Reports

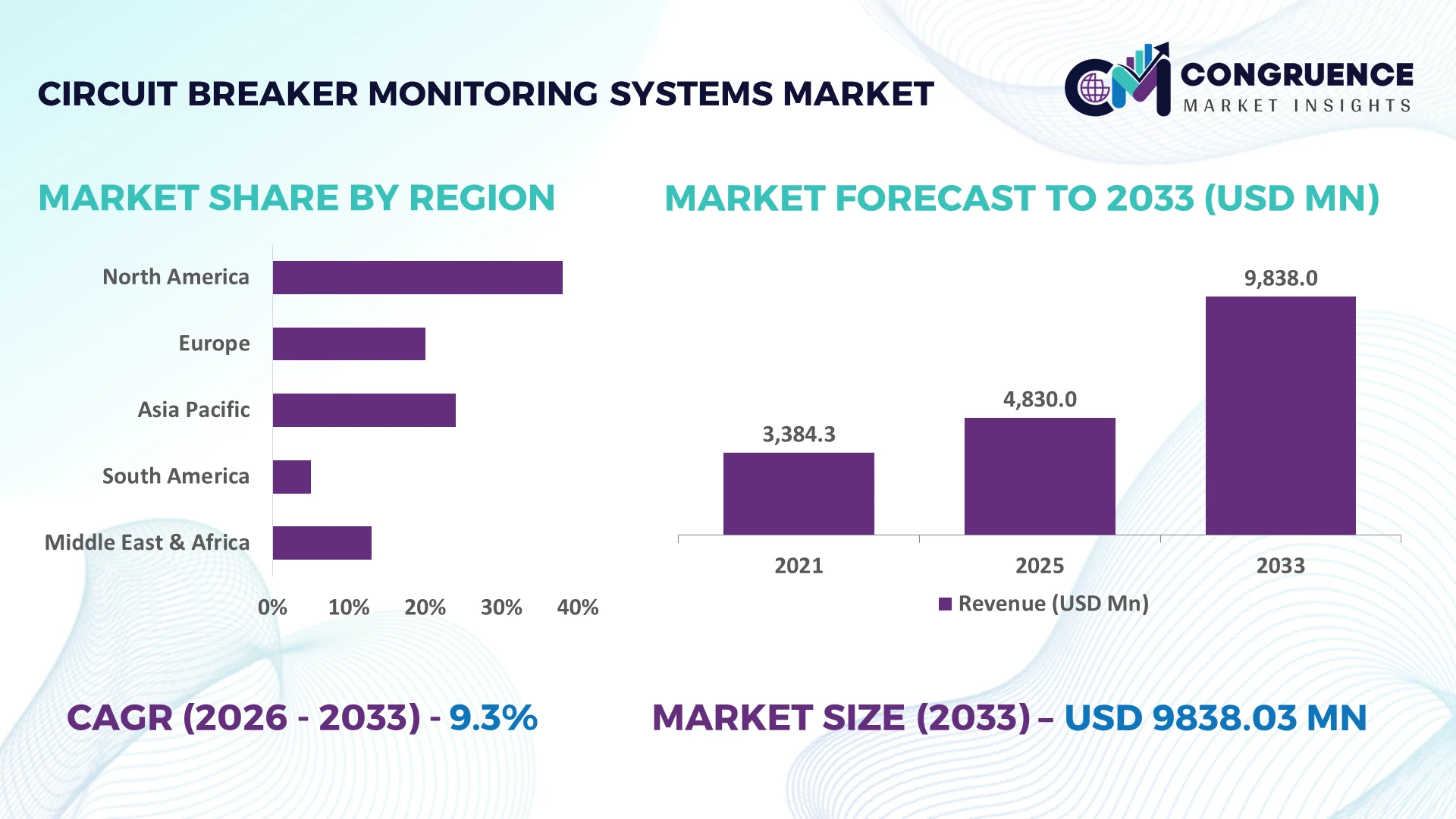

The Global Circuit Breaker Monitoring Systems Market was valued at USD 4830 Million in 2025 and is anticipated to reach a value of USD 9838.03 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033. Grid modernization programs, digital substations, predictive maintenance deployment, and stricter power reliability requirements across utilities, industrial facilities, and renewable energy networks are accelerating the adoption of advanced circuit breaker monitoring systems.

China remains the leading market, accounting for approximately 31% of global high-voltage equipment manufacturing capacity, supported by annual grid investments exceeding USD 80 billion and rapid digital substation deployment. Compared with the United States, China demonstrates faster utility-scale implementation, while the U.S. leads in software-enabled asset monitoring across transmission infrastructure. Ongoing energy security initiatives and post-supply-chain realignment investments in 2026 continue strengthening deployment priorities.

Organizations investing in intelligent monitoring platforms with predictive analytics and scalable integration capabilities are positioned to achieve stronger operational resilience and long-term infrastructure value.

Market Size & Growth: The market is projected to grow from USD 4830 Million in 2025 to USD 9838.03 Million by 2033 at a CAGR of 9.3%, driven by smart grid modernization and predictive maintenance adoption.

Top Growth Drivers: Utility digitalization (42%), renewable energy integration (35%), and predictive maintenance implementation (29%) are the primary market growth drivers.

Short-Term Forecast: By 2028, intelligent monitoring systems are expected to reduce maintenance costs by 24% while improving asset availability by 30%.

Emerging Technologies: AI-powered diagnostics, IoT-enabled sensors, and edge computing platforms improve fault detection accuracy by more than 25% in advanced electrical networks.

Regional Leaders: Asia Pacific is projected to exceed USD 4.2 Billion, North America USD 2.4 Billion, and Europe USD 2.1 Billion, supported by smart grid expansion and transmission upgrades.

Consumer/End-User Trends: More than 58% of large utilities are prioritizing continuous equipment health monitoring to improve operational reliability and asset lifecycle performance.

Pilot/Case Example: A 2026 digital substation modernization project achieved a 32% reduction in maintenance visits while increasing equipment availability by 18%.

Competitive Landscape: The top manufacturers collectively hold approximately 45% of the global market, led by Schneider Electric, Siemens, ABB, Hitachi Energy, and GE Vernova.

Regulatory & ESG Impact: Grid resilience regulations and energy efficiency initiatives improve operational performance by nearly 20%, supporting lower maintenance-related emissions and higher network reliability.

Investment & Funding: More than USD 6 Billion has been committed to grid modernization, with investments focused on strategic partnerships, smart substations, and transmission infrastructure expansion.

Innovation & Future Outlook: Digital twins, cloud-based monitoring platforms, and cybersecurity-integrated asset management solutions are accelerating the next phase of intelligent grid infrastructure.

Circuit Breaker Monitoring Systems Market demand continues expanding across utilities, renewable energy facilities, rail infrastructure, and energy-intensive industries seeking continuous asset visibility. AI-enabled diagnostics, wireless sensing platforms, and cloud-integrated monitoring solutions improve maintenance planning, with predictive maintenance reducing unexpected equipment failures by approximately 30%. Strengthening grid reliability regulations and ongoing transmission network modernization are reinforcing long-term technology adoption, setting the stage for deeper strategic market evaluation.

Circuit Breaker Monitoring Systems have become a strategic asset for utilities, industrial operators, and transmission network owners as grid reliability, asset utilization, and predictive maintenance increasingly determine operational competitiveness. Infrastructure modernization programs, digital substations, and stricter power resilience standards are reshaping procurement priorities, while supply-chain diversification since 2026 has accelerated investment in intelligent monitoring platforms capable of supporting distributed energy assets and critical industrial infrastructure.

Modern AI-enabled monitoring systems identify equipment degradation up to 35% earlier than conventional periodic inspection methods while reducing maintenance interventions by nearly 30%, lowering operational costs and unplanned outages. China continues deploying monitoring technologies at utility scale through extensive transmission expansion, whereas Germany focuses on digital grid automation and renewable integration with higher software interoperability standards. Over the next two to three years, utilities are expected to increase online condition-monitoring coverage beyond 60% of critical transmission assets, supported by growing deployment of edge-connected sensors and cloud analytics.

A 2026 digital substation modernization project demonstrated a 32% reduction in emergency maintenance activities after integrating continuous breaker health diagnostics with centralized asset management. Equipment manufacturers are strengthening software partnerships, expanding digital service portfolios, and investing in predictive analytics capabilities to secure long-term customer relationships. Organizations that combine intelligent monitoring with lifecycle asset optimization will establish stronger competitive positioning as electricity networks become increasingly digital and performance driven.

National grid modernization programs and predictive asset management initiatives are driving widespread deployment of circuit breaker monitoring systems across transmission and distribution infrastructure. More than 58% of large utilities have expanded investments in digital asset monitoring, while predictive maintenance reduces unexpected equipment failures by approximately 30% and extends equipment service life by nearly 20%. India's transmission expansion and China's continued digital substation rollout are increasing demand for real-time equipment diagnostics. In response, leading manufacturers are expanding software capabilities, strengthening utility partnerships, and integrating AI-powered condition monitoring into switchgear portfolios. Companies combining hardware intelligence with digital asset management platforms are improving maintenance efficiency while strengthening long-term service-based business models.

Legacy electrical infrastructure continues to limit seamless deployment of advanced monitoring systems, particularly across aging substations and mixed-vendor environments. Nearly 40% of installed switchgear assets require customized integration, while interoperability challenges increase implementation timelines by approximately 25%. Dependence on specialized electronic components and communication modules also exposes projects to periodic supply-chain disruptions, particularly in highly industrialized markets such as Japan and Germany. To reduce operational risk, manufacturers are localizing component sourcing, developing vendor-neutral communication protocols, and offering modular retrofit solutions. Companies capable of minimizing integration complexity gain stronger deployment scalability and improved project execution across modern and legacy electrical networks.

The rapid expansion of AI-driven diagnostics, digital substations, and cloud-connected asset management platforms is creating new commercial opportunities beyond conventional equipment monitoring. AI-enabled analytics improve fault prediction accuracy by over 25%, while digital maintenance strategies reduce inspection frequency by approximately 30%. Australia and India continue expanding renewable transmission infrastructure, creating demand for intelligent monitoring across geographically distributed electrical assets. Technology providers are increasing investment in digital twin applications, edge computing, and cybersecurity-enabled monitoring ecosystems while forming partnerships with utility software vendors. Organizations delivering integrated analytics rather than standalone hardware are positioned to capture higher-value lifecycle service opportunities and long-term infrastructure contracts.

As circuit breaker monitoring systems become increasingly connected, cybersecurity protection and skilled workforce availability are emerging as critical execution challenges. Approximately 45% of utilities identify operational technology cybersecurity as a primary digital infrastructure concern, while nearly 30% report shortages of engineers experienced in intelligent grid asset management. The growing integration of cloud platforms and remote diagnostics increases system complexity and requires continuous software maintenance. Utilities in the United States are strengthening cybersecurity frameworks alongside digital grid investments, prompting technology suppliers to expand secure communication protocols and specialized training programs. Companies that successfully combine resilient cybersecurity architecture with workforce development will achieve more reliable deployments and stronger long-term operational performance.

AI-Powered Predictive Maintenance: Utilities are accelerating deployment of AI-enabled circuit breaker diagnostics, improving fault detection accuracy by nearly 35% while reducing emergency maintenance by around 30%. The transition toward predictive maintenance is being reinforced by stricter grid reliability requirements and aging transmission assets. Manufacturers are expanding software capabilities, integrating machine learning into monitoring platforms, and strengthening digital service partnerships to improve operational efficiency and reduce maintenance cycles.

Wireless Retrofit Deployments: Wireless monitoring systems are accounting for more than 40% of new retrofit installations because they reduce installation time by approximately 25% and lower implementation costs by nearly 20%. Industrial facilities and utilities are modernizing legacy substations without extensive infrastructure modifications. Companies are responding by developing modular sensor platforms, expanding low-power communication technologies, and accelerating deployment across existing electrical networks.

Digital Substation Integration: More than 55% of newly commissioned digital substations incorporate continuous circuit breaker monitoring through IEC 61850-compatible automation platforms. China and India continue expanding smart transmission infrastructure to strengthen grid reliability and renewable energy integration. Equipment suppliers are integrating monitoring solutions with SCADA systems, protection relays, and centralized asset management software to improve operational visibility and maintenance planning.

Service-Based Monitoring Expansion: Utilities are increasingly adopting long-term monitoring service agreements that improve maintenance efficiency by approximately 28% while extending equipment service life by nearly 20%. Skilled workforce shortages and increasing operational complexity are encouraging remote diagnostics and centralized monitoring centers. Manufacturers are expanding lifecycle service portfolios, investing in cloud-based asset management, and strengthening strategic partnerships to deliver continuous operational support.

Online Monitoring Systems hold the largest market share because they provide continuous equipment diagnostics, real-time fault detection, and seamless integration with utility asset management platforms. Around 52% of transmission operators prioritize permanent online monitoring for critical switchgear, reducing maintenance response time by nearly 30% while improving asset utilization. Wired Monitoring Systems continue serving high-security installations where communication stability remains essential, while Portable Monitoring Systems retain importance for scheduled inspections and temporary field assessments.

IoT-Enabled Monitoring Systems represent the fastest-growing segment as utilities accelerate digital grid transformation and cloud-connected asset management. Adoption of IoT-enabled solutions has increased by approximately 34%, supported by predictive analytics and remote monitoring capabilities. Wireless Monitoring Systems are also gaining traction, reducing retrofit installation complexity by nearly 25%. Manufacturers are expanding AI-enabled product portfolios, strengthening software integration, and developing scalable monitoring architectures to address both greenfield and brownfield electrical infrastructure projects.

Power Transmission accounts for the largest application share because high-voltage infrastructure requires continuous equipment monitoring to maintain network stability and minimize operational disruptions. More than 60% of advanced monitoring deployments are concentrated within transmission assets, where predictive diagnostics reduce unexpected equipment failures by approximately 30%. Power Distribution remains a mature segment as utilities modernize aging distribution networks, while Substations continue expanding through digital automation initiatives.

Renewable Energy Plants are emerging as the fastest-growing application due to increasing grid integration of wind and solar projects requiring intelligent switching infrastructure. Monitoring deployment within renewable facilities has expanded by nearly 33%, improving remote asset visibility and maintenance planning. Industrial Facilities continue investing in advanced monitoring systems to reduce production downtime and strengthen electrical reliability. Equipment manufacturers are expanding integrated monitoring platforms and automation capabilities to support increasingly complex electrical networks.

Utilities remain the dominant end-user segment because extensive transmission and distribution infrastructure requires continuous equipment health monitoring and predictive maintenance. Approximately 58% of large utility operators have expanded digital monitoring programs, improving maintenance planning while reducing equipment downtime by nearly 30%. Industrial Manufacturing remains a major customer group where uninterrupted electrical reliability directly supports production efficiency, while Oil & Gas operators prioritize monitoring solutions for critical power infrastructure operating in demanding environments.

Renewable Energy represents the fastest-growing end-user segment as expanding renewable generation requires intelligent monitoring across substations and grid interconnection assets. Adoption has increased by approximately 36% as operators seek improved remote diagnostics and asset visibility. Railways are also increasing deployment to strengthen traction power reliability and reduce service interruptions. Technology providers are responding through industry-specific software platforms, strategic utility partnerships, customized monitoring solutions, and lifecycle service agreements that enhance long-term customer retention.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

Grid Digitalization and Asset Modernization Drive Deployment

North America represents one of the most advanced markets for circuit breaker monitoring systems, supported by large-scale transmission modernization, utility digitalization, and predictive maintenance adoption. The region accounted for approximately 26.5% of global market activity in 2025, with utilities increasingly integrating real-time equipment diagnostics into transmission and distribution networks. More than 60% of major utilities have incorporated condition-based monitoring into critical asset management strategies to improve grid reliability and reduce outage risks. Rising renewable integration and replacement of aging electrical infrastructure continue driving deployment. Equipment suppliers are expanding cloud-connected monitoring platforms, strengthening software integration, and developing lifecycle service offerings to improve maintenance efficiency and operational performance.

United States Market Outlook: The United States leads the regional market through extensive transmission infrastructure, advanced utility automation, and continuous investment in intelligent grid technologies. More than 65% of leading transmission operators have expanded deployment of digital asset management platforms supporting predictive maintenance. Utility modernization initiatives and growing adoption of AI-enabled diagnostics continue strengthening long-term demand for advanced circuit breaker monitoring solutions across substations and transmission networks.

Grid Modernization and Energy Transition Accelerate Adoption

Europe continues strengthening deployment of circuit breaker monitoring systems through transmission modernization, renewable energy integration, and digital grid management initiatives. The region contributed nearly 23.4% of global market activity in 2025, supported by replacement of aging electrical assets and expansion of intelligent substations. More than 55% of newly upgraded high-voltage installations include continuous equipment monitoring to improve operational reliability and maintenance planning. Utilities are integrating monitoring platforms with centralized asset management systems, while manufacturers continue expanding cybersecurity features and IEC-compliant digital technologies to support increasingly automated power networks.

Germany Market Outlook: Germany remains the largest regional market due to its advanced industrial ecosystem, renewable energy transition, and extensive transmission modernization programs. Approximately 40% of newly upgraded transmission assets incorporate digital condition-monitoring technologies to improve equipment utilization and reduce maintenance requirements. Domestic manufacturers continue investing in intelligent monitoring software and advanced switchgear technologies to strengthen long-term grid resilience.

Large-Scale Infrastructure Expansion Sustains Leadership

Asia-Pacific remains the largest regional market, accounting for approximately 41.8% of global demand due to rapid industrialization, smart grid expansion, and continuous investment in transmission infrastructure. China, India, Japan, and South Korea continue deploying digital substations and intelligent monitoring technologies across large-scale electrical networks. More than 50% of newly commissioned high-voltage substations integrate continuous equipment monitoring to improve operational reliability and maintenance planning. Manufacturers are expanding production capacity, localized engineering support, and software development capabilities to meet rising infrastructure requirements while improving deployment efficiency.

China Market Outlook: China dominates the regional market through its extensive electrical equipment manufacturing base and aggressive smart grid investment strategy. The country accounts for approximately 31% of global high-voltage equipment manufacturing capacity while continuing rapid deployment of intelligent substations. Domestic companies are expanding AI-enabled monitoring technologies and integrated switchgear solutions to support nationwide transmission modernization and long-term grid reliability.

Transmission Modernization Creates New Deployment Opportunities

South America continues expanding adoption of circuit breaker monitoring systems as utilities modernize transmission infrastructure and strengthen network reliability. The region accounted for approximately 4.9% of global market activity in 2025, supported by investment in grid automation and renewable energy integration. Utilities are increasingly deploying intelligent monitoring technologies across aging substations to reduce maintenance requirements and improve asset visibility. Infrastructure constraints remain in selected markets, but growing investment in digital utility operations continues supporting long-term deployment. Equipment manufacturers are expanding regional partnerships and technical service capabilities to improve implementation efficiency.

Brazil Market Outlook: Brazil represents the largest market within South America because of its extensive transmission network and ongoing infrastructure modernization programs. More than 45% of major transmission upgrade projects include advanced monitoring technologies supporting predictive maintenance and operational reliability. Utilities continue strengthening digital asset management capabilities while technology suppliers expand local engineering support and long-term maintenance partnerships.

Infrastructure Investment Supports Digital Grid Transformation

Middle East & Africa is emerging as the fastest-growing regional market due to expanding electricity infrastructure, industrial diversification, and smart utility investments. The region represented approximately 3.4% of global market demand in 2025, with increasing deployment across transmission projects, industrial facilities, and renewable energy developments. National infrastructure programs continue accelerating digital substation implementation, while utilities replace aging equipment with intelligent monitoring systems to improve operational reliability and maintenance efficiency. Technology providers are strengthening regional engineering capabilities and strategic collaborations to support long-term infrastructure modernization.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through substantial investment in transmission infrastructure, industrial expansion, and smart grid development. More than 35% of newly commissioned transmission projects incorporate advanced circuit breaker monitoring technologies to improve equipment reliability and predictive maintenance. Utilities and technology providers continue expanding strategic partnerships and digital infrastructure initiatives to support long-term power network modernization.

Global technology leaders including Schneider Electric, Siemens, ABB, Hitachi Energy, and GE Vernova compete directly on digital monitoring capabilities, while regional automation providers and specialized condition-monitoring companies challenge them through cost-efficient customization and faster deployment. The top five players collectively account for approximately 47% of the market, creating a moderately consolidated competitive environment. Competition increasingly revolves around AI-enabled diagnostics, software interoperability, cybersecurity, and lifecycle service capabilities rather than hardware alone. Digital monitoring platforms reduce maintenance costs by nearly 30%, while cloud-based asset management improves fault response time by approximately 25%, giving technology-focused suppliers a measurable advantage. Global OEMs continue expanding software partnerships, strengthening regional engineering centers, and integrating monitoring platforms with protection and SCADA systems, whereas regional suppliers compete through localized support and retrofit expertise. The competitive landscape is shifting toward software-centric differentiation and integrated digital ecosystems. High certification requirements, utility qualification processes, and cybersecurity compliance create significant entry barriers. Sustainable competitive success depends on combining intelligent analytics, seamless integration, strong service networks, and long-term customer partnerships.

Schneider Electric

Siemens

ABB

Hitachi Energy

GE Vernova

Mitsubishi Electric Corporation

Eaton Corporation

Toshiba Energy Systems & Solutions Corporation

Hyundai Electric & Energy Systems

NR Electric Co., Ltd.

Schweitzer Engineering Laboratories (SEL)

Qualitrol Corporation

Megger Group Limited

OMICRON electronics GmbH

Artificial intelligence, Industrial IoT, and edge computing are redefining circuit breaker monitoring by enabling continuous equipment diagnostics instead of periodic inspections. AI-driven analytics improve fault prediction accuracy by approximately 35%, while IoT-enabled sensing reduces unexpected equipment failures by nearly 30%. More than 55% of newly commissioned digital substations now integrate intelligent monitoring platforms, reflecting a clear shift toward data-driven asset management. Utilities and industrial operators increasingly prioritize interoperable solutions capable of supporting centralized monitoring across geographically distributed electrical networks.

Traditional time-based maintenance is rapidly being replaced by condition-based monitoring supported by cloud analytics and digital twins. Compared with conventional inspection methods, modern intelligent monitoring reduces maintenance interventions by approximately 28% while improving equipment availability by nearly 20%. Global OEMs with integrated software ecosystems gain a competitive advantage through predictive diagnostics, whereas specialized technology providers differentiate through retrofit-ready wireless monitoring solutions and advanced cybersecurity capabilities.

Between 2026 and 2028, digital twins, edge AI, and cybersecurity-integrated monitoring platforms will become standard across critical transmission infrastructure. Companies investing in scalable analytics, secure communications, and software-enabled lifecycle services will strengthen operational resilience, accelerate maintenance decisions, and secure long-term competitive positioning as intelligent grid infrastructure continues expanding worldwide.

May 2026 Hitachi Energy introduced the world's first 800 kV SF₆-free dead tank circuit breaker under its EconiQ portfolio, extending the roadmap with new voltage classes up to 800 kV for sustainable transmission networks. The launch strengthens next-generation digital monitoring and eco-efficient grid modernization strategies. Source: Hitachi

June 2026 Schneider Electric partnered with Kraken to accelerate grid flexibility through advanced digital grid monitoring and demand management solutions, enabling utilities to unlock existing network capacity and speed up large industrial and data center grid connections without major infrastructure expansion.

October 2025 Hitachi Energy presented advanced AI-driven condition monitoring and predictive diagnostics for high-voltage circuit breakers during an IEEE technical webinar, highlighting digital twin integration capable of improving maintenance planning and extending equipment lifecycle through continuous asset intelligence. Source: IEEE DEIS

April 2026 Schneider Electric showcased more than 400 energy technologies and launched over 30 new electrification and automation solutions during its Innovation Summit India, reinforcing digital grid modernization strategies and expanding intelligent infrastructure deployment across utility and industrial sectors. Source: Schneider Electric India

The report provides comprehensive analysis of the Circuit Breaker Monitoring Systems market across Online Monitoring Systems, Portable Monitoring Systems, Wired Monitoring Systems, Wireless Monitoring Systems, and IoT-Enabled Monitoring Systems. It evaluates deployment across Power Transmission, Power Distribution, Industrial Facilities, Renewable Energy Plants, and Substations while assessing demand from Utilities, Industrial Manufacturing, Oil & Gas, Renewable Energy, and Railways. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting operational trends, technology adoption, deployment patterns, and competitive developments.

The study examines digital substations, AI-enabled diagnostics, Industrial IoT integration, edge computing, wireless monitoring, and predictive maintenance technologies shaping the market between 2026 and 2033. It assesses strategic positioning of major industry participants, analyzes evolving deployment priorities, identifies emerging application areas, and evaluates investment opportunities across established and developing markets. The report supports expansion planning, competitive benchmarking, product development, partnership evaluation, and long-term business decision-making through detailed segmentation, regional intelligence, technology assessment, and operational market insights.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4830 Million |

Market Revenue in 2033 | USD 9838.03 Million |

CAGR (2026 - 2033) | 9.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Schneider Electric, Siemens, ABB, Hitachi Energy, GE Vernova, Mitsubishi Electric Corporation, Eaton Corporation, Toshiba Energy Systems & Solutions Corporation, Hyundai Electric & Energy Systems, NR Electric Co., Ltd., Schweitzer Engineering Laboratories (SEL), Qualitrol Corporation, Megger Group Limited, OMICRON electronics GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |