Reports

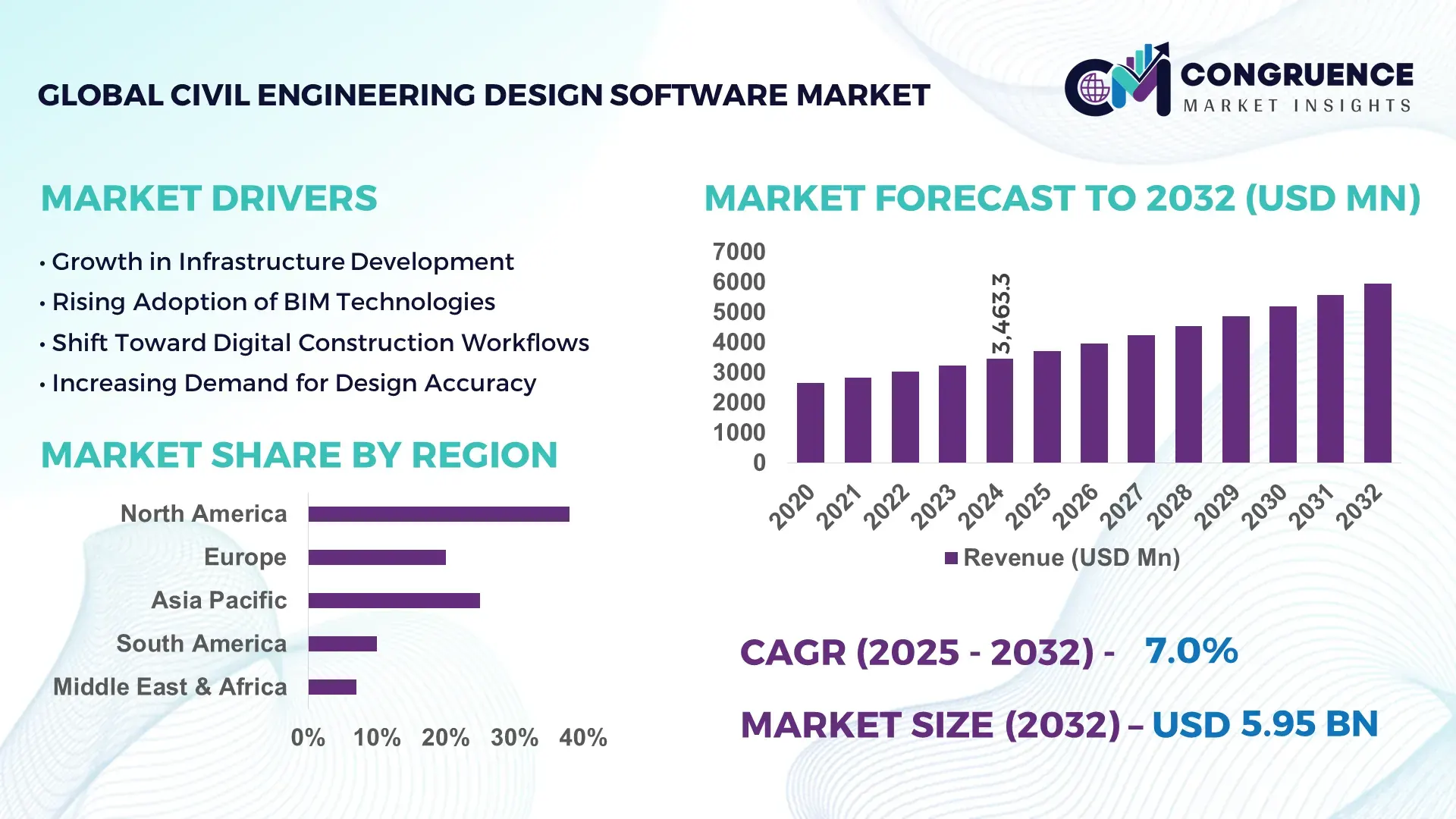

The Global Civil Engineering Design Software Market was valued at USD 3463.32 Million in 2024 and is anticipated to reach a value of USD 5950.63 Million by 2032 expanding at a CAGR of 7% between 2025 and 2032. This growth is driven by the rapid adoption of advanced modeling and simulation tools supporting sustainable infrastructure development.

The United States leads the Civil Engineering Design Software market, with over 45,000 licensed enterprise deployments and annual software investment exceeding USD 820 Million in 2024. U.S. firms leverage high-performance computing for large-scale infrastructure design, generating more than 60% of global BIM (Building Information Modeling) integrated workflows. Federal and state-level funding has accelerated adoption across transportation, water resources, and energy sectors, with documented productivity improvements of 25–30% in project delivery timelines.

Market Size & Growth: Valued at USD 3463.32 Million in 2024; projected to reach USD 5950.63 Million by 2032 at a 7% CAGR, driven by demand for 3D modeling and integrated design platforms.

Top Growth Drivers: Increased BIM adoption (42%), cloud-based design platforms usage (35%), infrastructure modernization requirements (28%).

Short-Term Forecast: By 2028, expected average project cost reduction of 18% through automation and collaborative tools.

Emerging Technologies: AI-assisted design optimization; Digital Twins integration; augmented reality for field validation.

Regional Leaders: North America ~USD 2.1B by 2032 with accelerated smart-city projects; Europe ~USD 1.5B driven by green infrastructure policies; Asia-Pacific ~USD 1.8B with rapid urbanization and transport expansion.

Consumer/End-User Trends: Municipal engineering departments increasing adoption of cloud-based collaborative suites; contractors emphasizing interoperability.

Pilot or Case Example: 2025 pilot in a major U.S. transit authority delivered 22% reduction in rework through AI-enhanced clash detection.

Competitive Landscape: Market leader ~28% share; key competitors include Bentley Systems, Autodesk, Trimble, Hexagon, and Nemetschek Group.

Regulatory & ESG Impact: Stricter emissions and sustainability regulations drive adoption of energy-efficient design modules and compliance reporting tools.

Investment & Funding Patterns: Over USD 450 Million in venture funding in 2024–2025 for SaaS and analytics platforms; growth in project-finance tied to digital infrastructure initiatives.

Innovation & Future Outlook: Enhanced multi-user real-time collaboration, integration with IoT sensors for feedback loops, and predictive maintenance planning via machine learning.

The Civil Engineering Design Software market spans transportation, water resources, energy, and urban development sectors—with transportation infrastructure contributing a significant portion of global software utilization. Innovations such as cloud-native design suites, real-time data integration, and machine learning-based optimization are reshaping project delivery. Regulatory drivers include sustainability mandates and digital construction standards, while economic growth in emerging regions fuels consumption. Adoption patterns show heightened demand in mid-sized engineering firms for modular, scalable tools, and future trends point to AI-driven autonomous design workflows and expanded use of digital twin ecosystems.

The Civil Engineering Design Software market plays an increasingly strategic role in enabling efficient infrastructure planning, execution, and lifecycle management within the global civil construction ecosystem. Adoption of AI‑enhanced design tools delivers up to a 35% improvement compared to traditional CAD standards in design accuracy and task automation, driving firms to upgrade legacy workflows. North America dominates in volume, while Asia‑Pacific leads in adoption with over 48% of engineering enterprises deploying cloud‑based and AI‑integrated platforms, reflecting regional digital transformation variances. By 2028, integrated digital twin and predictive analytics tools are expected to improve project delivery KPIs, such as schedule adherence and cost accuracy, by more than 25%, as firms shift toward real‑time design and monitoring platforms.

Strategic investments are increasingly aligned with sustainability and regulatory compliance objectives; leading engineering firms are committing to ESG metrics with targets like a 20% reduction in embodied carbon in infrastructure design by 2030 through software‑driven simulation and materials optimization workflows. In 2025, a major infrastructure contractor in the United States achieved a 28% reduction in design iteration cycles through deployment of generative AI modules, showcasing measurable performance gains from advanced toolsets. The ongoing integration of Building Information Modeling (BIM), generative design, cloud collaboration, and IoT interoperability underscores a future pathway where Civil Engineering Design Software becomes foundational to resilient infrastructure, compliance adherence, and sustainable growth across sectors.

The integration of advanced modeling tools, including 3D modeling, BIM, and AI‑based modules, is a key driver of demand for Civil Engineering Design Software. Over 42% of engineering and construction firms have incorporated 3D modeling into workflows to improve visualization, coordination, and planning accuracy, reducing design errors and rework. Cloud‑based platforms now support remote access and real‑time collaboration across distributed teams, enabling faster decision cycles and alignment among stakeholders. Government infrastructure programs in numerous countries mandate digital submittals and BIM compliance, prompting firms to adopt standardized design suites. As infrastructure projects grow in complexity, digital tools enable engineers to manage constraints and simulate outcomes, improving schedule predictability, resource utilization, and integration with GIS systems. This convergence of digital modeling, analytics, and collaborative capabilities has become essential for maintaining competitiveness and executing large‑scale projects with precision.

Despite strong demand, high acquisition and implementation costs hinder broader adoption of Civil Engineering Design Software. Professional solutions often require significant upfront investment for licenses, specialized hardware, and ongoing maintenance expenses, which can deter small and medium‑sized enterprises with constrained budgets. Training requirements add financial and time burdens, as engineers must attain proficiency through structured programs—frequently incurring costs for extended sessions and professional certifications. Interoperability with legacy systems poses additional implementation complexity, requiring technical expertise and custom integration efforts that can delay full deployment. Data security concerns with cloud platforms and compliance with regional regulations further contribute to hesitancy among firms handling sensitive infrastructure data. These combined restraints slow market penetration, particularly in regions with budgetary limitations or less mature digital ecosystems.

Emerging AI and analytics capabilities present significant opportunities for the Civil Engineering Design Software market, enabling predictive insights, automated optimization, and enhanced design intelligence. Next‑generation modules capable of processing millions of sensor data points daily with predictive accuracy rates exceeding 90% are unlocking new use cases in structural health monitoring and asset lifecycle management. Cloud‑native analytics platforms attract enterprise deployments seeking real‑time condition assessments across infrastructure portfolios, particularly utility networks and transportation systems. Additionally, AI‑driven generative design tools can rapidly produce thousands of design alternatives, enabling engineers to evaluate performance trade‑offs efficiently. These advancements are particularly valuable for firms managing extensive civil assets requiring continuous monitoring, remote diagnostics, and adaptive planning. As demand grows for data‑centric decision‑making and asset resilience, vendors are positioned to capitalize on analytics‑enabled solutions that extend beyond traditional design functions.

Workforce skill gaps present a persistent challenge for growth in the Civil Engineering Design Software market. Many engineers and technical staff lack proficiency with advanced digital tools, leading to longer onboarding periods and reduced productivity. Industry metrics show that only about 54% of new users achieve proficiency within 30 days of software deployment, underscoring the complexity of mastering BIM, analytics, and AI‑enhanced features. Training programs often require substantial time commitments and financial investment, diverting resources from core project work. Recruitment also struggles to keep pace with demand for specialists skilled in digital design, data analytics, and cloud collaboration—creating shortages that particularly affect small and mid‑sized firms. These gaps can lead to project delays, inefficiencies in design execution, and underutilization of software capabilities, ultimately hindering the pace of digital transformation across the sector.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Civil Engineering Design Software market. Approximately 55% of new projects report measurable cost benefits from using prefabricated and modular practices. Pre-bent and cut elements are fabricated off-site with automated machines, reducing labor requirements by 30% and accelerating project timelines by 25%. Europe and North America are witnessing the highest demand for high-precision software capable of supporting modular planning, integration, and clash detection workflows.

• Integration of AI and Predictive Analytics: AI-driven tools now influence over 48% of large-scale infrastructure design projects, enhancing accuracy and reducing rework. Predictive analytics modules improve structural performance simulations by up to 32%, allowing engineers to forecast material needs and potential design conflicts before on-site execution. Early adopters report up to a 20% reduction in design iteration cycles, while machine learning algorithms optimize layout efficiency and compliance with regulatory standards. Asia-Pacific firms lead in adopting AI-assisted design, with 43% of urban development projects utilizing predictive modules.

• Expansion of Cloud-Based Collaboration Platforms: Cloud-enabled Civil Engineering Design Software supports real-time collaboration for distributed teams, with 61% of engineering enterprises adopting remote-access capabilities. Projects using cloud collaboration experience 28% faster coordination between stakeholders and a 22% reduction in design conflicts. North America dominates in deployment volume, whereas Europe leads in adoption intensity, with 52% of firms leveraging integrated cloud modules for BIM workflows and digital twin management.

• Focus on Sustainability and ESG Compliance: Civil Engineering Design Software increasingly incorporates energy modeling, material lifecycle analysis, and carbon footprint assessment tools. Firms report up to a 17% improvement in sustainable design outcomes, such as reduced material waste and optimized energy efficiency. Regulatory pressures drive adoption in Europe and North America, where 44% of projects now mandate ESG reporting within digital design platforms. This trend also supports green certifications and sustainable infrastructure investment initiatives.

The Civil Engineering Design Software market is structured around key segmentation pillars—type, application, and end-user—each reflecting distinct deployment patterns and value drivers. By type, solutions range from traditional 2D drafting and 3D modeling to advanced BIM and simulation environments, with differing levels of integration into project lifecycle workflows. Application segmentation spans infrastructure design, structural analysis, transportation planning, and terrain mapping, showing how diverse engineering disciplines leverage tailored software capabilities. End-user segmentation differentiates between large engineering consultancies, independent contractors, public sector agencies, and specialist design firms, each exhibiting unique adoption rates, implementation depths, and software customization needs. Precision modeling, collaborative cloud platforms, and specialized analytics modules are increasingly significant across segments. Data indicate that over 62% of projects utilize 3D modeling tools for core design tasks, while 4D and 5D extensions support schedule and cost integration needs, illustrating how software capabilities tier according to project complexity and user requirements. This segmentation helps decision-makers align product portfolios with specific technical demands and organizational maturity levels.

The Civil Engineering Design Software market encompasses a range of product types including 3D modeling/BIM platforms, 2D CAD drafting tools, 4D schedule and simulation extensions, and specialized analysis modules. 3D modeling and BIM platforms currently account for the largest share (~62%) of adoption, due to their foundational role in visual design, clash detection, and integrated documentation workflows for complex infrastructure projects. 4D/BIM time-linked extensions hold around 21% adoption, enabling dynamic schedule visualization and real-time sequencing that enhance project control and reduce onsite conflicts. While 2D tools remain relevant for basic drafting, they comprise a smaller share as firms prioritize integrated, multidimensional design environments. The remaining segments, including 5D cost-linked modules and geospatial/terrain analysis add-ons, together represent roughly 17% of deployments, supporting advanced budgeting or GIS integration.

Civil Engineering Design Software applications include infrastructure planning and transportation network design, structural modeling, site development, and terrain analysis. Infrastructure planning and transportation design lead with approximately 45% of deployments, as large road, bridge, and urban projects rely on advanced modeling and coordination capabilities. Structural analysis and safety assessment applications are the fastest-growing segment, fueled by simulation engines that improve load and stress visualization for high-rise and seismic environments (complexity tools usage rising around 20%). Other applications—such as site grading, hydrology modeling, and utility design—collectively account for 35% of usage, supporting land development and environmental compliance.

End-users of Civil Engineering Design Software include large engineering and construction firms, specialized design consultancies, public infrastructure agencies, and smaller civil practices. Large engineering consultancies are the leading segment with about 40% market share, benefiting from extensive project portfolios and the need for integrated design and analysis capabilities. Public sector agencies are the fastest-growing end-user group, driven by digital mandates for infrastructure planning and regulatory compliance, with software procurement growth exceeding 22% for state and municipal projects. Other end-users, including boutique consultancies and independent contractors, account for roughly 38% of usage, leveraging modular and scalable software for specialized projects such as land development and stormwater management.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8% between 2025 and 2032.

North America leads with over 16,500 active enterprise deployments, particularly in transportation and urban infrastructure projects, while Asia-Pacific is accelerating adoption with more than 12,000 new projects initiated in 2024 alone. Europe holds 27% of regional share, with Germany and the UK driving demand for regulatory-compliant solutions. South America contributes roughly 6% to the market, supported by Brazil and Argentina’s infrastructure modernization programs. The Middle East & Africa region accounts for 4%, with UAE and South Africa leading oil, gas, and smart-city-related design software initiatives. Across these regions, adoption of cloud-based collaboration, AI-assisted modeling, and digital twin technologies has increased project efficiency by up to 30%, while government incentives and regulatory mandates are further accelerating software deployment in public infrastructure projects.

How is digital transformation reshaping engineering design efficiency?

North America holds 38% of the Civil Engineering Design Software market, driven primarily by transportation, urban development, and energy infrastructure projects. Key industries such as highways, bridges, and utility networks are increasingly deploying AI-assisted BIM tools, which reduce design iteration cycles by up to 25%. Federal and state-level digital infrastructure policies support the adoption of cloud-based platforms and interoperability standards. Local players like Bentley Systems are enhancing platform capabilities with predictive analytics and real-time collaboration modules. Enterprise adoption is highest in construction, healthcare, and finance sectors, where software integration improves project planning, monitoring, and compliance. Regional consumer behavior reflects a preference for scalable, modular software solutions that support cross-departmental collaboration and regulatory reporting.

What regulatory and sustainability trends are shaping engineering software adoption?

Europe contributes 27% to the Civil Engineering Design Software market, with Germany, the UK, and France being the primary markets. Adoption is heavily influenced by strict sustainability regulations and building codes, prompting demand for explainable, compliance-focused software solutions. Emerging technologies such as cloud-based BIM, generative design, and AI-driven structural analysis are increasingly integrated into projects. Local players like Nemetschek Group are advancing collaborative platforms that combine energy modeling with lifecycle analysis. Regional behavior trends indicate high adoption among public sector agencies and large consultancies, driven by regulatory reporting requirements and green infrastructure initiatives that require measurable ESG improvements.

How is rapid urbanization driving digital design software adoption?

Asia-Pacific is emerging as the fastest-growing market, with over 12,000 new Civil Engineering Design Software projects initiated in 2024. Leading countries include China, India, and Japan, where infrastructure expansion, transportation modernization, and smart city programs drive demand. Software adoption emphasizes integration with digital twin technologies, AI-assisted optimization, and cloud collaboration platforms. Companies like China State Construction Engineering are implementing BIM-driven workflows for large-scale projects, improving design accuracy by 28%. Regional consumer trends show strong demand for modular, scalable software solutions capable of supporting both public and private infrastructure projects in urbanizing regions.

What factors influence infrastructure software adoption in emerging markets?

South America accounts for roughly 6% of the Civil Engineering Design Software market, with Brazil and Argentina leading demand due to urban expansion and energy sector projects. Government incentives and trade policies encourage investment in infrastructure digitalization. Companies are increasingly adopting cloud-based design and simulation tools for public transportation and utility projects. Local players focus on modular and low-cost software solutions to meet regional budget constraints. Consumer behavior in South America emphasizes ease of use, language localization, and adaptability to smaller-scale construction projects, enabling broader adoption across both public and private infrastructure sectors.

How is infrastructure modernization driving software demand in emerging regions?

The Middle East & Africa region contributes about 4% of the market, with UAE and South Africa leading adoption for oil, gas, and smart city infrastructure projects. Technological modernization, including digital twin integration, AI-based planning, and BIM-enabled workflows, supports faster design cycles and improved project coordination. Government regulations and trade partnerships incentivize sustainable and energy-efficient design practices. Local players focus on cloud-based and scalable solutions to accommodate diverse project requirements. Consumer behavior highlights preference for software that supports high-speed collaboration, regulatory compliance, and multi-language capabilities to manage diverse project teams and international partners.

United States: 38% market share; strong end-user demand from large-scale infrastructure projects and advanced technological integration drives dominance.

China: 21% market share; rapid urbanization, infrastructure investments, and adoption of AI-assisted design workflows fuel market leadership.

The Civil Engineering Design Software market is moderately consolidated, with an estimated over 60 active competitors globally, ranging from large multinational software providers to specialized regional vendors. The top five companies—Bentley Systems, Autodesk, Trimble, Hexagon, and Nemetschek Group—together account for approximately 68% of total market adoption, highlighting significant concentration in high-end design and BIM solutions. Strategic initiatives such as partnerships with construction firms, cloud integration collaborations, and AI-enhanced product launches have intensified competition. Over 45% of firms are investing in generative design, digital twin integration, and real-time collaboration platforms to differentiate themselves. Mergers and acquisitions are shaping the competitive landscape, with more than 12 deals completed globally between 2023 and 2024 aimed at expanding geographic reach or enhancing technological capabilities. Regional competition varies, with North America seeing strong enterprise-focused consolidation, Europe emphasizing regulatory-compliant solutions, and Asia-Pacific experiencing fast-growing adoption among mid-sized firms. Innovation trends such as predictive analytics, modular design support, and sustainability-driven software features are now key factors influencing market positioning and competitive advantage.

Hexagon

Nemetschek Group

Dassault Systèmes

RIB Software

ProtaStructure

Allplan

Carlson Software

Vectorworks

Bricsys

The Civil Engineering Design Software market is increasingly driven by the adoption of advanced digital technologies that enhance design accuracy, collaboration, and efficiency. Building Information Modeling (BIM) platforms currently account for approximately 62% of enterprise deployments, providing integrated 3D modeling, clash detection, and project documentation capabilities. Advanced 4D and 5D BIM extensions are being implemented in over 28% of large-scale infrastructure projects, linking schedules and cost estimates directly with design models to improve project management efficiency.

Artificial intelligence (AI) and machine learning are emerging as transformative technologies, supporting automated design optimization, predictive maintenance planning, and real-time risk analysis. AI modules now assist in identifying potential structural conflicts and material inefficiencies, reducing design rework by up to 25% in active projects. Digital twin technology is gaining traction, with more than 1,200 smart city and urban infrastructure projects globally integrating real-time simulation for monitoring structural performance and lifecycle planning.

Cloud-based platforms have also become essential, enabling 61% of engineering enterprises to conduct remote collaboration, access multi-user environments, and streamline cross-department coordination. Generative design and parametric modeling tools are being increasingly applied in transportation, energy, and water infrastructure projects, producing thousands of optimized alternatives and improving material utilization by 18–20%. Emerging technologies such as augmented reality (AR) and virtual reality (VR) are also being integrated for immersive design review, training, and stakeholder presentations. Overall, technological advancements in AI, digital twins, cloud collaboration, and AR/VR are positioning Civil Engineering Design Software as a strategic tool for improving project accuracy, compliance, and operational efficiency across global infrastructure initiatives.

• In October 2024, Bentley Systems unveiled OpenSite+, a generative AI‑powered civil site design application that automates layout optimization and drawing production, boosting design speed by up to 10× and enhancing productivity and accuracy in residential, commercial, and industrial site planning. (Bentley Systems)

• In January 2024, Autodesk rolled out a major update to Autodesk Forma, introducing the Forma Board for collaborative design visualization, enhanced solar energy analysis tools, and streamlined conceptual design workflows, significantly improving stakeholder collaboration and early‑stage planning efficiency. (Autodesk)

• In June 2024, Trimble launched the Trimble Unity asset lifecycle management suite, enabling owners and infrastructure teams to plan, design, build, operate, and maintain assets via centralized data and connected digital workflows, helping reduce total cost of ownership by up to 40%. (Trimble Mediaroom)

• In August 2024, Trimble expanded Trimble Unity with AI and GIS enhancements, adding pavement management and project integration features that streamline asset maintenance insights, improve field decision‑making, and extend digital capabilities for infrastructure design and operations. (engineering.com)

The Civil Engineering Design Software Market Report provides a comprehensive analysis of the global landscape, covering extensive segmentation by product type, application area, and geographic deployment to support strategic decisions. In product segmentation, the report examines core design tools such as 3D modeling and BIM platforms, 2D CAD drafting utilities, advanced analysis modules, and collaborative cloud‑native extensions, detailing their roles in different engineering workflows. Application analysis addresses infrastructure planning, structural modeling, transportation and terrain design, and site development, with insights into how each application integrates with adjacent project lifecycle tools such as scheduling and cost estimation systems.

Regionally, the scope spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting unique adoption trends, technology priorities, regulatory influences, and consumer behaviors in each market. The report also assesses emerging technologies, including digital twin integration, AI automation, augmented and virtual reality review tools, and mobile field integration, reflecting real‑time collaboration and data streaming demands. End‑user insights encompass large engineering consultancies, public agencies, design firms, and independent contractors, profiling deployment depth, tool preferences, and custom workflow integrations.

Additionally, the report explores competitive dynamics with company profiles, innovation trends, strategic alliances, and technology partnerships emphasizing how vendors enhance interoperability and performance. Targeted for decision‑makers, the scope includes actionable intelligence on niche segments such as geotechnical analysis plug‑ins, modular design tools, and AI‑driven optimization engines, offering a thorough basis for investment, procurement, and deployment planning across civil engineering projects worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 3463.32 Million |

Market Revenue in 2032 | USD 5950.63 Million |

CAGR (2025 - 2032) | 7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Bentley Systems, Autodesk, Trimble, Hexagon, Nemetschek Group, Dassault Systèmes, RIB Software, ProtaStructure, Allplan, Carlson Software, Vectorworks, Bricsys |

Customization & Pricing | Available on Request (10% Customization is Free) |