Reports

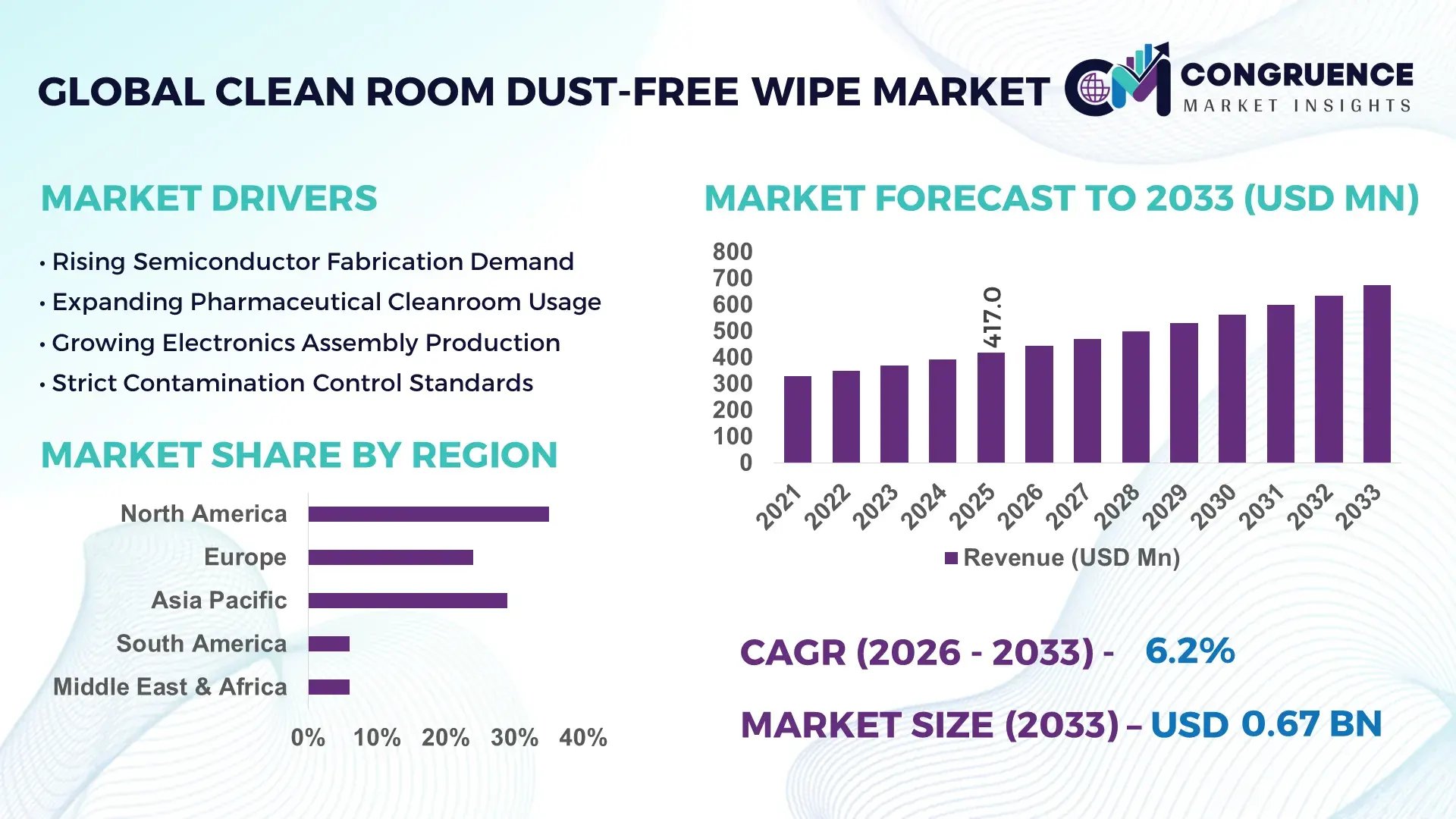

The Global Clean Room Dust-Free Wipe Market was valued at USD 417.0 Million in 2025 and is anticipated to reach a value of USD 674.7 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. The market is being propelled by rising semiconductor fabrication investments, accelerated pharmaceutical manufacturing expansion, and stricter contamination-control requirements across advanced electronics and biotechnology facilities. Between 2024 and 2026, supply chain localization initiatives, reinforced cleanroom compliance standards, and capacity expansion across strategic manufacturing hubs have reshaped procurement priorities for contamination-control consumables.

The United States remains the dominant country, accounting for approximately 31% of global demand, supported by over USD 50 billion in semiconductor manufacturing commitments, more than 20 major wafer fabrication projects under development, and a pharmaceutical sector contributing nearly 45% of North America's cleanroom consumables consumption. Compared with several mature European markets, U.S. cleanroom automation adoption exceeds 68%, enabling higher wipe utilization standards and contamination monitoring frequency. The country's advanced electronics, biotechnology, and aerospace industries collectively represent over 60% of high-specification wipe procurement volumes. The implementation of the CHIPS manufacturing initiatives has further accelerated domestic cleanroom infrastructure deployment, reinforcing demand for low-particle and high-absorbency wiping solutions.

For market participants, success increasingly depends on aligning product innovation, contamination-control performance, and regional manufacturing strategies with the rapidly expanding cleanroom infrastructure ecosystem.

Market Size & Growth: USD 417.0 million in 2025 reaching USD 674.7 million by 2033 at 6.2% CAGR, driven by semiconductor fab expansion and pharmaceutical cleanroom upgrades.

Top Growth Drivers: Semiconductor investments (+22%), biologics production growth (+18%), and contamination-control compliance expansion (+15%) are accelerating demand.

Short-Term Forecast: By 2028, automated cleanroom operations are expected to improve cleaning efficiency by 20% while reducing consumable waste by 12%.

Emerging Technologies: AI-enabled contamination monitoring, advanced microfiber composites, and automated dispensing systems are improving process precision by 15–25%.

Regional Leaders: North America (USD 165 million), Asia-Pacific (USD 142 million), and Europe (USD 96 million) lead through semiconductor, electronics, and pharmaceutical adoption.

Consumer/End-User Trends: More than 63% of cleanroom operators prioritize low-lint and particle-retention performance over product cost.

Pilot/Case Example: A 2025 semiconductor facility modernization project reduced contamination incidents by 28% through advanced wipe deployment protocols.

Competitive Landscape: Leading suppliers collectively control nearly 42% of global supply, with Berkshire, Texwipe, Contec, Valutek, and Micronova maintaining strong positions.

Regulatory & ESG Impact: Sustainable wipe materials lowered waste generation by 18% while supporting compliance with evolving environmental standards.

Investment & Funding: Over USD 2.1 billion in cleanroom infrastructure investments globally are supporting contamination-control ecosystem expansion.

Innovation & Future Outlook: Next-generation recyclable microfiber technologies and smart inventory systems are reshaping procurement and operational optimization.

Semiconductor manufacturing accounts for approximately 36% of overall demand, followed by pharmaceuticals at 29% and electronics assembly at 18%, reflecting the market’s strong dependence on contamination-sensitive industries. Advanced microfiber and ultra-low particle-generation products continue gaining traction, with adoption increasing by nearly 21% across high-specification cleanrooms. Regional demand patterns are shifting toward Asia-Pacific manufacturing clusters while North America maintains leadership in premium-grade products. Ongoing supply chain localization and compliance-focused procurement strategies are further influencing purchasing decisions. These developments are creating a foundation for deeper strategic evaluation across competitive, operational, and investment dimensions.

The Clean Room Dust-Free Wipe Market is becoming a critical battleground for manufacturers seeking competitive advantage in semiconductor fabrication, biotechnology production, advanced electronics assembly, and pharmaceutical processing. As contamination tolerance thresholds continue tightening across high-value manufacturing environments, cleanroom consumables are transitioning from operational necessities to strategic quality-control assets. Organizations increasingly recognize that contamination-related production losses can exceed operational savings gained through lower-cost alternatives, transforming procurement priorities throughout the value chain.

A significant market shift is being driven by supply chain regionalization, stricter contamination-control frameworks, and heightened regulatory scrutiny across pharmaceutical and semiconductor industries. Companies are accelerating investments in premium contamination-control products to maintain production continuity and compliance performance.Advanced microfiber composite technologies improve particle capture efficiency by 35% while reducing operational cleaning costs by 18% compared to conventional polyester-based wiping systems. This performance differential is reshaping purchasing decisions among large-scale cleanroom operators seeking measurable productivity gains.

Asia-Pacific leads in volume consumption with approximately 39% of global demand, while North America leads in technological adoption and contamination-control innovation with nearly 68% penetration of advanced cleanroom monitoring systems. Over the next two to three years, automated cleanroom management systems are expected to reduce contamination incidents by more than 22% while improving operational efficiency by approximately 17%. Sustainability has emerged as a competitive differentiator, with recyclable and low-waste wiping solutions reducing disposal costs by nearly 14% while supporting environmental compliance objectives. A recent semiconductor manufacturing modernization initiative demonstrated a 27% reduction in contamination-related process interruptions following implementation of advanced wipe-management protocols.

Market leaders are increasingly shifting capital allocation toward localized manufacturing, premium-grade product portfolios, and integrated contamination-control ecosystems. Strategic partnerships, capacity expansions, and product innovation programs are accelerating across key regions as competition intensifies. Organizations that successfully combine contamination-control performance, sustainability advantages, and regional supply resilience will be best positioned to capture long-term value as the market continues accelerating, transforming, and optimizing global cleanroom operations.

The Clean Room Dust-Free Wipe Market is experiencing significant transformation as contamination-control standards become increasingly stringent across semiconductor, pharmaceutical, biotechnology, aerospace, and precision electronics industries. Demand is being shaped by the growing complexity of manufacturing processes where microscopic particle contamination directly impacts product yield, quality consistency, and regulatory compliance. Advanced cleanroom environments now require highly specialized wiping materials capable of minimizing particle generation while improving absorption performance and chemical compatibility. Industry participants are increasingly investing in premium materials, automated contamination-control systems, and localized manufacturing capabilities to strengthen supply reliability. The market is also being influenced by sustainability initiatives, stricter quality management frameworks, and growing adoption of next-generation cleanroom technologies. As global manufacturing networks evolve, procurement strategies are shifting toward performance-driven products capable of supporting increasingly sophisticated production environments.

Semiconductor fabrication and biopharmaceutical manufacturing expansion remain the primary growth engines driving the Clean Room Dust-Free Wipe Market. Semiconductor facilities now account for approximately 36% of specialized wipe consumption, while biologics manufacturing demand has increased by nearly 19% over recent years. The global shift toward advanced chip manufacturing, coupled with increased pharmaceutical production capacity, is forcing stricter contamination-control requirements across production environments. As contamination thresholds tighten by up to 25% in leading facilities, operators are increasing wipe consumption intensity and product specification requirements. This cause-and-effect relationship is accelerating investment in premium microfiber technologies and low-particle-generation materials. Companies are responding through manufacturing capacity expansion, strategic supplier partnerships, and product portfolio diversification. Recent supply chain restructuring initiatives across North America and Asia have further reinforced demand for locally sourced contamination-control products, prompting manufacturers to expand regional production footprints and strengthen distribution networks.

Raw material volatility and supply concentration continue constraining growth potential within the Clean Room Dust-Free Wipe Market. Polyester and advanced microfiber input costs have experienced fluctuations exceeding 14% during recent procurement cycles, creating pricing uncertainty for manufacturers. Approximately 62% of specialized material processing capacity remains concentrated within limited manufacturing regions, increasing exposure to supply disruptions and logistics challenges. These structural limitations directly affect production planning, inventory management, and long-term contract pricing. Businesses operating in highly regulated sectors face additional pressure as compliance-related manufacturing costs have increased by nearly 11%. In response, market participants are diversifying supplier networks, negotiating long-term procurement agreements, and exploring alternative fiber technologies to reduce dependency risks. While these mitigation strategies improve resilience, they also require additional capital investment, creating tension between operational stability and cost competitiveness.

Emerging opportunities are increasingly concentrated within advanced semiconductor nodes, biologics manufacturing, and next-generation electronics production. Adoption of automated contamination-control systems has improved cleaning process efficiency by approximately 24%, creating demand for specialized wipe solutions designed for automated environments. Sustainable wipe technologies are gaining traction, with environmentally optimized products experiencing adoption growth exceeding 20% in regulated industries. Another powerful opportunity lies in expanding cleanroom infrastructure across emerging manufacturing economies, where new facility development has increased by nearly 17%. Beyond traditional demand drivers, digital contamination monitoring integration presents a non-obvious upside by enabling data-driven consumable optimization and reduced operational waste. Companies are aggressively positioning for future dominance through research and development initiatives, regional manufacturing expansion, and ecosystem partnerships. These actions are redefining competitive positioning while opening access to high-value demand segments that prioritize performance and compliance over cost.

Maintaining consistent contamination-control performance across expanding global manufacturing networks represents a significant long-term challenge. Product specification requirements vary across industries, with performance tolerances differing by as much as 30% between semiconductor and pharmaceutical applications. Regulatory complexity continues increasing, while quality assurance costs have risen by approximately 13% in advanced manufacturing environments. Infrastructure constraints in emerging markets, combined with skilled workforce shortages affecting nearly 18% of specialized facilities, further complicate operational scaling. These challenges threaten growth consistency by increasing operational complexity and extending qualification timelines. Companies seeking long-term competitiveness must invest in advanced quality systems, manufacturing automation, and collaborative partnerships that support standardized performance outcomes. Success will increasingly depend on balancing global expansion objectives with rigorous contamination-control requirements and evolving regulatory expectations.

22% Increase in Automated Cleanroom Consumable Management Adoption — Manufacturers are deploying automated inventory tracking and dispensing systems across contamination-sensitive environments, reducing stockout incidents by 18% and lowering consumable waste by 14%. This operational shift is optimizing procurement cycles and improving cleaning consistency. Companies are responding through digital integration partnerships and smart facility upgrades.

28% Growth in Advanced Microfiber Wipe Utilization Across High-Specification Facilities — Semiconductor and biotechnology operators are replacing conventional materials with engineered microfiber products capable of improving particle retention by 25% and liquid absorption performance by 20%. The shift is reshaping supplier priorities and forcing manufacturers to expand premium product portfolios while investing in material innovation.

31% Expansion in Regionalized Production and Localized Supply Networks — Ongoing supply chain restructuring has accelerated regional manufacturing strategies, reducing lead times by nearly 16% and improving supply reliability by 21%. Companies are establishing localized production hubs and strengthening regional partnerships to mitigate procurement disruptions and maintain operational continuity.

19% Rise in Sustainable Contamination-Control Product Deployment — Regulatory expectations and waste-reduction initiatives are driving adoption of recyclable and low-environmental-impact wiping materials. Facilities implementing these products have reported waste reductions exceeding 15% while maintaining contamination-control performance standards. Manufacturers are responding through sustainable product launches, circular-material initiatives, and compliance-focused innovation programs.

The Clean Room Dust-Free Wipe Market is segmented by type, application, and end-user, reflecting the diverse contamination-control requirements across highly regulated industries. Demand remains concentrated in premium-performance wipe categories used in semiconductor fabrication, pharmaceutical manufacturing, and biotechnology facilities where contamination tolerance levels are extremely low. Approximately 58% of market demand originates from high-specification cleanroom environments requiring superior particle retention and absorbency performance. Demand is increasingly shifting toward advanced microfiber and low-particle-generation products as facilities pursue operational efficiency and compliance optimization. Application trends indicate stronger adoption in semiconductor and pharmaceutical manufacturing, while end-user demand continues expanding among electronics manufacturers and biotechnology companies. These segmentation dynamics are redefining product development priorities, procurement strategies, and capacity investment decisions across the global contamination-control ecosystem.

Polyester Knit Wipes dominate the Clean Room Dust-Free Wipe Market with an estimated 41% market share due to their proven contamination-control performance, chemical compatibility, durability, and cost-effectiveness across pharmaceutical, semiconductor, and electronics manufacturing environments. Their scalability and consistent quality standards make them the preferred choice for high-volume cleanroom operations.Microfiber Wipes represent the fastest-growing segment, with adoption expanding by approximately 8.9% annually due to superior particle capture efficiency, enhanced absorbency, and improved cleaning precision. Compared with traditional polyester products, advanced microfiber wipes can retain significantly smaller particles, making them increasingly attractive for advanced semiconductor and biotechnology applications. Nonwoven Wipes, Foam Wipes, and Specialty Composite Wipes collectively account for approximately 59% of total demand. Nonwoven products maintain strong adoption in cost-sensitive operations, while foam-based solutions remain strategically important for precision cleaning and solvent management. Specialty composite products are gaining traction within ultra-clean manufacturing environments where contamination-control performance outweighs procurement costs. Demand is steadily shifting toward premium-performance products as manufacturers prioritize yield optimization and contamination reduction. Companies are responding through product innovation, advanced material engineering, and expanded production capabilities focused on high-value cleanroom applications. The most attractive investment opportunities remain concentrated within advanced microfiber and specialty-performance wipe technologies where specification requirements continue increasing.

• According to a 2025 report by the International Society for Pharmaceutical Engineering (ISPE), advanced microfiber wipe technologies were adopted by over 64% of newly commissioned high-grade cleanrooms, resulting in particle-removal efficiency improvements exceeding 24%, reinforcing their growing strategic importance.

Semiconductor Manufacturing remains the leading application segment, accounting for approximately 34% of global demand. The concentration of demand within this segment reflects increasingly stringent contamination-control requirements associated with advanced wafer fabrication, chip packaging, and precision electronics production. Even microscopic contamination events can significantly impact manufacturing yields, making premium wipe solutions essential. Pharmaceutical Manufacturing is the fastest-growing application segment, with adoption increasing by approximately 8.4% annually due to expanding biologics production, vaccine manufacturing capacity, and stricter regulatory compliance requirements. Compared with the mature semiconductor segment, pharmaceutical facilities are accelerating investment in contamination-control consumables as quality assurance standards become more demanding. Biotechnology, Electronics Assembly, Aerospace, and Medical Device Manufacturing collectively account for roughly 66% of market demand. These industries continue expanding their use of specialized wipe products to support contamination-sensitive production environments and advanced quality-control protocols. Usage patterns are evolving toward higher-frequency cleaning cycles, automated contamination monitoring integration, and stricter operational validation processes. Companies are responding through application-specific product development, expanded technical support services, and strategic partnerships targeting regulated industries. Demand is increasingly moving toward sectors where contamination-control directly influences product quality, compliance outcomes, and operational efficiency.

• According to a 2025 report by SEMI, advanced contamination-control consumables were deployed across more than 75 major semiconductor fabrication facilities, improving process yield efficiency by approximately 18%, highlighting rapid operational adoption.

The Semiconductor Industry represents the largest end-user segment, accounting for approximately 32% of total market demand. Demand concentration remains high due to intensive wipe utilization rates, strict contamination-control protocols, and continuous investment in advanced fabrication technologies. Cleanroom consumables directly influence production quality and operational yield within semiconductor manufacturing environments. Biotechnology Companies represent the fastest-growing end-user group, with adoption expanding by approximately 9.1% annually. Growth is being fueled by increasing biologics production, cell and gene therapy development, and rising investment in advanced research and manufacturing facilities. Compared with traditional pharmaceutical operations, biotechnology organizations often require more specialized contamination-control solutions to support complex production processes. Pharmaceutical Manufacturers, Electronics Producers, Medical Device Companies, and Aerospace Organizations collectively contribute approximately 68% of market demand. These segments continue increasing procurement of premium-performance wipe products to strengthen compliance, product quality, and manufacturing efficiency. Purchasing behavior is increasingly shifting toward performance-based procurement rather than cost-based purchasing decisions. Suppliers are responding through customized product offerings, technical consulting support, and strategic partnership programs designed to improve long-term customer retention. Future demand growth will increasingly concentrate among biotechnology and advanced manufacturing organizations seeking higher-performance contamination-control solutions.

• According to a 2025 report by the Biotechnology Innovation Organization (BIO), contamination-control solution adoption among biotechnology manufacturers increased by 21%, with over 1,200 facilities implementing advanced cleanroom protocols that improved operational efficiency by 17%, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 35% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.3% between 2026 and 2033.

North America maintains leadership through strong semiconductor, pharmaceutical, and biotechnology demand, while Asia-Pacific benefits from manufacturing expansion and semiconductor production growth. Europe accounts for approximately 24% of global demand, supported by stringent compliance standards and advanced pharmaceutical production. Asia-Pacific represents nearly 29% of market activity and continues strengthening its manufacturing position through large-scale facility investments. South America contributes around 6% of demand, while the Middle East & Africa accounts for 6%, driven by expanding healthcare and industrial infrastructure. Supply chain regionalization and cleanroom localization strategies are encouraging global manufacturers to diversify production networks. Companies are increasingly prioritizing North America for innovation, Asia-Pacific for scale, and Europe for compliance-driven premium product opportunities.

North America holds approximately 35% of global market demand, supported by strong semiconductor fabrication, pharmaceutical manufacturing, and biotechnology research activity. Nearly 45% of regional wipe consumption originates from semiconductor and advanced electronics facilities. Regulatory compliance requirements and domestic manufacturing expansion initiatives continue strengthening contamination-control investments. Advanced monitoring systems are now utilized in approximately 68% of high-specification cleanrooms, improving operational consistency and cleaning validation procedures. Several major manufacturing projects have increased regional cleanroom capacity by more than 20% since 2024. Enterprises increasingly prioritize premium-performance products that reduce contamination risk and improve production yields. The region remains a strategic investment destination because quality assurance requirements continue intensifying across high-value manufacturing sectors.

Europe accounts for approximately 24% of global market demand, with Germany, France, and the United Kingdom representing major consumption centers. Regulatory compliance and sustainability initiatives are powerful market-shaping forces, with over 55% of large cleanroom operators integrating environmental performance criteria into procurement decisions. Manufacturers are increasingly adopting recyclable wipe materials and waste-reduction strategies to meet evolving compliance objectives. Sustainable product deployment has increased by nearly 19% across advanced pharmaceutical and electronics facilities. Quality-first procurement behavior remains dominant, particularly among highly regulated industries. Companies are accelerating product innovation programs focused on sustainable materials and contamination-control performance. The region continues forcing adaptation through increasingly sophisticated regulatory and environmental expectations.

Asia-Pacific represents approximately 29% of global market demand and ranks as the fastest-expanding regional market. China, Japan, South Korea, and Taiwan serve as major demand centers due to their dominant semiconductor, electronics, and precision manufacturing industries. More than 52% of new cleanroom infrastructure projects announced globally since 2024 have been concentrated within the region. Localized manufacturing strategies have reduced supply lead times by nearly 18%, improving operational responsiveness. Enterprises increasingly prioritize scale, speed, and production efficiency when selecting contamination-control solutions. Manufacturers are expanding regional production facilities and strengthening distribution networks to support rising demand. Asia-Pacific remains essential for companies pursuing volume growth, manufacturing scale, and long-term market expansion.

South America contributes approximately 6% of global demand, led by Brazil and Argentina. Pharmaceutical production, healthcare expansion, and industrial modernization initiatives continue supporting contamination-control product adoption. However, import dependency and logistics complexity remain structural constraints affecting procurement efficiency and pricing stability. Demand for cleanroom consumables has increased by approximately 11% across regulated manufacturing environments, while localized supply capabilities remain comparatively limited. Enterprises demonstrate strong price sensitivity and prioritize operational reliability when evaluating suppliers. Manufacturers are responding through regional partnerships and expanded distributor networks designed to improve product availability. The region offers meaningful growth potential but requires careful management of operational and infrastructure-related risks.

The Middle East & Africa accounts for approximately 6% of global market activity, with demand concentrated in Saudi Arabia, the United Arab Emirates, and South Africa. Healthcare infrastructure development, pharmaceutical investments, and industrial diversification programs are strengthening contamination-control requirements across the region. More than 15% of newly announced advanced healthcare facility projects incorporate upgraded cleanroom specifications. Technology adoption and operational modernization initiatives continue expanding, particularly within pharmaceutical and medical manufacturing sectors. Enterprises increasingly seek high-performance contamination-control solutions capable of supporting international quality standards. Manufacturers are entering strategic partnerships and expanding regional distribution capabilities to capture emerging opportunities. The region is becoming increasingly strategic as infrastructure investment and industrial modernization accelerate.

United States – 31% Market Share: Benefits from extensive semiconductor fabrication capacity, advanced pharmaceutical manufacturing infrastructure, and strong contamination-control compliance requirements.

China – 18% Market Share: Driven by large-scale electronics production, semiconductor manufacturing expansion, and rapidly growing cleanroom infrastructure investments.

The Clean Room Dust-Free Wipe Market is characterized by intense competition between global contamination-control leaders such as Berkshire Corporation, Contec Inc., Texwipe, Valutek, Micronova, and regional cleanroom consumable suppliers competing on cost efficiency and localized distribution. Global leaders primarily compete through advanced material engineering, contamination-control performance, and regulatory compliance capabilities, while regional players focus on pricing flexibility and faster fulfillment.

The top five suppliers collectively account for approximately 42% of global market activity, reflecting a moderately consolidated structure. Competition is increasingly centered on particle-retention efficiency, contamination reduction, and supply resilience. Advanced microfiber products improve particle-capture performance by nearly 25%, while automated cleanroom integration solutions reduce operational cleaning time by approximately 18%. Product qualification cycles can exceed 6–12 months, creating significant entry barriers for new suppliers.

Companies are expanding manufacturing footprints, strengthening pharmaceutical and semiconductor partnerships, and accelerating innovation programs focused on sustainable materials and low-particle technologies. The competitive shift is moving toward integrated contamination-control ecosystems, localized production networks, and premium-performance products. Winning in this market requires proven contamination-control reliability, regulatory credibility, application-specific innovation, and strong regional supply execution.

Contec Inc.

Texwipe

Valutek Inc.

Micronova Manufacturing Inc.

Nitritex Ltd.

High-Tech Conversions Inc.

ITW Texwipe

KM Corporation

VWR International

DuPont

Kimberly-Clark Professional

ACL Staticide Inc.

Puritech

Advanced microfiber engineering continues transforming contamination-control performance across semiconductor, pharmaceutical, and biotechnology facilities. Modern microfiber wipes improve particle-capture efficiency by approximately 25% and liquid absorption performance by nearly 20% compared with conventional polyester-based alternatives. More than 60% of newly commissioned high-specification cleanrooms now prioritize microfiber-based contamination-control systems due to superior cleaning precision and lower particle generation.

Automation integration is becoming a defining technology trend. Automated dispensing, contamination-monitoring platforms, and smart inventory management systems have reduced consumable waste by approximately 14% while improving operational efficiency by nearly 18%. Semiconductor manufacturers and biotechnology companies are leading adoption because contamination-control consistency directly influences production yield and regulatory compliance outcomes. Facilities implementing automated monitoring frameworks are achieving faster validation cycles and stronger process control.

Sustainable material technologies are also gaining momentum. Recyclable contamination-control materials and low-waste wipe systems have reduced disposal volumes by nearly 15% across regulated manufacturing environments. Compared with legacy disposable products, advanced sustainable solutions provide improved compliance alignment and stronger environmental performance. Between 2026 and 2028, AI-assisted contamination analytics, smart cleanroom integration, and next-generation composite microfiber technologies are expected to redefine operational standards. Organizations investing early in advanced contamination-control technologies will gain measurable quality, compliance, and productivity advantages while strengthening long-term competitive positioning.

May 2025 – Berkshire Corporation received European Union authorization for its SatPax® 70/30 IPA presaturated cleanroom wipes, enabling distribution across EU and EEA markets. The product combines 70% USP-grade IPA with sterile water formulations, strengthening Berkshire’s compliance position and expanding regulated-market access. [Regulatory Expansion] Source: www.berkshire.uk.com

May 2026 – Berkshire Corporation highlighted its MicroPolx® SuperSorb technology in Cleanroom Technology’s May issue, showcasing next-generation contamination-control materials engineered for critical environments. The product portfolio demonstrated enhanced absorbency and precision-cleaning performance, reinforcing Berkshire’s premium product positioning within advanced cleanroom operations. [Material Innovation]

2026 – Contec Inc. expanded deployment of its PowerMop CE battery-powered mechanized cleaning platform through an exclusive partnership with i-team Global. The system supports contamination-control automation initiatives while improving cleaning consistency across highly regulated pharmaceutical and microelectronics environments. [Automation Partnership]

January 2026 – Berkshire Corporation expanded visibility of its VersaHOCl® next-generation cleanroom disinfectant platform following INTERPHEX-focused product promotion activities. The solution was positioned to strengthen contamination-control effectiveness while supporting advanced cleanroom disinfection protocols across pharmaceutical and biotechnology facilities. [Portfolio Expansion]

The Clean Room Dust-Free Wipe Market Report delivers comprehensive coverage of contamination-control consumables across major product categories, applications, end-user industries, and geographic regions. The study evaluates Polyester Knit Wipes, Microfiber Wipes, Nonwoven Wipes, Foam Wipes, and Specialty Composite Wipes while assessing demand patterns across semiconductor manufacturing, pharmaceutical production, biotechnology, electronics assembly, aerospace, and medical device applications. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating evolving manufacturing, compliance, and supply-chain dynamics.

The report provides deep analytical assessment of more than 14 major industry participants, multiple application environments, and key technology trends influencing operational performance. Semiconductor manufacturing accounts for approximately 34% of demand concentration, while premium microfiber technologies exceed 60% adoption across advanced cleanroom facilities. The analysis also evaluates contamination-control automation, sustainable wipe materials, and smart cleanroom integration technologies that are reshaping procurement and operational strategies.

Beyond current market positioning, the report provides forward-looking assessment covering 2026–2033 industry transformation pathways. It supports investment planning, expansion strategy development, supplier evaluation, competitive benchmarking, and regional market prioritization. Particular attention is given to emerging contamination-control technologies, advanced manufacturing expansion, and evolving regulatory frameworks influencing long-term industry competitiveness and operational decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 417.0 Million |

| Market Revenue (2033) | USD 674.7 Million |

| CAGR (2026–2033) | 6.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Berkshire Corporation; Contec Inc.; Texwipe; Valutek Inc.; Micronova Manufacturing Inc.; Nitritex Ltd.; High-Tech Conversions Inc.; ITW Texwipe; KM Corporation; VWR International; DuPont; Kimberly-Clark Professional; ACL Staticide Inc.; Puritech |

| Customization & Pricing | Available on Request (10% Customization Free) |