Reports

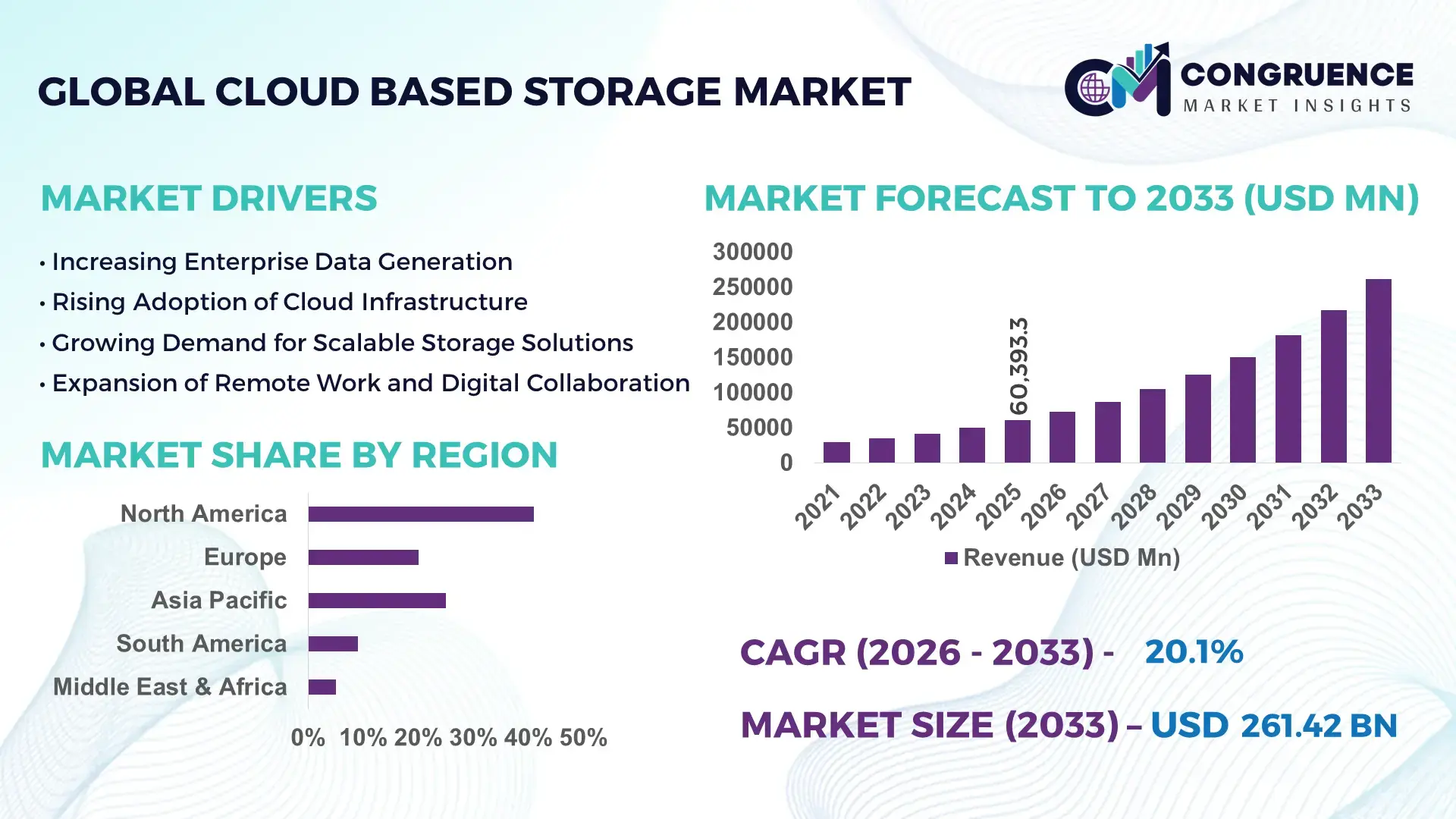

The Global Cloud Based Storage Market was valued at USD 60393.32 Million in 2025 and is anticipated to reach a value of USD 261416.52 Million by 2033 expanding at a CAGR of 20.1% between 2026 and 2033. The rapid digitization of enterprise operations and the accelerating shift toward scalable data infrastructure are key factors supporting market expansion.

The United States continues to lead the Cloud Based Storage market through extensive hyperscale data center infrastructure and large-scale enterprise adoption. As of 2025, the country hosts more than 5,300 operational data centers, accounting for over 38% of global hyperscale capacity. Large cloud infrastructure providers collectively operate storage systems capable of handling exabytes of enterprise and consumer data across sectors such as healthcare, finance, media streaming, and e-commerce. Enterprise cloud adoption in the United States exceeds 90% among large organizations, while more than 70% of small and medium enterprises rely on hybrid or multi-cloud storage solutions. The country has also seen over USD 70 billion invested in new data center expansions between 2022 and 2025, significantly increasing cloud storage processing capabilities and improving data redundancy, cybersecurity frameworks, and real-time storage analytics.

Market Size & Growth: The Cloud Based Storage Market reached USD 60393.32 Million in 2025 and is projected to expand to USD 261416.52 Million by 2033, reflecting a CAGR of 20.1%, driven by rising enterprise data volumes, remote collaboration demand, and scalable digital infrastructure adoption.

Top Growth Drivers: Enterprise cloud adoption exceeding 85%, operational cost reduction benefits reaching 35% through scalable storage, and up to 40% improvement in data accessibility for distributed workforces.

Short-Term Forecast: By 2028, advanced cloud storage automation and intelligent workload management are expected to reduce enterprise infrastructure maintenance costs by nearly 28% while improving data retrieval performance by approximately 32%.

Emerging Technologies: Artificial intelligence-driven storage optimization, edge-cloud integration, and automated data lifecycle management are shaping next-generation cloud storage ecosystems.

Regional Leaders: North America is projected to surpass USD 105 billion by 2033 due to enterprise cloud infrastructure expansion; Asia-Pacific may exceed USD 88 billion driven by rapid digitalization and startup ecosystems; Europe is expected to approach USD 54 billion supported by regulatory-compliant data hosting services.

Consumer/End-User Trends: IT and telecommunications, banking and financial services, healthcare providers, and media streaming platforms represent major users, with enterprise cloud storage adoption surpassing 80% among large organizations.

Pilot or Case Example: In 2024, a multinational retail enterprise deployed AI-enabled cloud storage architecture that reduced system downtime by 41% while improving real-time inventory data processing efficiency by 37%.

Competitive Landscape: The market leader holds approximately 32% share, followed by major competitors including leading global cloud service providers and enterprise storage platform developers operating across multi-cloud ecosystems.

Regulatory & ESG Impact: Data sovereignty regulations, cybersecurity compliance frameworks, and green data center initiatives encouraging up to 25% reduction in energy consumption are influencing enterprise storage decisions.

Investment & Funding Patterns: Global cloud infrastructure investment exceeded USD 120 billion in the past three years, with growing venture funding directed toward cloud security, storage virtualization, and distributed data management technologies.

Innovation & Future Outlook: Integration of quantum-resistant encryption, predictive storage analytics, and decentralized cloud architectures is expected to transform secure data storage and cross-platform interoperability across industries.

Enterprise demand for cloud based storage continues to expand across sectors such as banking, healthcare, telecommunications, and digital media where large-scale data management is essential. Financial institutions contribute nearly 20% of enterprise cloud storage demand due to digital transaction volumes, while healthcare organizations increasingly rely on secure cloud storage for medical imaging and patient records. Recent innovations include automated data tiering, intelligent storage orchestration, and container-based storage platforms that enhance operational efficiency. Regulatory frameworks emphasizing data protection and cybersecurity compliance are accelerating cloud migration across Europe and North America. Meanwhile, Asia-Pacific markets are experiencing strong consumption growth driven by mobile internet penetration, digital commerce expansion, and government-backed cloud infrastructure development programs.

Cloud Based Storage Market development has become strategically critical for modern enterprises seeking scalable digital infrastructure, advanced analytics capabilities, and secure data management environments. As global data generation surpasses 180 zettabytes annually by the end of the decade, organizations are increasingly shifting from on-premise storage architectures toward flexible multi-cloud environments capable of supporting large-scale digital operations. Businesses across finance, healthcare, manufacturing, and e-commerce sectors are prioritizing cloud-native storage platforms to support artificial intelligence workloads, big data analytics, and distributed computing environments.

Technological innovation plays a defining role in the strategic expansion of the Cloud Based Storage Market. For instance, object-based storage architecture delivers nearly 45% improvement in scalability and metadata management compared to traditional block storage systems widely used in legacy enterprise data centers. This transition enables enterprises to manage petabyte-level data environments while reducing operational complexity and enabling automated storage provisioning across hybrid infrastructures.

Regional performance trends highlight differences in infrastructure deployment and adoption behavior. North America dominates in data storage volume due to its concentration of hyperscale data centers, while Asia-Pacific leads in enterprise adoption growth with nearly 72% of large organizations implementing cloud storage solutions as part of digital transformation strategies. The expansion of mobile connectivity, artificial intelligence applications, and digital government services is accelerating adoption across emerging economies.

In 2024, a major technology firm in South Korea deployed AI-enabled predictive storage analytics within its national cloud infrastructure, achieving a 33% improvement in data processing efficiency and reducing operational downtime by nearly 27%. Similar initiatives demonstrate how intelligent cloud storage solutions are improving operational resilience across digital ecosystems. As data volumes continue to expand globally, the Cloud Based Storage Market will remain a fundamental pillar supporting enterprise resilience, regulatory compliance, and sustainable digital transformation.

The exponential increase in global data creation is one of the most powerful drivers shaping the Cloud Based Storage Market. Modern enterprises generate massive volumes of structured and unstructured data through digital transactions, social media engagement, industrial sensors, and connected devices. Global data generation is expected to surpass 180 zettabytes by the end of the decade, creating unprecedented demand for scalable storage platforms capable of handling large and continuously expanding datasets. Cloud based storage solutions allow organizations to expand storage capacity instantly without major capital investments in physical infrastructure. Businesses can store petabytes of operational data while maintaining accessibility across global teams and digital platforms. In sectors such as healthcare and financial services, where regulatory compliance requires long-term data retention and secure archiving, cloud storage platforms offer advanced encryption and automated backup mechanisms. Additionally, enterprises adopting artificial intelligence and machine learning applications require large centralized datasets for algorithm training and analytics. These operational requirements are significantly increasing the demand for flexible, high-capacity cloud storage systems that can efficiently manage data across multiple geographic regions and digital ecosystems.

Despite its advantages, the Cloud Based Storage Market faces restraints related to cybersecurity threats, data privacy concerns, and compliance complexities. Organizations storing critical business information in cloud environments must address potential risks such as unauthorized access, ransomware attacks, and data breaches. Global cybersecurity reports indicate that more than 70% of organizations experienced at least one cloud security incident in recent years, highlighting the vulnerability of digital storage infrastructure when security protocols are inadequate. Many enterprises remain cautious about transferring sensitive financial, healthcare, or government data to external cloud environments due to concerns about regulatory compliance and data sovereignty requirements. In highly regulated industries, strict data protection frameworks require companies to maintain detailed audit trails, encryption standards, and geographic data storage restrictions. Implementing these compliance measures often increases operational complexity and security investment requirements. Furthermore, organizations operating across multiple countries must navigate diverse data protection regulations, including strict privacy frameworks and national data localization policies. These regulatory and security challenges can slow enterprise adoption and require significant investments in cybersecurity infrastructure to ensure safe cloud storage operations.

Artificial intelligence integration presents substantial opportunities for the Cloud Based Storage Market by transforming how organizations manage, analyze, and optimize their data assets. AI-powered storage management systems can automatically categorize, prioritize, and allocate storage resources based on data usage patterns, enabling enterprises to reduce operational inefficiencies and improve data accessibility. Advanced machine learning algorithms can also identify redundant data, automate backup scheduling, and optimize storage tiering, improving overall infrastructure efficiency. In industries such as healthcare, AI-driven cloud storage platforms are being used to process and store large medical imaging datasets while enabling real-time analytics for diagnostics and treatment planning. Similarly, financial institutions are using AI-enabled storage environments to analyze transaction data and detect fraudulent activities with higher precision. Edge computing combined with cloud storage is also creating new opportunities for industries that rely on real-time data processing, including smart manufacturing and autonomous transportation systems. As organizations continue to integrate artificial intelligence into core operations, the demand for intelligent cloud storage platforms capable of supporting advanced analytics and predictive data management will continue to grow rapidly.

One of the major challenges facing the Cloud Based Storage Market is the increasing cost associated with large-scale data storage infrastructure and high-volume data transfers. While cloud platforms offer flexible scalability, organizations with massive datasets often encounter significant operational expenses related to storage capacity expansion, network bandwidth usage, and data retrieval processes. For example, enterprises operating data-intensive applications such as high-resolution video streaming, scientific research simulations, or real-time analytics may transfer terabytes of data daily across cloud environments. Data egress charges and network bandwidth costs can significantly increase operational budgets for companies managing large distributed workloads. Additionally, migrating legacy data from on-premise systems to cloud infrastructure often requires complex integration processes and specialized data migration tools, which can increase implementation time and project costs. Businesses also need to invest in robust connectivity infrastructure to ensure fast and reliable access to cloud storage platforms across global operations. These financial and technical complexities require careful planning and cost management strategies, particularly for organizations handling large-scale digital data environments.

• AI-Driven Storage Automation Improving Operational Efficiency: Artificial intelligence integration is transforming how organizations manage and optimize cloud based storage environments. Nearly 62% of large enterprises now deploy AI-enabled storage analytics platforms to automate data classification, predictive maintenance, and intelligent workload allocation. Automated data lifecycle management tools have reduced manual storage administration workloads by approximately 45% across enterprise IT departments. Additionally, AI-based predictive storage optimization systems can detect performance anomalies with over 90% accuracy, helping organizations minimize downtime and improve system availability. This trend is particularly visible in financial services and e-commerce industries where high-frequency transaction data requires real-time storage management and instant accessibility across distributed infrastructure networks.

• Rapid Expansion of Multi-Cloud Storage Architectures: Multi-cloud strategies are becoming a dominant trend in the Cloud Based Storage market as enterprises seek greater flexibility and risk mitigation across digital infrastructure. More than 76% of global enterprises currently utilize multi-cloud storage frameworks that combine infrastructure from at least two cloud providers. These architectures allow organizations to distribute workloads, improve redundancy, and enhance disaster recovery capabilities. Multi-cloud adoption has increased enterprise data availability by nearly 38% while reducing service outage risks by approximately 30%. Large organizations operating across global markets are increasingly integrating cross-platform storage orchestration tools that enable centralized management of multiple cloud environments, improving operational efficiency and enabling seamless scalability for rapidly expanding digital operations.

• Surge in Edge-Cloud Storage Integration for Real-Time Data Processing: Edge computing integration with cloud based storage platforms is emerging as a key trend supporting real-time data processing for digital ecosystems. Around 58% of industrial companies deploying Internet of Things devices now integrate edge-cloud storage infrastructure to process data closer to the source. Edge-enabled storage systems can reduce data latency by nearly 40%, enabling faster decision-making in sectors such as smart manufacturing, autonomous transportation, and telecommunications networks. By processing high-volume sensor data locally before transferring it to centralized cloud storage environments, organizations can significantly reduce bandwidth consumption while maintaining real-time analytics capabilities. This trend is accelerating as global IoT device installations are projected to surpass 29 billion connected devices by the end of the decade.

• Rise in Green Data Centers and Sustainable Cloud Storage Infrastructure: Environmental sustainability is increasingly influencing infrastructure investments in the Cloud Based Storage market. Approximately 48% of new hyperscale data center projects now incorporate renewable energy sources and advanced cooling technologies to reduce environmental impact. Modern energy-efficient data center architectures have demonstrated up to 35% reductions in electricity consumption compared to traditional facilities. Leading cloud infrastructure providers are deploying liquid cooling systems capable of lowering server energy requirements by nearly 20% while maintaining high-performance storage operations. Additionally, large technology companies have committed to operating carbon-neutral cloud storage facilities by 2030, encouraging widespread adoption of sustainable data infrastructure and environmentally responsible digital storage solutions.

The Cloud Based Storage Market is structured across several key segments including storage types, application areas, and diverse end-user industries. Storage types typically include public cloud storage, private cloud storage, and hybrid cloud storage architectures designed to address different enterprise data management requirements. Application segmentation highlights how organizations utilize cloud storage platforms for backup and disaster recovery, big data analytics, media content storage, and enterprise collaboration environments. End-user segmentation further reflects the growing reliance on cloud infrastructure among sectors such as banking, healthcare, telecommunications, retail, and government organizations. The increasing scale of digital data generation across industries has accelerated the need for flexible storage platforms capable of managing structured and unstructured datasets. Organizations are adopting cloud storage solutions to support artificial intelligence workloads, high-volume transaction systems, and real-time analytics platforms. This segmentation framework allows technology providers to tailor scalable solutions that address industry-specific operational requirements while ensuring data security, regulatory compliance, and performance optimization across global digital infrastructure networks.

Public cloud storage, private cloud storage, and hybrid cloud storage represent the primary storage architectures within the Cloud Based Storage market. Public cloud storage currently leads the segment, accounting for nearly 52% of global enterprise deployments due to its scalability, cost efficiency, and simplified infrastructure management. Organizations prefer public cloud platforms for large-scale data archiving, application hosting, and collaborative data sharing environments where rapid expansion of storage capacity is essential. Hybrid cloud storage follows with approximately 31% adoption, allowing enterprises to integrate on-premise infrastructure with external cloud platforms for improved data flexibility and enhanced disaster recovery capabilities. Private cloud storage environments account for roughly 17% of deployments, primarily within sectors requiring strict data protection and regulatory compliance such as financial institutions, healthcare providers, and government agencies. These systems offer higher levels of security control and data sovereignty, making them suitable for handling sensitive information and confidential operational data. Hybrid cloud storage represents the fastest-growing segment, expanding at an estimated 23% CAGR as organizations increasingly adopt flexible infrastructure strategies combining private security with public scalability. Businesses managing large datasets often utilize hybrid models to store critical data internally while leveraging public platforms for analytics and large-scale processing workloads.

Backup and disaster recovery represent the leading application within the Cloud Based Storage market, accounting for nearly 36% of total enterprise usage. Organizations rely heavily on cloud storage platforms to maintain secure off-site backups and ensure rapid data recovery in the event of system failures or cyber incidents. The ability to automatically replicate data across geographically distributed data centers significantly improves operational resilience and business continuity for enterprises managing critical digital assets. Big data analytics applications account for approximately 28% of cloud storage usage as companies increasingly process large datasets generated through digital transactions, IoT networks, and customer interaction platforms. Cloud storage environments enable organizations to centralize and process massive data volumes required for predictive analytics, machine learning model training, and real-time business intelligence systems. Media storage and content distribution platforms represent about 19% of applications, particularly among streaming platforms, digital entertainment companies, and online gaming providers managing high-resolution video and multimedia files. Collaboration and file-sharing applications collectively account for the remaining 17% of market usage, enabling distributed teams to securely access shared digital workspaces.

The IT and telecommunications sector represents the largest end-user segment within the Cloud Based Storage market, accounting for approximately 34% of enterprise deployments. Telecommunications companies and digital platform providers generate enormous volumes of data through network operations, video streaming services, and cloud applications, requiring highly scalable storage infrastructure capable of supporting continuous data processing and real-time service delivery. Banking and financial services represent around 22% of cloud storage adoption, driven by the need to manage transaction records, digital payment systems, and regulatory compliance data. Financial institutions increasingly rely on secure cloud storage platforms for advanced analytics, fraud monitoring, and large-scale digital banking operations. Healthcare organizations contribute nearly 18% of end-user demand as hospitals and medical research institutions increasingly adopt cloud storage to manage electronic health records, medical imaging datasets, and genomics research data. Retail and e-commerce sectors account for approximately 15% of market demand, supported by rapid growth in online shopping platforms and digital consumer analytics systems.

Region North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24% between 2026 and 2033.

Europe followed with nearly 27% market share, supported by strong regulatory compliance infrastructure and enterprise digitalization initiatives. Asia-Pacific held approximately 22% share, driven by rapid cloud adoption across China, India, and Japan. South America represented nearly 6%, while the Middle East & Africa contributed around 4%. Globally, more than 65% of enterprises now rely on cloud-based data storage, with hyperscale data center capacity exceeding 1,000 operational facilities worldwide supporting massive digital storage demand.

How Is Advanced Enterprise Digital Infrastructure Accelerating Cloud Storage Adoption?

North America holds approximately 41% of the global Cloud Based Storage market, supported by the presence of more than 5,300 operational data centers and a highly mature enterprise digital ecosystem. Key industries driving demand include financial services, healthcare, media streaming, and e-commerce platforms that generate massive volumes of real-time transactional data. More than 90% of large enterprises across the region rely on hybrid or multi-cloud storage solutions for data management and analytics. Government-backed digital security frameworks and privacy regulations have strengthened enterprise confidence in cloud infrastructure. Technological innovation remains strong, with AI-driven storage optimization systems improving storage efficiency by nearly 35% across enterprise IT environments. One notable example is a major regional technology provider expanding hyperscale storage capacity with new data centers capable of supporting hundreds of petabytes of enterprise data. Consumer behavior trends indicate higher enterprise adoption in healthcare and finance sectors where large-scale data archiving and regulatory compliance requirements are critical.

What Factors Are Accelerating Secure and Compliant Enterprise Data Storage Solutions?

Europe accounts for nearly 27% of the global Cloud Based Storage market, with major markets including Germany, the United Kingdom, and France leading enterprise cloud infrastructure adoption. Strong regulatory frameworks related to digital privacy and data sovereignty have significantly influenced cloud storage deployment strategies across the region. Enterprises are investing heavily in secure storage environments capable of complying with strict data protection policies and cybersecurity regulations. Sustainability initiatives are also shaping data center investments, with approximately 45% of new facilities integrating renewable energy-powered infrastructure. Technological adoption is expanding rapidly as organizations implement artificial intelligence-based storage optimization and advanced data lifecycle management tools. A leading regional cloud infrastructure provider recently launched a distributed data platform designed to manage more than 10 million enterprise workloads across European digital networks. Regional consumer behavior reflects strong demand for regulatory-compliant cloud storage solutions, particularly among financial institutions, public sector organizations, and healthcare systems handling highly sensitive data.

How Is Rapid Digital Transformation Driving Enterprise Data Storage Expansion?

Asia-Pacific ranks among the fastest expanding Cloud Based Storage markets, accounting for approximately 22% of global demand while experiencing strong digital infrastructure development. Major consuming countries include China, India, and Japan, where cloud adoption is accelerating across e-commerce, telecommunications, and digital financial services sectors. The region hosts more than 350 hyperscale data centers, supporting rapidly expanding digital ecosystems and mobile-based applications. Infrastructure investments are rising significantly as governments support national cloud computing initiatives and technology innovation hubs. Several regional technology companies are investing in large-scale storage infrastructure capable of handling exabyte-level data processing workloads. One prominent regional provider recently launched a multi-cloud storage platform capable of supporting over 1 million enterprise users across digital services networks. Consumer behavior in the region reflects strong growth driven by mobile commerce platforms, digital payment systems, and artificial intelligence applications, with more than 70% of enterprises adopting cloud-based digital infrastructure strategies.

What Role Do Digital Media Expansion and Infrastructure Modernization Play in Cloud Storage Demand?

South America represents roughly 6% of the global Cloud Based Storage market, with Brazil and Argentina emerging as key national markets. Infrastructure modernization initiatives and the expansion of digital media platforms are contributing to increasing cloud storage adoption across the region. Brazil alone hosts more than 120 operational data centers, supporting digital transformation initiatives across financial services, telecommunications, and government digital platforms. Governments in several countries are promoting digital infrastructure investments through technology incentives and trade partnerships aimed at strengthening regional data hosting capabilities. A leading regional cloud services provider recently launched an enterprise storage platform capable of supporting more than 500,000 corporate users across Latin American digital ecosystems. Consumer behavior trends indicate that demand is closely tied to digital entertainment services, localized media content platforms, and mobile internet expansion, with streaming services generating significant storage requirements for high-definition multimedia content.

How Are Digital Infrastructure Investments Supporting Enterprise Data Storage Growth?

The Middle East & Africa Cloud Based Storage market accounts for approximately 4% of global demand, supported by increasing investments in digital infrastructure and smart technology initiatives. Key growth countries include the United Arab Emirates, Saudi Arabia, and South Africa, where governments are promoting cloud computing adoption to strengthen digital economies. Oil and gas companies, financial institutions, and large construction enterprises are among the major industries generating demand for secure cloud-based data storage. The region has witnessed more than 40 new hyperscale and enterprise data center projects in the past five years, significantly improving regional storage capacity. A major regional telecommunications provider recently launched a cloud storage platform capable of managing petabyte-scale enterprise data workloads for digital government services. Consumer behavior trends indicate rising demand for mobile cloud storage solutions as smartphone penetration exceeds 70% in several urban markets, supporting the growth of digital applications and cloud-hosted business services.

United States – 38% share: The United States Cloud Based Storage market dominates due to extensive hyperscale data center infrastructure and widespread enterprise cloud adoption across finance, healthcare, and digital services sectors.

China – 17% share: The China Cloud Based Storage market leads through massive digital infrastructure expansion and strong demand from e-commerce, mobile platforms, and artificial intelligence-driven data processing ecosystems.

The Cloud Based Storage market is moderately consolidated with more than 60 active global technology providers competing across enterprise cloud infrastructure and storage platform solutions. The top five companies collectively control nearly 55% of global deployments, supported by extensive hyperscale data center networks and integrated cloud service ecosystems. Competition is largely driven by infrastructure expansion, advanced cybersecurity capabilities, and artificial intelligence-powered storage optimization technologies. Major providers continue to invest heavily in global data center development, with more than 150 new hyperscale facilities planned or under construction worldwide. Strategic partnerships between cloud infrastructure providers and enterprise software vendors are accelerating innovation in hybrid and multi-cloud environments. Additionally, mergers, product launches, and cross-platform integration tools are shaping competitive dynamics as companies seek to deliver scalable, secure, and high-performance storage services for data-intensive digital enterprises.

Amazon Web Services

Microsoft

IBM

Oracle

Alibaba Cloud

Tencent Cloud

Hewlett Packard Enterprise

Dell Technologies

Dropbox

Box Inc.

Wasabi Technologies

Cloud based storage infrastructure is rapidly evolving through the integration of artificial intelligence, distributed storage architectures, and high-performance networking technologies. Modern cloud storage platforms increasingly rely on object-based storage systems, which now manage more than 80% of unstructured enterprise data, enabling scalable management of petabyte-scale datasets across global networks. AI-driven storage orchestration tools can automatically classify and allocate data across storage tiers, improving storage utilization efficiency by nearly 30% and reducing manual administration workloads by over 40% in enterprise environments.

Another significant technological advancement is the adoption of NVMe-over-Fabrics (NVMe-oF) architectures in hyperscale data centers. These high-speed storage protocols reduce latency by up to 50% compared to traditional SATA-based storage, supporting real-time analytics, machine learning model training, and large transactional databases. Additionally, software-defined storage (SDS) solutions are gaining traction as organizations shift toward hybrid and multi-cloud environments. SDS platforms enable centralized control of distributed storage resources across public and private infrastructures, improving scalability and interoperability.

Edge computing integration is also reshaping the Cloud Based Storage Market. Edge-enabled storage architectures can process data closer to the source, reducing network bandwidth consumption by approximately 35% while improving real-time analytics capabilities. As global IoT device installations continue to exceed 25 billion connected devices, these technologies are becoming essential for industries managing massive volumes of sensor, multimedia, and operational data across geographically distributed environments.

• In April 2024, Google Cloud introduced Hyperdisk ML, a high-performance block storage service designed for AI and machine learning workloads. The platform delivers up to 2.6 million IOPS and 10 GB/s throughput, enabling large-scale AI model training and data processing across enterprise cloud environments.

• In November 2024, Amazon Web Services announced Amazon S3 Tables, a new storage capability designed to optimize analytics workloads by storing tabular data directly in S3. The technology integrates Apache Iceberg support and improves query performance for large datasets used in data lakes and analytics pipelines.

• In October 2024, Dropbox launched Dropbox Dash, an AI-powered universal search and knowledge management tool integrated with its cloud storage platform. The system allows users to locate files across multiple applications and data repositories, improving enterprise productivity and reducing search time by more than 30%.

• In March 2025, Backblaze announced that its B2 Cloud Storage platform surpassed 3 exabytes of customer data stored, reflecting rapid adoption among enterprises managing large multimedia archives, application backups, and AI datasets across distributed digital infrastructure.

The Cloud Based Storage Market Report provides a comprehensive evaluation of global storage infrastructure developments across enterprise and consumer cloud ecosystems. The report examines key storage architectures including public cloud, private cloud, and hybrid cloud environments, analyzing their operational roles in managing large-scale digital data systems. It evaluates major applications such as backup and disaster recovery, big data analytics, content distribution networks, enterprise collaboration platforms, and IoT data management systems, which collectively support billions of daily digital transactions and data transfers worldwide.

The report also analyzes market activity across five major geographic regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting differences in infrastructure maturity, regulatory frameworks, and digital transformation initiatives. It further explores technological advancements including AI-driven storage optimization, software-defined storage platforms, NVMe-based high-performance architectures, and edge-cloud storage integration. Industry adoption trends are examined across sectors such as banking and financial services, healthcare, telecommunications, retail, government, and media streaming, where organizations increasingly rely on cloud platforms to store petabyte-scale datasets. Additionally, the report evaluates emerging areas such as green data center infrastructure, distributed cloud environments, and advanced cybersecurity frameworks, providing strategic insights for technology providers, investors, and enterprise decision-makers operating within the global Cloud Based Storage ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

20.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amazon Web Services, Microsoft, Google, IBM, Oracle, Alibaba Cloud, Tencent Cloud, Hewlett Packard Enterprise, Dell Technologies, Dropbox, Box Inc., Wasabi Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |