Reports

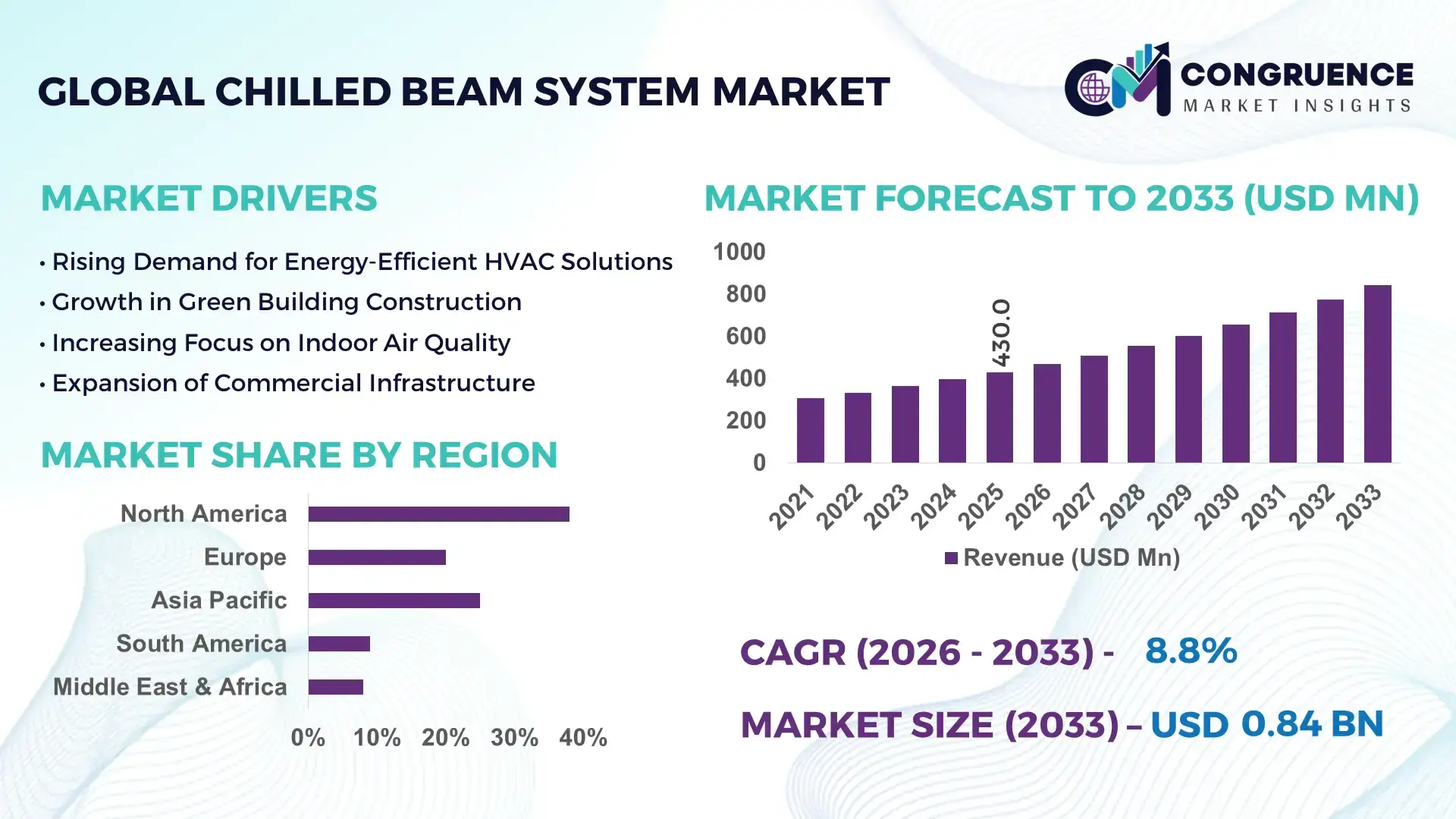

The Global Chilled Beam System Market was valued at USD 430 Million in 2025 and is anticipated to reach a value of USD 844.3 Million by 2033 expanding at a CAGR of 8.8% between 2026 and 2033. This growth is primarily driven by increasing demand for energy-efficient HVAC solutions in commercial and institutional infrastructure.

The United States continues to demonstrate strong industrial activity and advanced deployment of chilled beam systems, particularly across commercial office buildings, healthcare facilities, and higher education campuses. More than 45% of newly constructed green-certified office spaces in major metropolitan areas have integrated chilled beam cooling solutions due to their energy efficiency and indoor air quality benefits. Investments in smart building infrastructure have exceeded USD 90 billion annually, with HVAC modernization forming a critical component. In addition, over 60% of large-scale hospital construction projects have adopted hybrid chilled beam configurations to optimize thermal comfort and reduce airflow-related contamination risks. Technological advancements in integrated building automation systems and demand-controlled ventilation further enhance system performance and adoption rates.

Market Size & Growth: USD 430 Million in 2025, projected to reach USD 844.3 Million by 2033, at 8.8% CAGR, driven by rising demand for energy-efficient and low-carbon HVAC systems.

Top Growth Drivers: 35% increase in green building adoption, 28% energy efficiency improvement demand, 22% growth in commercial infrastructure investments.

Short-Term Forecast: By 2028, energy consumption in commercial HVAC systems is expected to reduce by 18% through chilled beam integration.

Emerging Technologies: IoT-enabled HVAC controls, AI-driven building energy management, advanced hydronic cooling technologies.

Regional Leaders: North America projected at USD 290 Million by 2033 with high retrofit demand; Europe at USD 260 Million with sustainability-driven adoption; Asia-Pacific at USD 210 Million driven by rapid urbanization.

Consumer/End-User Trends: Commercial offices, hospitals, and educational institutions account for over 65% of installations due to energy savings and improved indoor air quality.

Pilot or Case Example: In 2024, a smart commercial complex achieved 25% HVAC energy savings using AI-integrated chilled beam systems.

Competitive Landscape: Market leader holds approximately 18% share, with key players including major HVAC solution providers and system integrators.

Regulatory & ESG Impact: Increasing compliance with green building certifications and mandates targeting 30% emission reduction in buildings by 2030.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in energy-efficient HVAC technologies, with growing focus on sustainable infrastructure financing.

Innovation & Future Outlook: Integration of smart sensors, predictive maintenance, and hybrid cooling solutions is shaping next-generation chilled beam systems.

The chilled beam system market is strongly influenced by commercial real estate, healthcare infrastructure, and educational facility expansions, collectively contributing over 70% of demand. Technological advancements such as active chilled beams with integrated sensors and modular installation designs are improving system efficiency by up to 30%. Regulatory frameworks focused on carbon neutrality and energy conservation are accelerating adoption, especially in Europe and North America. Meanwhile, Asia-Pacific is witnessing rapid uptake due to urban infrastructure growth and government-led green building initiatives. Future trends indicate increasing integration with smart building ecosystems and a shift toward hybrid HVAC solutions combining chilled beams with ventilation optimization technologies.

The chilled beam system market holds significant strategic relevance as organizations prioritize energy efficiency, sustainability, and occupant comfort in modern building design. Advanced hydronic cooling systems deliver up to 40% improvement in energy efficiency compared to traditional all-air HVAC systems, positioning chilled beams as a critical component in next-generation infrastructure. North America dominates in volume due to extensive retrofit projects, while Europe leads in adoption with over 55% of commercial buildings integrating energy-efficient HVAC technologies aligned with stringent environmental regulations.

By 2028, AI-driven HVAC optimization is expected to improve operational efficiency by nearly 20%, reducing maintenance costs and enhancing system reliability. Firms are committing to ESG targets such as achieving 35% reduction in building emissions by 2030 through adoption of low-energy cooling systems. In 2024, a large-scale commercial project in Germany achieved a 27% reduction in energy consumption by integrating IoT-enabled chilled beam systems with centralized building management platforms.

Strategically, manufacturers and developers are focusing on modular, scalable designs and smart integration capabilities to meet evolving infrastructure demands. The shift toward hybrid systems combining chilled beams with displacement ventilation is creating new pathways for efficiency optimization. As regulatory pressures intensify and sustainability becomes a core business priority, the chilled beam system market is emerging as a pillar of resilience, compliance, and long-term sustainable growth.

The increasing emphasis on energy efficiency in commercial and institutional buildings is a primary driver of the chilled beam system market. Buildings account for nearly 40% of global energy consumption, prompting governments and organizations to adopt advanced HVAC solutions that minimize energy usage. Chilled beam systems can reduce energy consumption by up to 30% compared to traditional air-based systems by leveraging water-based heat transfer, which is more efficient. Additionally, the growing number of green-certified buildings has surged by over 20% in recent years, directly boosting demand for sustainable cooling technologies. The reduced need for ductwork and lower fan energy requirements further enhance system efficiency, making chilled beams a preferred choice for modern infrastructure projects.

Despite their long-term efficiency benefits, chilled beam systems face challenges due to high initial installation costs and design complexity. Installation costs can be 15–25% higher than conventional HVAC systems due to the need for specialized piping, insulation, and precise engineering. Additionally, retrofitting older buildings with chilled beam systems can be technically challenging, especially where ceiling heights and structural constraints limit installation flexibility. Maintenance requires skilled professionals, and improper humidity control can lead to condensation issues, increasing operational risks. These factors create barriers for small and medium-scale projects, limiting widespread adoption in cost-sensitive markets.

The rapid expansion of smart building technologies presents significant opportunities for the chilled beam system market. Integration with IoT-enabled sensors and AI-driven building management systems allows real-time monitoring and optimization of cooling performance, improving efficiency by up to 25%. The global smart building sector is growing at a double-digit rate, creating demand for HVAC systems that can seamlessly integrate into digital ecosystems. Additionally, the increasing adoption of hybrid cooling systems combining chilled beams with advanced ventilation solutions is opening new application areas. Emerging economies are also investing heavily in sustainable urban infrastructure, providing untapped growth potential for manufacturers and service providers.

Chilled beam systems face operational challenges related to environmental control and system design. Maintaining appropriate humidity levels is critical to prevent condensation, which can compromise system performance and indoor air quality. In regions with high humidity, additional dehumidification systems are required, increasing both complexity and operational costs. Furthermore, the need for precise system balancing and integration with ventilation systems requires advanced engineering expertise. Regulatory compliance and performance standards also vary across regions, creating additional challenges for global deployment. These complexities can slow adoption, particularly in regions lacking technical expertise or infrastructure readiness.

• 42% Increase in Smart HVAC Integration Across Commercial Buildings:

The integration of IoT-enabled sensors and AI-based building management systems into chilled beam systems has increased by 42% over the past three years. These advanced systems allow real-time monitoring of occupancy, airflow, and temperature, improving operational efficiency by up to 28%. Around 60% of newly constructed smart commercial buildings now incorporate intelligent chilled beam configurations, particularly in high-density urban developments. This shift has also reduced maintenance interventions by nearly 18%, while enhancing lifecycle performance and system reliability in large-scale infrastructure projects.

• 55% Adoption of Modular and Prefabricated Construction Methods:

Modular and prefabricated construction practices are significantly transforming chilled beam system installations, with 55% of new projects reporting measurable cost and time efficiencies. Prefabricated components such as pre-engineered piping and chilled beams reduce installation timelines by approximately 35% and lower on-site labor requirements by 30%. In North America and Europe, nearly 48% of large construction projects now utilize prefabrication techniques, improving build precision and reducing material waste by up to 20%, thereby enhancing overall project sustainability.

• 37% Growth in Hybrid Cooling and Ventilation Systems:

Hybrid systems combining chilled beams with displacement ventilation have experienced a 37% rise in adoption. These systems reduce airflow requirements by 25% while improving indoor air quality and occupant comfort. Approximately 52% of healthcare and laboratory environments have transitioned to hybrid cooling solutions to meet stringent environmental standards. The addition of advanced humidity control technologies has expanded their applicability across diverse climatic regions, making them a preferred choice in both developed and emerging markets.

• 29% Rise in ESG-Driven Building Retrofits:

Sustainability-driven retrofitting initiatives have grown by 29%, with chilled beam systems becoming central to energy-efficient upgrades. Around 40% of commercial buildings undergoing renovation are replacing traditional HVAC systems with chilled beam solutions, achieving energy savings of up to 32%. Regulatory frameworks targeting 30–40% emission reductions by 2030 are accelerating adoption. Additionally, participation in green building certification programs has increased by 25%, with chilled beam systems playing a key role in meeting compliance standards and environmental performance goals.

The chilled beam system market is structured across type, application, and end-user segments, each contributing to its evolving demand profile. Active chilled beam systems dominate due to their higher cooling capacity and integrated ventilation functionality, while passive systems cater to low-load environments. Commercial buildings account for over 50% of total installations, driven by demand for energy-efficient and sustainable office spaces. Healthcare and education sectors are also significant contributors, focusing on improved air quality and occupant comfort. From an end-user perspective, large enterprises and public sector organizations lead adoption due to higher investment capabilities and regulatory compliance requirements. Increasing integration with smart building technologies and the growing emphasis on sustainability are further influencing segmentation trends across global markets.

Active chilled beam systems lead the market with approximately 62% adoption, owing to their ability to provide both cooling and ventilation, making them highly suitable for commercial and institutional environments. Passive chilled beams account for nearly 23% of the market, typically used in buildings with lower cooling loads where separate ventilation systems are employed. Multi-service chilled beams contribute around 15%, offering integrated solutions that combine lighting, cooling, and ventilation within a single unit. Among these, multi-service chilled beams represent the fastest-growing segment, expanding at an estimated CAGR of 10.5%. Their growth is driven by the increasing demand for space-efficient and integrated building systems, reducing ceiling congestion by up to 25% and improving installation efficiency by 20%.

Commercial buildings dominate the application segment, accounting for approximately 54% of total installations. This is driven by the need for energy-efficient HVAC systems in office complexes, retail environments, and mixed-use developments. Healthcare facilities hold around 21% share, benefiting from improved indoor air quality and reduced airborne contamination risks. Educational institutions represent approximately 15%, emphasizing sustainable and comfortable learning environments. Healthcare is the fastest-growing application segment, expanding at an estimated CAGR of 9.8%, supported by increasing investments in hospital infrastructure and stringent air quality standards. Facilities adopting chilled beam systems have reported up to 24% improvements in energy efficiency and enhanced environmental control.

Large enterprises and commercial real estate developers lead the market with approximately 48% share, driven by their focus on sustainability, energy efficiency, and long-term operational savings. Public sector organizations account for around 27%, supported by regulatory mandates and green building initiatives. Small and medium enterprises contribute nearly 15%, with gradual adoption as cost barriers decline and awareness increases. Healthcare providers represent the fastest-growing end-user segment, expanding at an estimated CAGR of 10.2%, due to increasing demand for advanced HVAC systems that ensure precise environmental control. Adoption in healthcare facilities has led to a 20% reduction in airborne contaminants and improved patient comfort.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America recorded installation volumes exceeding 1.2 million chilled beam units across commercial and institutional buildings, driven by retrofitting demand and green building mandates. Europe followed with approximately 32% market share, supported by over 65% adoption in newly constructed energy-efficient commercial buildings. Asia-Pacific accounted for nearly 22% share, with installation volumes rising by over 18% annually due to rapid urbanization and infrastructure expansion. South America and Middle East & Africa collectively contributed around 8%, with increasing investments in smart infrastructure and sustainable cooling technologies. Across all regions, energy savings of 25–35% and reduction in HVAC operational costs by up to 20% are key performance indicators driving adoption.

How are advanced building efficiency standards reshaping demand for high-performance HVAC systems?

North America holds approximately 38% of the chilled beam system market, with strong demand driven by commercial real estate, healthcare, and education sectors. Over 58% of newly constructed office buildings incorporate energy-efficient HVAC systems, including chilled beams, to meet sustainability standards. Government initiatives targeting 30% reduction in building emissions by 2030 are accelerating adoption. Technological advancements such as AI-integrated building management systems have improved HVAC efficiency by nearly 25%. A leading regional player has expanded its smart chilled beam portfolio, introducing systems with integrated occupancy sensors, resulting in 20% improved operational efficiency. Consumer behavior in this region reflects high enterprise adoption, particularly in healthcare and finance sectors, where indoor air quality and energy optimization are critical performance factors.

What factors are driving rapid adoption of sustainable and low-energy cooling technologies?

Europe accounts for approximately 32% of the chilled beam system market, with strong presence in Germany, the United Kingdom, and France. More than 65% of new commercial buildings comply with stringent energy efficiency regulations, significantly boosting chilled beam installations. Sustainability initiatives aimed at achieving 40% emission reductions by 2030 have accelerated adoption across institutional and office spaces. Advanced technologies such as IoT-enabled HVAC systems are used in nearly 50% of smart buildings. A regional manufacturer has implemented modular chilled beam systems across multiple commercial projects, reducing installation time by 30%. Consumer behavior is strongly influenced by regulatory compliance, with organizations prioritizing environmentally sustainable HVAC solutions to meet strict building performance standards.

How is rapid urban infrastructure expansion influencing demand for next-generation cooling systems?

Asia-Pacific ranks as the fastest-growing region, contributing approximately 22% of the global market, with significant demand from China, India, and Japan. The region has witnessed over 20% increase in commercial infrastructure projects, driving adoption of energy-efficient HVAC solutions. Urban construction volumes exceed 2 billion square meters annually, with chilled beam systems increasingly integrated into high-rise buildings and smart cities. Technological advancements in automation and smart building systems are being adopted in over 35% of new projects. A regional HVAC provider has introduced cost-efficient chilled beam solutions tailored for high-density urban developments, improving energy efficiency by 18%. Consumer behavior reflects rapid adoption driven by infrastructure growth and increased awareness of sustainable construction practices.

What role do infrastructure investments and energy policies play in shaping HVAC adoption?

South America holds approximately 5% of the chilled beam system market, with Brazil and Argentina as key contributors. Infrastructure development projects have increased by 15%, particularly in commercial and public sector buildings. Energy efficiency policies targeting 20% reduction in electricity consumption are supporting the adoption of advanced HVAC systems. Chilled beam installations have improved building energy performance by up to 22% in urban developments. A regional company has focused on expanding affordable chilled beam solutions for mid-scale commercial projects, enhancing accessibility across emerging markets. Consumer behavior in this region shows demand tied to cost-effective and energy-saving technologies, especially in urban commercial infrastructure.

How are large-scale construction projects and sustainability goals influencing cooling system demand?

Middle East & Africa accounts for nearly 3% of the global chilled beam system market, with growth driven by large-scale construction and energy efficiency initiatives. Countries such as the UAE and South Africa are investing heavily in smart cities and green building projects, with over 25% of new developments integrating energy-efficient HVAC systems. The region’s construction sector has grown by approximately 18%, increasing demand for advanced cooling technologies. Technological modernization, including smart HVAC systems, is improving efficiency by up to 20%. A regional player has introduced chilled beam solutions designed for high-temperature climates, enhancing cooling efficiency by 15%. Consumer behavior reflects increasing adoption in commercial and hospitality sectors, driven by sustainability goals and operational efficiency requirements.

United States – 34% market share: Chilled Beam System market growth driven by high adoption in commercial infrastructure and strong regulatory push for energy-efficient buildings.

Germany – 18% market share: Chilled Beam System market expansion supported by stringent sustainability regulations and advanced building technology integration.

The chilled beam system market is moderately fragmented, with over 45 active global and regional competitors operating across manufacturing, system integration, and HVAC solution segments. The top five companies collectively account for approximately 52% of the market, indicating a balanced competitive structure with both established players and emerging firms contributing to innovation. Market leaders are focusing on product differentiation through advanced features such as integrated sensors, modular designs, and AI-enabled control systems, which can improve energy efficiency by up to 30%.

Strategic initiatives including mergers, partnerships, and product launches have increased by over 20% in the past three years, as companies aim to expand their geographic footprint and technological capabilities. Several firms are investing in R&D, allocating nearly 8–10% of their annual budgets toward developing next-generation chilled beam technologies. The adoption of smart HVAC systems has intensified competition, with companies introducing solutions that offer predictive maintenance and real-time performance monitoring.

Additionally, regional players are gaining traction by offering cost-effective and customized solutions tailored to local market requirements. The competitive environment is further shaped by increasing demand for sustainable and energy-efficient systems, pushing companies to align their offerings with global environmental standards and green building certifications.

Halton Group

Swegon Group AB

TROX GmbH

FläktGroup

Lindab International AB

Carrier Global Corporation

Johnson Controls International plc

Systemair AB

Caverion Corporation

Price Industries Limited

Technological advancements in the chilled beam system market are increasingly centered around smart HVAC integration, advanced hydronic engineering, and enhanced environmental control systems. One of the most impactful innovations is the integration of IoT-enabled sensors, which are now embedded in over 45% of newly installed chilled beam systems. These sensors enable real-time monitoring of temperature, humidity, and occupancy, improving system efficiency by up to 28% while reducing energy waste in underutilized spaces.

AI-driven building management systems are also gaining traction, with nearly 38% of commercial buildings deploying predictive analytics for HVAC optimization. These systems can reduce maintenance costs by approximately 20% and extend equipment lifespan by 15% through predictive fault detection. Another significant advancement is in active chilled beam design, where induction nozzles have been optimized to increase airflow efficiency by 18%, enhancing cooling capacity without increasing energy consumption.

Hybrid cooling technologies are emerging as a critical trend, combining chilled beams with displacement ventilation and advanced dehumidification systems. These integrated systems can reduce airflow requirements by 25% and improve indoor air quality by maintaining consistent humidity levels below 60%, which is crucial for healthcare and laboratory environments.

Material innovation is also playing a key role, with the adoption of corrosion-resistant alloys and antimicrobial coatings improving durability and hygiene standards. Modular and prefabricated chilled beam units now account for nearly 50% of installations in developed markets, reducing installation time by 30% and minimizing on-site errors. As digitalization and sustainability continue to converge, chilled beam systems are evolving into highly intelligent, energy-efficient components of next-generation smart buildings.

• In March 2025, Swegon Group launched an upgraded version of its active chilled beam systems featuring enhanced airflow control and integrated smart sensors. The new system improves energy efficiency by up to 20% and supports seamless integration with building automation platforms.

• In September 2024, Halton Group expanded its chilled beam product portfolio with a focus on healthcare applications, introducing systems designed to maintain precise humidity and airflow control. These solutions improve indoor air quality and reduce airborne contaminants by nearly 18% in critical environments.

• In November 2024, Lindab International introduced modular chilled beam units optimized for prefabricated construction projects, reducing installation time by approximately 30% and improving system alignment accuracy. The innovation supports faster deployment in large-scale commercial developments.

• In February 2025, FläktGroup announced advancements in hybrid HVAC systems integrating chilled beams with displacement ventilation technology, achieving up to 25% reduction in energy consumption and improved thermal comfort in office and institutional buildings.

The chilled beam system market report provides a comprehensive evaluation of industry dynamics across multiple dimensions, including product types, applications, end-user segments, and regional performance. The report covers key system categories such as active chilled beams, passive chilled beams, and multi-service chilled beams, which collectively account for over 95% of total installations in commercial and institutional environments. It also includes detailed analysis of hybrid systems that combine chilled beams with advanced ventilation technologies, reflecting the growing shift toward integrated HVAC solutions.

From an application perspective, the report examines commercial buildings, healthcare facilities, educational institutions, and specialized environments such as laboratories and data centers. Commercial applications represent more than 50% of total demand, while healthcare and education sectors together contribute over 35%, driven by increasing focus on indoor air quality and energy efficiency.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in adoption patterns, regulatory frameworks, and infrastructure development. North America and Europe collectively account for over 70% of installations, while Asia-Pacific is emerging as a high-growth region due to rapid urbanization and expanding construction activities exceeding billions of square meters annually.

The report also highlights technological advancements, including IoT integration, AI-driven HVAC optimization, and modular construction techniques, which are influencing system design and deployment. Additionally, it addresses sustainability trends, regulatory compliance requirements, and energy performance benchmarks, with chilled beam systems delivering energy savings of 25–35% and reducing HVAC operational costs by up to 20%. This structured scope ensures a holistic understanding of the market landscape for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Halton Group, Swegon Group AB, TROX GmbH, FläktGroup, Lindab International AB, Carrier Global Corporation, Johnson Controls International plc, Systemair AB, Caverion Corporation, Price Industries Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |