Reports

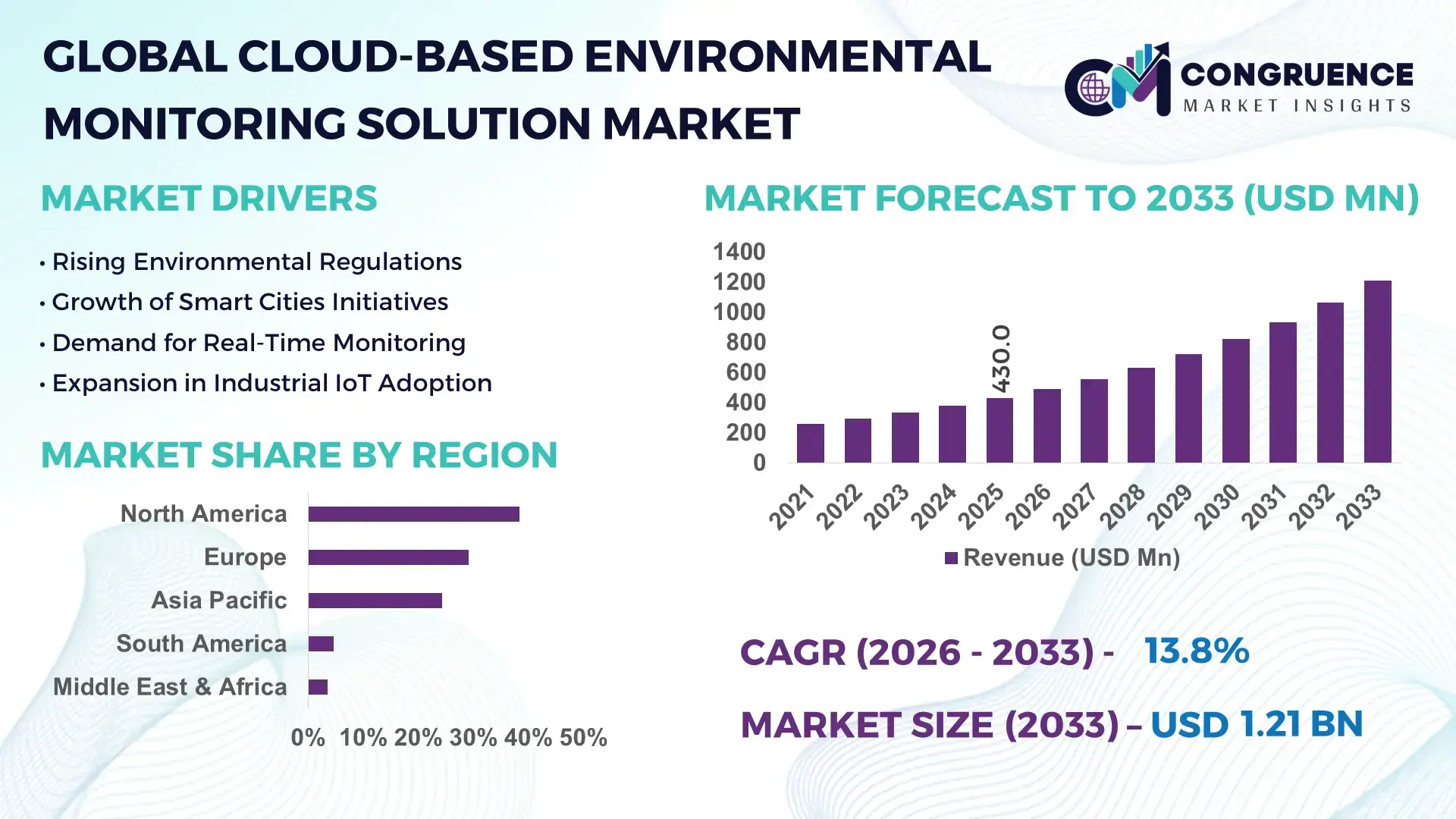

The Global Cloud-based Environmental Monitoring Solution Market was valued at USD 430.0 Million in 2025 and is anticipated to reach a value of USD 1,209.5 Million by 2033 expanding at a CAGR of 13.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rising integration of IoT sensors with cloud analytics to enable real-time, compliance-ready environmental intelligence across industrial and urban ecosystems.

The United States represents the most advanced production and deployment base for cloud-based environmental monitoring solutions, supported by over 35 large-scale data centers dedicated to environmental analytics workloads and more than USD 4.2 billion in cumulative investments in smart environment platforms since 2020. The country hosts over 45% of global hyperscale cloud infrastructure supporting environmental data processing. Key applications span air quality management in 120+ smart cities, water quality monitoring across 65% of major river basins, and industrial emissions tracking across more than 18,000 manufacturing sites. Technologically, over 70% of U.S. environmental monitoring platforms now integrate AI-driven anomaly detection and edge-cloud hybrid architectures, enabling sub-5-second alerting and predictive compliance reporting.

Market Size & Growth: USD 430.0 Million (2025) projected to reach USD 1,209.5 Million by 2033 at 13.8% CAGR, driven by real-time compliance automation and smart infrastructure expansion.

Top Growth Drivers: IoT adoption (68%), cloud migration in utilities (61%), regulatory digitalization mandates (54%).

Short-Term Forecast: By 2028, cloud-based monitoring is expected to reduce environmental compliance costs by 27% across industrial users.

Emerging Technologies: AI-based anomaly detection, edge-cloud hybrid monitoring, and digital twin-based environmental simulation.

Regional Leaders: North America (USD 410M by 2033 – smart city analytics), Europe (USD 360M – regulatory-driven adoption), Asia-Pacific (USD 310M – industrial pollution control).

Consumer/End-User Trends: Utilities and manufacturing account for 62% usage, with municipal smart city projects contributing 24%.

Pilot or Case Example: In 2024, Singapore’s cloud-based water quality pilot reduced response time by 38% and leakage losses by 22%.

Competitive Landscape: Market leader holds ~18% share, followed by IBM, Siemens, Oracle, SAP, and Honeywell.

Regulatory & ESG Impact: Carbon reporting mandates and ISO 14001 digital compliance tools accelerating adoption by over 45% among listed firms.

Investment & Funding Patterns: Over USD 6.5 Billion invested globally since 2020, with strong venture inflows into AI-driven monitoring startups.

Innovation & Future Outlook: Integration with autonomous sensors and climate-risk analytics shaping next-generation monitoring ecosystems.

Cloud-based Environmental Monitoring Solution Market integrates industrial (38%), municipal (24%), energy (20%), and agriculture (18%) sectors, driven by AI-enabled analytics, digital compliance platforms, and smart sensor integration. Regulatory carbon disclosure norms, climate risk reporting, and urban pollution controls are accelerating adoption, particularly in North America and Europe. Asia-Pacific shows fastest industrial uptake due to environmental digitization mandates. Emerging trends include predictive pollution modeling, ESG-linked cloud dashboards, and climate-resilience analytics shaping future solution architectures.

The Cloud-based Environmental Monitoring Solution Market is becoming strategically indispensable as enterprises and governments transition from reactive environmental compliance to proactive, data-driven sustainability management. These platforms centralize multi-source environmental data, enabling real-time visibility across air, water, soil, and emissions metrics, thereby transforming environmental governance into a continuous, auditable digital function.

From a strategic efficiency standpoint, AI-powered cloud monitoring delivers up to 42% faster anomaly detection compared to manual sampling-based monitoring standards, significantly reducing environmental incident response times. In operational benchmarking, AI-driven predictive monitoring delivers 35% improvement compared to traditional threshold-based alert systems, allowing organizations to prevent violations rather than merely report them.

Regionally, North America dominates in volume of deployments, while Europe leads in adoption with over 58% of large enterprises integrating cloud-based environmental monitoring into ESG reporting systems. Asia-Pacific, meanwhile, is emerging as a scale-driven growth region, with over 2,500 industrial parks adopting centralized cloud environmental platforms.

By 2029, the integration of AI-driven climate-risk analytics is expected to improve pollution forecasting accuracy by 31%, enabling governments to implement preventive regulatory interventions rather than corrective penalties. On the ESG front, firms are committing to carbon intensity reductions of 30–40% by 2035, with cloud-based monitoring forming the backbone of digital carbon accounting and verification.

In 2024, Japan achieved a 26% reduction in urban particulate matter exceedances through nationwide cloud-linked air quality monitoring combined with AI traffic flow optimization.

Looking forward, the Cloud-based Environmental Monitoring Solution Market will serve as a cornerstone of environmental resilience, regulatory compliance, and sustainable growth by embedding real-time intelligence into climate governance, infrastructure planning, and corporate sustainability frameworks.

The Cloud-based Environmental Monitoring Solution Market is shaped by the convergence of digital transformation, regulatory digitization, and sustainability-driven operational reforms. Governments and industries are increasingly replacing fragmented, manual environmental monitoring systems with centralized cloud platforms capable of processing high-frequency sensor data in real time. The proliferation of IoT devices, declining cloud storage costs, and advancements in AI-based environmental analytics are redefining how environmental data is captured, interpreted, and acted upon. Moreover, rising urbanization and industrial density are intensifying the need for continuous monitoring of air quality, water contamination, and emissions. At the same time, enterprises are embedding environmental data into enterprise risk management and ESG reporting structures, elevating monitoring from a compliance tool to a strategic decision-support system. These dynamics collectively position cloud-based environmental monitoring as a critical digital infrastructure layer for modern environmental governance.

Regulatory authorities across major economies are mandating continuous environmental reporting rather than periodic disclosures, significantly driving demand for cloud-based monitoring platforms. Over 70 countries now require digital submission of emissions and pollution data, increasing reliance on automated, cloud-integrated systems. In the European Union alone, more than 45,000 industrial facilities are obligated to report environmental metrics through centralized digital portals. Cloud-based solutions enable real-time compliance tracking, automated alerts, and audit-ready reporting, reducing non-compliance risks by over 30%. Additionally, environmental permits increasingly require high-frequency data logging, which traditional on-premise systems struggle to manage efficiently. As regulatory complexity grows and enforcement becomes more data-driven, cloud platforms are emerging as the most scalable and cost-effective compliance infrastructure for both public and private sector stakeholders.

Despite technological advantages, concerns around data security and sovereignty continue to restrain adoption in sensitive sectors. Environmental data often intersects with national infrastructure, defense installations, and critical utilities, making cloud storage subject to strict jurisdictional controls. In countries such as Germany, France, and India, over 40% of public sector environmental projects mandate local data residency, limiting the use of global cloud platforms. Cybersecurity risks also persist, with environmental monitoring systems increasingly targeted due to their linkage with industrial control systems. In 2023 alone, over 18% of reported cyber incidents in utilities involved environmental monitoring interfaces. These concerns force organizations to invest heavily in hybrid or private cloud architectures, increasing deployment complexity and slowing mass-market adoption.

Global smart city initiatives are unlocking substantial opportunities for cloud-based environmental monitoring solutions. Over 1,000 smart city projects worldwide now incorporate digital environmental management as a core pillar. These projects require continuous monitoring of air pollution, noise levels, water quality, and urban heat islands, all of which are optimally managed through cloud-based platforms. In Asia-Pacific alone, more than 350 smart cities are deploying centralized environmental data platforms connected to traffic, energy, and public health systems. This integration enables cross-domain analytics, such as correlating traffic congestion with pollution spikes, improving urban planning efficiency by over 25%. As urban populations continue to grow, cloud-enabled environmental intelligence is becoming foundational to sustainable city governance.

A major challenge in this market is the lack of standardized interoperability across diverse sensors, platforms, and regulatory systems. Environmental monitoring ecosystems often combine legacy hardware, proprietary sensor protocols, and multiple cloud providers, creating integration complexity. More than 60% of industrial users report difficulties in consolidating multi-vendor environmental data into a single analytics environment. Additionally, differences in data formats, calibration standards, and reporting frameworks across regions hinder seamless scalability. This fragmentation increases deployment timelines by up to 35% and raises long-term maintenance costs. Without broader adoption of open standards and interoperable frameworks, organizations face technical barriers that slow the full digital transformation of environmental monitoring infrastructures.

Rapid Integration of AI-Driven Predictive Analytics (Adopted by 47% of New Deployments): Nearly 47% of newly deployed cloud environmental monitoring platforms now integrate AI-based predictive analytics, enabling early identification of pollution events and system failures. These systems improve forecasting accuracy by over 30% compared to rule-based monitoring. Industrial users report a 24% reduction in unplanned shutdowns due to predictive alerts on air and water quality deviations, significantly enhancing operational resilience.

Expansion of Edge-Cloud Hybrid Monitoring Architectures (Used in 52% of Urban Projects): More than 52% of urban environmental monitoring projects now utilize edge-cloud hybrid models, allowing local processing of sensor data with cloud-based aggregation. This reduces data latency by 41% and improves real-time responsiveness in high-density urban zones. Hybrid architectures also lower bandwidth costs by approximately 28%, making large-scale sensor deployments economically viable.

Growth of ESG-Linked Environmental Dashboards (Adopted by 58% of Listed Enterprises): Around 58% of publicly listed enterprises have integrated cloud-based environmental dashboards into their ESG reporting systems. These platforms enable automated carbon, water, and waste tracking, reducing ESG reporting cycle times by 35% and improving audit accuracy by 22%, strengthening investor confidence and regulatory transparency.

Rising Use of Digital Twins for Environmental Simulation (Deployed in 34% of New Industrial Sites): Digital twin models are now used in 34% of newly built industrial facilities to simulate environmental impact under varying operational scenarios. This approach enables up to 29% optimization in pollution control investments and supports scenario-based compliance planning, significantly improving long-term sustainability performance.

The Cloud-based Environmental Monitoring Solution Market is segmented across type, application, and end-user, reflecting how technological configuration, operational use cases, and sectoral demand collectively shape adoption patterns. By type, solutions vary from real-time air and water monitoring platforms to advanced multi-parameter environmental intelligence systems, each addressing specific regulatory and operational requirements. Application-wise, the market spans industrial compliance, urban environmental management, climate research, and resource optimization, indicating its role beyond mere regulatory adherence toward strategic sustainability planning. From an end-user perspective, demand is concentrated among utilities, manufacturing enterprises, municipalities, and government agencies, with emerging traction in agriculture and healthcare infrastructure. The segmentation highlights a shift from isolated monitoring tools toward integrated, cloud-based decision-support ecosystems, where scalability, interoperability, and predictive capabilities determine competitive positioning. This layered segmentation underscores the market’s evolution from fragmented environmental sensing to unified digital environmental governance platforms.

The Cloud-based Environmental Monitoring Solution Market by type includes Air Quality Monitoring Systems, Water Quality Monitoring Systems, Soil and Waste Monitoring Systems, Noise Monitoring Systems, and Integrated Multi-Parameter Environmental Platforms. Air quality monitoring systems currently account for approximately 38% of total adoption, driven by urban pollution control mandates, industrial emissions tracking, and public health surveillance requirements. These systems are widely deployed in smart cities and industrial clusters to continuously assess particulate matter, NO₂, and CO₂ levels through cloud-connected sensors and AI analytics. Water quality monitoring platforms represent a major secondary segment, widely adopted across municipal utilities and industrial wastewater management. However, integrated multi-parameter platforms are the fastest-growing type, expanding at around 15.2% CAGR, as enterprises increasingly prefer unified dashboards that consolidate air, water, noise, and emissions data into a single cloud environment for compliance and operational optimization. Soil and waste monitoring systems and noise monitoring solutions collectively contribute around 29% of the remaining market, serving niche yet critical use cases in agriculture, construction, mining, and urban zoning. Their relevance is growing as environmental impact assessments become digitized and more frequent.

• In 2024, a national smart city initiative deployed cloud-based multi-parameter monitoring across over 90 urban zones, enabling real-time integration of air, noise, and water data to improve regulatory response times by more than 35%.

By application, the market is segmented into Industrial Environmental Compliance, Smart Cities & Urban Infrastructure, Energy & Utilities, Agriculture & Natural Resource Management, and Research & Climate Monitoring. Industrial environmental compliance remains the leading application, accounting for approximately 41% of total adoption, due to stringent emissions control requirements across manufacturing, chemicals, oil & gas, and mining. These platforms are used to automate regulatory reporting, detect violations early, and optimize pollution control investments. Smart cities and urban infrastructure applications are emerging rapidly, while energy and utilities applications are the fastest-growing, expanding at nearly 14.6% CAGR, supported by the integration of environmental intelligence into grid management, water utilities, and renewable energy forecasting. Utilities increasingly rely on cloud platforms to link environmental variables with asset performance and service reliability. Agriculture, natural resource management, and climate research together contribute about 34% of the remaining market, with cloud monitoring enabling precision irrigation, soil health analytics, and biodiversity tracking.

In 2025, more than 46% of global utilities reported integrating cloud-based environmental monitoring into operational planning systems, while over 39% of large enterprises piloted cloud platforms specifically for ESG-linked environmental reporting.

• In 2024, a national environmental agency implemented a cloud-based flood and water quality monitoring system across 150 river basins, improving early warning accuracy by over 28%.

By end-user, the Cloud-based Environmental Monitoring Solution Market is segmented into Utilities, Manufacturing & Industrial Enterprises, Government & Municipal Bodies, Energy Producers, Agriculture, and Commercial Infrastructure Operators. Utilities represent the leading end-user group, accounting for approximately 36% of total market adoption, driven by the need for continuous monitoring of water quality, emissions, and environmental compliance across large-scale infrastructure networks. Manufacturing and industrial enterprises follow closely, using cloud platforms to ensure regulatory adherence, reduce environmental risk exposure, and integrate sustainability into operational KPIs. Government and municipal bodies form another major segment, particularly in urban air quality management and public environmental transparency programs. Energy producers constitute the fastest-growing end-user segment, expanding at about 14.1% CAGR, as renewable integration, carbon tracking, and climate resilience planning become core to energy strategy. Other end-users—including agriculture, logistics hubs, healthcare infrastructure, and commercial real estate—collectively contribute around 33% of the market, supported by rising adoption of environmental intelligence in non-traditional sectors.

In 2025, nearly 44% of large industrial enterprises globally reported deploying cloud-based environmental platforms for real-time compliance monitoring, while over 31% of municipal governments adopted cloud dashboards for public environmental data disclosure.

• In 2024, a nationwide utility modernization program enabled over 200 water utilities to migrate to cloud-based environmental monitoring, reducing contamination response times by approximately 32%.

North America accounted for the largest market share at 38.4% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2026 and 2033.

Europe followed North America with a 29.1% share, driven by regulatory digitalization and ESG-linked compliance platforms, while Asia-Pacific held 24.3%, supported by industrialization and smart city deployments. South America and the Middle East & Africa jointly represented 8.2%, reflecting emerging but strategically significant adoption. Over 62% of global cloud-based environmental monitoring deployments are concentrated across North America and Europe, whereas Asia-Pacific accounts for nearly 47% of new industrial installations annually. Urban air quality platforms constitute over 41% of regional demand globally, while water and emissions monitoring collectively contribute over 46%. Cross-region investments in AI-driven environmental platforms have increased by more than 55% since 2021, underlining the global shift toward digitized environmental governance infrastructures.

North America holds approximately 38.4% market share, making it the largest regional contributor to the Cloud-based Environmental Monitoring Solution Market. The region is driven primarily by utilities, manufacturing, oil & gas, healthcare infrastructure, and smart city operators. Regulatory programs enforcing digital emissions reporting across over 70% of industrial facilities have accelerated adoption. Technologically, more than 64% of deployments integrate AI-based anomaly detection and real-time regulatory dashboards. Digital transformation initiatives across municipalities have led to cloud-based monitoring adoption in over 120 smart cities. A leading regional player has expanded cloud-based air and water analytics across 18 U.S. states, enabling automated compliance and predictive maintenance. Higher enterprise adoption is observed in healthcare and finance-linked infrastructure, where environmental compliance and risk analytics are tightly integrated into corporate governance frameworks.

Europe commands around 29.1% market share, with Germany, the UK, and France collectively accounting for over 61% of regional deployments. Strong sustainability frameworks, carbon disclosure mandates, and environmental transparency regulations are central growth drivers. More than 58% of European large enterprises have embedded cloud-based environmental monitoring into ESG reporting systems. Emerging technologies such as explainable AI, digital twins, and federated cloud architectures are increasingly adopted to meet regulatory auditability requirements. A prominent European technology provider has implemented pan-regional water quality analytics across over 40 river basins, improving contamination response coordination. Regulatory pressure leads to higher demand for explainable and auditable environmental analytics platforms compared to other regions.

Asia-Pacific ranks as the fastest-growing regional market, contributing approximately 24.3% of global volume, with China, India, and Japan representing over 72% of regional consumption. The region leads in new industrial installations, accounting for nearly 47% of annual global industrial cloud-based monitoring deployments. Rapid infrastructure expansion, industrial parks digitization, and smart city programs across over 300 urban centers are driving adoption. Regional innovation hubs in Shenzhen, Bangalore, and Tokyo are developing AI-based pollution forecasting and edge-cloud hybrid monitoring systems. A major regional technology firm recently deployed cloud-based emissions platforms across 250 manufacturing clusters. Growth is driven by infrastructure digitization, industrial compliance automation, and mobile-enabled environmental analytics in urban ecosystems.

South America holds approximately 4.7% market share, led by Brazil and Argentina, which together represent over 68% of regional demand. Growth is primarily driven by energy sector modernization, mining operations, and large-scale infrastructure development. Over 45% of new energy projects in Brazil now incorporate cloud-based environmental monitoring for emissions and water quality. Government incentives linked to clean energy and environmental transparency are encouraging digital adoption. A regional utility group has implemented cloud-based river pollution tracking across 1,200 km of waterways. Adoption is closely tied to infrastructure projects and export-oriented industries requiring environmental compliance for international trade.

Middle East & Africa account for around 3.5% of global market share, with UAE, Saudi Arabia, and South Africa as key growth countries. Demand is strongly linked to oil & gas operations, large-scale construction, and water resource management. Over 52% of new oil & gas projects in the GCC region now integrate cloud-based emissions and leak detection systems. Smart city programs in the UAE and environmental digitization initiatives in South Africa are accelerating market penetration. A regional cloud service provider has deployed AI-based air quality monitoring across over 25 urban districts. Adoption is driven by infrastructure megaprojects and sustainability-linked investment mandates rather than SME-led digital transformation.

United States – 27.6% Market Share: Dominates due to high deployment density across utilities, smart cities, and industrial compliance systems supported by strong digital infrastructure.

China – 18.9% Market Share: Leads through large-scale industrial digitization, smart city expansion, and centralized environmental data governance platforms.

The competitive landscape of the Cloud-based Environmental Monitoring Solution Market is characterized by a moderately consolidated yet dynamically evolving structure, with 25+ active competitors spanning global cloud infrastructure leaders, industrial technology conglomerates, and specialized environmental intelligence firms. Top-tier vendors, including IBM, Microsoft, AWS, Siemens, and Schneider Electric, collectively hold an estimated ~36–40% combined market share, reflecting both their deep cloud expertise and broad vertical integration across utilities, industrial automation, and smart infrastructure platforms. These established players are strategically investing in partnerships, advanced analytics capabilities, sensor interoperability, and turnkey environmental intelligence solutions to enhance real-time compliance, predictive insights, and ESG reporting functionality.

Innovation trends influencing competition include AI-based predictive analytics, edge-to-cloud hybrid monitoring architectures, digital twin implementations, open APIs for cross-platform interoperability, and automated regulatory reporting workflows. Strategic initiatives being pursued in recent years encompass collaborations between cloud and industrial automation firms, product launches with expanded multi-parameter sensor integration, and targeted acquisitions to strengthen regional presence. Emerging challengers such as Aclima, Envirosuite, EarthSense, Airthings, and Clarity Movement are carving niches with hyperlocal data models, urban-scale deployments, and highly customizable dashboards that appeal to municipalities, utilities, and ESG-focused enterprises.

The nature of the market reflects fragmentation at the solution-specialist level with consolidation among global cloud and automation incumbents shaping the broader competitive order. The evolving ecosystem underscores continuous technological upgrades, expanding partner networks, and aggressive go-to-market expansions especially in emerging regions.

Siemens AG

Schneider Electric SE

Oracle Corporation

General Electric (GE Digital)

Envirosuite Limited

Aclima Inc.

EarthSense Systems Ltd.

Bosch Sensortec GmbH

Sphera Solutions, Inc.

Airthings AS

Clarity Movement Co.

Aeroqual Ltd.

EMSOL Ltd.

EcoVadis SAS

Trimble Inc.

The Cloud-based Environmental Monitoring Solution Market is driven by a convergence of advanced technologies aimed at delivering real-time, scalable, and actionable environmental intelligence. Core technologies include IoT sensor networks, which collect high-frequency data across air quality, water quality, noise, and emissions parameters, enabling continuous visibility into environmental conditions across wide geographic footprints. These sensor networks are increasingly integrated with edge computing capabilities, reducing latency and optimizing bandwidth usage by locally preprocessing data before transmission to cloud analytics platforms.

Cloud-native platforms form the backbone of environmental monitoring, providing scalable storage, distributed processing, and advanced analytics capabilities. AI and machine learning algorithms play a pivotal role in identifying patterns, predicting anomalies, and generating actionable insights, with some implementations achieving 20–40% improvements in early detection accuracy compared to traditional threshold-based systems. Digital twin frameworks are emerging, enabling virtual replication of environmental systems to simulate scenarios and support strategic planning in infrastructure, industrial operations, and urban ecosystems.

Interoperability standards and open APIs are fostering greater integration between disparate sensor manufacturers and analytics solutions, reducing integration costs and supporting cross-domain insights. Hybrid architectures, combining edge AI processing with centralized cloud analytics, are gaining traction in regions where connectivity or regulatory constraints demand distributed intelligence. Furthermore, GIS and geospatial analytics technologies are enhancing the spatial contextualization of environmental data, aiding decision-makers in resource allocation, compliance reporting, and sustainability planning.

Security and data privacy technologies are equally critical, as sensitive environmental and operational data traverse public and private cloud environments. Encryption, role-based access controls, and industry-standard compliance frameworks ensure data integrity and trust in enterprise and public sector deployments. Advanced visualization tools, including dashboards and mobile apps, are enabling stakeholder access to real-time insights, supporting both tactical operations and strategic ESG reporting.

• In October 2025, CLS completed the acquisition of Ground Control, a specialist in satellite IoT devices and cloud-based environmental monitoring platforms, expanding CLS’s global footprint to 35 offices and over 1,100 employees to deliver enhanced remote environmental and infrastructure monitoring solutions. Source: www.iotm2mcouncil.org

• In late 2025, Monnit’s Environmental Monitoring Solution was recognized with the 2025 Smart City Product of the Year Award, highlighting its cloud-integrated IoT sensors and gateways used for real-time climate, energy, water, and HVAC data in smart buildings and cities. Source: www.monnit.com

• In December 2025, Aimtron Electronics entered an OEM agreement with Aurassure to locally manufacture IoT-enabled environmental and weather monitoring stations in India that transmit real-time parameters (PM2.5, PM10, humidity, wind speed, etc.) to cloud-based platforms for analytics and operational use. Source: www.manufacturing.economictimes.indiatimes.com

• In August 2024, Honeywell introduced an end-to-end emissions monitoring solution certified for hazardous offshore environments, integrating cloud-ready emissions tracking with its Versatilis Signal Scout hardware for offshore oil & gas and marine applications. Source: www.honeywell.com

The Cloud-based Environmental Monitoring Solution Market Report provides an expansive, multi-dimensional assessment of environmental intelligence platforms delivered via cloud infrastructure. The report covers market segmentation by type—air monitoring, water quality, soil and noise monitoring, biodiversity, and climate change analytics—highlighting technological distinctions and operational applications across industry verticals. It also includes segmentation by application, such as industrial compliance, smart city infrastructure, energy & utilities oversight, agriculture sustainability, and climate research, offering insights into how cloud-hosted environmental solutions are tailored for sector-specific challenges.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed analyses of regional adoption patterns, regulatory environments, infrastructure readiness, and consumer behavior variations influencing deployment strategies. The report also examines end-user categories, including utilities, manufacturing enterprises, government municipalities, and commercial operators, illustrating how environmental monitoring supports compliance, operational resilience, risk management, and ESG reporting.

From a technological viewpoint, the report delves into IoT and sensor ecosystems, edge-cloud architectures, AI and machine learning integration, digital twin frameworks, geospatial analytics, and interoperability standards, emphasizing how these innovations enhance real-time data fidelity and decision support. Additionally, it profiles deployment modes (public, private, hybrid cloud) and explores the impact of cybersecurity, data governance, and platform scalability on enterprise adoption.

In summary, the report furnishes decision-makers with a comprehensive view of market dynamics, competitive positioning, technological trends, and growth opportunities, enabling strategic investments, vendor selection, and roadmap planning across the evolving landscape of cloud-based environmental monitoring solutions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 430.0 Million |

| Market Revenue (2033) | USD 1,209.5 Million |

| CAGR (2026–2033) | 13.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | IBM Corporation, Microsoft Corporation, Amazon Web Services (AWS), Siemens AG, Schneider Electric SE, Oracle Corporation, General Electric (GE Digital), Envirosuite Limited, Aclima Inc., EarthSense Systems Ltd., Bosch Sensortec GmbH, Sphera Solutions, Inc., Airthings AS, Clarity Movement Co., Aeroqual Ltd., EMSOL Ltd., EcoVadis SAS, Trimble Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |