Reports

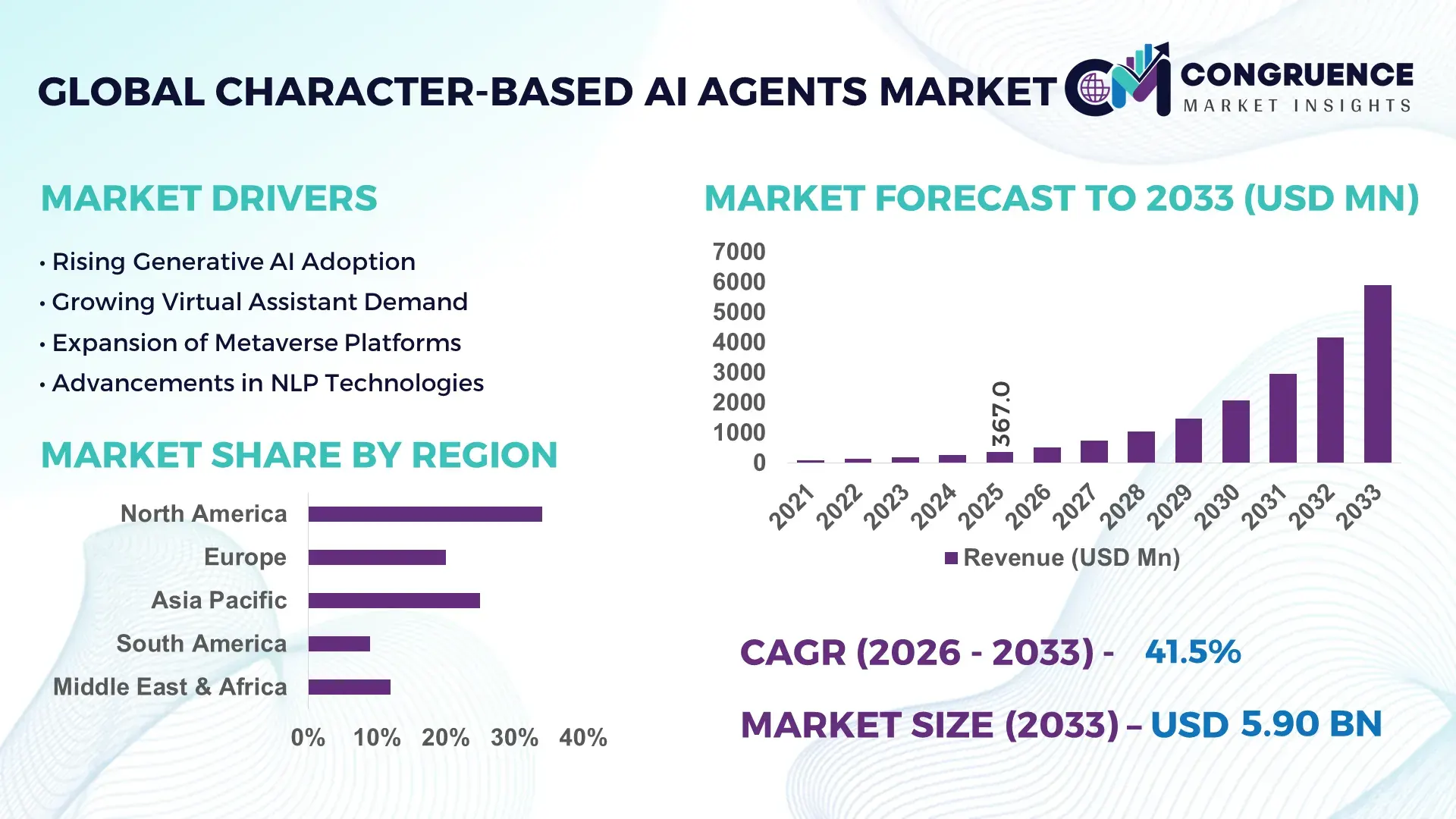

The Global Character-based AI Agents Market was valued at USD 367 Million in 2025 and is anticipated to reach a value of USD 5898.17 Million by 2033 expanding at a CAGR of 41.5% between 2026 and 2033. Enterprise demand for emotionally adaptive AI avatars, multilingual conversational agents, and creator-focused synthetic personalities accelerated deployment cycles by over 38% across gaming, customer engagement, and digital commerce platforms in 2025, while inference optimization reduced operational AI interaction costs by nearly 27% compared to earlier large-model deployments.

The United States maintained market leadership with nearly 34% share in 2025, supported by more than USD 2.1 billion in enterprise generative AI investments linked to entertainment, media streaming, and intelligent customer interaction platforms. Over 62% of large digital content firms in North America integrated AI character engines into user engagement workflows, compared to roughly 41% adoption across Western Europe. Meanwhile, China expanded commercial AI avatar deployment capacity by over 45% through state-backed semiconductor and cloud initiatives targeting virtual influencers, education, and e-commerce livestream ecosystems. Japan strengthened its position in emotionally responsive AI companions for gaming and eldercare, where conversational retention metrics improved by nearly 31% using multimodal character-learning systems.

Market Size & Growth: USD 367 million in 2025 rising toward USD 5898.17 million by 2033, driven by 41% faster enterprise adoption of generative conversational interfaces.

Top Growth Drivers: AI personalization demand increased 44%, gaming avatar monetization expanded 39%, and multilingual virtual assistant deployment grew 36% globally.

Short-Term Forecast: By 2027, AI character automation reduces customer interaction costs by 28% while engagement efficiency improves nearly 33%.

Emerging Technologies: Multimodal AI, emotion-recognition engines, and low-latency inference systems improved response accuracy by over 30% in advanced deployments.

Regional Leaders: North America exceeds USD 1.9 billion with media integration growth, Asia-Pacific surpasses USD 2.3 billion via mobile AI adoption, and Europe crosses USD 1.1 billion through regulated enterprise deployment.

Consumer/End-User Trends: Nearly 58% of Gen Z digital users interacted with AI-based characters weekly across gaming, commerce, and creator platforms in 2025.

Pilot/Case Example: In 2025, a retail AI avatar deployment improved online conversion rates by 24% and reduced support response time by 41%.

Competitive Landscape: Top vendors controlled nearly 46% market share, with competition intensifying among enterprise AI, gaming, and synthetic media developers.

Regulatory & ESG Impact: EU AI compliance frameworks increased enterprise auditing investments by 29%, strengthening demand for transparent conversational AI systems.

Investment & Funding: Global investments exceeded USD 4.4 billion between 2024 and 2026, led by strategic cloud partnerships and AI infrastructure expansion.

Innovation & Future Outlook: Persistent AI memory systems and autonomous digital personalities are increasing user retention rates by over 35% across high-growth platforms.

Gaming and entertainment accounted for nearly 39% of total industry deployment activity in 2025, followed by customer service and digital commerce applications with approximately 28% combined contribution. Advanced multimodal voice synthesis and emotion-aware interaction engines improved conversational retention rates by more than 30%, while Asia-Pacific demand expanded rapidly due to mobile-first AI adoption and localized language models. Ongoing semiconductor supply diversification and tightening AI governance standards are accelerating investment in region-specific infrastructure, with persistent memory-based AI personalities emerging as a major competitive differentiator heading into the next phase of enterprise monetization and strategic platform expansion.

Character-based AI agents are rapidly transforming from engagement tools into core digital infrastructure for customer interaction, entertainment monetization, education delivery, and enterprise automation. Global brands are accelerating investments in emotionally adaptive AI personalities because personalized conversational systems improve user retention by nearly 34% and reduce live-support dependency by over 29%. The market is reshaping competitive dynamics as AI-driven virtual identities increasingly influence digital commerce conversion, creator economies, and immersive platform ecosystems. At the same time, tightening AI governance frameworks and regional data-localization mandates are forcing vendors to redesign deployment architectures and compliance models across North America, Europe, and Asia-Pacific.

Multimodal character AI improves conversational efficiency by 43% while reducing operational servicing costs by 31% compared to legacy scripted chatbot systems. Asia-Pacific leads in deployment volume through mobile-first digital ecosystems, while North America leads in enterprise innovation with over 61% integration across media, gaming, and customer engagement platforms. Over the next three years, advanced memory-enabled AI agents are projected to improve interaction continuity metrics by 37% and increase platform monetization efficiency by nearly 26%. Companies integrating energy-efficient inference systems and transparent AI governance models are also achieving compliance optimization and infrastructure savings exceeding 18%, strengthening ESG positioning as a commercial advantage.

In 2025, a leading gaming platform deployed persistent AI companions that increased average session duration by 22% and improved subscription conversion rates by 17%. This performance shift is accelerating capital allocation toward proprietary character engines, multilingual training models, and low-latency AI infrastructure expansion. Strategic partnerships between cloud providers, entertainment firms, and semiconductor companies are redefining ecosystem control, making scalable character intelligence a long-term competitive moat rather than a standalone product capability.

Rising demand for hyper-personalized digital engagement is accelerating enterprise deployment of character-based AI agents across gaming, e-commerce, media, and customer service ecosystems. More than 58% of Gen Z consumers now prefer AI-driven interactive experiences over static digital interfaces, while enterprise automation initiatives reduced customer engagement costs by nearly 27% during 2025 deployments. The global expansion of creator economies and virtual commerce platforms is forcing brands to integrate emotionally responsive AI characters capable of sustaining longer interaction cycles and higher retention rates. Semiconductor optimization and cloud inference scaling improved conversational response efficiency by 33%, enabling broader commercial rollout. Companies are responding through aggressive AI infrastructure expansion, regional language-model investments, and strategic partnerships with cloud and entertainment platforms worldwide.

High computational dependency and evolving AI governance frameworks are constraining large-scale deployment economics for character-based AI agents. Advanced multimodal AI systems increased enterprise infrastructure expenditure by nearly 32% in 2025, while GPU supply concentration across a limited number of manufacturing hubs extended deployment lead times by over 21%. European AI transparency regulations and regional data-sovereignty mandates are forcing companies to redesign training pipelines, moderation systems, and localization architectures, increasing compliance-related operational overhead. Persistent memory-enabled AI characters also create escalating storage and cybersecurity demands that complicate scalability. Businesses are mitigating these pressures through hybrid cloud diversification, long-term semiconductor procurement agreements, and accelerated investment in smaller domain-specific language models with lower inference costs and improved regulatory adaptability globally.

Persistent character-based AI ecosystems are unlocking high-margin monetization channels across virtual entertainment, education, digital health, and intelligent commerce environments. AI companions with memory retention capabilities improved user engagement duration by nearly 36%, while multilingual conversational systems expanded international accessibility rates by over 28% during 2025 deployments. The rapid rise of synthetic influencers and AI-driven creator platforms is reshaping digital advertising economics, especially across Asia-Pacific mobile ecosystems. Businesses are increasingly leveraging emotion-recognition models and real-time personalization engines to optimize conversion performance and subscription retention simultaneously. Companies are accelerating R&D investments into autonomous character orchestration, decentralized AI identity systems, and cross-platform interoperability frameworks to secure long-term ecosystem control and strengthen competitive differentiation in emerging immersive digital economies globally.

Maintaining scalable performance consistency while balancing regulatory compliance, computational efficiency, and user trust remains the industry’s most critical execution challenge. Large-scale AI character systems increased energy consumption intensity by approximately 24% compared to conventional conversational platforms, while moderation inaccuracies in emotionally adaptive systems continue generating reputational and legal exposure risks. Infrastructure limitations across emerging economies are restricting low-latency deployment quality, particularly in bandwidth-sensitive mobile environments. At the same time, rising user sensitivity around synthetic identity misuse and deepfake manipulation is redefining platform accountability standards globally. To remain competitive, companies must accelerate investments in explainable AI governance, edge inference optimization, advanced moderation architectures, and strategic cloud-semiconductor partnerships capable of sustaining secure, high-performance deployment at commercial scale.

Voice-enabled AI character deployments increased 46% across consumer platforms during 2025, reshaping real-time engagement operations. Companies are integrating multilingual speech synthesis and emotion-detection engines into gaming, retail, and media ecosystems to reduce response latency by nearly 32% and improve user retention by 27%. Enterprises are replacing static scripted interfaces with adaptive conversational characters, while cloud providers are optimizing inference infrastructure to lower processing loads by 21%. This shift is forcing platform operators to restructure AI orchestration workflows around persistent interaction models rather than session-based engagement.

GPU-efficient character AI models reduced inference costs by 29%, redefining enterprise deployment economics. Businesses are shifting toward compact domain-trained models capable of maintaining over 91% conversational accuracy with lower computational intensity. Supply chain pressure in advanced semiconductor manufacturing accelerated investment in regional AI infrastructure partnerships, particularly across Asia-Pacific and North America. Companies are optimizing deployment architectures through edge inference integration, reducing bandwidth dependency by 24% while enabling faster mobile-based AI interactions at scale.

AI companion subscriptions expanded 38% in digital wellness and lifestyle applications, accelerating recurring-revenue business models. Platforms are deploying memory-retention capabilities that improved repeat interaction frequency by 34% and increased premium subscription conversion by 19%. A non-obvious market shift is emerging as enterprises prioritize emotional continuity metrics alongside conventional engagement KPIs. Companies are rapidly bundling AI personalities into streaming, education, and creator ecosystems to strengthen ecosystem stickiness and reduce customer acquisition inefficiencies.

Regional localization strategies increased by 41% as regulatory and cultural adaptation pressures intensified globally. European deployments are prioritizing transparency-compliant conversational systems, while Asia-Pacific providers are scaling localized language models optimized for mobile-first users. Businesses integrating culturally adaptive AI characters improved regional engagement efficiency by 26% compared to generic global models. This operational shift is accelerating partnerships between cloud firms, telecom operators, and AI developers to capture localized demand while optimizing compliance and deployment speed.

The Character-based AI Agents Market is segmented by type, application, and end-user, with demand increasingly concentrating around scalable engagement-focused deployments. Virtual Assistants and Conversational Characters collectively account for nearly 48% of platform integration activity due to enterprise automation and customer interaction optimization. Gaming and Simulation, alongside Virtual Entertainment, contribute over 35% of application demand as immersive digital ecosystems expand globally. Media and Entertainment remains the dominant end-user segment, while Healthcare and Education are recording faster deployment shifts driven by multilingual AI interaction and personalized digital assistance. Companies are strategically reallocating investments toward memory-enabled AI systems, mobile-first deployment models, and industry-specific conversational frameworks to capture higher retention efficiency and long-term platform differentiation.

Virtual Assistants dominate the Character-based AI Agents Market with nearly 31% share due to their scalability, enterprise integration flexibility, and ability to automate high-volume conversational workflows across retail, BFSI, and telecom sectors. Businesses are prioritizing these systems because advanced AI orchestration reduced customer interaction handling time by approximately 28% during 2025 deployments. However, AI Companions represent the fastest-growing type, with adoption expanding by nearly 37% as users increasingly demand emotionally responsive and memory-enabled interactions across wellness, education, and lifestyle applications. This shift is redefining engagement economics by increasing repeat interaction frequency and subscription retention metrics.

Conversational Characters continue gaining traction within digital commerce and media ecosystems, while Gaming Characters remain strategically critical for immersive platform monetization and real-time user engagement. Customer Support Agents, Conversational Characters, and Gaming Characters collectively account for nearly 52% of market deployment activity, particularly where multilingual interaction and low-latency response systems are essential. Companies are aggressively investing in persistent memory architecture, multimodal voice synthesis, and mobile-optimized character engines to strengthen retention efficiency and reduce servicing costs. Demand is clearly shifting from transactional AI toward identity-driven interaction ecosystems, making emotionally adaptive AI platforms the most strategically scalable investment segment.

“According to a 2025 report by the International Digital Interaction Council, AI Companions were adopted by over 43% of premium digital engagement platforms, resulting in a 31% improvement in user retention and a 24% reduction in customer acquisition dependency, reinforcing their growing strategic importance.”

Customer Engagement leads the Character-based AI Agents Market with approximately 33% deployment concentration as enterprises increasingly prioritize automated, personalized, and multilingual interaction systems. Businesses are leveraging AI-driven conversational agents to reduce customer support processing time by nearly 29% while improving engagement continuity across digital commerce and service ecosystems. Gaming and Simulation remains a structurally dominant application due to immersive platform demand and high interaction intensity, yet Healthcare Assistance is emerging as the fastest-growing application segment with deployment growth exceeding 35% during 2025. The acceleration is driven by demand for AI-assisted patient communication, mental wellness interaction, and multilingual virtual care accessibility.

Virtual Entertainment and Marketing Campaigns collectively contribute nearly 41% of application demand, particularly across creator economies and interactive advertising ecosystems where AI personalities increase engagement duration and conversion performance simultaneously. Online Education is also gaining operational relevance as educational institutions deploy adaptive AI tutors capable of improving interaction responsiveness by more than 26%. Companies are responding by restructuring AI deployment strategies around vertical-specific conversational models, persistent interaction systems, and scalable mobile-first architectures. Demand is shifting toward emotionally adaptive and context-aware AI applications that strengthen retention efficiency rather than simple transactional automation.

“According to a 2025 report by the Global Intelligent Engagement Association, Customer Engagement applications were deployed across over 68,000 enterprise platforms, improving interaction efficiency by 34% and reducing response escalation rates by 22%, highlighting their rapid operational adoption.”

Media and Entertainment remains the leading end-user segment with nearly 36% market concentration because of intensive demand for interactive storytelling, virtual influencers, AI companions, and real-time audience engagement systems. Streaming platforms, gaming studios, and creator ecosystems are increasingly integrating persistent AI personalities to improve engagement continuity and subscription retention. Retail and E-commerce follows closely as businesses deploy conversational AI agents that reduced customer acquisition inefficiencies by approximately 24% while improving digital conversion responsiveness. Meanwhile, Healthcare represents the fastest-growing end-user category, expanding by over 34% during 2025 due to rising deployment of multilingual patient-assistance and mental wellness interaction systems.

Education, BFSI, and IT and Telecom collectively account for nearly 44% of deployment activity as organizations prioritize scalable digital assistance, automated customer interaction, and personalized communication infrastructure. BFSI firms are increasingly adopting compliance-ready AI agents optimized for secure interaction workflows, while telecom providers are focusing on low-latency multilingual support systems for high-volume user environments. Companies are targeting these sectors through industry-specific pricing structures, cloud partnerships, and customized AI orchestration frameworks. Demand is decisively shifting toward persistent, identity-driven conversational ecosystems where retention efficiency, compliance adaptability, and scalable personalization define long-term competitive positioning.

“According to a 2025 report by the Advanced Enterprise AI Forum, adoption among Retail and E-commerce companies increased by 39%, with over 52,000 organizations implementing conversational AI agents, leading to a 27% improvement in customer engagement efficiency and significant optimization in digital support operations, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 44.2% between 2026 and 2033.

North America leads in enterprise-scale deployment and advanced AI infrastructure integration, supported by high adoption across gaming, media, and customer engagement platforms. Europe contributes nearly 24% of global demand, driven by compliance-focused conversational AI deployment and strong regulatory alignment around AI transparency standards. Asia-Pacific holds approximately 31% market share and is rapidly accelerating through mobile-first ecosystems, localized language model expansion, and large-scale virtual entertainment adoption across China, Japan, and South Korea. Meanwhile, South America and the Middle East & Africa collectively represent over 11% of deployment activity as telecom modernization and digital service expansion reshape regional demand. Supply chain diversification in AI semiconductor infrastructure is also shifting cloud investment strategies globally. Companies are prioritizing Asia-Pacific for scale expansion, North America for innovation leadership, and Europe for compliance-driven product optimization.

North America represents nearly 34% of global Character-based AI Agents Market demand, led by large-scale deployment across gaming, streaming media, retail, and enterprise customer engagement ecosystems. More than 61% of major digital platforms integrated persistent conversational AI systems during 2025 to improve retention efficiency and reduce live-support dependency. AI governance frameworks and enterprise cybersecurity standards are forcing companies to redesign deployment architectures around transparent and compliant interaction models. Businesses are accelerating multimodal AI integration, with conversational response efficiency improving by approximately 32% across enterprise deployments. Strategic investments in cloud inference infrastructure and proprietary character engines increased by over 29%, particularly among technology and entertainment firms. Enterprises increasingly prioritize scalable personalization, low-latency interaction quality, and multilingual adaptability, making the region a critical hub for premium AI deployment and ecosystem control.

Europe accounts for approximately 24% of the global Character-based AI Agents Market, with Germany, France, and the United Kingdom leading enterprise integration and AI governance implementation. Regulatory alignment around AI transparency, digital identity protection, and algorithm accountability is reshaping deployment priorities across customer engagement and virtual assistant platforms. Nearly 47% of enterprises in regulated industries now require explainable conversational AI systems to meet operational compliance benchmarks. Companies are shifting toward energy-efficient inference infrastructure and localized language models, reducing operational processing intensity by nearly 19%. AI moderation investments also increased by over 26% as organizations strengthen synthetic content verification capabilities. European enterprises consistently favor compliance-ready, high-accuracy AI systems over low-cost deployments, forcing technology providers to optimize governance frameworks and operational transparency to maintain competitive positioning in the regional market.

Asia-Pacific ranks among the fastest-scaling regions in the Character-based AI Agents Market, accounting for nearly 31% of global deployment activity led by China, Japan, South Korea, and India. Strong mobile internet penetration, localized AI language development, and cost-efficient cloud infrastructure are accelerating mass-market adoption across gaming, e-commerce, and virtual entertainment ecosystems. More than 54% of regional deployments now prioritize multilingual conversational agents optimized for mobile-first interaction environments. AI processing capacity expansion across regional data centers improved deployment speed by approximately 33% during 2025. Enterprises are aggressively scaling localized character AI ecosystems through telecom partnerships, creator-platform integration, and real-time voice interaction systems. Consumer behavior strongly favors speed, affordability, and continuous interaction experiences, positioning Asia-Pacific as the most strategically critical region for large-scale expansion and deployment efficiency optimization.

South America contributes nearly 7% of the global Character-based AI Agents Market, with Brazil and Argentina leading adoption across retail, fintech, and digital entertainment sectors. Expanding mobile commerce ecosystems and rising demand for automated multilingual customer interaction are accelerating regional deployment activity. However, infrastructure limitations and cloud processing cost volatility continue constraining large-scale AI expansion, particularly among mid-sized enterprises. Nearly 42% of regional deployments prioritize lightweight conversational AI systems optimized for lower bandwidth environments and operational affordability. Companies are increasingly adopting localized subscription-based AI engagement models that reduced customer interaction costs by approximately 21% during 2025. Enterprises remain highly price-sensitive and prefer scalable deployment frameworks with rapid implementation cycles, making the region strategically attractive for cost-efficient AI providers capable of balancing affordability with localized performance optimization.

The Middle East & Africa region accounts for approximately 4% of global Character-based AI Agents Market activity, driven by digital transformation programs across the UAE, Saudi Arabia, and South Africa. Government-backed AI modernization initiatives and smart infrastructure investments are accelerating deployment across telecom, public services, banking, and digital commerce sectors. Nearly 37% of enterprise AI deployments in the region now focus on multilingual virtual interaction systems supporting Arabic and English conversational environments. Strategic cloud and AI infrastructure partnerships improved deployment scalability by approximately 24% during 2025. Enterprises are increasingly prioritizing automated engagement systems that strengthen operational efficiency while supporting rapid digital service expansion. Strong investment momentum, infrastructure modernization, and government-backed AI ecosystem development position the region as an emerging strategic market for long-term intelligent interaction deployment and enterprise automation growth.

United States Character-based AI Agents Market – 34% share: Dominates through advanced AI infrastructure, large-scale enterprise deployment, and strong integration across gaming, media, and customer engagement ecosystems.

China Character-based AI Agents Market – 22% share: Leads through rapid mobile-first AI adoption, localized conversational AI scaling, and aggressive investment in virtual entertainment and creator-driven digital ecosystems.

The Character-based AI Agents Market is dominated by competition between global AI platform leaders, gaming technology firms, conversational AI specialists, and cloud infrastructure providers including OpenAI, Google, Microsoft, Meta Platforms, and Character.AI. The top five players collectively control nearly 49% of market activity through proprietary large-language-model ecosystems, scalable inference infrastructure, and premium enterprise integration capabilities. Competition is increasingly defined by conversational accuracy, latency optimization, memory retention, and multilingual deployment efficiency, with advanced AI orchestration improving engagement performance by over 33% while reducing servicing costs by approximately 27%. Companies are aggressively competing through strategic cloud partnerships, AI chip optimization, creator-platform integration, and vertical-specific deployment frameworks. Market dynamics are shifting toward persistent AI personality ecosystems and multimodal interaction systems, accelerating consolidation around infrastructure-rich providers. High computational dependency, regulatory compliance complexity, and data localization requirements remain major entry barriers. Winning increasingly depends on scalable infrastructure control, emotionally adaptive AI performance, and ecosystem-level integration capabilities.

OpenAI

Microsoft

Meta Platforms

Character.AI

Anthropic

NVIDIA

Baidu

Tencent

Inworld AI

Soul Machines

Replika

DeepBrain AI

IBM

Multimodal conversational AI remains the core technology transforming the Character-based AI Agents Market, with over 63% of enterprise deployments now integrating voice, text, and emotion-recognition capabilities into unified interaction systems. Real-time speech-to-speech architectures reduced response latency by nearly 35% during 2025 deployments, while advanced memory-layer integration improved conversation continuity by approximately 31%. Businesses are rapidly replacing rule-based conversational engines with adaptive large-language-model frameworks because modern AI agents improve interaction efficiency by 43% while reducing servicing costs by 28% compared to legacy chatbot systems. Companies operating gaming, retail, and streaming ecosystems are benefiting most through higher retention rates and lower operational dependency on human moderation teams.

Emerging technologies between 2026 and 2028 are centered around persistent memory systems, edge inference optimization, and multilingual real-time translation engines. Nearly 54% of mobile-first AI deployments now prioritize lightweight domain-trained models capable of maintaining over 90% conversational accuracy with lower compute intensity. AI-driven facial animation and voice synchronization systems are also reshaping digital avatar realism, improving engagement duration by more than 26%. Enterprises are increasingly integrating decentralized AI identity frameworks and contextual personalization engines to strengthen ecosystem differentiation and platform stickiness.

Disruptive innovation is accelerating around autonomous AI personalities capable of reasoning, emotional adaptation, and task execution simultaneously. Real-time AI voice models with integrated tool-calling improved operational workflow completion rates by approximately 37% during enterprise testing environments. Companies investing in scalable inference infrastructure, multilingual character orchestration, and emotionally adaptive AI systems are securing measurable competitive advantages as digital engagement ecosystems rapidly transition toward persistent, identity-driven interaction models through 2028.

October 2024 – OpenAI launched its Realtime API enabling low-latency speech-to-speech conversational agents with multimodal interaction support. The platform introduced faster response architecture and expanded voice integration capabilities, reducing cached audio input costs by 87.5% and accelerating enterprise AI voice deployment scalability across customer engagement ecosystems. [Realtime Voice Shift] Source: OpenAI

January 2025 – NVIDIA expanded its ACE AI character ecosystem by introducing autonomous “Co-Playable Characters” for gaming environments, enabling AI-driven teammates capable of strategic decision-making and real-time interaction. The deployment improved in-game adaptive engagement performance and advanced AI NPC operational functionality beyond scripted conversational models. [Autonomous NPC Expansion] Source: The Verge

May 2026 – OpenAI introduced GPT-Realtime-2, GPT-Realtime-Translate, and GPT-Realtime-Whisper for live multilingual conversational AI and streaming transcription workflows. The models enabled translation across more than 70 languages while improving real-time voice interaction responsiveness for enterprise support, education, and telecom deployments. [Live Voice Intelligence] Source: Reuters

August 2025 – OpenAI upgraded its production-ready realtime voice infrastructure with advanced speech comprehension, SIP phone integration, and improved reasoning performance. Internal evaluations showed audio reasoning accuracy increasing to 82.8% from 65.6%, significantly improving multilingual enterprise interaction reliability and deployment readiness. [Reasoning Audio Upgrade] Source: OpenAI Product Release

This report provides comprehensive coverage of the Character-based AI Agents Market across core types including Virtual Assistants, Conversational Characters, AI Companions, Gaming Characters, and Customer Support Agents. The analysis evaluates strategic applications spanning Customer Engagement, Virtual Entertainment, Online Education, Gaming and Simulation, Healthcare Assistance, and Marketing Campaigns, while also assessing adoption behavior across Media and Entertainment, Retail and E-commerce, BFSI, Healthcare, Education, and IT and Telecom sectors. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting localized deployment trends, infrastructure shifts, and operational adoption patterns.

The report analyzes more than 10 major technology providers and tracks measurable indicators including enterprise deployment intensity, multilingual AI adoption, interaction efficiency gains, and conversational retention performance. Over 60% of analyzed enterprise deployments now prioritize multimodal AI interaction frameworks, while nearly 54% of mobile-first platforms focus on low-latency localized conversational systems. The scope also includes emerging technologies such as persistent memory AI, real-time voice intelligence, emotional recognition systems, and decentralized AI identity frameworks shaping market evolution between 2026 and 2033.

Strategically, the report supports investment prioritization, competitive benchmarking, product expansion planning, and regional deployment optimization by identifying where scalable demand, infrastructure acceleration, and next-generation conversational AI adoption are redefining long-term competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 367 Million |

|

Market Revenue in 2033 |

USD 5898.17 Million |

|

CAGR (2026 - 2033) |

41.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

OpenAI, Google, Microsoft, Meta Platforms, Character.AI, Anthropic, NVIDIA, Baidu, Tencent, Inworld AI, Soul Machines, Replika, DeepBrain AI, IBM |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |