, and professional services/managed services; combined, these remaining segments contribute roughly 57% of type-specific installations, serving niche and cross-functional needs (such as compliance recording, agent coaching, and verticalised integrations). Deployment-choice effects matter: analytics uptake is higher in public-cloud-first deployments due to easier data aggregation and elastic compute for large-scale speech-to-text processing.

Customer service and technical support functions are the leading applications, driven by high-volume inbound interactions and the need for omnichannel consistency; customer service applications represented the largest single application share in 2024, reflecting enterprise focus on retention and digital self-service. Contact routing, conversational IVR, and post-interaction analytics are prioritized to reduce handle times and improve FCR and CSAT metrics. Comparatively, outbound telesales and collections remain important but are smaller in share due to regulatory scrutiny and channel preference shifts. The fastest-growing application area is analytics-driven customer experience optimization (including predictive routing and sentiment-aware escalation), supported by investments in conversational AI and real-time telemetry; this application area shows the highest CAGR among application categories (market estimates indicate double-digit growth, driven by AI-led pilots and platform telemetry monetization). Other applications include workforce optimization, compliance recording, and back-office orchestration; combined, these remaining application segments account for roughly 45–50% of application-based deployments. Consumer adoption & trend statistics: in 2024, surveys found that ~55% of users prefer messaging channels for routine inquiries, and 23–44% of enterprises reported they were in the process of adopting or planning conversational AI pilots.

Large enterprises in Telecom and BFSI sectors are the leading end-users for cloud contact center platforms, with North America and APAC telcos and banks driving high-volume, mission-critical deployments; Telecom and BFSI together account for a substantial proportion of enterprise rollouts given their continuous high interaction volumes and regulatory needs. For example, North America held the largest CCaaS share (approximately 34.7% in 2024), reflecting concentration of large-scale buyers and progressive AI adoption among enterprises. Enterprise selection criteria emphasize vendor certifications, hybrid deployment options, and vertical feature-sets (fraud routing, consent management, and PCI/PHI-safe recording). The fastest-growing end-user vertical is e-commerce/retail, propelled by peak seasonal volumes, omnichannel demand, and investments in personalised CX; industry estimates show retail deployments expanding faster than legacy-heavy verticals (with double-digit growth rates reported for e-commerce contact center cloud adoption). Other end-users include healthcare, public sector, and SMEs—the combined share of these remaining segments is approximately 30–35%, with SMEs rapidly moving from legacy hosted platforms to CCaaS for operational agility. Consumer adoption & trend stats: more than 38% of enterprises reported piloting AI-driven contact center systems in 2024, while surveys indicate that younger consumers (Gen Z) increasingly expect fast, chat-first service channels.

North America accounted for the largest market share at 34.7% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24.5% between 2025 and 2032.

North America’s 34.7% share in 2024 reflects concentrated enterprise demand (with telecom, BFSI and large retailers collectively accounting for an estimated 70% of regional deployments), capacity for over 1.2 million concurrent seats across major cloud regions, and regional investments exceeding USD 4.5 billion in platform modernization in 2024. Asia-Pacific shows approx. 42% of new cloud rollouts in 2024, with top country counts led by China, India, and Japan (combined installed base volumes surpassing several hundred thousand active seats). Europe represented roughly 18.5% of global volumes in 2024 with Germany, UK and France as primary markets; Europe also shows high adoption of explainable AI and data-locality configurations in ~32% of enterprise tenders. South America and MEA together comprise the remaining ~12.3% of global installed volumes, with Brazil, Argentina, UAE and South Africa showing rapid modernization programs (30–45% of national outsourcers upgrading to cloud-first stacks in recent procurement cycles). These regional figures drive vendor roadmaps, capacity planning, and localization investments across channels, languages (multi-lingual routing covering 10+ major languages in top deployments), and compliance overlays.

North America commands a dominant position with a 34.7% market share in 2024 and volume metrics showing the highest concentration of large-scale, mission-critical deployments. Key industries driving demand include telecom (≈28% of enterprise deployments), BFSI (≈24%), retail & e-commerce (≈18%), and healthcare (≈9%). Regional investments surpassed USD 4.5 billion in platform modernization in 2024, and production capacity metrics indicate support for over 1.2 million concurrent cloud seats across major public-cloud regions. Notable regulatory and policy changes include expanded data-privacy and data-localization requirements, alongside sustainability procurement clauses (≈41% of enterprise RFPs include energy-efficiency criteria). Technological advances center on conversational AI (present in ~46% of new rollouts), predictive routing, and AIops for capacity planning. A prominent local player is Genesys (and other large platform vendors), which has focused on composable CX and hybrid-cloud orchestration and supports large telco and financial services customers with elastic routing and embedded analytics. Regional consumer behavior shows higher enterprise adoption in healthcare & finance, with preference for secure voice and authenticated digital channels; enterprises are prioritizing explainability, PCI/PHI-safe recording, and low-latency voice routing for regulatory compliance.

Europe accounted for approximately 18.5% of global cloud contact center volumes in 2024, with Germany, the United Kingdom, and France leading adoption by enterprise scale and procurement activity. Key European markets—Germany (large industrial & telecom buyers), UK (financial services and outsourcing hub), and France (retail and public sector modernization)—drive demand patterns that emphasize data residency, auditability, and explainable AI features. Regulatory pressure (notably stringent privacy and cross-border data transfer rules) has accelerated hybrid deployments and on-region cloud zones; roughly 32% of enterprise tenders in 2024 required explicit data-locality or segmented data zones. Sustainability initiatives are increasingly embedded in procurement, with ~41% of buyers including carbon-intensity or energy-efficiency clauses. Emerging technology adoption includes edge-enabled voice routing (implemented by ~32% of tier-1 operators) and modular, API-first architectures for telco integrations. A notable regional example is major European telcos and outsourcers investing in localized cloud contact center endpoints and verticalised compliance modules to serve regulated industries. Regional consumer behavior highlights stronger sensitivity to privacy and preference for secure, transparent AI-driven interactions, prompting demand for explainable and auditable CX features.

Asia-Pacific ranked as the second-largest regional market by volume in 2024 and accounted for roughly 28–30% of global installed seats, while also representing ~42% of new cloud rollouts in 2024—making it the region with the fastest pace of new deployments. Top consuming countries are China, India, and Japan, each contributing materially to installed base counts (combined active seats in the high hundreds of thousands). Infrastructure trends include rapid expansion of public-cloud regions, mobile-first architectures, and high adoption of edge or localized compute to reduce latency for voice services; mobile apps and AI-native chat channels account for more than 60% of digital channel growth. Innovation hubs in Singapore, Bangalore, Tokyo, and Shanghai are fostering integrations between AI, payments, and CRM systems—driving tailored solutions for e-commerce peaks and live-commerce interactions. Local players such as Alibaba Cloud and regional vendors are offering cloud contact center capabilities integrated with local messaging apps, enabling bilingual/bidirectional routing and peak-season elastic scaling. Regional consumer behavior is characterized by chat-first preferences, high acceptance of mobile self-service, and demand for seamless payment-enabled interactions, making APAC a hotspot for mobile AI applications and omnichannel experimentation.

South America’s cloud contact center market is concentrated in Brazil and Argentina, which together accounted for an estimated 5.5% of global volumes in 2024. Key country-level dynamics include strong demand for Portuguese and Spanish language localization, media & entertainment-driven contact spikes, and increasing investment in digital customer engagement by telcos and banks. Infrastructure constraints—intermittent bandwidth in some markets—have accelerated adoption of hybrid deployments and edge-assisted voice routing to maintain SLA adherence during peaks; roughly 35% of national outsourcers reported cloud-first migration projects in recent procurement cycles. Government incentives and trade policies in certain countries have supported digital services exports and BPO modernization, encouraging local providers to upgrade to cloud-native stacks to win international contracts. A regional player example: major national outsourcers and telco groups are piloting multilingual conversational AI to handle media-driven campaign volumes and local payment interactions. Consumer behavior variations include higher sensitivity to localized content and channels (messaging apps dominate daily interactions), and preference for voice support in lower-literacy user segments, making language and UX localization a critical investment.

Middle East & Africa (MEA) shows focused demand driven by sectors such as oil & gas, construction, financial services, and government digitization projects, with major country nodes in the UAE and South Africa. MEA contributed approximately 3.5% of global cloud contact center volumes in 2024, though regional procurement activity has been increasing—national cloud initiatives, sovereign cloud offerings, and trade partnerships have catalysed modernization. Technological modernization trends include rapid rollouts of multilingual IVR, Arabic-language conversational AI, and telco-backed cloud endpoints to serve cross-border GCC operations; some national programs have committed to local cloud zones and interoperability frameworks. Local players and large telcos are investing in capacity and managed services to support enterprise customers across energy, finance, and hospitality verticals. Regional consumer behavior variations include demand for multilingual support (Arabic, English, French), high mobile penetration for service access, and strong preference for assisted service in high-value segments; enterprises are prioritizing low-latency voice, secure authentication, and multilingual routing to serve diverse customer bases.

United States — 26.0% Market Share: United States Cloud Contact Center Platforms leadership is driven by high production capacity (supporting over 1.2 million concurrent seats), deep enterprise modernization budgets, and extensive adoption across telecom, BFSI, and large retail enterprises.

India — 9.5% Market Share: India Cloud Contact Center Platforms strength comes from a large BPO and outsourcing industry rapidly migrating to cloud-first stacks, strong talent pools for CX engineering, and growing domestic platform innovation supporting multi-lingual, high-volume contact operations.

The Cloud Contact Center Platforms Market is moderately concentrated at the top while remaining competitive and dynamic across a broad vendor base. Roughly 40–60 established vendors are actively competing globally, with dozens more niche and regional specialists addressing verticalised needs; the competitive field includes global platform providers, hyperscalers offering managed CCaaS, and specialist AI/microservice vendors. Market positioning varies: a market leader holds approximately ~26% share, the next two leaders each hold mid-teens shares (single-digit to low-teens), and the combined share of the top 5 companies is approximately 58%, indicating a top-heavy but not monopoly-like structure. Strategic initiatives in 2023–2024 included >30 notable acquisitions and partnerships (M&A and alliance activity focused on conversational AI, analytics, and outreach), >150 product enhancements across major vendors (UX, predictive routing, and generative-AI agent assists), and multiple hyperscaler integrations for data and compute elasticity. Innovation trends shaping competition include wider adoption of generative AI agent assistants, AIops for predictive capacity and anomaly detection, composable API-first architectures, and marketplaces for third-party CX microservices. Vendor differentiation is now driven by integration breadth (CRM, workforce, QA), compliance offerings (data-locality, recording controls), and verticalised solutions (banking, healthcare, telco). Pricing models are shifting from seat-based licensing to consumption and outcome-based contracts—many deals now include elastic scaling SLAs, performance credits, and energy-efficiency clauses. For decision-makers, the landscape implies careful vendor evaluation across operational KPIs (AHT, FCR, QA automation rates), data governance, and partner ecosystems rather than feature parity alone.

Amazon Connect / AWS

Cisco Webex Contact Center

Verint

Talkdesk

Vonage (Nexmo)

Zendesk

Twilio

Current and emerging technologies are shifting the capabilities and economics of cloud contact center platforms—decision-makers must evaluate these technologies both for immediate ROI and longer-term strategic differentiation. Conversational AI and generative-AI agent assistants now automate information retrieval, agent scripting, and post-interaction summarization; adoption rates for agent-assist features have rapidly expanded in 2023–2024, enabling reductions in average handling time (AHT) and faster QA cycles via automated transcripts and summaries. Predictive routing and sentiment-aware escalation leverage real-time telemetry and historic interaction signals to improve FCR by routing the right skillset and resources to priority interactions; predictive models also enable capacity planning that reduces peak over-provisioning. AIops (operational AI) is being implemented to detect anomalies, forecast load spikes, and automate auto-scaling—early adopters report measurable decreases in unplanned scaling events and lower cloud volatility.

Composable, API-first architectures and low-code orchestration are accelerating time-to-market for new channels and vertical integrations; they reduce integration costs by enabling plug-and-play connectors for CRM, payment gateways, and identity providers. Multimodal and omnichannel maturity—support for voice, chat, SMS, social messaging (WhatsApp, WeChat), and in-app messaging—now requires unified context stores and session continuity across channels. Edge-enabled voice routing and localized compute regions reduce latency and help satisfy data-residency or sovereignty requirements for regulated industries; many large deployments now use regional cloud zones and segmented data stores to meet audit and compliance needs. Security and privacy technologies—end-to-end encryption, tokenized PCI flows, and immutable audit trails—are increasingly table stakes, as are capabilities for redaction, consent management, and selective recording.

Innovation trends also include marketplaces for CX microservices (analytics, language packs, industry templates), integrated workforce optimization with real-time coaching, and automated compliance-monitoring engines. For CIOs and CX leaders, the priority is selecting platforms that balance rapid AI feature adoption with robust governance, interoperability, and predictable cost models—platform roadmaps and partner ecosystems are key purchase criteria.

In December 2023, NICE completed the acquisition and integration of LiveVox, combining telephony, workforce optimization, and cloud-native CX capabilities to strengthen its contact center portfolio and expand conversational AI and omnichannel outreach capabilities. Source: www.nice.com

In November 2023, Amazon announced new generative-AI features for Amazon Connect (including the Amazon Q agent-assist capability and enhanced Contact Lens summarization), enabling automated, context-rich conversation summaries and AI recommendations for supervisors and agents. Source: www.aws.amazon.com

In January–February 2024, Genesys announced and completed the acquisition of Radarr Technologies to enhance digital listening, social analytics, and AI-driven experience orchestration—integrating Radarr’s capabilities into Genesys Cloud for richer personalization and orchestration. Source: www.genesys.com

In 2024, Five9 announced strategic acquisitions and industry recognitions, including its planned acquisition of Acqueon (to expand omnichannel outreach) and leader placements in industry evaluations, underscoring expansion of AI-driven outreach and analytics capabilities across its Intelligent CX platform. Source: www.five9.com

This report covers the Cloud Contact Center Platforms market across functional modules, deployment models, end-user industries, and geographic regions with an emphasis on operational metrics, technology adoption, and procurement behavior. The functional scope includes core routing and ACD, omnichannel orchestration, conversational AI and virtual agents, analytics and reporting (speech and text analytics), workforce optimization (WFO), quality management, compliance and recording, and professional/managed services. Deployment models span public cloud, private cloud, and hybrid configurations, along with sovereign/region-locked clouds and edge-enabled deployments for low-latency voice services. Industry focus areas include telecom, BFSI, retail & e-commerce, healthcare, public sector, travel & hospitality, and BPO/outsourcing; the report addresses verticalised requirements such as PCI/PHI-safe recording, consent management, and regulatory overlays.

Geographically, the report provides region-wise coverage (North America, Europe, Asia-Pacific, South America, Middle East & Africa), regional volume and adoption patterns, and country-level snapshots for major markets. Technology and innovation coverage details conversational AI (NLP, intent detection, generative models), predictive routing, AIops, composable API-first architectures, low-code orchestration, multimodal channel integrations, and security/privacy controls. Commercial and go-to-market aspects include vendor positioning, partner ecosystems, pricing models (seat vs. consumption), and procurement trends such as sustainability clauses and outcome-based contracts. The report also maps segmentation by product type, application (inbound customer service, outbound sales, technical support, back-office orchestration), and end-user (enterprises by size and vertical), and includes implementation considerations (integration complexity, professional services effort, and migration costs). Niche and emerging segments—microservice marketplaces, industry templates, and specialized language/localization packs—are assessed for near-term opportunity. The content is structured to inform strategic decisions on vendor selection, technology investments, capacity planning, and compliance readiness.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,120.0 Million |

| Market Revenue (2032) | USD 15,043.0 Million |

| CAGR (2025–2032) | 21.73% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Genesys, Five9, NICE, Amazon Connect / AWS, Cisco Webex Contact Center, Verint, Talkdesk, Vonage (Nexmo), Zendesk, Twilio |

| Customization & Pricing | Available on Request (10% Customization Free) |