Reports

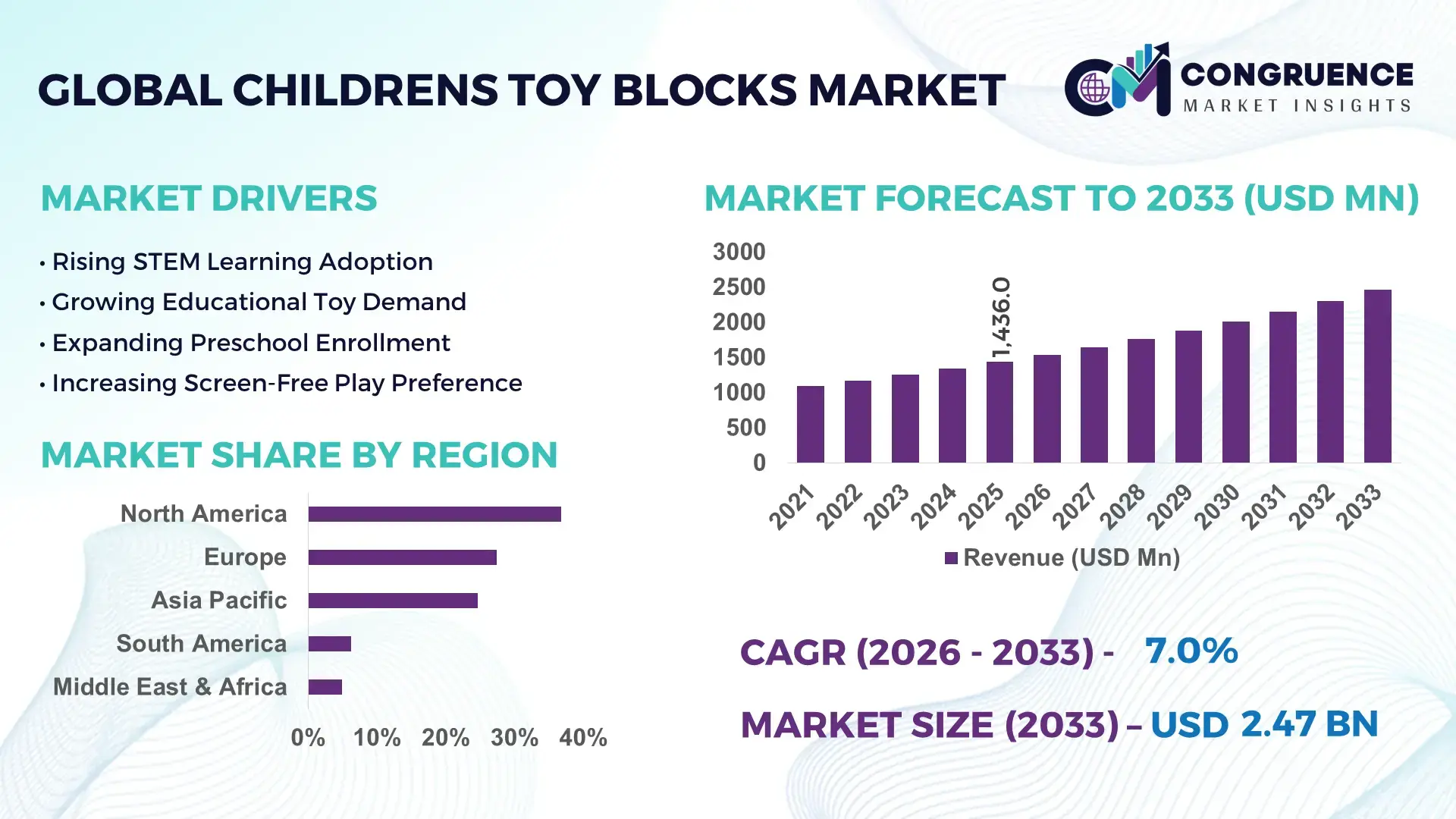

The Global Childrens Toy Blocks Market was valued at USD 1,436.0 Million in 2025 and is anticipated to reach a value of USD 2,467.3 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033. Rising integration of STEM-focused learning toys, licensed entertainment franchises, and eco-friendly construction sets is accelerating premium toy block adoption across developed and emerging consumer markets.

The United States remains the dominant country, accounting for approximately 28% of global toy block consumption, supported by annual toy industry spending exceeding USD 40 billion and strong STEM-learning adoption across schools and households. Compared with Germany, where educational construction toys represent nearly 18% of the learning toy segment, U.S. penetration is substantially higher due to larger retail networks and licensing ecosystems. Continued investment in sustainable materials and digital-connected play experiences further strengthens market leadership. The ongoing diversification of global manufacturing beyond China is also reshaping sourcing strategies and product availability.

Strategically, manufacturers that combine educational value, licensed content, and sustainable production capabilities are positioned to capture the highest-margin demand segments.

Market Size & Growth: USD 1,436.0 Million in 2025, reaching USD 2,467.3 Million by 2033 at 7.0% CAGR, driven by STEM-learning adoption and premium construction toy innovation.

Top Growth Drivers: STEM toy demand up 22%, eco-friendly toy purchases up 18%, and licensed character-based toy sales increasing by 16%.

Short-Term Forecast: By 2028, recycled-material usage in toy blocks is expected to increase by 25%, reducing virgin plastic dependency across major brands.

Emerging Technologies: AI-enabled interactive play, augmented reality integration, and bio-based polymer materials are improving engagement and product differentiation.

Regional Leaders: North America surpasses USD 700 Million, Europe exceeds USD 560 Million, and Asia-Pacific approaches USD 650 Million, supported by educational toy adoption and retail expansion.

Consumer/End-User Trends: Nearly 62% of parents prioritize educational play products, while demand for screen-connected learning toys continues expanding.

Pilot/Case Example: In 2024, digital-enhanced construction toy programs improved child engagement metrics by approximately 30% during structured learning activities.

Competitive Landscape: LEGO commands roughly 35% market share, alongside Mattel, Hasbro, Melissa & Doug, and Spin Master.

Regulatory & ESG Impact: Recycled-content initiatives reduced plastic usage by nearly 20% across selected product portfolios following sustainability commitments.

Investment & Funding: More than USD 500 Million has been directed toward manufacturing upgrades, sustainable materials, and regional supply-chain expansion initiatives.

Innovation & Future Outlook: Smart-connected building sets, modular educational ecosystems, and sustainable material platforms are strengthening long-term competitive positioning.

The Childrens Toy Blocks Market is increasingly shaped by educational play concepts, sustainable material innovation, and digital engagement features. Demand remains particularly strong across STEM-learning applications, preschool development programs, and licensed entertainment products. Approximately 62% of parents actively seek toys with educational benefits, encouraging manufacturers to introduce interactive and sensor-enabled building systems. Simultaneously, supply-chain diversification beyond traditional manufacturing hubs is improving resilience and accelerating product customization, creating a strong foundation for the market’s next strategic phase.

The Childrens Toy Blocks Market is becoming strategically important as educational outcomes, brand engagement, and digital play ecosystems increasingly influence purchasing decisions. Manufacturers are no longer competing solely on product variety; they are competing on learning effectiveness, sustainability credentials, and consumer retention. Supply-chain restructuring following geopolitical trade disruptions has encouraged greater production diversification across Vietnam, India, and Eastern Europe, improving sourcing flexibility and reducing concentration risk.

Technology integration is redefining competitive dynamics. Interactive toy block systems incorporating augmented reality demonstrate engagement levels approximately 25–30% higher than traditional construction sets, while recycled-material manufacturing processes reduce raw-material dependency by nearly 15% compared with conventional production models. North America leads in premium product penetration and licensing partnerships, whereas Asia-Pacific records faster adoption of educational toy formats driven by expanding middle-class spending and growing STEM-focused curricula.

Recent deployment examples include connected building platforms that combine physical construction with mobile-based learning modules, improving user retention and repeat purchases. Major manufacturers are expanding investments in sustainable polymers, digital content partnerships, and regional manufacturing capabilities to strengthen operational resilience. Over the next two to three years, educational product portfolios, localized production strategies, and technology-enhanced play experiences will increasingly determine competitive positioning, brand loyalty, and long-term market relevance.

STEM-focused learning programs have become a major catalyst for toy block adoption, with educational toy purchases increasing by approximately 22% across developed consumer markets. Nearly 62% of parents now prioritize products supporting cognitive and problem-solving development, while school-based learning activities increasingly incorporate construction-based educational tools. The United States and Japan continue expanding educational technology initiatives that reinforce hands-on learning environments. This shift directly increases demand for advanced construction sets designed around engineering, mathematics, and creative thinking concepts. In response, leading manufacturers are launching curriculum-aligned product portfolios, expanding licensing partnerships, and investing in digital learning integrations. A notable strategic outcome is the convergence of education and entertainment, allowing companies to command premium pricing while strengthening long-term customer engagement and repeat purchase behavior.

Volatility in petrochemical-derived plastic inputs remains a structural limitation for toy block manufacturers. Raw-material cost fluctuations have periodically exceeded 15%, while logistics expenses remain elevated compared with pre-disruption benchmarks. China still accounts for a substantial portion of global toy manufacturing capacity, creating exposure to supply-chain concentration risks and trade-related disruptions. These pressures affect profitability, inventory planning, and pricing strategies, particularly for mid-sized producers. Companies are responding by diversifying sourcing networks, increasing production capacity in India and Vietnam, and negotiating longer-term supplier agreements. An important operational insight is that manufacturers with localized production capabilities can reduce transportation exposure and improve fulfillment responsiveness, creating a measurable competitive advantage during periods of supply instability.

Demand for environmentally responsible products is creating significant opportunities for advanced toy block manufacturers. Surveys indicate that nearly 45% of parents actively consider sustainability attributes during toy purchases, while recycled-material adoption within premium toy categories continues expanding. Bio-based plastics, recyclable polymers, and smart-connected construction systems are emerging as key innovation areas. In Europe, sustainability regulations are encouraging greater transparency in material sourcing and product lifecycle management. Companies are accelerating R&D investments, partnering with material science providers, and developing digital-enhanced construction experiences that combine physical and virtual play. A particularly attractive opportunity lies in modular learning ecosystems that integrate coding, robotics, and engineering concepts, enabling brands to expand beyond traditional toy categories and capture higher-value educational spending.

As manufacturers introduce connected and interactive building platforms, maintaining affordability and broad accessibility has become increasingly complex. Smart-enabled construction sets can cost 20–35% more than traditional alternatives, limiting adoption among price-sensitive consumers. Software maintenance, content development, and compatibility requirements also increase long-term operational complexity. Markets such as Germany and the United States are witnessing growing expectations for seamless digital experiences, placing pressure on manufacturers to continually update technology ecosystems. Companies must balance innovation investments with product affordability while ensuring consistent user experiences across multiple devices and platforms. The most successful participants are building strategic partnerships with educational technology providers and digital content developers, enabling scalable innovation without significantly increasing production complexity or consumer acquisition costs.

Sustainable Material Transition Accelerates Manufacturers are rapidly replacing conventional plastics with recycled and bio-based polymers as sustainability requirements reshape procurement strategies. More than 35% of newly launched premium toy block products now incorporate recycled content, while material substitution initiatives have reduced virgin plastic consumption by nearly 20% in selected portfolios. European packaging compliance requirements and retailer sustainability mandates are pushing suppliers to redesign production workflows. Companies are expanding partnerships with material innovators and restructuring supply chains to improve environmental performance while strengthening brand differentiation.

Digital-Enhanced Play Experiences Expand Connected play ecosystems are becoming mainstream as manufacturers integrate mobile applications, augmented reality features, and interactive learning modules into construction sets. Engagement rates for digitally enhanced products are approximately 28% higher than traditional alternatives, while repeat usage levels have improved by nearly 22%. The transition toward hybrid physical-digital play is encouraging brands to invest in software development, content licensing, and educational technology collaborations. This shift is improving customer retention and extending product lifecycle value.

Supply Chain Diversification Intensifies Ongoing geopolitical trade adjustments and logistics volatility are accelerating manufacturing diversification beyond traditional production hubs. Nearly 18% of toy-sector sourcing contracts have shifted toward India and Vietnam over the past few years, reducing concentration risks and improving inventory resilience. Companies are increasing regional assembly capabilities, implementing supplier redundancy programs, and adopting advanced planning systems. A notable outcome is faster product replenishment cycles and greater responsiveness to seasonal demand fluctuations.

Licensed Educational Themes Strengthen Demand Educational content and entertainment licensing are increasingly converging within the toy block category. Licensed construction products now account for approximately 30% of premium segment launches, while STEM-oriented themes have recorded adoption gains exceeding 20% among school-age consumers. Manufacturers are securing long-term intellectual property partnerships and expanding curriculum-aligned product portfolios. This operational shift enables stronger pricing power, broader retail visibility, and improved consumer engagement across multiple age groups.

Plastic Blocks remain the dominant segment, accounting for approximately 58% of global demand due to their durability, manufacturing scalability, design flexibility, and compatibility with large-scale production systems. Their ability to support intricate construction designs and extensive product ecosystems has enabled leading brands to maintain strong market penetration across retail and educational channels. Wooden Blocks continue to hold relevance in preschool learning environments where tactile development and sustainability attributes influence purchasing decisions. Foam Blocks retain strategic importance in early-childhood applications because of their safety profile and lightweight construction. Eco-friendly and Recycled Material Blocks represent the fastest-growing segment as sustainability considerations increasingly influence procurement decisions. Adoption of recycled-content products has expanded by more than 25% among premium toy portfolios, encouraging manufacturers to invest in alternative materials and sustainable production capabilities. Companies are prioritizing innovation in bio-based polymers, recyclable packaging, and environmentally responsible product lines to strengthen competitive positioning. Investment priorities are gradually shifting from traditional volume-based expansion toward value-added sustainable offerings capable of attracting environmentally conscious consumers and institutional buyers.

Educational Learning remains the leading application segment, representing nearly 45% of total demand as schools, learning centers, and parents increasingly prioritize cognitive development tools. Construction toys are widely used to support problem-solving, creativity, spatial reasoning, and STEM-based learning outcomes. Strong integration into classroom activities and structured educational programs has reinforced demand concentration within this segment. Skill Development applications also maintain substantial adoption as parents seek products that encourage motor coordination, teamwork, and critical thinking. STEM and Coding-Oriented Learning applications are emerging as the fastest-growing segment, supported by increasing emphasis on science and engineering education. Adoption rates for STEM-focused toy block programs have increased by approximately 22%, particularly within developed education markets. Recreational Play continues to generate significant volume demand, while Therapeutic and Developmental Learning applications are gaining traction among specialized educational institutions. Manufacturers are responding through curriculum-aligned product launches, digital integration initiatives, and partnerships with educational organizations to strengthen long-term market relevance and diversify demand channels.

Households remain the largest end-user segment, accounting for roughly 68% of overall market demand. Parents continue to prioritize construction toys for creativity, problem-solving development, and screen-free engagement, resulting in sustained purchasing activity across multiple age categories. Strong brand recognition, licensed content, and product innovation further reinforce household demand. Retail distribution networks and e-commerce platforms have expanded accessibility, supporting consistent consumption patterns throughout major consumer markets. Educational Institutions represent the fastest-growing end-user category as schools increasingly integrate hands-on learning methodologies into classroom environments. Adoption of construction-based learning tools has increased by approximately 20% within STEM-focused educational programs. Childcare Centers and Early Learning Facilities continue to expand procurement of age-specific building systems designed to enhance collaborative learning and motor-skill development. Corporate learning and specialized therapy centers remain niche but strategically important buyers. Manufacturers are responding through institutional pricing models, curriculum partnerships, customized educational kits, and ecosystem-based product offerings that align with evolving learning objectives and procurement requirements.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America maintains the leading position through strong household spending, advanced retail distribution, and widespread adoption of STEM-oriented learning products. The region contributes approximately 36.8% of global demand, supported by high penetration of licensed construction toys and educational play systems. More than 60% of parents prioritize learning-focused toys, encouraging manufacturers to expand curriculum-aligned product portfolios. Retailers continue increasing shelf allocation for sustainable and interactive construction sets, while digital-connected toy ecosystems are improving engagement metrics by nearly 25%. Companies are strengthening regional production networks and strategic licensing agreements to improve supply responsiveness and product differentiation across major consumer segments.

United States Market Outlook: The United States represents the largest national market due to its extensive toy retail infrastructure, strong licensing ecosystem, and significant educational toy adoption. Approximately 28% of global toy block consumption originates from the country, supported by widespread integration of STEM learning concepts into household purchasing decisions. Manufacturers continue investing in sustainable materials, digital engagement features, and entertainment partnerships. The combination of premium consumer spending, advanced e-commerce penetration, and established brand loyalty provides a substantial competitive advantage for market participants operating within the U.S. toy industry.

Europe accounts for approximately 27.4% of global market activity and remains a key center for sustainable toy innovation. Consumer preference for environmentally responsible products is encouraging manufacturers to increase recycled-content utilization and redesign packaging formats. More than 35% of premium construction toy launches now incorporate sustainability-focused materials. Regulatory emphasis on circular economy initiatives is accelerating material innovation and supply-chain transparency. Educational institutions across major European economies continue expanding hands-on learning methodologies, supporting demand for construction-based learning tools. Companies are responding through sustainable manufacturing investments, product redesign programs, and long-term partnerships with environmentally focused material suppliers.

Germany Market Outlook: Germany serves as Europe's most strategically important market due to its strong educational toy culture, advanced manufacturing ecosystem, and sustainability leadership. Educational construction toys represent a significant share of learning-oriented toy purchases, while environmentally certified products continue gaining traction among consumers. Domestic and international manufacturers are expanding investments in recycled materials, sustainable packaging technologies, and premium educational product portfolios. Germany's established retail infrastructure and strong consumer preference for quality-focused products create favorable conditions for long-term market expansion and innovation deployment.

Asia-Pacific accounts for approximately 24.6% of global demand and serves as the world's most important toy manufacturing hub. Rising disposable income, urbanization, and expanding middle-class populations are increasing spending on educational and developmental toys. The region produces a substantial share of global toy exports, supported by extensive manufacturing ecosystems and supply-chain infrastructure. Production diversification efforts have accelerated investment into India and Southeast Asia, while educational toy adoption continues strengthening across key consumer markets. Companies are expanding regional manufacturing capacity, localizing product portfolios, and strengthening distribution networks to capitalize on growing domestic demand and export opportunities.

China Market Outlook: China remains the dominant country due to its unmatched manufacturing scale, integrated supplier ecosystem, and export-oriented production capabilities. The country accounts for a majority share of global toy manufacturing output and continues investing in automation, smart production systems, and supply-chain modernization. Domestic demand is also strengthening as educational toy purchases expand among urban households. Manufacturers are increasingly targeting higher-value product categories, including interactive learning systems and sustainable toy blocks, improving both export competitiveness and domestic market penetration.

South America represents approximately 6.3% of global market activity and is witnessing steady expansion through increasing awareness of developmental learning products. Urban households are allocating greater spending toward educational toys that support creativity and cognitive development. Retail modernization and e-commerce adoption are improving product accessibility across major population centers. However, import dependency and currency volatility continue affecting product pricing and inventory management. Companies are mitigating these constraints through regional distribution partnerships and localized sourcing initiatives. Educational toy categories have recorded adoption increases exceeding 15% in selected metropolitan markets, strengthening long-term demand fundamentals.

Brazil Market Outlook: Brazil leads the regional market through its large consumer base, expanding retail infrastructure, and growing interest in educational play products. Major retailers continue broadening premium toy assortments, while online channels improve access to international brands. Demand for STEM-oriented toy blocks is increasing among middle-income households seeking developmental learning solutions. Manufacturers and distributors are investing in localized marketing strategies, educational partnerships, and improved logistics capabilities to strengthen market reach and improve responsiveness to evolving consumer preferences.

The Middle East & Africa region accounts for approximately 4.9% of global market demand and is increasingly benefiting from investments in education, retail modernization, and family-focused consumer spending. Premium toy retail formats are expanding across major urban centers, while educational learning initiatives are improving awareness of construction-based developmental toys. Modern shopping destinations and organized retail channels continue increasing product visibility. Several markets are recording double-digit growth in educational toy imports, reflecting strengthening demand fundamentals. Companies are pursuing regional partnerships, distributor expansion programs, and targeted product localization strategies to improve market penetration.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's most influential market due to its advanced retail infrastructure, strong consumer purchasing power, and growing focus on educational development. Premium toy categories continue expanding across major retail destinations, supported by international brand presence and high household spending levels. Educational institutions increasingly incorporate interactive learning approaches, creating favorable conditions for construction-based learning products. Strategic investments in retail modernization, logistics efficiency, and family-oriented consumer experiences position the UAE as a key gateway market for regional expansion.

The Childrens Toy Blocks Market is led by global brands including LEGO Group, Mattel (Mattel Brick Shop/MEGA), Hasbro, Spin Master, and Melissa & Doug, competing against regional educational toy manufacturers and value-focused private-label suppliers. The top five players collectively control approximately 65% of global market activity, with LEGO maintaining the strongest position through brand equity, licensing reach, and manufacturing scale. Competition centers on innovation, educational value, sustainability, and ecosystem expansion rather than price alone. Premium construction sets generate engagement rates nearly 25% higher than conventional products, while licensed product portfolios improve sell-through performance by over 20%. Companies are expanding through franchise partnerships, digital play integration, sustainable material adoption, and supply-chain diversification. The competitive shift is moving from traditional brick manufacturing toward connected learning experiences and sustainability-led differentiation. High tooling costs, intellectual property protection, retail shelf access, and brand trust create significant entry barriers. Success increasingly depends on combining educational outcomes, strong intellectual property partnerships, sustainable production capabilities, and omnichannel distribution excellence.

Mattel Inc.

Hasbro Inc.

Spin Master Corp.

Melissa & Doug

Hape Holding AG

BanBao Co., Ltd.

Sluban Toys

Cobi S.A.

Oxford Co., Ltd.

Magformers LLC

Simba Dickie Group

PlayMonster Group LLC

BRIKSMAX

Technology development is increasingly focused on sustainable materials, digital engagement, and advanced manufacturing efficiency. Recycled and renewable polymers are replacing conventional petroleum-based plastics, improving material sustainability while maintaining durability standards. In 2025, some leading manufacturers achieved more than 50% renewable or recycled material integration across production portfolios. Automated molding systems have reduced manufacturing waste by approximately 12–15%, improving operational efficiency and production consistency.

Digital integration is emerging as a major differentiator. Augmented reality-enabled building experiences and mobile-connected construction platforms increase user engagement by nearly 28% compared with traditional standalone products. Educational toy ecosystems incorporating coding, robotics, and interactive learning modules have recorded adoption growth exceeding 20% among school-age users. AI-assisted design platforms are also accelerating product development cycles, enabling faster concept testing and improved customization capabilities.

Compared with legacy toy block systems, connected learning platforms deliver approximately 25% higher engagement and stronger repeat-use behavior. Global leaders with established intellectual property portfolios and digital capabilities benefit most from this transition. Between 2026 and 2028, smart construction ecosystems, advanced sustainable materials, and AI-supported design workflows are expected to become critical competitive assets. Companies acting early gain stronger consumer retention, improved operational flexibility, and greater differentiation within increasingly sophisticated educational play markets.

January 2025 – Mattel Inc. launched the new Mattel Brick Shop building-set brand at the Nuremberg International Toy Fair, entering the construction-toy segment with global rollout plans. The initiative expanded product portfolio diversification and strengthened competitive positioning against established category leaders. Source: www.corporate.mattel.com

May 2025 – Mattel Inc. unveiled the first Hot Wheels Collector Builds collection under Mattel Brick Shop, introducing seven collectible building sets with integrated die-cast vehicles. The launch strengthened licensing-driven product differentiation and expanded presence in premium construction toy categories.

June 2025 – Mattel Inc. and OpenAI announced a strategic collaboration to develop AI-powered play experiences. The partnership introduced advanced digital engagement capabilities and accelerated innovation in connected toy ecosystems, creating new opportunities for interactive educational experiences.

February 2025 – LEGO Group introduced selected tire components containing at least 30% recycled content and planned deployment across approximately 120 product sets by year-end. The initiative strengthened sustainable material adoption while reducing dependence on virgin fossil-based inputs.

The report provides comprehensive analysis of market dynamics, competitive positioning, technology evolution, and demand patterns across the global Childrens Toy Blocks industry. Coverage includes key product categories such as Plastic Blocks, Wooden Blocks, Foam Blocks, and Eco-friendly or Recycled Material Blocks. Application analysis evaluates Educational Learning, Recreational Play, Skill Development, STEM Learning, and Therapeutic Learning segments, while end-user assessment examines households, educational institutions, childcare centers, and specialized learning facilities.

Regional evaluation spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level operational insights and adoption trends. The report assesses sustainability initiatives, digital play integration, smart learning ecosystems, advanced materials, and manufacturing modernization strategies. More than 60% of purchasing decisions are increasingly influenced by educational value and developmental outcomes, making innovation and product differentiation critical. Strategic insights support investment planning, market entry assessment, expansion prioritization, partnership development, competitive benchmarking, and long-term positioning across evolving educational and interactive play ecosystems through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,436.0 Million |

| Market Revenue (2033) | USD 2,467.3 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | LEGO Group; Mattel Inc.; Hasbro Inc.; Spin Master Corp.; Melissa & Doug; Hape Holding AG; BanBao Co., Ltd.; Sluban Toys; Cobi S.A.; Oxford Co., Ltd.; Magformers LLC; Simba Dickie Group; PlayMonster Group LLC; BRIKSMAX |

| Customization & Pricing | Available on Request (10% Customization Free) |