Reports

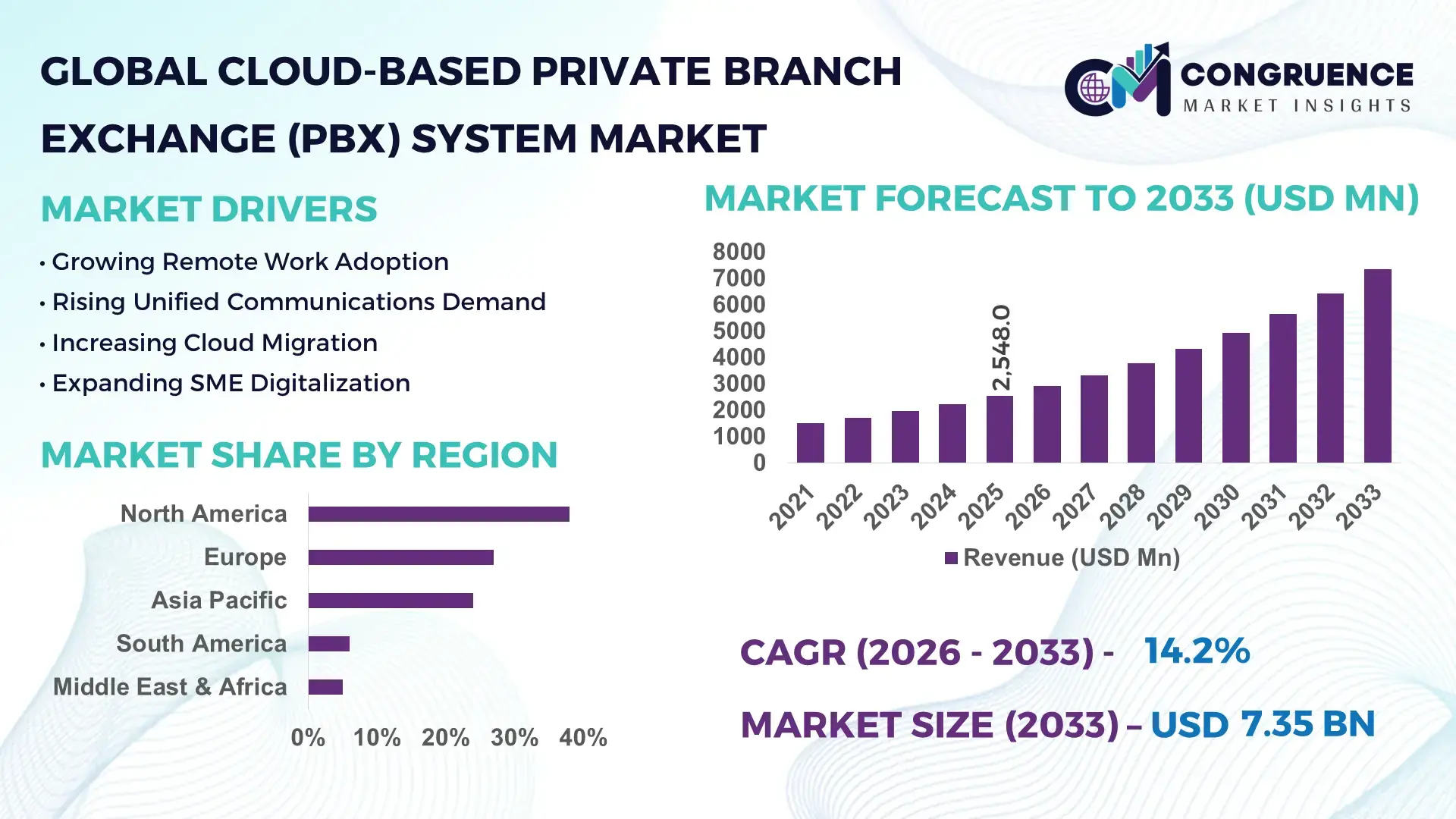

The Global Cloud-Based Private Branch Exchange (PBX) System Market was valued at USD 2,548.0 Million in 2025 and is anticipated to reach a value of USD 7,345.3 Million by 2033 expanding at a CAGR of 14.15% between 2026 and 2033. Growth is being accelerated by enterprise migration from legacy telephony infrastructure to unified cloud communication platforms integrating AI-enabled call routing, workforce mobility, and multi-location business operations.

The United States dominates the market with an estimated 34% share, supported by over 5.5 million businesses utilizing cloud communication services and sustained enterprise digital transformation investments exceeding USD 100 billion annually. Compared with Germany, where cloud communication adoption among enterprises is approaching 48%, U.S. deployment rates exceed 65%, driven by advanced SaaS ecosystems, large-scale hybrid work environments, and rapid AI integration. The ongoing modernization of enterprise communications following post-pandemic workplace restructuring continues to reinforce market leadership.

Organizations prioritizing scalable communication infrastructure and AI-driven customer engagement capabilities are securing stronger operational flexibility and long-term competitive differentiation.

Market Size & Growth: USD 2,548.0 Million in 2025, reaching USD 7,345.3 Million by 2033 at 14.15% CAGR, driven by enterprise migration from legacy PBX systems to cloud-native unified communications.

Top Growth Drivers: Hybrid workforce adoption (+58%), AI-enabled customer engagement deployment (+46%), and multi-site enterprise connectivity demand (+41%) remain primary market accelerators.

Short-Term Forecast: By 2028, cloud communication operating costs are expected to decline by nearly 25% while deployment efficiency improves by over 35% through automation.

Emerging Technologies: AI-based call analytics, conversational intelligence, automated routing, and API-driven communication integration are reshaping advanced PBX deployments.

Regional Leaders: North America (~USD 2.8 Billion), Europe (~USD 1.9 Billion), and Asia-Pacific (~USD 1.6 Billion) lead adoption through enterprise digitization and cloud infrastructure expansion.

Consumer/End-User Trends: More than 62% of mid-sized enterprises now prioritize cloud voice systems supporting remote and mobile workforce management.

Pilot/Case Example: In 2024, enterprise cloud communication modernization projects reported up to 30% faster response times and 22% lower support workloads.

Competitive Landscape: Market concentration remains moderate, with leading vendors controlling approximately 38% share; key participants include RingCentral, Microsoft, Cisco, Zoom, and 8x8.

Regulatory & ESG Impact: Cloud-based deployments reduce on-premise hardware requirements by nearly 40%, supporting enterprise sustainability and digital infrastructure policies.

Investment & Funding: More than USD 4 billion has been directed toward cloud communication infrastructure, strategic partnerships, and AI-powered platform expansion initiatives.

Innovation & Future Outlook: Generative AI assistants, autonomous contact-center functions, and communications-platform ecosystems are becoming core competitive differentiators globally.

Cloud-Based Private Branch Exchange (PBX) systems have become foundational communication infrastructure across BFSI, healthcare, retail, IT services, and professional services sectors. Recent innovation focuses on AI-powered voice intelligence, omnichannel collaboration, and embedded communication APIs. Nearly 45% of new deployments now integrate workflow automation capabilities. Rising enterprise compliance requirements and distributed workforce management needs are accelerating adoption, setting the stage for broader strategic transformation across communication ecosystems.

Cloud-Based Private Branch Exchange (PBX) systems are becoming strategically critical as enterprises seek communication environments that support workforce mobility, customer engagement, and digital operating models. The market's importance extends beyond voice communication into broader business transformation initiatives where integrated collaboration platforms influence productivity, customer retention, and operational responsiveness. Enterprise infrastructure modernization and increasing cloud-first procurement policies are accelerating replacement cycles for traditional telephony assets.

Modern cloud PBX platforms deliver measurable advantages over legacy on-premise systems. Organizations commonly achieve deployment timelines that are 60–70% faster while reducing communication administration workloads by approximately 40%. In the United States, large enterprises are prioritizing AI-enabled communication ecosystems, while Japan and Germany focus heavily on secure cloud communication frameworks and compliance-driven deployments. Over the next two to three years, AI-assisted call management and automated customer interaction capabilities are expected to become standard enterprise requirements.

A practical example can be seen among multinational service providers consolidating multiple communication vendors into unified cloud environments, reducing infrastructure complexity and improving service consistency across locations. Vendors are expanding strategic partnerships with cloud providers, CRM developers, and AI technology firms to strengthen ecosystem capabilities. Organizations that align communication infrastructure with broader digital transformation objectives will secure stronger operational agility, improved customer experience, and more durable competitive positioning.

The strongest growth catalyst is the replacement of aging on-premise telephony infrastructure with cloud-native communication platforms. More than 65% of large enterprises now support hybrid work models, while AI-enabled communication deployments have increased by over 40% during the past three years. The rapid expansion of distributed workforces following global workplace restructuring has increased demand for location-independent communication environments. This shift improves workforce accessibility, customer response quality, and business continuity. In response, technology providers are expanding data center capacity, integrating advanced analytics, and forming partnerships with collaboration software vendors. A notable strategic insight is that enterprises increasingly view cloud PBX investments as productivity infrastructure rather than telecom expenditure, accelerating board-level approval for deployment programs and long-term platform standardization initiatives.

Data localization regulations and interoperability requirements remain significant barriers to deployment. Approximately 39% of enterprises cite compliance obligations as a major implementation concern, while nearly 32% report integration challenges with legacy ERP, CRM, and contact-center environments. In Germany and several Asia-Pacific markets, stricter data residency requirements increase deployment complexity and vendor qualification timelines. These constraints elevate implementation costs and extend migration schedules. Companies are mitigating exposure through regional hosting strategies, localized cloud infrastructure investments, and expanded compliance certifications. An important operational insight is that organizations operating across multiple jurisdictions often require hybrid communication architectures, increasing system complexity and delaying full cloud migration despite clear efficiency advantages.

A major opportunity lies in integrating AI and automation directly into enterprise communication workflows. More than 50% of enterprises are evaluating conversational AI tools, while intelligent call routing can reduce customer handling times by nearly 25%. The emergence of embedded communications, communications-platform-as-a-service (CPaaS), and workflow automation creates new monetization opportunities beyond traditional voice services. India is emerging as a key deployment hub due to expanding cloud adoption among SMEs and digital service providers. Vendors are increasing R&D investments, acquiring AI capabilities, and building ecosystem partnerships with CRM and productivity software developers. A less obvious opportunity is the growing demand for communication analytics that convert customer interaction data into operational intelligence and sales optimization insights.

As communication platforms become more interconnected, cybersecurity and scalability pressures intensify. Industry surveys indicate that approximately 47% of enterprises rank communication security among their top cloud concerns, while voice-related cyber incidents have increased by more than 20% in recent years. High-volume environments handling thousands of concurrent interactions require resilient network architecture and consistent service quality. In the United States and the United Kingdom, stricter cybersecurity expectations are increasing vendor accountability and compliance obligations. Failure to maintain service reliability can directly affect customer experience, productivity, and enterprise trust. Vendors must invest in advanced threat detection, zero-trust security frameworks, and distributed infrastructure architectures to ensure sustainable growth and maintain competitive relevance in increasingly complex enterprise environments.

AI-Powered Call Intelligence Expansion Enterprise adoption of AI-enabled PBX functions has increased by nearly 42%, while automated call routing deployment has exceeded 55% among large organizations. Businesses are integrating conversational analytics, sentiment detection, and intelligent workflow automation directly into communication platforms. This shift is reducing average call handling times by approximately 20% and improving first-contact resolution rates. Vendors are expanding AI partnerships and embedding machine-learning capabilities into core communication stacks to differentiate enterprise offerings.

Unified Communications Platform Consolidation More than 60% of multinational enterprises are consolidating separate voice, messaging, and collaboration tools into unified cloud communication environments. Following workforce decentralization and IT cost optimization initiatives, organizations are reducing vendor complexity while improving communication governance. Platform consolidation has lowered communication administration workloads by nearly 30% in several enterprise deployments. Providers are responding through ecosystem partnerships, API expansion, and integrated productivity suite development to strengthen platform stickiness.

Compliance-Centric Cloud Deployments Data residency requirements and cybersecurity regulations are reshaping deployment strategies across Germany, Japan, and the United Kingdom. Nearly 38% of enterprise buyers now rank compliance capabilities among their top procurement criteria, while demand for localized hosting environments has increased by over 25%. Providers are investing in regional infrastructure, advanced encryption frameworks, and compliance certifications to address evolving governance requirements and accelerate enterprise onboarding.

Embedded Communication Workflow Growth Adoption of embedded communication capabilities within CRM, ERP, and customer service platforms has risen by approximately 48% over the past two years. Rather than treating telephony as a standalone function, enterprises are integrating voice workflows directly into operational systems. This approach improves employee productivity by nearly 22% and reduces application switching. Technology vendors are accelerating API development, automation frameworks, and strategic software alliances to support increasingly workflow-centric communication environments.

Hosted PBX remains the leading segment, accounting for an estimated 46% of total market adoption due to its lower infrastructure requirements, centralized management capabilities, and rapid deployment advantages. Enterprises increasingly prefer hosted environments because they eliminate hardware maintenance costs while supporting distributed workforce communication needs. Large organizations with multiple branch locations are accelerating migration programs, with deployment rates exceeding 60% among cloud-first enterprises. Vendors continue expanding managed service capabilities and AI-enabled administration tools to strengthen value propositions.mVirtual PBX represents the fastest-growing segment as small and medium-sized businesses seek affordable communication modernization without significant IT investment. Adoption within SMB environments has increased by nearly 35% over the past three years. Hybrid Cloud PBX solutions are also gaining traction among regulated industries requiring greater control over communication infrastructure and data handling. Unified Communications (UC)-Integrated PBX platforms remain strategically important as enterprises increasingly consolidate collaboration, messaging, and voice services into a single environment. Vendors are prioritizing product integration, ecosystem partnerships, and automation capabilities to address evolving customer requirements and improve platform differentiation.

Unified Communications & Collaboration represents the largest application segment, contributing approximately 41% of overall deployment activity. Organizations are prioritizing integrated voice, messaging, video conferencing, and team collaboration capabilities to support hybrid work environments and operational efficiency. Enterprise demand remains concentrated in sectors where employee coordination, customer engagement, and workforce mobility directly influence performance outcomes. Adoption rates among large enterprises now exceed 65%, reflecting the strategic importance of integrated communication ecosystems. Customer Service & Contact Center applications are the fastest-growing segment as businesses deploy AI-assisted routing, omnichannel engagement tools, and customer interaction analytics. Adoption has expanded by nearly 38% across service-intensive industries. Voice Communication & Telephony continues to represent a mature but essential use case, particularly among organizations replacing legacy systems. Meanwhile, Remote Workforce Management applications are gaining momentum as employers prioritize flexible operating models and workforce productivity monitoring. Vendors are expanding integrations with CRM platforms, workflow software, and automation solutions to improve communication visibility and enhance operational responsiveness across enterprise environments.

Large Enterprises constitute the dominant end-user segment, representing approximately 52% of market demand due to extensive communication requirements, multi-site operations, and complex collaboration needs. These organizations typically deploy advanced PBX environments integrated with CRM, ERP, cybersecurity, and workforce management platforms. Communication standardization initiatives and digital workplace transformation programs continue driving investment activity. Vendors increasingly target this segment through customized deployment models, advanced analytics capabilities, and enterprise-grade service agreements. Small & Medium Enterprises (SMEs) represent the fastest-growing end-user category as cloud delivery models reduce deployment barriers and upfront infrastructure costs. Adoption among SMEs has increased by nearly 40% as businesses seek scalable communication systems supporting customer engagement and workforce flexibility. Government & Public Sector organizations continue expanding cloud communication investments to improve citizen services and operational efficiency, while Healthcare and BFSI sectors remain strategically significant due to secure communication requirements and regulatory compliance demands. Providers are responding through industry-specific offerings, subscription-based pricing models, and strategic partnerships that simplify deployment and improve accessibility for emerging customer groups.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

North America maintains its leadership position through high enterprise cloud maturity, advanced telecom infrastructure, and strong adoption of unified communication ecosystems. The region accounts for approximately 38% of global deployments, supported by widespread migration from legacy PBX systems to cloud-native communication environments. Large enterprises increasingly integrate voice, messaging, video collaboration, and AI-powered customer engagement within single communication platforms. More than 65% of medium and large organizations have implemented hybrid workplace strategies, reinforcing demand for scalable cloud communication infrastructure. Strategic partnerships among telecom operators, software providers, and hyperscale cloud companies continue strengthening deployment capabilities and accelerating enterprise modernization initiatives.

United States Market Outlook: The United States represents the largest country market due to its concentration of multinational enterprises, advanced cloud infrastructure, and mature SaaS ecosystem. Enterprise cloud communication penetration exceeds 65%, supported by extensive deployment across financial services, healthcare, retail, and technology sectors. Organizations are increasingly deploying AI-assisted call analytics, automated routing systems, and integrated collaboration platforms. Strong investment in digital workplace transformation and customer experience modernization continues to position the country as a primary innovation hub for cloud-based communication technologies.

Europe remains a strategically important market, accounting for nearly 27% of global adoption. Demand is strongly influenced by enterprise modernization initiatives, cybersecurity requirements, and data governance regulations. Organizations increasingly prioritize secure communication environments capable of supporting distributed operations while maintaining regulatory compliance. Cloud communication deployments across enterprise environments have increased by more than 30% over recent years as organizations replace aging telephony infrastructure. Regional providers are expanding local hosting capabilities and strengthening security frameworks to align with evolving compliance expectations. Integration between communication platforms and business applications is becoming a standard procurement requirement.

Germany Market Outlook: Germany leads the regional market through its strong industrial base, advanced enterprise IT infrastructure, and high concentration of medium-sized manufacturing companies. Cloud communication adoption among large enterprises continues to expand as organizations modernize operational technology and customer service environments. More than 50% of enterprise communication transformation projects now include cloud-based collaboration capabilities. German organizations place particular emphasis on secure deployment architectures, interoperability standards, and long-term digital infrastructure planning, making the country a major driver of advanced communication platform investments.

Asia-Pacific accounts for approximately 24% of the global market and represents the fastest-evolving deployment environment. Rapid cloud adoption among enterprises, expanding digital economies, and increasing demand for workforce mobility solutions are accelerating implementation activity. Small and medium-sized businesses account for a significant share of new deployments as subscription-based communication models reduce infrastructure barriers. Cloud communication adoption across enterprise environments has increased by nearly 40% in several major economies. Technology vendors are expanding regional data center footprints, partner ecosystems, and localized service capabilities to support growing demand across diverse industry verticals.

China Market Outlook: China serves as the region’s largest market due to its extensive enterprise base, expanding cloud infrastructure, and large-scale digital transformation initiatives. Domestic businesses are increasingly replacing traditional communication systems with integrated cloud collaboration platforms supporting operational efficiency and customer engagement. Enterprise cloud adoption continues to expand across manufacturing, e-commerce, financial services, and technology sectors. Strong investments in digital infrastructure and AI-enabled business applications are reinforcing China's position as a major deployment and innovation center within the global cloud communication landscape.

South America represents approximately 6% of global market activity, supported by growing enterprise digitization and increasing demand for cost-efficient communication infrastructure. Organizations are modernizing communication environments to improve operational flexibility and support geographically dispersed workforces. Cloud communication deployments among mid-sized enterprises have increased by nearly 28% as businesses seek scalable alternatives to hardware-intensive systems. However, infrastructure disparities and uneven broadband availability continue influencing deployment speed across certain markets. Service providers are responding through localized partnerships, managed service offerings, and flexible subscription models designed to lower adoption barriers and improve accessibility.

Brazil Market Outlook: Brazil dominates regional demand through its large enterprise sector, expanding digital economy, and improving cloud infrastructure environment. Businesses across banking, telecommunications, retail, and professional services increasingly adopt cloud-based communication platforms to improve customer engagement and workforce collaboration. Enterprise cloud service utilization has expanded significantly over the past several years, supported by ongoing digital transformation initiatives. Local technology partnerships and growing investment in enterprise software ecosystems continue strengthening Brazil’s position as the region’s primary cloud communication market.

The Middle East & Africa region accounts for approximately 5% of global demand and is experiencing steady adoption driven by infrastructure modernization and public-sector digitization initiatives. Governments and enterprises are increasingly investing in cloud technologies to improve operational efficiency, citizen services, and business connectivity. Cloud communication deployment activity has increased by more than 25% across key markets as organizations prioritize scalable and centralized communication architectures. Expanding data center investments and enterprise technology partnerships are improving platform availability while supporting long-term digital transformation objectives across both public and private sectors.

United Arab Emirates Market Outlook: The United Arab Emirates represents the most strategically significant market within the region due to its advanced digital infrastructure, cloud-first government initiatives, and strong enterprise technology adoption. Organizations across financial services, aviation, hospitality, and government sectors are deploying integrated communication platforms to support operational agility and customer experience enhancement. More than 70% of large enterprises have accelerated cloud adoption strategies as part of broader digital transformation programs. Continued investment in smart infrastructure, technology partnerships, and innovation ecosystems reinforces the UAE’s leadership position within the regional cloud communication landscape.

The Cloud-Based Private Branch Exchange (PBX) System market is led by RingCentral, Cisco, Microsoft, Zoom, and 8x8, which collectively control approximately 52% of global market activity. Competition is increasingly defined by global UCaaS leaders competing against regional telecom-integrated providers, while AI-focused communication vendors challenge traditional voice-centric platforms. Technology capability now outweighs pricing alone, with enterprises reporting up to 35% higher platform retention when AI automation and workflow integration are embedded within communication systems. Deployment speed has become another differentiator, with cloud-native solutions reducing implementation timelines by nearly 60% compared with legacy environments. Leading vendors are expanding through strategic partnerships, AI-driven product development, and ecosystem integration with CRM, ERP, and productivity software providers. Market consolidation is accelerating as communication, contact center, and collaboration functions converge into unified platforms. The primary entry barrier remains enterprise-scale infrastructure, security compliance, and ecosystem depth. Winning requires superior AI functionality, seamless integrations, enterprise-grade reliability, and scalable customer experience outcomes.

Cisco Systems

Microsoft Corporation

Zoom Communications

8x8 Inc.

Nextiva

Dialpad

Vonage

GoTo

Mitel Networks

Avaya

Ooma Inc.

Aircall

NTT Communications

Cloud PBX platforms are rapidly evolving from hosted telephony solutions into intelligent communication ecosystems. AI-powered call routing, conversational analytics, and automated virtual receptionists are becoming standard deployment requirements. Enterprises implementing AI-assisted communication workflows report operational efficiency improvements of 20–30%, while automated call handling reduces routine interaction workloads by approximately 25%. More than 50% of new enterprise deployments now include integrated analytics and automation capabilities. Vendors that combine communication services with AI-enabled customer engagement tools are gaining a significant competitive advantage.

The strongest technology transition is occurring between traditional rule-based call management and AI-driven communication orchestration. Modern AI-enabled platforms improve routing accuracy by nearly 35% and reduce average response times by more than 20% compared with conventional PBX architectures. API-first integration frameworks are also accelerating adoption, allowing communication systems to connect directly with CRM, ERP, and workflow applications. Organizations deploying integrated communication environments report productivity gains approaching 22% through reduced application switching and improved collaboration visibility.

Between 2026 and 2028, generative AI assistants, autonomous customer interaction agents, and predictive communication analytics will reshape enterprise communications. Nearly 60% of large organizations are expected to prioritize AI-native communication platforms during technology refresh cycles. Companies adopting these technologies early will benefit from faster customer engagement, lower administrative overhead, stronger workforce productivity, and improved long-term platform scalability.

October 2024 – Cisco Systems launched Webex AI Agent and AI Agent Studio for contact-center automation. The platform is designed to automate customer inquiries and improve interaction efficiency, supporting faster issue resolution and enhanced service delivery across enterprise communication environments. Business impact: stronger AI-led differentiation in cloud communications. Source: www.newsroom.cisco.com

June 2024 – Cisco Systems announced a USD 1 billion Global AI Investment Fund alongside new AI-powered communication and collaboration innovations. The initiative expanded AI capabilities across networking, security, and workplace communications. Business impact: accelerated AI ecosystem development and enterprise adoption of intelligent communication infrastructure.

February 2025 – RingCentral introduced RingCentral AI Receptionist (AIR), an embedded AI phone agent that automates customer inquiries and call transfers. The solution requires no complex deployment and supports businesses of multiple sizes. Business impact: expanded AI-driven call automation and reduced front-desk operational workload.

February 2025 – RingCentral and BT launched Cloud Work RingCX, an AI-powered cloud contact-center platform supporting BT’s network serving more than 1 million business and public-sector customers. The solution integrates voice and messaging workflows. Business impact: strengthened enterprise contact-center modernization and expanded cloud communication deployment opportunities.

This report provides comprehensive coverage of the Cloud-Based Private Branch Exchange (PBX) System market across Hosted PBX, Virtual PBX, Hybrid Cloud PBX, and UC-Integrated PBX solutions. The assessment evaluates deployment patterns across unified communications, customer service and contact center operations, voice communication, and remote workforce management applications. Analysis extends across large enterprises, small and medium enterprises, government organizations, healthcare institutions, financial services providers, and other key industry participants driving communication modernization initiatives.

The study examines competitive positioning, technology adoption trends, enterprise deployment strategies, and regional market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 60% of current enterprise deployments emphasize integrated collaboration and automation capabilities, reflecting changing communication priorities. The report also evaluates AI-powered communication technologies, embedded workflow integrations, cloud infrastructure developments, and emerging business models. Strategic insights support investment planning, expansion decisions, partnership development, competitive benchmarking, and long-term market positioning through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,548.0 Million |

| Market Revenue (2033) | USD 7,345.3 Million |

| CAGR (2026–2033) | 14.15% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | RingCentral; Cisco Systems; Microsoft Corporation; Zoom Communications; 8x8 Inc.; Nextiva; Dialpad; Vonage; GoTo; Mitel Networks; Avaya; Ooma Inc.; Aircall; NTT Communications |

| Customization & Pricing | Available on Request (10% Customization Free) |