Reports

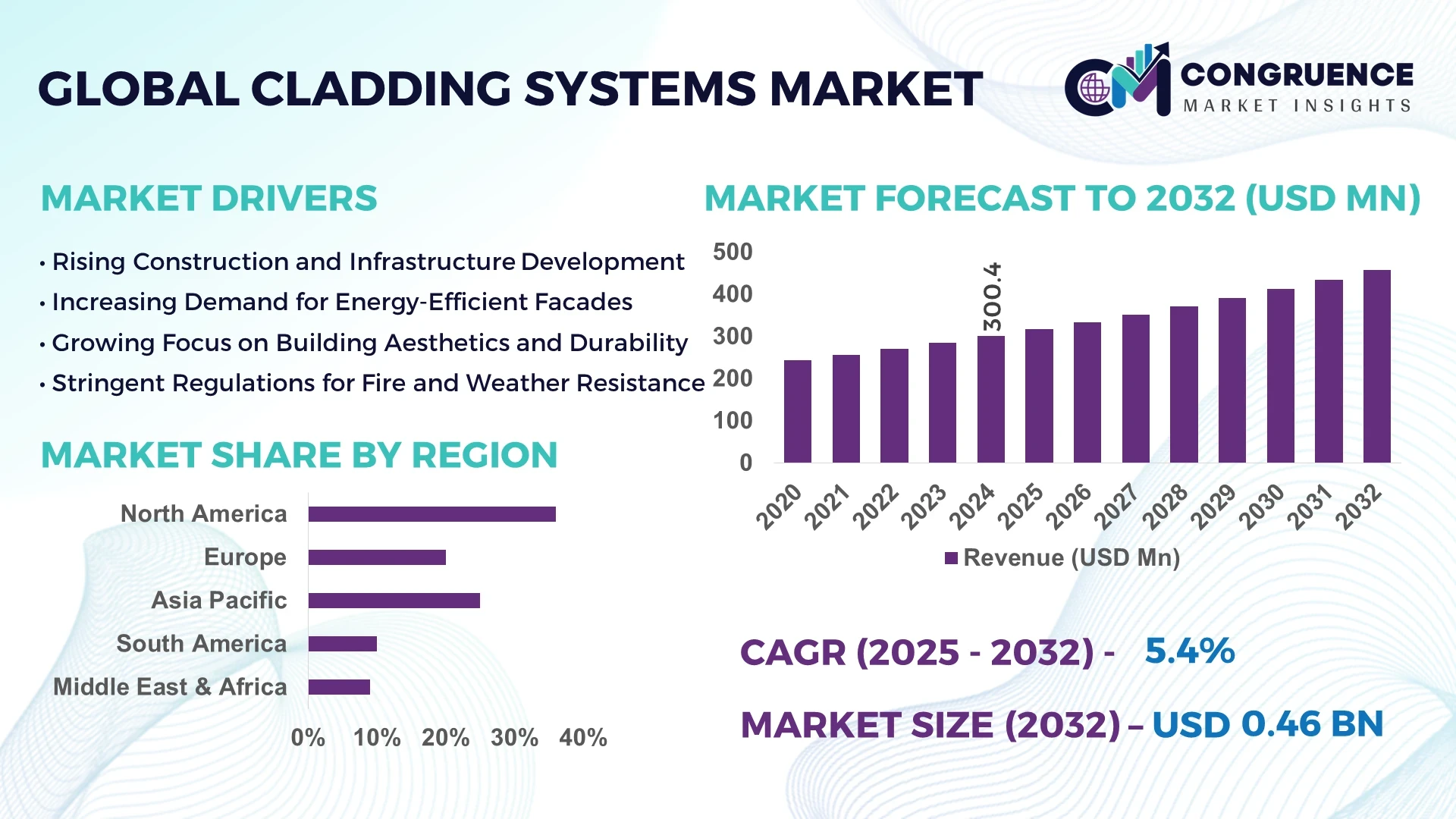

The Global Cladding Systems Market was valued at USD 300.39 Million in 2024 and is anticipated to reach a value of USD 457.52 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032. The market growth is driven by the rising demand for energy-efficient and sustainable façade materials across construction and infrastructure projects worldwide.

The United States dominates the global cladding systems market due to its strong production infrastructure and continuous investments in sustainable building technologies. The country’s advanced manufacturing capacity exceeds 40 million square meters annually, driven by high adoption in commercial and institutional construction. Major investments exceeding USD 2.1 billion have been directed toward innovative materials like fiber cement and composite claddings. Additionally, over 65% of new urban projects in major cities integrate insulated cladding solutions aligned with energy efficiency standards such as LEED and BREEAM, reflecting technological advancement and consumer adoption strength in the country’s construction sector.

• Market Size & Growth: The market reached USD 300.39 Million in 2024 and is projected to reach USD 457.52 Million by 2032, expanding at a CAGR of 5.4%. Growth is driven by the increasing shift toward green building materials and enhanced aesthetic preferences in infrastructure design.

• Top Growth Drivers: Rising adoption of ventilated façades (28%), improvement in material durability (24%), and energy-efficiency benefits (33%) are key growth factors influencing global adoption.

• Short-Term Forecast: By 2028, average installation efficiency is expected to improve by 18%, with overall cladding system costs reducing by nearly 12% due to automation and modular assembly practices.

• Emerging Technologies: Smart cladding panels with embedded sensors, self-cleaning nanocoatings, and 3D-printed composite façades are revolutionizing design and maintenance efficiency in modern construction.

• Regional Leaders: North America is projected to reach USD 152.6 Million by 2032 with strong commercial adoption; Europe is forecasted at USD 136.4 Million led by retrofit projects; Asia-Pacific expected to reach USD 128.5 Million driven by rapid urban infrastructure expansion.

• Consumer/End-User Trends: High adoption among real estate developers and institutional builders, with 45% preference for composite panels and 32% for metal claddings due to low maintenance and sustainability compliance.

• Pilot or Case Example: In 2024, a pilot project in Singapore’s Green District implemented solar-integrated cladding achieving 22% energy savings and reducing overall building maintenance costs by 15%.

• Competitive Landscape: Kingspan Group holds an estimated 9.2% market share, followed by Etex Group, Alucobond, Nichiha Corporation, and Tata Steel as key competitors focusing on innovative product portfolios.

• Regulatory & ESG Impact: Stringent emission standards, building energy codes, and LEED certification requirements continue to drive adoption of recyclable and energy-efficient cladding materials globally.

• Investment & Funding Patterns: Over USD 3.7 billion invested in R&D and green infrastructure projects since 2023, with increased venture capital inflow toward modular cladding and low-carbon material innovations.

• Innovation & Future Outlook: Integration of photovoltaic façades, AI-based performance monitoring systems, and prefabricated composite materials will shape the future of sustainable building exteriors over the next decade.

The cladding systems market is evolving rapidly, with innovation and sustainability at its core. Key industry sectors such as commercial real estate, industrial facilities, and public infrastructure collectively contribute over 70% of total demand. Technological innovations including AI-driven design optimization, modular installation systems, and smart energy-integrated façades are reshaping industry standards. Environmental regulations promoting carbon-neutral construction and government-led urban development programs in Asia-Pacific and Europe are accelerating market penetration. Regional consumption trends highlight growing demand in emerging economies driven by urbanization, while mature markets emphasize retrofitting and energy performance upgrades. The future outlook remains robust, supported by continuous investments, sustainability commitments, and cross-sector collaborations enhancing product efficiency and environmental compliance.

The strategic relevance of the Cladding Systems Market lies in its ability to merge aesthetics, structural performance, and sustainability across the global construction ecosystem. As urban infrastructure evolves toward high-efficiency, eco-friendly standards, cladding systems have become central to energy conservation and building longevity strategies. Modern aluminum composite panels and fiber cement systems deliver 35% better thermal efficiency compared to conventional brick-and-mortar façades, significantly reducing long-term operational costs for developers. North America dominates in volume due to its high concentration of commercial and institutional projects, while Europe leads in adoption with 48% of enterprises integrating sustainable cladding solutions in new constructions.

By 2027, AI-driven façade analytics and smart material monitoring technologies are expected to improve design efficiency by 26% and reduce installation downtime by 18%, enhancing construction productivity and asset lifecycle performance. Firms are committing to ESG metrics targeting a 30% reduction in embodied carbon and a 45% recycling rate of composite panels by 2030, aligning with global green building mandates. In 2024, Germany achieved a 22% energy efficiency improvement in commercial infrastructure through AI-enabled adaptive cladding design, underscoring measurable progress in technological integration. Moving forward, the Cladding Systems Market will remain a pillar of resilience, compliance, and sustainable growth, integrating innovation, digital intelligence, and environmental stewardship across the global construction value chain.

The accelerating global push toward sustainable construction is a primary growth driver for the Cladding Systems Market. With over 55% of urban projects globally adopting energy-efficient building envelopes, demand for eco-friendly cladding materials is surging. Lightweight composites and ventilated façades now account for over 40% of modern installations, significantly improving thermal insulation and energy performance. Construction companies are prioritizing materials with recyclable content exceeding 60% to comply with green building certifications. This transition aligns with government-backed initiatives promoting carbon-neutral infrastructure, particularly in Europe and Asia-Pacific, where rapid urban development and environmental mandates are reinforcing large-scale deployment of advanced cladding systems.

Volatility in raw material prices, particularly aluminum, steel, and polymer composites, poses a substantial restraint on the Cladding Systems Market. The cost of aluminum rose by over 20% between 2022 and 2024 due to supply chain disruptions and energy cost inflation, directly impacting manufacturing margins. Smaller producers face challenges maintaining cost competitiveness while adhering to stringent quality and safety standards. Additionally, inconsistencies in global supply logistics have extended project timelines, leading to a preference for localized sourcing and hybrid material use. These fluctuations discourage long-term procurement planning and create uncertainty in large-scale construction projects, limiting short-term growth potential.

Technological advancement presents a major opportunity for growth in the Cladding Systems Market. Smart cladding materials with integrated photovoltaic cells and self-cleaning nanocoatings are gaining traction, improving operational efficiency and reducing maintenance costs by up to 25%. The integration of AI-driven design software and digital twins allows architects to optimize thermal performance and structural safety simultaneously. Additionally, emerging economies in Asia-Pacific and the Middle East are investing in large-scale smart infrastructure projects, creating strong opportunities for advanced cladding applications. The market’s future growth will be defined by automation, customization, and the expansion of multifunctional façade technologies enhancing both sustainability and performance.

Regulatory complexities and compliance costs continue to challenge the Cladding Systems Market, especially amid evolving building codes emphasizing fire resistance, sustainability, and safety. Manufacturers must align with multiple regional standards—such as EN 13501 in Europe and NFPA 285 in North America—resulting in higher testing and certification expenditures. Compliance-related costs can increase project expenses by 12–18%, particularly for multi-material façade systems. Additionally, the implementation of stricter environmental standards limits the use of non-recyclable composites, necessitating continuous product innovation. These challenges, though fostering quality improvement, pose significant barriers for small and mid-tier manufacturers seeking to expand in highly regulated markets.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Cladding Systems Market. Approximately 55% of new building projects report cost advantages when integrating modular and prefabricated methods. Automated off-site fabrication of pre-bent and precision-cut panels has reduced labor costs by nearly 20% and accelerated project timelines by 25%. Europe and North America are leading adopters, with 47% of commercial developers shifting toward pre-assembled façade modules to minimize on-site disruption and enhance build quality.

• Integration of Smart and Energy-Responsive Cladding: Intelligent cladding systems embedded with sensors and responsive coatings are witnessing a surge in deployment. Nearly 38% of newly developed urban buildings in 2024 integrated cladding solutions capable of thermal regulation and real-time energy monitoring. These innovations have delivered up to 30% improvement in building energy efficiency. Asia-Pacific leads in deployment volume, while Europe drives advanced design integration with over 41% of new projects incorporating adaptive cladding technologies for sustainability compliance.

• Increased Use of Recyclable and Low-Carbon Materials: Sustainable materials are becoming a dominant trend as global construction targets carbon-neutral goals. Around 62% of manufacturers now incorporate recyclable composites or bio-based polymers in their cladding portfolios. This shift has resulted in a 28% average reduction in material waste during production. North America remains a hub for low-carbon product innovation, while Europe enforces stricter sustainability benchmarks pushing 36% of producers to switch to green-certified cladding solutions.

• Digital Twin and AI-Driven Design Expansion: The integration of AI and digital twin technologies in cladding design has advanced significantly, improving design precision and structural performance forecasting. In 2024, about 33% of large construction firms employed digital twins for façade simulations, achieving 22% optimization in thermal behavior modeling and 18% reduction in installation errors. The Middle East and Asia-Pacific regions are emerging adopters, investing in digital-driven construction platforms to modernize large-scale urban projects and improve lifecycle asset management.

The Cladding Systems Market demonstrates a diverse segmentation across types, applications, and end-user industries, reflecting the sector’s multidimensional growth. Among product types, metal cladding and composite panels lead global adoption, collectively accounting for more than 55% of installations due to their high durability and energy efficiency. Applications are predominantly concentrated in residential and commercial construction, driven by rising urbanization and the push for sustainable building materials. End-user segmentation indicates significant participation from real estate developers and industrial contractors, who collectively represent over 60% of total consumption. This diversified structure enables the market to adapt rapidly to regional construction trends, evolving safety standards, and architectural innovation, supporting consistent demand across developed and emerging economies.

Metal cladding currently accounts for approximately 38% of total installations, making it the leading segment due to its superior fire resistance, low maintenance requirements, and long lifecycle. Fiber cement cladding follows with a 27% market share, offering enhanced weather protection and acoustic insulation benefits. Composite panels are the fastest-growing type, expanding at an estimated 6.8% CAGR, fueled by increasing adoption in high-rise and modular building projects for their lightweight, aesthetic, and energy-efficient characteristics. Stone and vinyl cladding collectively represent 20% of the market, maintaining niche relevance in residential and heritage restoration applications. The remaining 15% is distributed among ceramic, glass, and wooden cladding, favored for premium architectural designs and eco-friendly construction projects.

Commercial construction dominates the Cladding Systems Market, accounting for 46% of total demand due to the widespread adoption of façade enhancement and energy-efficient building materials in office complexes, retail centers, and institutional facilities. Residential construction follows with a 33% share, driven by a surge in green housing projects and government initiatives promoting low-energy buildings. The industrial segment, currently holding 15%, is projected to grow fastest at 6.3% CAGR, supported by the adoption of metal and composite cladding for warehouse insulation and corrosion resistance. The remaining 6% represents public infrastructure, including airports, transport hubs, and educational institutions increasingly incorporating high-durability façades.

Real estate developers lead the Cladding Systems Market, representing approximately 41% of total adoption, driven by the demand for high-quality façades in urban and commercial developments. Construction contractors follow with 29%, supported by ongoing public infrastructure investments and technological integration in building systems. The industrial and institutional end-users collectively hold around 22% share, utilizing cladding systems for energy management and durability in manufacturing, logistics, and educational facilities. Residential builders represent the remaining 8%, reflecting steady adoption in mid- to high-end housing projects. The fastest-growing end-user group is institutional construction, expanding at an estimated 6.5% CAGR due to rising retrofitting and sustainability mandates across public sector buildings.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Europe followed closely with a 29% share, driven by stringent sustainability standards and renovation projects. The Middle East & Africa represented 12%, supported by infrastructure megaprojects, while South America accounted for 8%, fueled by construction in urban centers. North America’s market volume surpassed 40 million square meters in 2024, largely due to demand from institutional and commercial sectors. Asia-Pacific’s rapid infrastructure expansion, particularly in China and India, is expected to add over 25 million square meters of new cladding installations by 2030. Collectively, these regional trends reflect a strong global alignment toward sustainable, efficient, and design-oriented construction practices across residential, commercial, and industrial domains.

The North American Cladding Systems Market held a 36% share in 2024, supported by rapid growth in the commercial, healthcare, and institutional sectors. Regulatory measures such as LEED certification and energy code updates have spurred the adoption of high-performance and insulated cladding materials. Advanced digital fabrication and smart façade systems are increasingly integrated into new builds, with 42% of large-scale projects employing automation and 3D modeling for installation optimization. Key regional players like Kingspan North America have expanded production capacity by 15% to meet sustainability-driven demand. Regional consumer behavior indicates higher adoption in healthcare, finance, and retail construction, where energy-efficient façades and aesthetic design drive investment decisions. This trend is reinforced by government-backed green infrastructure programs promoting zero-carbon buildings across the U.S. and Canada.

The European Cladding Systems Market accounted for approximately 29% of the global volume in 2024, led by major economies such as Germany, the United Kingdom, and France. EU regulations under the Energy Performance of Buildings Directive (EPBD) have accelerated demand for recyclable, low-emission materials. Around 47% of new urban projects in Western Europe incorporated ventilated façades or fiber cement cladding due to their durability and insulation benefits. Local companies like Etex Group and Alucobond continue investing in digital manufacturing and carbon-neutral production. Regulatory pressure has created demand for explainable, certified cladding materials, with 52% of enterprises now prioritizing environmental compliance in procurement. The region’s consumer behavior is defined by preference for modular, retrofit-friendly systems, particularly in public and commercial renovations where sustainability reporting is mandatory.

Asia-Pacific held 25% of the global market volume in 2024, emerging as the fastest-growing regional segment. China, India, and Japan are the top consumers, together accounting for over 70% of regional installations. The region’s construction boom—driven by smart city initiatives and industrial expansion—has accelerated adoption of lightweight aluminum and composite cladding systems. Advanced manufacturing hubs in China have achieved a 20% production increase year-over-year, supporting large-scale infrastructure projects. India’s commercial construction sector reported a 28% surge in façade modernization between 2023 and 2024. Local manufacturers are increasingly leveraging digital twin design tools to enhance accuracy and performance. Consumer behavior emphasizes energy savings and design adaptability, reflecting a preference for modular, eco-friendly exteriors aligned with government-led urban development programs.

The South American Cladding Systems Market represented roughly 8% of global share in 2024, driven primarily by Brazil, Argentina, and Chile. Regional construction growth is supported by large-scale commercial and public infrastructure projects, particularly in energy and transportation sectors. Government incentives for sustainable building materials have increased adoption of composite and metal cladding systems by 18% year-on-year. Brazilian manufacturers have expanded their local production by 12% to meet growing demand from industrial applications. Consumer behavior in South America is increasingly aligned with aesthetic appeal and cost-efficiency, favoring modular panels and insulated façades. Rising adoption of building codes focused on fire safety and energy optimization further underscores the region’s modernization efforts.

The Middle East & Africa region accounted for 12% of the global Cladding Systems Market in 2024, led by countries such as the UAE, Saudi Arabia, and South Africa. Demand is primarily driven by extensive infrastructure and tourism-related projects, including mixed-use developments and smart city initiatives. High adoption of solar-integrated and fire-resistant façades has been observed, with over 35% of new constructions integrating advanced cladding materials. Regional manufacturers are collaborating with international firms to improve design and material technology. Local company Emirates Building Systems has increased façade production capacity by 14% to cater to mega-projects under Vision 2030 initiatives. Consumer behavior trends highlight preference for high-durability, weather-resistant materials suited to extreme climatic conditions.

• United States (21%) – Leads due to high production capacity, technological innovation, and strong adoption of energy-efficient façades across commercial and institutional projects.

• China (17%) – Dominates through large-scale construction output, continuous urbanization, and government-backed investments in smart infrastructure and green building initiatives.

The global Cladding Systems market exhibits a moderately consolidated landscape, with the top five companies accounting for approximately 48% of the total market share in 2024. The market hosts nearly 85–90 active competitors, spanning across metal, vinyl, ceramic, fiber cement, and composite cladding segments. Around 62% of manufacturers are now focusing on sustainable materials, integrating recycled metal, bio-based composites, and low-carbon façades to align with global green building mandates. Competitive intensity is heightened by digital transformation, with 35% of large-scale construction projects adopting AI-driven façade design or robotic fabrication systems to enhance precision and speed. Between 2022 and 2024, over 30 strategic mergers, acquisitions, and partnerships reshaped the market structure, primarily aimed at capacity expansion and regional diversification. European and North American players maintain leadership in high-quality compliance-based systems, while Asia-Pacific participants gain ground through cost efficiency and rapid urbanization projects. Overall, competition in the Cladding Systems market is driven by material innovation, regulatory compliance, and technological integration across the construction value chain.

Rockwool International A/S

Nichiha Corporation

Etex Group NV

Alucobond (3A Composites)

Cembrit Holding A/S

James Hardie Industries plc

Boral Limited

FunderMax GmbH

Trespa International B.V.

Sika AG

Saint-Gobain S.A.

Mitsubishi Chemical Corporation

Technological innovation is significantly reshaping the Cladding Systems market, with digital design tools, sustainable material engineering, and automated fabrication processes driving operational efficiency and product differentiation. Around 68% of construction companies globally have adopted Building Information Modeling (BIM) for façade and cladding design, improving accuracy, reducing rework rates by nearly 30%, and enabling precise prefabrication. The integration of 3D scanning and digital twin technologies has further enhanced project visualization, allowing real-time simulation of building performance before installation.

Material science advancements are also central to the industry’s evolution. Over 55% of new cladding products launched in 2024 utilized hybrid materials, including fiber-cement composites, ceramic laminates, and lightweight aluminum honeycomb panels. These materials offer up to 40% better thermal insulation and 25% lower lifecycle maintenance costs compared to conventional metal or stone cladding. Furthermore, the increasing use of self-cleaning and photocatalytic coatings—now featured in about 22% of premium façade projects—has reduced maintenance frequency, aligning with green construction goals.

Automation and robotics are transforming production workflows. Approximately 33% of leading cladding manufacturers have adopted robotic panel cutting, folding, and installation systems, cutting production time by 20–25%. The shift toward modular and prefabricated systems has driven demand for high-precision CNC machining and AI-powered quality inspection tools, ensuring consistency and compliance in large-scale urban projects. Collectively, these technological advancements are not only enhancing durability and aesthetics but also positioning the Cladding Systems industry at the forefront of the global smart construction revolution.

In January 2023, Kingspan Group Plc launched an insulated panel line that delivered a 41% reduction in embodied-carbon across production compared to their prior standard panels, marking a major step in sustainability-driven façade solutions.

In October 2024, Tata Steel Limited announced a £1.25 billion investment to convert its Port Talbot steelworks to scrap-based electric arc furnace production, targeting a 90% reduction in CO₂ emissions and enabling supply of low-carbon steel for cladding substrate use.

In January 2024, Nichiha Corporation introduced new architectural wall-panel products at the International Builders’ Show (IBS), including a “ConcreteBoard” cladding that replicates concrete texture at lighter weight and full rainscreen compatibility for multifamily residential applications.

In December 2023, Etex Group NV acquired fibre-cement innovator SCALAMID to strengthen its architectural cladding portfolio with advanced digital print and coating technologies, supporting lightweight façade growth and customised design solutions in exteriors.

The Cladding Systems Market Report spans product offerings, applications, geographic regions, technology trends and industry segments, delivering a comprehensive framework for strategic decision-making. In the product dimension, it covers multiple types such as metal panels, composite panels, fiber-cement boards, stone panels, and modular façade systems. Application areas include new build residential, commercial, industrial, public infrastructure and renovation/retrofit projects. Geographic coverage addresses North America, Europe, Asia-Pacific, South America and Middle East & Africa, each analysed in terms of volume, end-use drivers and regulatory environments. Technology and innovation are key focus areas — for example, automated prefabrication, digital twin design, smart façades and low-embodied-carbon materials. The report also examines industry focus areas such as green building certification, fire-resistant material mandates, off-site construction methods and supply-chain resilience. Emerging segments such as solar-integrated cladding, modular envelope systems for data centres and high-rise urban refurbishments are included to highlight future growth potential. This breadth means the report supports executive-level planning, product portfolio optimisation, regional expansion strategies and innovation pipeline development in the cladding systems space.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 300.39 Million |

Market Revenue in 2032 | USD 457.52 Million |

CAGR (2025 - 2032) | 5.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Kingspan Group Plc, Tata Steel Limited, Arconic Corporation, Rockwool International A/S, Nichiha Corporation, Etex Group NV, Alucobond (3A Composites), Cembrit Holding A/S, James Hardie Industries plc, Boral Limited, FunderMax GmbH, Trespa International B.V., Sika AG, Saint-Gobain S.A., Mitsubishi Chemical Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |