Reports

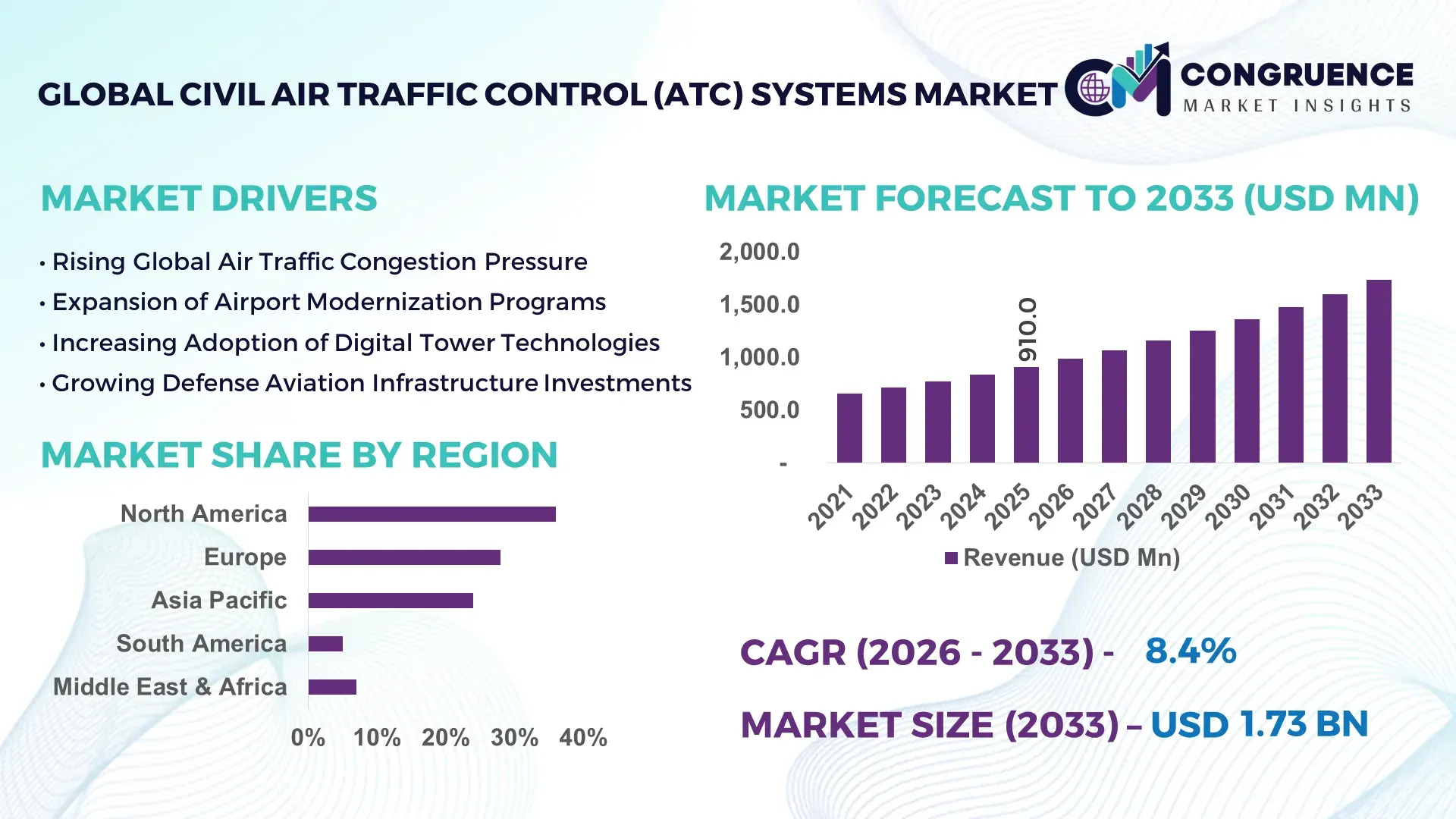

The Global Civil Air Traffic Control (ATC) Systems Market was valued at USD 910.0 Million in 2025 and is anticipated to reach a value of USD 1,734.9 Million by 2033 expanding at a CAGR of 8.4% between 2026 and 2033.

The market is accelerating due to rapid deployment of AI-assisted air traffic management platforms, satellite-based surveillance systems, and modernization of aging aviation infrastructure across high-density commercial flight corridors, improving aircraft routing efficiency by over 28% in congested airspaces. Between 2024 and 2026, global aviation authorities intensified digital airspace modernization initiatives following rising passenger traffic recovery, cross-border airspace congestion, and ICAO-led operational harmonization programs, forcing airports and navigation providers to prioritize automated traffic coordination systems and cyber-secure ATC infrastructure.

The United States dominates the global Civil Air Traffic Control (ATC) Systems Market with approximately 34% market share, supported by more than 19,700 operational airports and one of the world’s largest controlled airspace networks. The Federal Aviation Administration accelerated NextGen modernization programs with over USD 4 billion allocated toward digital tower deployment, ADS-B integration, and data-driven traffic optimization systems. Compared with conventional radar-centric infrastructure, AI-enabled predictive traffic sequencing platforms improve runway throughput by nearly 22% while reducing aircraft holding delays by 18%. Major aviation hubs including Atlanta, Dallas, and Chicago collectively manage over 6 million annual aircraft movements, reinforcing the country’s operational leadership and high-volume technology adoption capacity.

As airspace complexity intensifies globally, technology-led ATC modernization is shifting from infrastructure upgrade to a strategic aviation competitiveness requirement, forcing operators and governments to accelerate long-term digital transformation investments.

Market Size & Growth: The market will grow from USD 910.0 Million in 2025 to USD 1,734.9 Million by 2033 at 8.4% CAGR, driven by AI-enabled airspace automation and airport digitalization.

Top Growth Drivers: Satellite surveillance adoption is rising 31%, digital tower deployment is increasing 27%, and AI traffic sequencing integration is expanding 24% globally.

Short-Term Forecast: By 2028, advanced ATC systems will reduce aircraft holding delays by 19% and improve runway throughput efficiency by 23%.

Emerging Technologies: AI analytics, cloud-native ATC platforms, and remote digital towers are accelerating operational automation by over 35% across global aviation networks.

Regional Leaders: North America will exceed USD 624 Million demand, Europe USD 486 Million through SESAR upgrades, and Asia-Pacific USD 416 Million from airport expansion programs.

Consumer/End-User Trends: More than 62% of international airports are prioritizing predictive traffic coordination systems to strengthen congestion management and operational continuity.

Pilot/Case Example: In 2025, an Asia-Pacific digital tower modernization project improved traffic response efficiency by 26% while reducing coordination delays by 17%.

Competitive Landscape: Thales leads with nearly 14% market share alongside Indra, RTX, Leonardo, and Saab through advanced aviation modernization contracts.

Regulatory & ESG Impact: Emissions-focused flight optimization policies reduced inefficient aircraft holding patterns by 14%, accelerating sustainable ATC system deployment.

Investment & Funding: Global ATC modernization investments surpassed USD 5.2 Billion between 2024 and 2026 through infrastructure partnerships and regional airport expansion initiatives.

Innovation & Future Outlook: Autonomous traffic coordination, quantum-secure aviation communication, and AI-driven predictive routing are redefining next-generation intelligent airspace ecosystems.

Commercial aviation contributes nearly 58% of total Civil Air Traffic Control (ATC) Systems deployment demand due to rising international passenger density and airport expansion programs. AI-assisted traffic sequencing platforms improved flight scheduling efficiency by 21%, while digital tower implementation reduced staffing dependency by 16% across selected airports. Asia-Pacific is experiencing accelerated infrastructure deployment amid regional airport construction programs, while Europe’s regulatory-led modernization initiatives continue reshaping interoperability standards. Increasing geopolitical focus on resilient aviation infrastructure and cross-border airspace harmonization is also influencing procurement strategies. These operational and technology shifts are setting the foundation for deeper strategic transformation across the global ATC ecosystem.

The Civil Air Traffic Control (ATC) Systems Market is rapidly transforming into a strategic pillar of national aviation resilience, airport competitiveness, and airspace efficiency optimization. Rising global passenger volumes, increasing aircraft movement density, and pressure on aging airport infrastructure are accelerating investments in intelligent traffic coordination systems, remote digital towers, and AI-enabled airspace management platforms. Governments and airport operators are no longer treating ATC modernization as a routine infrastructure upgrade; it is becoming a mission-critical investment directly tied to aviation capacity expansion, safety optimization, and emissions reduction targets.

Global aviation networks are also facing mounting operational pressure from supply chain instability, labor shortages, cybersecurity threats, and regulatory harmonization requirements between 2024 and 2026. These shifts are forcing aviation authorities to accelerate digital transformation programs and integrate predictive traffic analytics into national airspace systems. AI-enabled traffic sequencing technology improves operational efficiency by nearly 29% while reducing coordination-related operating costs by 18% compared to conventional radar-based control systems. This measurable operational advantage is redefining procurement priorities across major aviation economies.

North America leads in operational volume and controlled airspace density, while Europe leads in modernization-driven adoption with over 41% of major airports integrating digital traffic coordination frameworks under SESAR-aligned aviation transformation programs. Meanwhile, Asia-Pacific is reshaping the competitive landscape through large-scale airport infrastructure expansion and smart aviation corridor deployment. Over the next three years, automated flight routing systems are expected to reduce average aircraft holding times by 20% while improving runway utilization rates by approximately 24%.

Sustainability-linked aviation modernization is also becoming a competitive differentiator. Optimized airspace routing systems are reducing unnecessary fuel burn by nearly 12%, improving both regulatory compliance and airline operating efficiency. In 2025, a major Middle Eastern aviation modernization project improved aircraft turnaround coordination efficiency by 19% through centralized digital traffic management deployment. Major industry participants are shifting capital allocation toward AI-powered traffic management software, cloud-integrated surveillance infrastructure, and cyber-secure aviation communication systems to secure long-term strategic positioning. Companies prioritizing scalable automation, predictive analytics integration, and interoperable digital airspace ecosystems are rapidly strengthening their competitive advantage as global aviation systems move toward fully connected intelligent traffic environments.

The Civil Air Traffic Control (ATC) Systems Market is undergoing rapid structural transformation driven by increasing global air traffic density, aviation infrastructure modernization, and integration of intelligent airspace management technologies. Rising pressure on airports to optimize runway throughput, reduce aircraft holding patterns, and improve operational coordination is accelerating adoption of automated traffic sequencing and satellite-based surveillance systems. More than 54% of international airports are currently prioritizing digital ATC modernization programs to address congestion management and operational efficiency requirements.

The market is also being reshaped by regulatory harmonization initiatives, cybersecurity mandates, and cross-border airspace interoperability requirements. Governments across North America, Europe, and Asia-Pacific are increasing investments in next-generation communication, navigation, and surveillance infrastructure to improve traffic coordination capabilities. Simultaneously, aviation authorities are balancing modernization ambitions against infrastructure complexity, integration costs, and legacy system compatibility challenges. Competitive positioning increasingly depends on technology scalability, real-time analytics capability, and long-term operational resilience rather than traditional hardware-centric deployment models.

AI-driven automation is becoming the primary structural growth engine within the Civil Air Traffic Control (ATC) Systems Market as airports and aviation authorities face mounting operational pressure from rising aircraft movement density and airspace congestion. Automated traffic sequencing systems improve runway utilization efficiency by nearly 24% while reducing coordination delays by approximately 18%, directly strengthening airport throughput capacity without requiring large-scale physical infrastructure expansion. More than 46% of major international airports initiated AI-supported traffic optimization projects between 2024 and 2026. Global aviation recovery and geopolitical pressure on resilient transport infrastructure are also accelerating investment cycles. Increased cross-border aviation coordination requirements are forcing governments to modernize legacy radar-centric systems with satellite-based surveillance and predictive analytics capabilities. In response, major companies are accelerating strategic partnerships, expanding cloud-based ATC platforms, and increasing investment in digital tower deployment. Several aviation technology providers expanded R&D spending by over 20% to strengthen intelligent traffic management capabilities and secure long-term airport modernization contracts across high-growth regions.

High infrastructure modernization costs and integration complexity remain major structural restraints across the Civil Air Traffic Control (ATC) Systems Market. More than 43% of airports operating legacy radar-based systems face compatibility limitations when integrating AI-driven traffic management platforms and cloud-enabled surveillance networks. Large-scale modernization programs frequently require multi-year deployment cycles, increasing operational disruption risk and delaying return on investment timelines. Cybersecurity compliance requirements and fragmented airspace communication standards are further constraining implementation scalability. In several developing aviation markets, infrastructure gaps and budget limitations have delayed digital tower deployment by over 17%. Aviation authorities are also facing rising costs linked to skilled workforce shortages and system interoperability testing. To mitigate these risks, companies are diversifying component sourcing strategies, deploying modular upgrade architectures, and signing long-term technology integration contracts. Several global ATC providers are increasingly offering phased modernization frameworks to reduce upfront capital pressure and accelerate adoption among mid-sized airport operators.

The rapid expansion of smart airport ecosystems is creating high-impact opportunities for next-generation Civil Air Traffic Control (ATC) Systems providers. Predictive traffic management systems improve aircraft movement coordination efficiency by nearly 27% while reducing fuel-intensive holding patterns by approximately 15%, generating strong operational value for airlines and airport authorities. More than 39% of upcoming airport infrastructure projects globally now include integrated digital ATC capabilities as part of long-term aviation modernization planning. An emerging opportunity is developing around remote digital tower deployment in secondary airports and regional aviation hubs, where infrastructure optimization and workforce efficiency are becoming strategic priorities. AI-enabled surveillance systems are also improving low-visibility operational performance by nearly 21%, strengthening demand in high-traffic and weather-sensitive airspaces. In response, technology companies are expanding R&D investment, building aviation software ecosystems, and partnering with governments to strengthen long-term platform integration. Businesses capable of delivering scalable, cyber-secure, and interoperable traffic coordination solutions are positioning themselves for dominant participation in future intelligent airspace networks.

Execution complexity and long-term infrastructure scalability remain major challenges within the Civil Air Traffic Control (ATC) Systems Market. Large-scale digital ATC modernization programs require integration across radar systems, communication infrastructure, satellite surveillance networks, and airport operational databases, increasing implementation risk and deployment delays. More than 31% of modernization projects experienced operational integration challenges linked to legacy infrastructure dependencies and fragmented system architectures. The growing sophistication of cyber threats targeting aviation infrastructure is also intensifying pressure on system resilience and operational continuity. Airports deploying interconnected cloud-based ATC platforms reported cybersecurity compliance costs increasing by nearly 14% between 2024 and 2026. Simultaneously, rising aircraft movement density is placing additional strain on aging airport coordination systems, particularly in high-volume aviation corridors. To remain competitive, companies must accelerate investment in cyber-secure infrastructure, predictive analytics, and modular deployment frameworks while strengthening strategic partnerships with governments and airport operators to improve integration speed, reliability, and long-term scalability.

Digital tower deployments increased 32% across mid-sized airports as operators optimized staffing efficiency and remote coordination capabilities: Airports are rapidly replacing conventional tower operations with centralized digital traffic monitoring platforms integrating high-resolution surveillance and AI-assisted traffic sequencing. Deployment time declined by nearly 21%, while operational coordination accuracy improved by 18%. Companies are expanding regional deployment partnerships and restructuring software integration teams to accelerate airport onboarding amid growing aviation labor constraints.

AI-driven traffic sequencing adoption expanded 29%, reshaping aircraft movement optimization across congested international airspaces: Aviation authorities are integrating predictive analytics into real-time runway coordination systems to reduce aircraft holding patterns and improve slot management efficiency. Average taxi delay time declined by 16% in upgraded airports. Technology providers are scaling cloud-enabled analytics platforms and strengthening cybersecurity layers as regulatory scrutiny around digital aviation infrastructure intensifies globally.

Asia-Pacific airport modernization activity surged 34% as infrastructure expansion accelerated across high-density aviation corridors: Governments and airport operators are deploying satellite-based surveillance systems, digital communication platforms, and integrated navigation frameworks to support rising passenger and cargo movement volumes. Localized procurement strategies increased by 19% amid supply chain restructuring pressures. Global vendors are expanding regional manufacturing and engineering partnerships to strengthen execution speed and cost competitiveness.

Integrated sustainability-focused airspace optimization programs reduced unnecessary flight routing inefficiencies by 14% globally: Airlines and aviation authorities are prioritizing precision traffic coordination systems to lower fuel-intensive holding patterns and strengthen emissions compliance. Automated route optimization improved flight scheduling efficiency by 17%. ATC technology providers are repositioning product portfolios around environmental performance metrics, transforming sustainability compliance into a measurable operational advantage rather than a regulatory obligation.

The Civil Air Traffic Control (ATC) Systems Market is segmented by type, application, and end-user, with demand distribution strongly influenced by airport modernization intensity, aircraft movement density, and digital airspace transformation priorities. Communication systems account for nearly 38% of overall deployment demand due to their central role in real-time aircraft coordination and airspace interoperability. Surveillance systems are rapidly gaining traction as airports accelerate satellite-based monitoring adoption and AI-integrated traffic analytics deployment. Demand is shifting toward integrated digital ATC ecosystems combining automation, navigation, and predictive coordination capabilities rather than standalone infrastructure systems. Commercial aviation applications continue dominating deployment activity with over 61% market concentration, while regional airport modernization programs are accelerating demand for scalable remote tower solutions. Airlines, airport operators, and aviation authorities are increasingly prioritizing modular, cyber-secure, and cloud-compatible ATC platforms to improve operational resilience and optimize long-term infrastructure scalability.

Communication systems dominate the Civil Air Traffic Control (ATC) Systems Market with approximately 38% share due to their foundational role in maintaining uninterrupted aircraft-to-ground coordination, cross-border interoperability, and real-time airspace communication reliability. Their structural dominance is reinforced by increasing integration of digital voice communication systems, satellite-based data exchange platforms, and secure networked coordination frameworks across high-density aviation corridors. Navigation systems remain strategically critical for route optimization and precision aircraft positioning, particularly in congested international airspaces. Surveillance systems are emerging as the fastest-growing segment with adoption expansion exceeding 27% as airports increasingly deploy AI-enabled radar analytics, ADS-B technology, and satellite-supported monitoring infrastructure. Compared with conventional communication-centric ATC architectures, surveillance-driven intelligent coordination systems improve aircraft tracking precision by nearly 23% while reducing airspace congestion response time. Automation systems, digital towers, and integrated software platforms collectively account for nearly 34% of market demand, supported by rising airport digitalization initiatives and operational efficiency requirements. Companies are shifting investment toward integrated software-defined ATC infrastructure, predictive analytics platforms, and cloud-enabled coordination systems to strengthen interoperability and scalability. Businesses prioritizing intelligent surveillance integration and automation-centric deployment frameworks are securing stronger competitive positioning in next-generation aviation traffic management ecosystems.

• According to a 2025 report by the International Civil Aviation Organization (ICAO), ADS-B-based surveillance systems were adopted by over 68% of high-traffic international airports, resulting in nearly 21% improvement in aircraft tracking precision and operational visibility, reinforcing their growing strategic importance.

Commercial aviation represents the leading application segment with approximately 61% market concentration due to rising international passenger traffic, airport congestion management requirements, and continuous expansion of global flight networks. Large international airports depend heavily on advanced Civil Air Traffic Control (ATC) Systems to optimize runway utilization, improve flight coordination accuracy, and reduce aircraft holding delays. Demand concentration remains strongest across high-volume aviation hubs managing complex multi-route aircraft movement environments. Military and defense-linked aviation applications are experiencing the fastest operational modernization shift, with digital traffic coordination adoption increasing by nearly 24% due to rising focus on integrated airspace surveillance, cybersecurity resilience, and dual-use aviation infrastructure optimization. Compared with traditional civilian-centric deployment models, defense-integrated ATC systems deliver stronger situational awareness and coordinated traffic monitoring capabilities across restricted and shared airspaces. Regional aviation and private airport operations collectively account for nearly 28% of application demand, supported by remote tower deployment and localized airspace modernization programs. Usage patterns are increasingly shifting toward integrated multi-airspace management systems capable of supporting civilian, cargo, and defense aviation simultaneously. Companies are expanding software-centric deployment capabilities, strengthening AI-based analytics integration, and repositioning operational platforms around scalable smart airport ecosystems to capture evolving application demand.

• According to a 2025 report by Eurocontrol, advanced commercial aviation traffic management systems were deployed across more than 420 airport operations centers, improving flight sequencing efficiency by 19% and reducing congestion-related coordination delays by 16%, highlighting rapid operational adoption.

Airport authorities and air navigation service providers represent the leading end-user group with approximately 57% market concentration due to their direct responsibility for airspace coordination, runway optimization, and aviation safety infrastructure management. Demand concentration remains strongest among large international airports and national aviation agencies managing high-density aircraft movement networks and cross-border traffic coordination systems. Commercial airport operators are emerging as the fastest-expanding end-user segment, with digital ATC infrastructure adoption increasing by nearly 26% as airports prioritize operational automation, passenger traffic scalability, and intelligent airspace management. Compared with government-controlled aviation networks, privately managed airports are accelerating investment cycles and adopting modular deployment frameworks to improve operational flexibility and reduce coordination inefficiencies. Airlines, regional aviation hubs, and defense-linked operators collectively account for nearly 43% of total deployment demand, supported by rising emphasis on integrated flight coordination ecosystems and predictive traffic analytics. Buying behavior is increasingly shifting toward long-term integrated platform contracts rather than standalone hardware procurement. Companies are responding through customized deployment frameworks, cloud-based software integration, and strategic partnerships with aviation authorities to strengthen customer retention and long-term operational scalability. Businesses capable of delivering cyber-secure, interoperable, and upgrade-friendly infrastructure are capturing the strongest competitive advantage across evolving end-user segments.

• According to a 2025 report by the Federal Aviation Administration (FAA), adoption among large commercial airport operators increased by 22%, with over 310 aviation facilities implementing AI-assisted traffic coordination systems, leading to approximately 18% improvement in runway management efficiency and operational throughput.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America maintains demand concentration due to extensive controlled airspace infrastructure, advanced airport modernization programs, and strong deployment of AI-assisted air traffic coordination systems. Europe accounts for nearly 28% of global demand, driven by regulatory-led interoperability programs and sustainability-focused aviation modernization initiatives. Asia-Pacific holds approximately 24% market share and is rapidly accelerating through large-scale airport construction, digital tower deployment, and smart aviation corridor expansion across China, India, and Southeast Asia. Meanwhile, Middle East & Africa contributes 7% through infrastructure-intensive airport transformation projects, while South America represents 5% of market demand supported by regional aviation expansion initiatives. Global supply chain restructuring and aviation resilience priorities are increasingly pushing companies toward regionalized deployment partnerships, localized engineering operations, and long-term infrastructure modernization contracts across high-growth aviation economies.

North America accounts for approximately 36% of the global Civil Air Traffic Control (ATC) Systems Market due to extensive commercial aviation traffic, advanced airport infrastructure, and aggressive NextGen modernization initiatives. The United States dominates regional deployment activity with over 70% of North American controlled airspace operations concentrated across major commercial hubs. AI-assisted traffic sequencing systems improved runway throughput efficiency by nearly 22% in upgraded airports between 2024 and 2026. Rising cybersecurity mandates and pressure to reduce airspace congestion are accelerating migration toward cloud-integrated surveillance and digital communication systems. Aviation authorities are expanding remote tower deployment and predictive traffic analytics adoption to optimize operational coordination. More than 44% of major airport modernization projects now include intelligent automation infrastructure. Airlines and airport operators increasingly prioritize scalable, interoperable platforms capable of improving efficiency while supporting long-term passenger traffic growth, reinforcing North America’s position as a strategic investment hub.

Europe represents approximately 28% of the global Civil Air Traffic Control (ATC) Systems Market, driven by aggressive regulatory modernization programs, sustainability-focused aviation policies, and cross-border airspace interoperability initiatives. Germany, France, and the United Kingdom remain the region’s leading aviation technology deployment centers. More than 41% of large European airports accelerated digital coordination platform integration under SESAR-linked modernization frameworks. Regulatory pressure to reduce flight inefficiencies and emissions is reshaping ATC procurement priorities toward AI-enabled traffic optimization systems and advanced surveillance infrastructure. Automated route coordination platforms reduced unnecessary aircraft holding patterns by nearly 15% across upgraded aviation corridors. Airlines and airport operators increasingly favor compliance-driven digital transformation investments focused on operational efficiency and environmental performance. This regulatory intensity is forcing continuous innovation and positioning Europe as a critical region for next-generation interoperable aviation infrastructure deployment.

Asia-Pacific holds approximately 24% of the global Civil Air Traffic Control (ATC) Systems Market and ranks as the fastest-expanding regional aviation infrastructure ecosystem. China, India, Japan, and Southeast Asian economies are aggressively expanding airport capacity and modernizing airspace coordination systems to support rising passenger and cargo movement volumes. More than 34% of ongoing airport construction projects globally are concentrated within Asia-Pacific. Large-scale infrastructure development and localized technology deployment are accelerating adoption of satellite-based surveillance systems, remote digital towers, and integrated navigation platforms. Regional aviation authorities improved traffic coordination efficiency by nearly 19% through AI-supported airspace management integration. Governments and airport operators increasingly prioritize scalable, cost-efficient deployment models capable of supporting rapid passenger growth and operational expansion. This combination of scale, speed, and infrastructure investment is positioning Asia-Pacific as a strategic center for long-term ATC deployment and aviation technology expansion.

South America contributes approximately 5% of the global Civil Air Traffic Control (ATC) Systems Market, led by Brazil, Colombia, and Chile through regional airport modernization and commercial aviation expansion initiatives. Increasing domestic air traffic volumes and tourism-linked aviation growth are strengthening demand for digital surveillance and communication systems. Regional passenger aviation activity improved by nearly 14% between 2024 and 2026. However, infrastructure funding limitations and uneven airport modernization capabilities remain structural constraints across several economies. Cost-sensitive airport operators are prioritizing phased deployment strategies and modular ATC upgrades to improve scalability while controlling operational expenditure. Adoption of cloud-assisted traffic coordination systems increased by approximately 16% in mid-sized airports. Companies targeting South America are focusing on localized partnerships, operational flexibility, and cost-optimized deployment models, positioning the region as a selective high-growth opportunity with execution-sensitive investment dynamics.

Middle East & Africa accounts for approximately 7% of the global Civil Air Traffic Control (ATC) Systems Market, supported by large-scale airport modernization programs, tourism-driven aviation expansion, and infrastructure-intensive smart city investments. The United Arab Emirates, Saudi Arabia, and South Africa remain key deployment markets due to growing international transit traffic and strategic aviation corridor positioning. Governments and airport operators are accelerating investment in satellite-based surveillance, intelligent communication systems, and centralized traffic coordination platforms. More than 18% of newly announced airport infrastructure projects in the region include integrated digital ATC modernization frameworks. Operational deployment of AI-assisted airspace management systems improved traffic coordination efficiency by nearly 17% across selected aviation hubs. Enterprise buyers increasingly prioritize reliability, scalability, and international interoperability standards, making the region strategically important for infrastructure-driven aviation transformation and long-term technology partnerships.

United States – 34% Market share: Dominates due to extensive controlled airspace infrastructure, NextGen aviation modernization programs, and one of the world’s highest commercial aircraft movement volumes.

China – 16% Market share: Maintains strong leadership through aggressive airport expansion projects, smart aviation corridor deployment, and rapid digital airspace modernization across major transportation hubs.

The Civil Air Traffic Control (ATC) Systems Market is characterized by intense competition between global aviation technology leaders, defense-integrated infrastructure providers, and specialized airspace automation companies. Major players including Thales, Indra, RTX, Leonardo, and Saab collectively account for nearly 48% of total market concentration, competing aggressively across digital tower systems, surveillance infrastructure, AI-assisted traffic analytics, and integrated communication platforms.

Competition is increasingly shifting from conventional hardware supply toward software-driven intelligent airspace ecosystems. Technology performance, interoperability, cybersecurity resilience, and deployment scalability have become primary competitive differentiators. AI-enabled traffic sequencing platforms improve runway coordination efficiency by nearly 24%, while advanced satellite-based surveillance systems reduce aircraft tracking latency by approximately 18%, intensifying pressure on legacy infrastructure providers.

Companies are expanding strategic partnerships with airport authorities, strengthening cloud-based integration capabilities, and accelerating regional deployment networks to secure long-term modernization contracts. Vertical integration across communication, navigation, and surveillance technologies is also reshaping competitive positioning. Rising regulatory complexity, certification requirements, and infrastructure integration costs remain major entry barriers, forcing smaller players toward niche specialization or alliance-based expansion. Winning in this market increasingly depends on scalable automation capability, cyber-secure infrastructure, and long-term operational integration expertise.

Indra Sistemas

RTX Corporation

Leonardo S.p.A.

Saab AB

Frequentis AG

Honeywell International Inc.

BAE Systems plc

L3Harris Technologies Inc.

Northrop Grumman Corporation

Adacel Technologies Limited

SITA

NATS Holdings Limited

Harris Corporation

Artificial intelligence, satellite-based surveillance, and cloud-enabled communication platforms are rapidly reshaping the Civil Air Traffic Control (ATC) Systems Market. AI-assisted traffic sequencing systems improve aircraft movement coordination efficiency by nearly 29% while reducing operational response time by approximately 18%. More than 47% of major international airports have accelerated integration of predictive traffic analytics platforms to optimize runway utilization and reduce congestion-related delays.

Digital tower technology is emerging as a major operational transformation trend, particularly across regional and secondary airports. Compared with conventional physical control towers, remote digital tower systems reduce infrastructure dependency by nearly 25% while improving low-visibility monitoring accuracy by approximately 20%. Airports deploying high-definition visual surveillance and AI-assisted monitoring systems are strengthening operational flexibility and reducing staffing constraints. Aviation technology providers are expanding cloud-based deployment frameworks to improve scalability and cross-airport operational coordination.

Satellite-supported ADS-B surveillance infrastructure is also redefining global airspace monitoring capability. Adoption rates exceeded 63% across high-density international aviation corridors between 2024 and 2026. Integrated communication-navigation-surveillance platforms are delivering measurable improvements in aircraft tracking precision, route optimization, and real-time coordination efficiency. Companies capable of combining cyber-secure analytics, interoperable communication systems, and scalable automation technologies are gaining significant competitive advantage as aviation authorities accelerate intelligent airspace modernization programs.

Between 2026 and 2028, intelligent automation, AI-enabled predictive coordination, and quantum-secure aviation communication systems are expected to become core competitive differentiators, forcing legacy infrastructure providers to rapidly transition toward software-defined, data-centric airspace management ecosystems.

May 2024 – Saab partnered with Belgium’s Skeyes to deploy advanced Remote Tower technology at the new Digital Tower Test Centre supporting Charleroi and Liège airports. The platform integrates A-SMGCS functionality and improves all-weather aircraft tracking efficiency across airports located 100 km apart, accelerating European digital ATC modernization. [Digital Tower Expansion] Source: www.saab.com

November 2024 – Saab, Thales, and ST Engineering signed a strategic MoU to modernize Singapore’s Air Traffic Management infrastructure using integrated Digital Tower Suite and automation technologies. The initiative supports next-generation ATM coordination from en-route operations to gate management, strengthening regional implementation speed and operational scalability. [ATM Innovation Alliance]

October 2025 – Thales launched a major upgrade program for its TopSky-ATC platform with a collaborative governance framework involving European ANSPs including skeyes. The modernization initiative improves operational efficiency for rising traffic volumes while expanding shared innovation capability across advanced ATM ecosystems. [Open Architecture Upgrade]

October 2025 – Thales and Skyguide signed a partnership agreement to accelerate deployment of open-architecture ATM systems through the OpenSky platform. The initiative enables integration of third-party aviation applications and strengthens flexible ATC modernization capabilities, improving interoperability and long-term digital airspace scalability across Europe. [Interoperability Push]

The Civil Air Traffic Control (ATC) Systems Market report provides comprehensive analysis across communication systems, navigation systems, surveillance platforms, automation technologies, digital towers, and integrated airspace management infrastructure. The study evaluates deployment trends across commercial aviation, defense-linked aviation operations, regional airports, and air navigation service providers while covering strategic technology integration patterns influencing global airspace modernization. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, enabling detailed comparison of infrastructure maturity, modernization intensity, and operational adoption patterns.

The report delivers deep analytical coverage across more than 20 market-level indicators including technology adoption rates, deployment concentration, operational efficiency trends, regional demand distribution, and competitive positioning insights. Over 63% of high-density international aviation corridors are currently integrating satellite-supported surveillance infrastructure, while approximately 47% of major airport modernization programs now prioritize AI-assisted traffic optimization systems. The analysis also examines emerging deployment opportunities linked to digital tower infrastructure, cloud-based coordination platforms, and cyber-secure aviation communication networks.

From a strategic perspective, the report supports investment prioritization, infrastructure expansion planning, competitive benchmarking, and long-term technology positioning. It highlights evolving operational requirements, procurement transformation patterns, and intelligent automation trends expected to reshape aviation traffic management frameworks between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 910.0 Million |

| Market Revenue (2033) | USD 1,734.9 Million |

| CAGR (2026–2033) | 8.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Thales Group; Indra Sistemas; RTX Corporation; Leonardo S.p.A.; Saab AB; Frequentis AG; Honeywell International Inc.; BAE Systems plc; L3Harris Technologies Inc.; Northrop Grumman Corporation; Adacel Technologies Limited; SITA; NATS Holdings Limited; Harris Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |