Reports

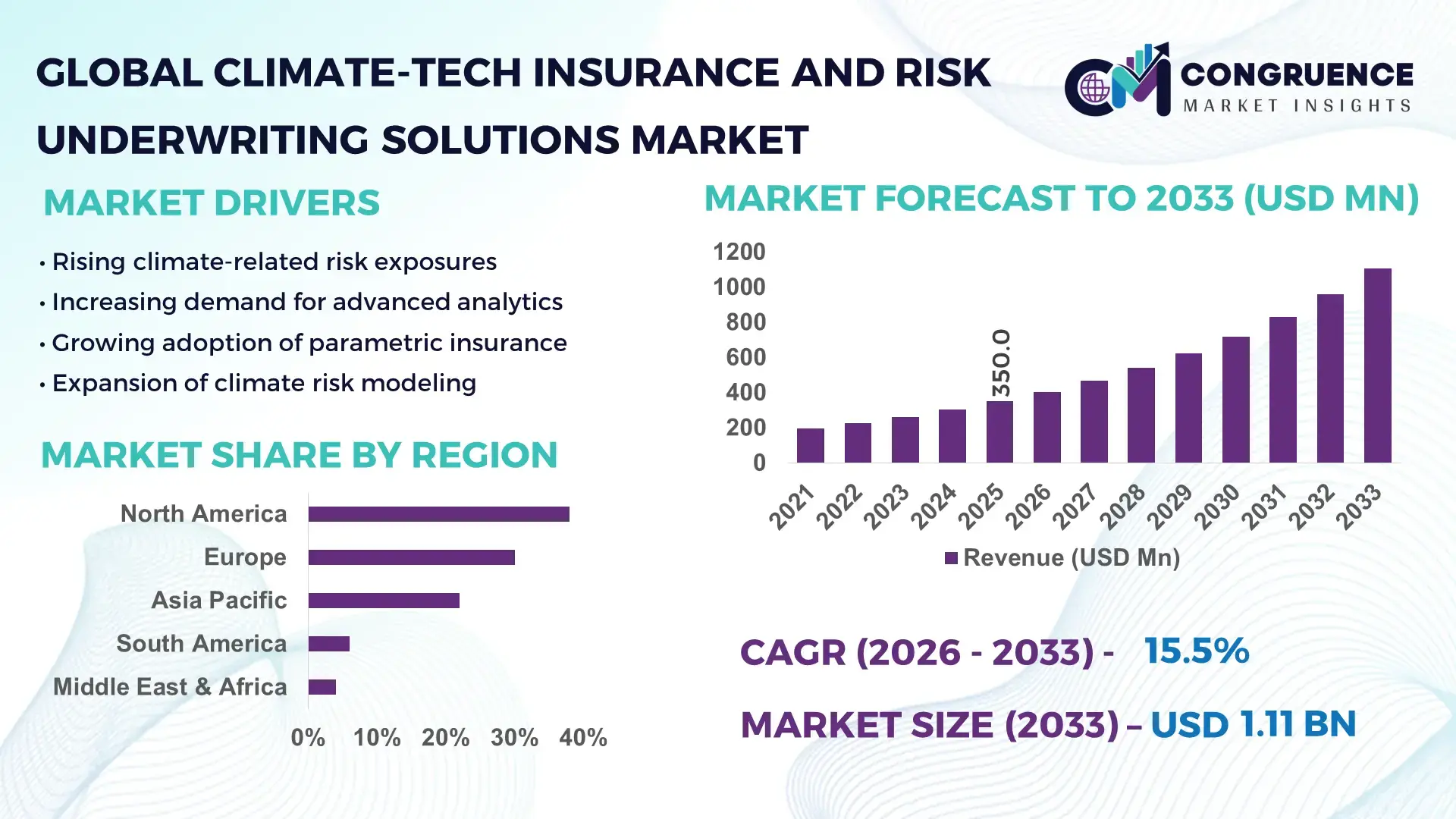

The Global Climate-Tech Insurance and Risk Underwriting Solutions Market was valued at USD 350.0 Million in 2025 and is anticipated to reach a value of USD 1,108.5 Million by 2033 expanding at a CAGR of 15.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing climate-related financial risks and the need for advanced data-driven underwriting models.

The United States leads the Climate-Tech Insurance and Risk Underwriting Solutions Market with over 45% of global climate-risk modeling infrastructure concentrated across its insurance and reinsurance ecosystem. More than 60% of large insurers in the country have integrated AI-based catastrophe modeling tools into underwriting workflows, while over USD 12 billion has been invested in climate risk analytics and insurtech platforms between 2020 and 2025. The country supports over 200 climate-tech startups specializing in risk analytics, with applications spanning property insurance, agriculture, and energy sectors. Additionally, nearly 55% of enterprises in high-risk regions such as California and Florida have adopted predictive climate risk scoring tools to enhance underwriting accuracy and reduce loss ratios.

Market Size & Growth: USD 350.0 Million in 2025, projected to reach USD 1,108.5 Million by 2033, expanding at 15.5%, driven by rising climate-related financial exposure and demand for predictive risk analytics.

Top Growth Drivers: Climate risk data adoption (68%), AI underwriting efficiency gains (52%), regulatory compliance demand (47%).

Short-Term Forecast: By 2028, automated underwriting platforms are expected to reduce risk assessment time by 35% and improve pricing accuracy by 28%.

Emerging Technologies: AI-based catastrophe modeling, satellite-driven risk analytics, blockchain-enabled parametric insurance solutions.

Regional Leaders: North America (~USD 420 Million by 2033) with strong insurtech adoption; Europe (~USD 310 Million) driven by regulatory mandates; Asia-Pacific (~USD 260 Million) fueled by climate vulnerability-driven demand.

Consumer/End-User Trends: Over 58% of insurers prioritize climate risk integration, with rising adoption among agriculture and property insurance providers.

Pilot or Case Example: In 2024, an AI-driven underwriting pilot reduced claim processing errors by 32% and improved loss prediction accuracy by 26%.

Competitive Landscape: Market leader holds ~18% share, followed by key players such as Swiss Re, Munich Re, RMS, and Aon.

Regulatory & ESG Impact: Over 70% of insurers are aligning with ESG frameworks, with mandatory climate risk disclosures expanding across 30+ countries.

Investment & Funding Patterns: Over USD 5 billion invested globally in climate insurtech platforms between 2021–2025, with increasing venture funding in predictive analytics startups.

Innovation & Future Outlook: Integration of IoT-based environmental sensors and real-time climate data platforms is expected to enhance underwriting precision by over 40%.

The market is characterized by strong contributions from property insurance (42%), agriculture insurance (27%), and energy sector coverage (18%). AI-powered catastrophe modeling tools have improved risk prediction accuracy by over 30%. Regulatory mandates across Europe and North America are accelerating adoption, while Asia-Pacific shows over 35% growth in climate-risk tool usage, driven by increasing climate-related disasters and digital insurance expansion.

The Climate-Tech Insurance and Risk Underwriting Solutions Market has become strategically critical as insurers and financial institutions face increasing exposure to climate-induced losses exceeding USD 300 billion annually across global markets. Advanced underwriting solutions powered by AI and geospatial analytics are enabling insurers to shift from reactive claims processing to proactive risk mitigation. For instance, AI-driven catastrophe models deliver 45% higher predictive accuracy compared to traditional actuarial methods, significantly improving underwriting efficiency and reducing claim volatility.

From a regional perspective, North America dominates in volume due to its mature insurance infrastructure, while Europe leads in adoption, with over 62% of insurers integrating climate-risk disclosures into underwriting processes. By 2028, AI-enabled climate risk platforms are expected to reduce underwriting cycle times by 30% while improving portfolio resilience metrics by 25%. Firms are committing to ESG-aligned underwriting strategies, targeting up to 40% reduction in carbon-intensive asset exposure by 2030.

In 2025, a leading reinsurer in Germany achieved a 28% improvement in loss prediction accuracy through satellite-based climate analytics integration. Similarly, insurers in Japan have deployed IoT-enabled environmental monitoring systems, reducing disaster-related claim uncertainties by 22%. The integration of blockchain in parametric insurance contracts has improved claim settlement speed by 35%, enhancing transparency and customer trust.

Looking ahead, the Climate-Tech Insurance and Risk Underwriting Solutions Market is positioned as a foundational pillar for financial resilience, regulatory compliance, and sustainable risk management. With increasing climate volatility and regulatory pressure, the market will continue to evolve through digital innovation, advanced analytics, and collaborative ecosystems, enabling insurers to build adaptive, future-ready underwriting frameworks.

The Climate-Tech Insurance and Risk Underwriting Solutions Market is evolving rapidly due to the growing frequency and severity of climate-related events, which have increased insured losses by over 35% globally in the past decade. Insurers are shifting toward advanced analytics and AI-driven underwriting tools to enhance predictive accuracy and manage exposure effectively. The integration of satellite data, IoT sensors, and geospatial analytics has improved real-time risk monitoring capabilities by nearly 40%, enabling insurers to refine pricing models and reduce claim volatility. Additionally, regulatory frameworks mandating climate risk disclosures are influencing underwriting strategies, particularly across Europe and North America. The market is also witnessing increased collaboration between insurtech firms and traditional insurers, with over 50% of large insurers engaging in strategic partnerships to enhance digital capabilities. Emerging economies are experiencing rapid adoption due to rising climate vulnerability, while technological advancements continue to redefine underwriting processes and operational efficiency.

The rising financial impact of climate-related disasters is a key driver of the Climate-Tech Insurance and Risk Underwriting Solutions Market. Global insured losses from natural catastrophes have exceeded USD 250 billion annually in recent years, pushing insurers to adopt advanced underwriting technologies. Over 65% of insurers have reported increased demand for climate risk analytics tools to improve loss forecasting and pricing accuracy. AI-driven models have enhanced predictive accuracy by up to 45%, enabling better risk segmentation and portfolio management. Additionally, sectors such as agriculture and property insurance have seen a 40% increase in demand for climate-based underwriting solutions due to rising exposure to floods, wildfires, and extreme weather events. Governments and regulatory bodies are also mandating climate risk assessments, further accelerating adoption. These factors collectively drive the transition toward data-driven underwriting systems, improving resilience and operational efficiency across the insurance ecosystem.

The high cost of implementing advanced climate-tech underwriting solutions remains a significant restraint for market growth. Deploying AI-based analytics platforms, satellite data integration, and real-time monitoring systems can increase operational costs by over 30% for insurers, particularly for small and mid-sized firms. Additionally, the complexity of integrating diverse data sources, including climate models, geospatial data, and historical loss datasets, poses challenges in achieving accurate risk assessments. Over 48% of insurers report difficulties in data standardization and interoperability across platforms. Limited access to high-quality climate data in developing regions further restricts adoption, affecting underwriting accuracy and scalability. Furthermore, the shortage of skilled professionals in data science and climate analytics has created a talent gap, impacting implementation timelines and efficiency. These challenges collectively hinder the widespread adoption of climate-tech underwriting solutions, particularly among smaller market participants.

The increasing adoption of digital technologies and parametric insurance models presents significant opportunities for the Climate-Tech Insurance and Risk Underwriting Solutions Market. Parametric insurance, which triggers payouts based on predefined climate events, has seen adoption growth of over 50% in recent years due to its efficiency and transparency. Digital platforms integrating AI, blockchain, and IoT technologies are enabling insurers to automate underwriting processes and improve claim settlement times by up to 35%. Emerging markets, particularly in Asia-Pacific and Africa, offer untapped potential, with climate risk insurance penetration below 20% despite high vulnerability to climate events. Additionally, partnerships between insurtech firms and governments are driving innovation in climate risk financing, with over 30 pilot programs launched globally. These developments create new avenues for market expansion and technological advancement, positioning the market for long-term growth.

Regulatory uncertainties and the evolving nature of climate models present ongoing challenges for the Climate-Tech Insurance and Risk Underwriting Solutions Market. Over 40 countries have introduced climate risk disclosure requirements, but the lack of standardized frameworks creates inconsistencies in reporting and compliance. Insurers must continuously update underwriting models to reflect changing climate patterns, increasing operational complexity and costs. Additionally, climate models often involve uncertainties due to unpredictable environmental variables, impacting risk accuracy and pricing strategies. More than 35% of insurers report challenges in aligning underwriting practices with evolving regulatory expectations. Furthermore, the need for continuous technological upgrades and data validation adds to operational burdens. These challenges require insurers to invest in adaptive systems and robust risk management frameworks to maintain competitiveness and compliance in a rapidly changing regulatory landscape.

Increasing Adoption of AI-Driven Risk Modeling: Over 65% of insurers have integrated AI-based climate risk models into underwriting processes, improving predictive accuracy by nearly 45%. Automated analytics platforms are reducing manual underwriting workloads by 30%, enabling faster decision-making and enhancing operational efficiency across property and agriculture insurance segments globally.

Expansion of Parametric Insurance Solutions: Parametric insurance adoption has grown by over 50%, with nearly 40% of climate-related policies now incorporating trigger-based payout mechanisms. These models have reduced claim settlement time by up to 35%, particularly in disaster-prone regions, improving financial resilience and customer satisfaction across emerging markets.

Integration of Satellite and Geospatial Data: Over 70% of advanced underwriting platforms now utilize satellite imagery and geospatial analytics, enhancing real-time risk monitoring capabilities by 38%. This trend is particularly prominent in North America and Europe, where insurers are leveraging high-resolution climate data for precise risk segmentation and pricing strategies.

Rising ESG and Regulatory Compliance Integration: More than 72% of insurers are aligning underwriting practices with ESG frameworks, incorporating climate risk disclosures and sustainability metrics. Regulatory mandates across 30+ countries have driven a 40% increase in climate-risk reporting tools, influencing underwriting strategies and investment decisions across the insurance sector.

The Climate-Tech Insurance and Risk Underwriting Solutions Market is segmented based on type, application, and end-user, reflecting the diverse use cases and technological integration across the insurance ecosystem. The market demonstrates strong differentiation in product offerings, ranging from AI-driven underwriting platforms to parametric insurance solutions and climate risk analytics tools. Applications span across property insurance, agriculture, energy, and disaster risk financing, each contributing significantly to overall adoption trends. End-users include insurance companies, reinsurance firms, government agencies, and large enterprises seeking climate risk mitigation strategies. Over 60% of adoption is concentrated within property and agriculture sectors, highlighting the impact of climate variability on these industries. Additionally, digital transformation initiatives have accelerated adoption across emerging economies, where climate risk exposure is increasing rapidly. The segmentation reflects a balanced mix of technological innovation and industry-specific applications, supporting market expansion and operational efficiency improvements.

The market includes AI-based underwriting platforms, climate risk analytics tools, parametric insurance solutions, and geospatial risk modeling systems. AI-based underwriting platforms lead the segment, accounting for approximately 38% of total adoption due to their ability to improve predictive accuracy and automate decision-making processes. Climate risk analytics tools hold around 27%, driven by demand for advanced data modeling and scenario analysis. Parametric insurance solutions, while currently representing 20%, are the fastest-growing segment with an estimated growth rate of 18% due to their efficiency in claims processing and transparency. Geospatial risk modeling systems and other niche technologies collectively account for the remaining 15%, offering specialized applications in disaster risk assessment and environmental monitoring.

• In 2025, a global reinsurer deployed AI-based underwriting platforms integrated with satellite data, improving catastrophe risk prediction accuracy by over 30% and reducing underwriting processing time by 25%.

Applications include property insurance, agriculture insurance, energy sector risk management, disaster risk financing, and infrastructure protection. Property insurance dominates with a 42% share due to high exposure to climate-related risks such as floods and wildfires. Agriculture insurance accounts for 25%, supported by increasing climate variability affecting crop yields. Disaster risk financing is the fastest-growing application, expanding at an estimated rate of 19% due to rising demand for rapid response mechanisms. Energy and infrastructure applications collectively contribute 33%, reflecting the growing need for climate resilience in critical sectors. In 2025, more than 58% of insurers globally reported integrating climate-tech solutions into property insurance underwriting. Additionally, over 46% of agricultural insurers have adopted climate risk analytics tools to enhance yield prediction and risk mitigation strategies.

• In 2024, a global insurance consortium implemented climate risk analytics in over 150 agricultural projects, improving crop loss prediction accuracy by 28% and supporting over 1 million farmers.

End-users include insurance companies, reinsurance firms, government agencies, and large enterprises. Insurance companies lead with a 48% share due to their primary role in underwriting and risk assessment. Reinsurance firms account for 26%, leveraging advanced analytics for portfolio risk management. Government agencies represent 15%, focusing on disaster risk financing and public sector resilience programs. Large enterprises and other end-users contribute 11%, utilizing climate risk solutions for asset protection and operational planning. Reinsurance firms are the fastest-growing segment, with adoption increasing at approximately 17%, driven by the need for advanced catastrophe modeling. In 2025, over 62% of large insurers reported deploying AI-driven underwriting tools, while nearly 40% of enterprises adopted climate risk analytics for infrastructure protection.

• In 2025, a government-led climate risk initiative enabled over 500 enterprises to integrate predictive analytics tools, improving disaster preparedness efficiency by 30%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.8% between 2026 and 2033.

North America benefits from advanced insurance infrastructure and high adoption of AI-driven underwriting tools, with over 65% of insurers integrating climate risk analytics. Europe holds approximately 30% share, driven by stringent regulatory frameworks and ESG mandates, with over 60% of insurers complying with climate disclosure requirements. Asia-Pacific accounts for around 22%, supported by increasing climate vulnerability and digital insurance expansion, particularly in China, India, and Japan. South America and the Middle East & Africa collectively contribute 10%, with growing adoption in agriculture and energy sectors. The regional landscape highlights strong technological integration in developed markets and rapid adoption in emerging economies, supported by increasing climate risk awareness and government initiatives.

North America holds approximately 38% of the global market, driven by strong demand across property, agriculture, and energy insurance sectors. The region has witnessed over 65% adoption of AI-based underwriting tools, improving predictive accuracy by nearly 45%. Regulatory frameworks such as climate risk disclosure mandates are influencing underwriting strategies, while government support for climate resilience initiatives continues to grow. Digital transformation trends, including integration of satellite data and IoT-based monitoring systems, have enhanced real-time risk assessment capabilities by over 35%. A leading reinsurer in the region has implemented AI-driven catastrophe modeling platforms, reducing claim uncertainty by 28%. Consumer behavior indicates higher adoption among enterprises in finance and healthcare sectors, with over 55% prioritizing climate risk integration in decision-making processes.

Europe accounts for nearly 30% of the global market, with key markets including Germany, the UK, and France leading adoption. Over 62% of insurers in the region have integrated climate risk disclosures into underwriting processes due to stringent ESG regulations. Sustainability initiatives and regulatory bodies are driving demand for explainable AI and transparent risk modeling tools. Technological advancements such as geospatial analytics and climate scenario modeling are widely adopted, improving underwriting efficiency by over 30%. A major European insurer has deployed AI-based risk assessment tools, enhancing loss prediction accuracy by 25%. Consumer behavior reflects a strong preference for sustainable and compliant insurance solutions, with regulatory pressure influencing adoption across the region.

Asia-Pacific ranks as the fastest-growing region, accounting for approximately 22% of the global market. Key countries such as China, India, and Japan are driving demand due to increasing climate vulnerability and expanding insurance penetration. The region has seen over 40% growth in digital insurance platforms, supported by mobile technology and fintech innovation. Infrastructure development and industrial expansion are increasing demand for climate risk solutions, particularly in agriculture and energy sectors. A regional insurer has implemented AI-driven underwriting systems, improving risk assessment efficiency by 27%. Consumer behavior shows strong growth in mobile-based insurance adoption, with over 50% of users preferring digital platforms for policy management and risk evaluation.

South America contributes approximately 6% to the global market, with Brazil and Argentina leading adoption. The region’s demand is driven by agriculture and energy sectors, which are highly exposed to climate risks. Government incentives and trade policies supporting climate resilience are encouraging adoption of underwriting solutions. Over 35% of insurers in the region have begun integrating climate risk analytics into underwriting processes. A local insurance provider has deployed parametric insurance models, reducing claim settlement time by 30%. Consumer behavior indicates demand tied to localized risk assessment and language-specific solutions, with increasing adoption across rural and agricultural communities.

The Middle East & Africa region accounts for approximately 4% of the global market, with growth driven by oil & gas, construction, and infrastructure sectors. Countries such as the UAE and South Africa are leading adoption due to increasing climate risk exposure and modernization initiatives. Technological trends include the adoption of AI-based analytics and satellite data integration, improving risk assessment efficiency by over 25%. Trade partnerships and regulatory frameworks are supporting the development of climate risk insurance solutions. A regional insurer has implemented digital underwriting platforms, enhancing operational efficiency by 20%. Consumer behavior reflects growing awareness of climate risks, with increased adoption among enterprises seeking risk mitigation strategies.

United States – 38% Market share: Driven by advanced insurance infrastructure and high adoption of AI-based underwriting technologies.

Germany – 14% Market share: Supported by strong regulatory frameworks and widespread integration of climate risk analytics tools.

The Climate-Tech Insurance and Risk Underwriting Solutions Market is moderately fragmented, with over 150 active global and regional players competing across technology, analytics, and insurance service segments. The top five companies collectively account for approximately 45% of the market, indicating a balanced mix of established players and emerging insurtech firms. Leading companies are focusing on strategic partnerships, mergers, and acquisitions to enhance technological capabilities and expand geographic presence. Over 60% of major insurers have collaborated with insurtech firms to integrate AI-driven underwriting solutions and climate risk analytics platforms. Product innovation is a key competitive factor, with more than 70% of companies investing in advanced technologies such as satellite data integration, IoT-based monitoring systems, and blockchain-enabled insurance models. Additionally, the market is witnessing increased competition from technology providers offering specialized climate risk solutions. Companies are also prioritizing ESG compliance and sustainability initiatives, with over 65% aligning their underwriting practices with global climate standards. The competitive landscape is expected to evolve further as new entrants introduce innovative solutions and existing players strengthen their digital transformation strategies.

Munich Re

Aon plc

RMS (Risk Management Solutions)

Willis Towers Watson

AXA Climate

Zurich Insurance Group

Hannover Re

SCOR SE

Descartes Underwriting

Jupiter Intelligence

ClimateAI

Cervest

One Concern

The Climate-Tech Insurance and Risk Underwriting Solutions Market is undergoing significant technological transformation driven by advancements in artificial intelligence, big data analytics, satellite imaging, and IoT-based environmental monitoring systems. AI-driven underwriting platforms are now capable of processing over 10 terabytes of climate data daily, enabling insurers to improve risk prediction accuracy by more than 40%. Machine learning algorithms are being used to analyze historical climate patterns and simulate future scenarios, enhancing decision-making processes and reducing underwriting errors by approximately 30%.

Satellite and geospatial technologies play a critical role in real-time risk assessment, with over 70% of advanced underwriting solutions incorporating high-resolution satellite imagery. These technologies allow insurers to monitor environmental changes such as deforestation, sea-level rise, and extreme weather events with improved precision. Additionally, IoT sensors deployed across infrastructure and agricultural assets provide continuous data streams, improving risk monitoring capabilities by nearly 35%.

Blockchain technology is emerging as a key innovation in parametric insurance, enabling automated claim settlements based on predefined climate triggers. This has reduced claim processing time by up to 35% while enhancing transparency and reducing fraud risks. Furthermore, cloud-based platforms are facilitating scalable data integration, allowing insurers to manage large datasets efficiently. The integration of predictive analytics, real-time data, and automated workflows is transforming underwriting processes, making them more efficient, accurate, and responsive to evolving climate risks.

• In March 2026, Swiss Re reported that secondary perils such as wildfires, floods, and severe storms accounted for a record 92% of global insured natural catastrophe losses, totaling USD 107 billion. The company highlighted that advanced risk modeling indicates potential losses could reach USD 320 billion in extreme scenarios, reinforcing the need for enhanced climate-risk underwriting solutions. Source: www.swissre.com

• In December 2025, Swiss Re Capital Markets structured and placed a USD 400 million catastrophe bond for Farmers Insurance Group, strengthening risk transfer mechanisms and enabling insurers to manage climate-related catastrophe exposure more effectively through capital market instruments integrated with underwriting strategies.

• In January 2025, Munich Re reported that tropical cyclones alone contributed USD 135 billion to total global losses and USD 52 billion to insured losses in 2024, emphasizing increasing reliance on advanced climate risk analytics and underwriting models to manage growing exposure to extreme weather events.

• In May 2025, Aon highlighted in its Climate and Catastrophe Insight report that global economic losses from natural disasters reached USD 368 billion in 2024, prompting insurers to adopt advanced climate risk underwriting solutions and integrate AI-driven analytics to better assess workforce, infrastructure, and operational risks.

The Climate-Tech Insurance and Risk Underwriting Solutions Market Report provides a comprehensive analysis of the global market, covering a wide range of segments, technologies, applications, and geographic regions. The report evaluates key product categories including AI-based underwriting platforms, climate risk analytics tools, parametric insurance solutions, and geospatial modeling systems, offering detailed insights into their adoption patterns and operational impact. It also examines application areas such as property insurance, agriculture, energy, disaster risk financing, and infrastructure protection, highlighting their respective contributions to market development.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed regional insights supported by quantitative data and qualitative analysis. The study explores market dynamics, including drivers, restraints, opportunities, and challenges, along with emerging trends shaping the industry. Additionally, the report analyzes end-user segments such as insurance companies, reinsurance firms, government agencies, and enterprises, focusing on their adoption behavior and strategic priorities.

The scope further includes technological advancements such as AI, IoT, satellite imaging, and blockchain, detailing their role in transforming underwriting processes and improving risk assessment accuracy. It also examines competitive landscape factors, including key players, strategic initiatives, and innovation trends. Overall, the report offers a holistic view of the market, enabling stakeholders to make informed decisions, identify growth opportunities, and develop effective strategies in the evolving climate-tech insurance ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 350.0 Million |

| Market Revenue (2033) | USD 1,108.5 Million |

| CAGR (2026–2033) | 15.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Swiss Re; Munich Re; Aon plc; RMS (Risk Management Solutions); Willis Towers Watson; AXA Climate; Zurich Insurance Group; Hannover Re; SCOR SE; Descartes Underwriting; Jupiter Intelligence; ClimateAI; Cervest; One Concern |

| Customization & Pricing | Available on Request (10% Customization Free) |