Reports

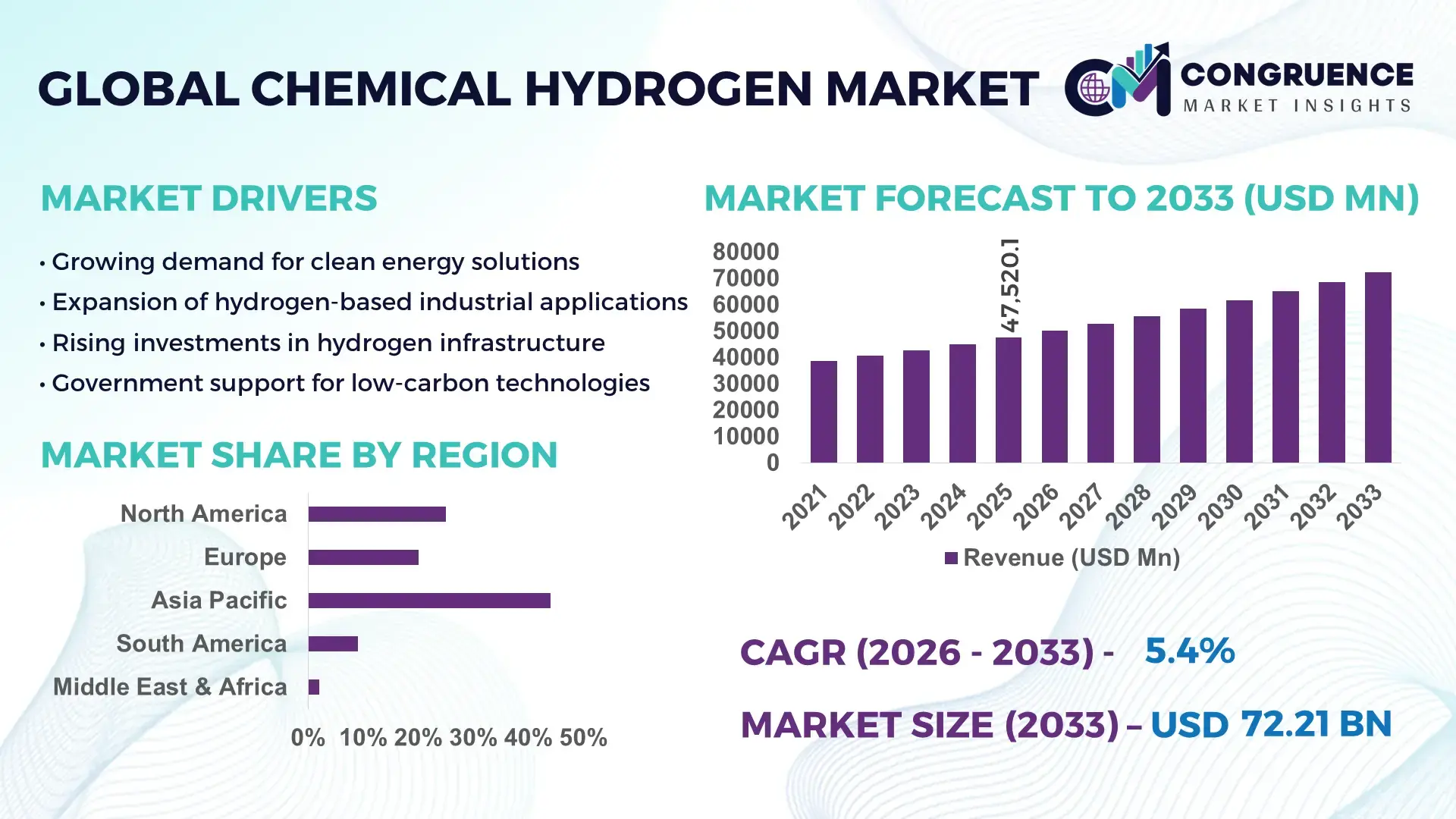

The Global Chemical Hydrogen Market was valued at USD 47520.14 Million in 2025 and is anticipated to reach a value of USD 72212.69 Million by 2033 expanding at a CAGR of 5.37% between 2026 and 2033. Rising industrial decarbonization initiatives and growing hydrogen demand in refining, fertilizers, and clean energy applications are accelerating global adoption.

China remains the most dominant country in the Chemical Hydrogen Market with extensive production infrastructure and strong industrial demand. The country operates more than 25 million metric tons of hydrogen production capacity annually, largely supplied through coal gasification and steam methane reforming. Major petrochemical complexes integrate hydrogen for ammonia, methanol, and refining processes, supporting large-scale industrial utilization. China has also invested heavily in green hydrogen projects, exceeding 300 planned electrolyzer installations with combined capacities above 3 GW. Industrial clusters across Inner Mongolia, Hebei, and Guangdong integrate hydrogen supply networks for steelmaking, chemicals, and synthetic fuels. Rapid expansion of hydrogen refueling stations, surpassing 350 operational units, further strengthens technological advancement and sector integration within the country’s chemical hydrogen ecosystem.

Market Size & Growth: Valued at USD 47.52 billion in 2025 and projected to reach USD 72.21 billion by 2033, driven by expanding hydrogen-based chemical processing and energy transition initiatives.

Top Growth Drivers: Industrial hydrogen demand rising by 42%, green hydrogen adoption improving by 35%, and refinery hydrogen efficiency increasing by 28%.

Short-Term Forecast: By 2028, advanced electrolysis systems are expected to reduce hydrogen production costs by nearly 18% through improved energy efficiency and automation.

Emerging Technologies: Proton exchange membrane electrolysis, solid oxide electrolyzers, and carbon capture integrated hydrogen production are reshaping large-scale chemical hydrogen manufacturing.

Regional Leaders: Asia-Pacific projected to reach USD 33 billion by 2033 with strong industrial usage; Europe USD 18 billion driven by green hydrogen mandates; North America USD 14 billion supported by hydrogen infrastructure expansion.

Consumer/End-User Trends: Refining, ammonia production, and methanol synthesis remain primary consumers, collectively accounting for over 70% of chemical hydrogen demand.

Pilot or Case Example: In 2024, a large-scale electrolyzer project in Europe demonstrated a 22% efficiency improvement in hydrogen generation for chemical feedstock applications.

Competitive Landscape: Air Liquide leads with approximately 14% share, followed by Linde, Air Products, Iwatani Corporation, and Plug Power.

Regulatory & ESG Impact: Carbon reduction policies target up to 40% industrial emission reduction by 2030, encouraging low-carbon hydrogen integration.

Investment & Funding Patterns: Over USD 85 billion has been committed globally to hydrogen infrastructure and production projects in recent years.

Innovation & Future Outlook: Integrated hydrogen hubs, digital plant optimization, and renewable-powered electrolysis are shaping the next generation of chemical hydrogen production.

Chemical hydrogen plays a critical role across multiple industrial sectors including petroleum refining, fertilizer manufacturing, methanol synthesis, and specialty chemicals. Refining accounts for roughly 38% of hydrogen consumption, while ammonia production contributes nearly 32%. Technological progress in electrolyzers, hydrogen purification systems, and carbon capture technologies is improving production efficiency and reducing environmental impact. Government policies encouraging low-carbon hydrogen production, particularly in Europe and Asia, are accelerating infrastructure development and industrial integration. Increasing demand for synthetic fuels, green ammonia, and sustainable chemical processing is expected to expand hydrogen utilization across heavy industries and emerging energy systems.

The Chemical Hydrogen Market has become strategically critical as industries transition toward low-carbon production systems and cleaner chemical processing technologies. Hydrogen serves as an essential feedstock in ammonia synthesis, refining hydrocracking, and methanol production, supporting more than 80 million metric tons of annual global demand. Modern proton exchange membrane electrolysis delivers nearly 25% efficiency improvement compared to conventional alkaline electrolysis, enabling scalable low-carbon hydrogen production. Asia-Pacific dominates in production volume due to large petrochemical and fertilizer industries, while Europe leads in adoption with over 45% of enterprises investing in green hydrogen integration across industrial clusters. Government-backed hydrogen strategies and carbon pricing frameworks are pushing industries to integrate cleaner hydrogen supply chains.

By 2028, AI-enabled hydrogen production optimization systems are expected to improve plant energy efficiency by approximately 15% while reducing operational downtime. Firms are committing to ESG-driven industrial decarbonization targets such as 30% emission reduction in chemical production by 2030 through renewable-powered hydrogen generation. In 2024, a large industrial hydrogen initiative in Germany achieved a 20% reduction in process emissions using renewable-powered electrolysis and digital monitoring technologies. These developments position the Chemical Hydrogen Market as a central pillar supporting industrial resilience, regulatory compliance, and sustainable global chemical production.

Refining and fertilizer industries remain the largest consumers of chemical hydrogen, accounting for nearly 70% of global demand. Hydrogen is essential for hydrocracking and desulfurization processes that enable production of cleaner fuels. Global ammonia production exceeds 180 million metric tons annually, requiring large volumes of hydrogen as a feedstock. Growing agricultural demand for nitrogen fertilizers is expanding ammonia manufacturing capacity in Asia and the Middle East. Additionally, stricter fuel emission standards require refineries to increase hydrogen consumption for ultra-low sulfur fuel production. These industrial requirements continue to drive consistent growth in hydrogen production capacity, encouraging investments in large-scale hydrogen plants and integrated chemical processing facilities worldwide.

Traditional hydrogen production methods such as steam methane reforming and coal gasification remain energy-intensive and carbon-emitting processes. Producing one kilogram of hydrogen through steam methane reforming can generate approximately 9–10 kilograms of carbon dioxide emissions. Rising natural gas prices and carbon taxation policies are increasing operational costs for hydrogen producers. In regions with strict environmental regulations, industries face additional expenses for carbon capture systems and emission mitigation technologies. Infrastructure limitations, including hydrogen transport pipelines and storage systems, further increase capital expenditure requirements. These cost challenges slow the transition toward cleaner hydrogen production technologies and restrict rapid expansion in several developing markets.

Green hydrogen produced through renewable-powered electrolysis presents a significant growth opportunity for the Chemical Hydrogen Market. Global electrolyzer capacity is projected to exceed 50 GW in the coming decade as governments accelerate decarbonization strategies. Renewable electricity costs have declined by nearly 70% over the past decade, improving the economic feasibility of large-scale hydrogen production. Green hydrogen is increasingly being used for sustainable ammonia, methanol, and synthetic fuel production. Industrial hydrogen hubs combining solar, wind, and electrolysis technologies are being developed across Europe, the Middle East, and Australia. These developments are enabling industries to replace carbon-intensive hydrogen sources with environmentally sustainable alternatives.

Hydrogen storage and transportation remain major technical challenges due to hydrogen’s low volumetric energy density and high diffusivity. Compressing hydrogen for storage requires pressures exceeding 350–700 bar, significantly increasing equipment and energy costs. Liquefaction processes require extremely low temperatures of around −253°C, demanding specialized cryogenic infrastructure. Many regions lack dedicated hydrogen pipelines, forcing industries to rely on costly transportation methods such as tube trailers or liquefied hydrogen tanks. Additionally, large-scale storage solutions such as underground salt caverns or advanced composite tanks require substantial capital investment. These infrastructure barriers limit rapid deployment of hydrogen supply networks and create logistical challenges for expanding industrial hydrogen consumption.

• Rapid Expansion of Green Hydrogen Electrolysis Capacity: Industrial investment in renewable-powered hydrogen production is accelerating rapidly. Global installed electrolyzer capacity surpassed 1.4 GW in 2024, with more than 320 large-scale projects under development worldwide. Nearly 60% of upcoming facilities are designed for chemical feedstock applications such as ammonia and methanol production. Europe alone plans over 90 industrial electrolysis plants exceeding 100 MW capacity each. Technological improvements have increased electrolysis efficiency by approximately 18% over the past five years, enabling large chemical producers to replace fossil-based hydrogen. Industrial decarbonization programs targeting 30–40% emission reductions in chemical processing are further strengthening adoption of green hydrogen systems.

• Integration of Carbon Capture with Hydrogen Production: Carbon capture and storage integration in hydrogen manufacturing is emerging as a critical trend. Blue hydrogen facilities now capture up to 90% of carbon dioxide emissions generated during steam methane reforming processes. More than 40 large industrial hydrogen plants globally are installing carbon capture systems capable of storing over 20 million metric tons of CO₂ annually. This technology is particularly expanding across North America and the Middle East, where over 65% of new hydrogen projects incorporate carbon capture infrastructure. Advanced catalytic reformers and digital monitoring technologies have improved carbon capture efficiency by nearly 15%, supporting cleaner hydrogen production for refining and chemical synthesis operations.

• Growth of Hydrogen Industrial Clusters and Supply Networks: Hydrogen hubs and industrial clusters are transforming how chemical hydrogen is produced and distributed. More than 70 hydrogen cluster projects are currently under development globally, linking hydrogen production with refining, steelmaking, fertilizer, and chemical plants. Industrial hydrogen pipeline networks now extend beyond 5,000 kilometers worldwide, enabling efficient transport across major production and consumption centers. In Asia-Pacific, hydrogen infrastructure investment has increased by nearly 45% over the past three years. Integrated hydrogen clusters improve supply chain efficiency and reduce transportation costs by approximately 20%, enabling large chemical manufacturers to maintain stable hydrogen feedstock availability.

• Increasing Hydrogen Utilization in Synthetic Fuel and Chemical Manufacturing: Hydrogen demand is expanding significantly in emerging chemical applications such as synthetic fuels, green ammonia, and methanol production. Global synthetic fuel pilot facilities increased by more than 50% between 2022 and 2024. Industrial methanol production consumes nearly 15% of global hydrogen output, while ammonia synthesis accounts for over 30%. Advancements in catalytic hydrogenation technologies have improved chemical conversion efficiency by nearly 12%. Several industrial plants are now producing over 500,000 tons of hydrogen-based synthetic fuels annually, demonstrating the growing role of hydrogen in future low-carbon chemical manufacturing systems.

The Chemical Hydrogen Market is segmented based on production type, industrial application, and end-user industries that consume hydrogen as a chemical feedstock. Production technologies include steam methane reforming, coal gasification, and electrolysis-based hydrogen generation. Applications are dominated by petroleum refining, ammonia production, methanol synthesis, and specialty chemical manufacturing. End-user industries range from oil and gas companies to fertilizer producers, chemical manufacturers, and emerging clean energy developers. Industrial hydrogen consumption remains heavily concentrated in large-scale chemical and petrochemical facilities, where hydrogen supports catalytic reactions and feedstock synthesis. Increasing environmental regulations and industrial decarbonization targets are gradually shifting production toward low-carbon hydrogen technologies and expanding usage across energy, transport fuel, and advanced chemical manufacturing sectors.

The Chemical Hydrogen Market is segmented into Steam Methane Reforming (SMR), Coal Gasification, Electrolysis-based Hydrogen Production, and other emerging technologies such as biomass gasification and methane pyrolysis. Steam methane reforming remains the leading production type, accounting for approximately 58% of global hydrogen production due to its established industrial infrastructure and relatively lower production cost. Coal gasification follows with nearly 28% share, particularly concentrated in large industrial regions where coal resources remain abundant. Electrolysis-based hydrogen production currently represents about 11% of the market but is expanding rapidly as industries transition toward low-carbon production systems.

Electrolysis hydrogen production is the fastest-growing segment with an estimated CAGR of around 16%, driven by falling renewable electricity costs and expanding industrial decarbonization initiatives. Proton exchange membrane and solid oxide electrolyzers are improving efficiency levels by nearly 20%, enabling large-scale green hydrogen production for chemical applications. Meanwhile, other emerging technologies such as methane pyrolysis and biomass gasification collectively contribute nearly 3% of hydrogen supply, serving niche low-emission hydrogen production markets.

The Chemical Hydrogen Market is widely applied across petroleum refining, ammonia production, methanol synthesis, and specialty chemical manufacturing. Petroleum refining represents the leading application segment with approximately 38% of total hydrogen utilization. Hydrogen is extensively used in hydrocracking and desulfurization processes that enable refineries to produce ultra-low sulfur fuels and cleaner petroleum products. Ammonia production follows with about 32% share, as hydrogen serves as the primary feedstock for nitrogen fertilizer manufacturing essential to global agricultural supply chains.

Methanol production accounts for nearly 18% of hydrogen consumption, where hydrogen participates in catalytic synthesis for fuels, solvents, and industrial chemicals. However, synthetic fuels and green chemical production represent the fastest-growing application segment with an estimated CAGR of nearly 14%, driven by global decarbonization policies and renewable energy integration. These applications are projected to exceed 20% adoption across hydrogen-consuming chemical industries by 2033.

End-user industries within the Chemical Hydrogen Market include oil and gas refining companies, fertilizer manufacturers, chemical producers, and emerging clean energy developers. Oil refining remains the leading end-user segment, accounting for approximately 40% of global hydrogen consumption. Hydrogen is critical for hydroprocessing operations that remove sulfur and improve fuel quality. Fertilizer manufacturers represent the second-largest end-user group with nearly 30% share, driven by the large-scale production of ammonia for nitrogen fertilizers.

Chemical manufacturing companies account for roughly 18% of hydrogen consumption, utilizing hydrogen in methanol synthesis, hydrogenation reactions, and specialty chemical processing. Meanwhile, the clean energy and synthetic fuel sector is the fastest-growing end-user category with an estimated CAGR of about 17%, supported by expanding green hydrogen projects and renewable fuel initiatives. Hydrogen adoption among energy transition projects has increased by nearly 35% over the past three years.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Asia-Pacific produced more than 38 million metric tons of hydrogen annually, largely consumed by refining and fertilizer industries across China, India, and Japan. Europe represented nearly 27% of global hydrogen demand, supported by more than 120 industrial hydrogen projects focused on low-carbon production and electrolyzer deployment exceeding 2 GW capacity. North America held approximately 19% share with over 1,600 hydrogen production facilities supporting petrochemical operations. Meanwhile, the Middle East & Africa accounted for about 5% of demand, supported by expanding hydrogen export infrastructure, while South America contributed roughly 3% with emerging renewable hydrogen initiatives and ammonia production projects.

How Are Industrial Decarbonization Projects Accelerating Hydrogen Demand Across Advanced Manufacturing Sectors?

North America accounts for approximately 19% of the global Chemical Hydrogen Market, supported by large-scale refining, petrochemical manufacturing, and fertilizer production industries. The United States operates more than 1,000 hydrogen production units supplying refineries and chemical plants. Government programs promoting clean hydrogen development include multi-billion-dollar hydrogen hub initiatives supporting electrolyzer deployment and carbon capture integration. Digital monitoring and AI-based hydrogen plant optimization have improved operational efficiency by nearly 12%. Air Products is actively expanding hydrogen production infrastructure and pipeline networks exceeding 1,200 kilometers to support industrial users. Regional industrial behavior shows higher enterprise adoption across refining, energy transition projects, and advanced chemical manufacturing sectors, where companies are integrating hydrogen into cleaner fuel and low-emission production processes.

How Are Sustainability Mandates and Clean Energy Policies Reshaping Industrial Hydrogen Adoption?

Europe holds roughly 27% of the global Chemical Hydrogen Market with major industrial demand concentrated in Germany, France, and the United Kingdom. These countries collectively operate more than 250 hydrogen production facilities supplying petrochemical and ammonia manufacturing sectors. Regional sustainability frameworks promote green hydrogen adoption through carbon reduction targets exceeding 40% across industrial sectors by 2030. Electrolyzer installations across Europe surpassed 2 GW of installed capacity in 2024. Air Liquide is investing heavily in renewable hydrogen production projects and industrial hydrogen pipelines connecting chemical manufacturing clusters. Regional enterprise behavior reflects strong regulatory pressure that encourages adoption of low-carbon hydrogen technologies, especially among chemical producers seeking compliance with strict environmental standards and sustainable industrial manufacturing requirements.

What Industrial Expansion Trends Are Driving Large-Scale Hydrogen Production and Consumption?

Asia-Pacific represents the largest Chemical Hydrogen Market with nearly 46% global consumption and annual production exceeding 38 million metric tons. China, India, and Japan dominate hydrogen utilization across petrochemical refining, fertilizer production, and methanol synthesis industries. China alone operates more than 25 million metric tons of hydrogen capacity annually. Expanding manufacturing sectors and government-backed hydrogen strategies have accelerated infrastructure development, including more than 350 hydrogen refueling stations and multiple electrolyzer projects exceeding 3 GW capacity. Iwatani Corporation continues to expand hydrogen supply networks and storage infrastructure supporting industrial and energy applications. Regional enterprise adoption is driven by rapid industrialization, manufacturing growth, and large-scale integration of hydrogen technologies across heavy industry and energy systems.

How Are Renewable Energy Resources Supporting Hydrogen Development in Emerging Industrial Economies?

South America accounts for approximately 3% of the global Chemical Hydrogen Market, with Brazil and Argentina representing the leading countries in hydrogen production and consumption. Regional hydrogen demand is closely linked to fertilizer manufacturing and petroleum refining operations. Brazil operates several hydrogen production plants supporting ammonia and methanol synthesis facilities. Government energy transition strategies promote renewable hydrogen development through wind and solar resources that exceed 70 GW of combined generation capacity. Petrobras is investing in pilot hydrogen projects focused on integrating renewable energy into industrial hydrogen production systems. Regional consumer behavior shows increasing demand from agricultural fertilizer production and energy transition initiatives supporting sustainable industrial development.

How Are Energy Export Strategies and Industrial Diversification Driving Hydrogen Production?

The Middle East & Africa represent roughly 5% of the global Chemical Hydrogen Market with significant growth driven by energy diversification strategies. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in hydrogen production projects linked to petrochemical industries and export markets. Several large hydrogen production facilities exceeding 500,000 tons annual capacity are under development across the region. Technological modernization includes advanced electrolysis systems and integrated hydrogen-to-ammonia export projects. Saudi Aramco is expanding hydrogen production technologies to support refining operations and future hydrogen export supply chains. Regional industrial behavior reflects strong integration with oil and gas sectors, where hydrogen production supports refinery efficiency and emerging clean fuel export opportunities.

China – 31% market share: China leads the Chemical Hydrogen Market due to its massive industrial hydrogen production capacity exceeding 25 million metric tons annually and extensive demand from refining, fertilizer manufacturing, and chemical processing sectors.

United States – 18% market share: The United States holds a strong position in the Chemical Hydrogen Market with more than 1,000 hydrogen production facilities supporting large petrochemical industries and expanding clean hydrogen infrastructure initiatives.

The Chemical Hydrogen Market features a moderately consolidated competitive landscape with more than 120 active global and regional producers involved in hydrogen generation, distribution, and technology development. The top five companies collectively account for nearly 48% of the global production capacity, reflecting strong industrial scale advantages and integrated supply chain capabilities. Major players operate large hydrogen production facilities, pipeline networks, and industrial gas distribution systems supporting refining, chemical manufacturing, and energy sectors.

Competition is driven by strategic investments in green hydrogen technologies, carbon capture integration, and large-scale electrolyzer deployment. More than 200 hydrogen infrastructure projects are currently under development globally, with many involving joint ventures between industrial gas companies and energy providers. Strategic partnerships between technology developers and industrial operators have increased by over 30% during the past three years. Companies are also focusing on expanding hydrogen pipeline infrastructure exceeding 5,000 kilometers globally to ensure stable supply for industrial clusters.

Innovation trends include the deployment of high-capacity electrolyzers above 100 MW, digital monitoring systems improving plant efficiency by nearly 15%, and hydrogen storage technologies capable of supporting large industrial demand. Competitive differentiation increasingly relies on technological innovation, infrastructure scale, and the ability to provide integrated hydrogen solutions across multiple industrial sectors.

Air Liquide

Linde plc

Air Products and Chemicals Inc.

Iwatani Corporation

Plug Power Inc.

Nel ASA

ITM Power plc

Ballard Power Systems

Bloom Energy Corporation

Cummins Inc.

Messer Group GmbH

Engie SA

Thyssenkrupp AG

Siemens Energy AG

Chart Industries Inc.

Technological advancements in hydrogen production, purification, and storage are reshaping the Chemical Hydrogen Market and improving the efficiency of large-scale industrial hydrogen supply chains. Steam methane reforming remains widely used, accounting for nearly 60% of global hydrogen production; however, innovations such as autothermal reforming and integrated carbon capture systems are enabling up to 90% carbon dioxide capture from hydrogen plants. These improvements significantly reduce emissions associated with conventional hydrogen generation.

Electrolysis technologies are rapidly advancing as industries move toward low-carbon hydrogen production. Proton exchange membrane (PEM) electrolyzers now operate at efficiencies exceeding 70%, while next-generation solid oxide electrolyzers can reach electrical efficiencies above 80% under optimized conditions. Industrial electrolyzer systems exceeding 100 MW capacity are increasingly deployed within hydrogen hubs supporting refining and chemical manufacturing clusters.

Hydrogen liquefaction and storage technologies are also evolving, enabling safer large-scale transport and distribution. Modern cryogenic liquefaction systems operate at temperatures near −253°C and can improve energy efficiency by nearly 10% compared with earlier systems. In parallel, advanced digital plant monitoring platforms using predictive analytics are improving hydrogen production reliability and reducing operational downtime by nearly 15%.

Emerging innovations such as ammonia cracking for hydrogen transport, methane pyrolysis for low-carbon hydrogen generation, and integrated hydrogen pipeline networks exceeding 5,000 kilometers globally are further strengthening the technological foundation supporting the expanding Chemical Hydrogen Market.

• In February 2025, Air Liquide and TotalEnergies announced two large-scale renewable hydrogen projects in the Netherlands, including a 200 MW electrolyzer and a joint venture 250 MW facility to supply industrial platforms and refineries. The projects aim to produce up to 45,000 tons of green hydrogen annually while reducing approximately 500,000 tons of CO₂ emissions. Source: totalenergies.com (TotalEnergies.com)

• In July 2025, Air Liquide confirmed the final investment decision for the 200 MW ELYgator electrolyzer project in Rotterdam. The facility will produce approximately 23,000 tons of renewable hydrogen per year and supply industrial clusters and heavy-duty mobility applications across the Netherlands once operational. Source: globalenergyworld.com (globalenergyworld.com)

• In November 2024, Air Liquide announced a renewable hydrogen production unit at the La Mède industrial platform in France. The facility will produce about 25,000 tons of hydrogen annually using biogenic by-products and is expected to reduce around 130,000 tons of CO₂ emissions per year at the biorefinery. Source: airliquide.com (Air Liquide Engineering)

• In December 2024, Air Liquide received €110 million in European Innovation Fund support for the ENHANCE project at the Port of Antwerp-Bruges. The initiative aims to build an industrial-scale ammonia cracking and hydrogen liquefaction facility to produce and distribute low-carbon hydrogen across European industrial clusters. Source: airliquide.com (Air Liquide Engineering)

The Chemical Hydrogen Market Report provides a comprehensive analysis of global hydrogen production, distribution, and consumption across major industrial sectors. The report examines multiple production technologies including steam methane reforming, coal gasification, proton exchange membrane electrolysis, and emerging processes such as methane pyrolysis and biomass gasification. It evaluates hydrogen utilization across key applications such as petroleum refining, ammonia synthesis, methanol production, synthetic fuels, and specialty chemical manufacturing.

The report covers regional market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, assessing production capacity, industrial demand patterns, and hydrogen infrastructure development including pipelines, storage systems, and hydrogen hubs. It analyzes more than 100 industrial hydrogen production facilities, large-scale electrolyzer installations exceeding 100 MW capacity, and integrated hydrogen supply networks supporting major chemical manufacturing clusters.

In addition, the report evaluates end-user industries such as oil refining companies, fertilizer manufacturers, chemical producers, and energy transition developers adopting hydrogen technologies. Emerging segments including green hydrogen, hydrogen-based synthetic fuels, ammonia cracking systems, and hydrogen export infrastructure are also analyzed. The study provides decision-makers with a structured view of technological innovation, industrial adoption patterns, regulatory frameworks, and competitive positioning shaping the future of the Chemical Hydrogen Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.37% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Air Liquide, Linde plc, Air Products and Chemicals Inc., Iwatani Corporation, Plug Power Inc., Nel ASA, ITM Power plc, Ballard Power Systems, Bloom Energy Corporation, Cummins Inc., Messer Group GmbH, Engie SA, Thyssenkrupp AG, Siemens Energy AG, Chart Industries Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |