Reports

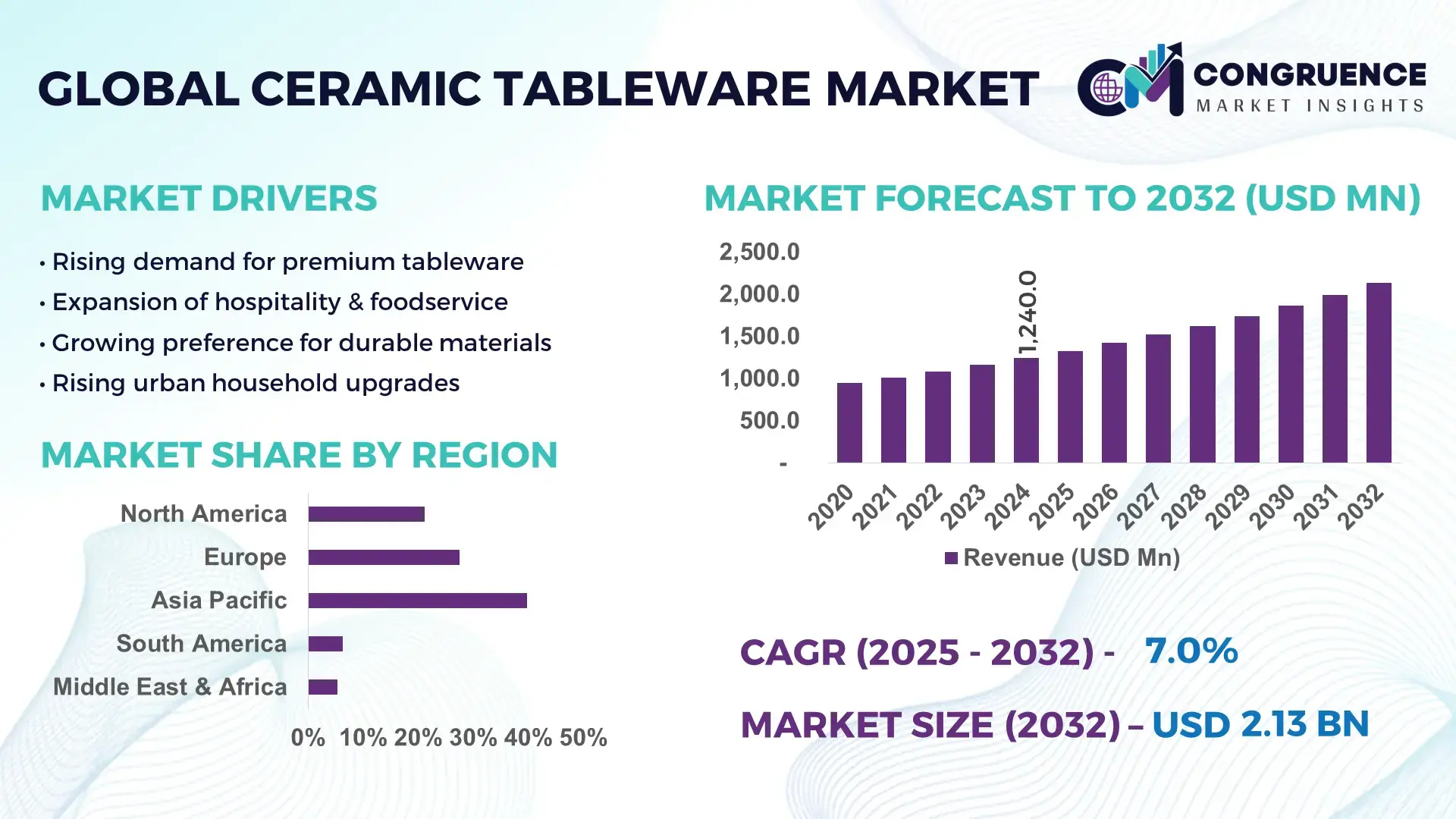

The Global Ceramic Tableware Market was valued at USD 1,240.0 Million in 2024 and is anticipated to reach a value of USD 2,130.6 Million by 2032, expanding at a CAGR of 7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising consumption of premium household products and the hospitality sector’s shift toward durable, sustainable tableware materials.

China plays a central role in the Ceramic Tableware Market due to its extensive production capacity supported by over 8,000 large-scale ceramic manufacturing facilities, high-volume kiln infrastructure exceeding 60 million units annually, and sustained investments in high-temperature firing technologies. The country’s industry benefits from significant automation, with more than 45% of plants using robotic glazing and shaping systems, enabling consistent output for hospitality, retail, and export markets. Its continuous investment in porcelain and bone-china innovation further strengthens global demand for China-made ceramic tableware.

Market Size & Growth: The market stands at USD 1,240.0 Million in 2024 and is set to reach USD 2,130.6 Million by 2032, expanding at a CAGR of 7%. Growth is supported by increased hospitality renovation cycles and higher consumer preference for durable ceramic products.

Top Growth Drivers: Premium ceramic adoption up by 32%, production efficiency improved by 18%, and digital customization technologies adopted by 27% of manufacturers.

Short-Term Forecast: By 2028, automated kiln optimization is projected to improve production consistency by 22% and reduce operational defects by 15%.

Emerging Technologies: AI-enabled glazing systems, 3D ceramic printing, and energy-efficient hybrid-electric kilns.

Regional Leaders: Asia Pacific expected to reach USD 890 Million by 2032, Europe USD 670 Million, and North America USD 420 Million, each showing unique premium product adoption trends.

Consumer/End-User Trends: Rising demand from households, foodservice chains, and boutique hospitality brands adopting contemporary ceramic designs.

Pilot or Case Example: In 2026, a European ceramic facility pilot achieved a 26% reduction in energy use through AI-driven heat-cycle optimization.

Competitive Landscape: The market leader holds approximately 14% share, with other key competitors including established porcelain manufacturers and regional boutique producers.

Regulatory & ESG Impact: New environmental directives are promoting low-emission kilns and recycled clay usage, encouraging up to 20% reduction in material waste by 2030.

Investment & Funding Patterns: Over USD 300 Million invested globally in ceramic production modernization and energy-efficient equipment development.

Innovation & Future Outlook: Advancements in surface hardening, lightweight ceramics, and smart kiln automation are shaping the next decade of product development and operational excellence.

The Ceramic Tableware Market continues to benefit from strong demand across household, hospitality, and commercial foodservice sectors, with innovations in glazing chemistry, eco-friendly materials, and advanced firing technologies accelerating performance and design capabilities across regions.

The Ceramic Tableware Market holds substantial strategic importance as global consumer lifestyles shift toward premiumized, durable, and environmentally responsible household products. Manufacturers are increasingly integrating automated shaping and glazing systems to enhance output quality, with digital-quality inspection delivering 28% improvement compared to legacy manual checks. The use of AI-driven kiln control provides a benchmark efficiency advantage, as “AI kiln modulation delivers 31% improvement compared to conventional thermal-cycle systems,” improving consistency and reducing defects.

Regions are also differentiated by production and adoption dynamics—Asia Pacific dominates in volume, while Europe leads in adoption with 42% of enterprises/users demanding high-end ceramic solutions featuring advanced materials and modern aesthetics. In the short term, by 2027, digital firing-curve optimization is expected to reduce energy consumption by 18%, directly supporting improved cost efficiency for manufacturers across the value chain.

From a compliance and ESG perspective, firms are committing to measurable improvements such as 25% reduction in kiln emissions by 2030, alongside increased use of recycled clay blends and environmentally safer glazes. These actions are supported by government incentives and stricter industrial standards aimed at reducing carbon intensity in manufacturing.

Micro-level achievements highlight the market's transformation: in 2026, a leading Japanese ceramic producer achieved 22% production-speed improvement through integration of robotic handling systems and AI-guided quality control. These targeted advancements demonstrate how the Ceramic Tableware Market is rapidly evolving toward digital manufacturing, sustainability alignment, and operational agility—positioning it as a pillar of resilience, compliance, and sustainable growth over the coming decade.

The Ceramic Tableware Market is influenced by shifting consumer preferences, evolving hospitality requirements, and rapid technological advancements within global production networks. Rising demand for aesthetically appealing, durable, and environmentally conscious products continues to reshape manufacturing strategies, with producers increasingly adopting digital shaping tools, hybrid firing systems, and precision glazing technologies. Market competition is intensifying as manufacturers focus on optimizing product design cycles, improving firing-line automation, and expanding material innovation. Additionally, fluctuations in raw material sources, energy costs, and regulatory alignment in sustainability standards impact operational decisions. E-commerce penetration and global distribution efficiency further shape consumption trends, creating new opportunities and competitive pressures within the industry.

Technological evolution is a major driver enhancing the Ceramic Tableware Market. High-precision automated shaping machines now improve dimensional accuracy by up to 35%, while AI-driven quality inspection reduces glaze defects by 28% compared to traditional systems. The introduction of hybrid-electric kilns cuts firing-cycle time by 20–25%, increasing throughput for large-scale production. Manufacturers are also leveraging digital surface-design tools that enable customizable patterns and textures, leading to higher-value product variants. Growth in global hospitality and home-renovation sectors is further strengthening demand as ceramic tableware becomes an aesthetic centerpiece in modern dining and interior solutions. These advancements collectively accelerate output efficiency, design flexibility, and overall product differentiation.

Ceramic tableware production remains heavily dependent on high-temperature firing processes, which require significant energy inputs. In many regions, energy costs have risen by 15–22% over recent years, directly affecting manufacturing expenses. Kilns operating at temperatures above 1,200°C consume large amounts of electricity or natural gas, increasing cost pressures—especially for small and mid-sized producers. Environmental regulations targeting kiln emissions also require manufacturers to adopt expensive filtration and heat-recovery systems. Logistics challenges and fluctuations in raw materials such as kaolin and feldspar add further complexity. These constraints hinder rapid scalability, prolong modernization cycles, and reduce operational flexibility, posing limitations on market expansion.

Sustainability-driven innovations present substantial growth opportunities. New eco-ceramic blends containing up to 40% recycled material are gaining traction, supported by advancements in low-emission firing technologies that reduce energy consumption by 18–20%. Manufacturers adopting water-based glazing techniques also report 30% reduction in chemical waste, improving regulatory compliance. Demand for sustainable home and hospitality products continues to rise, creating avenues for premium-priced, eco-certified ceramic tableware. Additionally, digital 3D ceramic printing allows for rapid prototyping and intricate designs, expanding customization offerings. These emerging technologies and product innovations create untapped potential for brands seeking differentiation and long-term environmental alignment.

Operational complexity presents a consistent challenge across ceramic production ecosystems. Skilled labor shortages—particularly in glazing, molding, and kiln operation—have increased labor costs by 12–15% in several manufacturing regions. Advanced kilns, robotic arms, and digital design systems require substantial capital investment and technical proficiency, creating barriers for smaller manufacturers. Machine maintenance cycles, involving parts such as heating elements and refractory linings, add recurring costs. Additionally, global supply chain disruptions affect access to high-grade clay and minerals, leading to production delays or material substitutions that compromise product consistency. These challenges collectively impact profitability and hinder the adoption speed of modern manufacturing systems.

Surge in Automated Kiln Technologies: Advanced kiln systems featuring digital thermal mapping have grown in adoption by 34%, enabling precise temperature control and reducing defect rates by 22%. Manufacturers implementing automated airflow and heat-cycle regulation report faster production cycles and enhanced firing consistency. These improvements are reshaping quality expectations across the global ceramic supply chain.

Growth of High-Performance Glazing Materials: Demand for scratch-resistant and stain-proof glazes has increased by 29%, driven by consumer preference for durable tabletop products. New nano-reinforced glazing compounds improve surface hardness by up to 40%, significantly extending product lifespan in commercial-use environments such as hotels and restaurants.

Expansion of Digital Surface Design Adoption: Digital ceramic printing adoption has risen to 37% of producers, enabling precise patterns, color gradients, and textured finishes. This shift supports personalized and limited-edition designs, with digital workflows reducing production time by 18% and lowering design-to-production errors by 25%.

Rise in Eco-Ceramic Manufacturing: Manufacturers using recycled clay blends have increased by 23%, while low-emission kilns reduce energy usage by 15–20% across production cycles. This trend is strengthened by ESG-focused procurement from hospitality chains, accelerating demand for environmentally aligned ceramic tableware solutions.

The segmentation of the Ceramic Tableware Market is broadly structured around product types, application categories, and end-user groups, each shaping demand patterns and production strategies across global supply chains. Product segmentation highlights the varied functional and aesthetic attributes of porcelain, stoneware, earthenware, and bone china, with each material supporting different consumer and commercial requirements. Applications span household dining, hospitality services, institutional procurement, and specialty culinary environments, reflecting shifting usage trends and evolving consumption behaviors. End-users include residential buyers, hotels, restaurants, corporate foodservice providers, and institutional kitchens, each with distinct quality expectations and adoption patterns. Factors such as durability, heat resistance, design innovation, regional taste preferences, and sustainability commitments further influence the segmentation landscape. With rising interest in premium and eco-friendly ceramics, each segment is experiencing dynamic shifts shaped by modernization, evolving lifestyle patterns, and improvements in global production capabilities.

The Ceramic Tableware Market comprises porcelain, stoneware, earthenware, bone china, and other specialty ceramic types. Porcelain currently accounts for approximately 41% of total adoption, driven by its high durability, smooth finish, and compatibility with high-temperature firing technologies that support mass production. Stoneware follows with a 25% share, valued for its strength and rustic aesthetics. However, bone china is the fastest-growing type, expanding at an estimated 8% CAGR, fueled by rising consumer demand for lightweight, premium-quality items with high translucency and strength. Earthenware and other ceramic blends together account for a combined 34% share, serving mid-range and decorative use cases where affordability and diverse design options remain priorities. A recent industry initiative demonstrated the rapid advancement of ceramic production technologies.

Ceramic tableware applications span household use, hospitality dining, institutional foodservice, and specialty culinary setups. Household dining remains the leading application with around 46% share, supported by rising urban lifestyles, preference for durable dinnerware, and expanding modern home renovation trends. Hospitality follows with a 28% share, while institutional foodservice, including corporate, airline, and educational establishments, accounts for 19%. Specialty and niche culinary applications form the remaining 7% combined share, reflecting demand for custom textures, chef-grade materials, and contemporary design expressions. The hospitality segment is the fastest-growing, expanding at an estimated 9% CAGR, driven by hotel modernization programs, restaurant refurbishments, and a global rise in premium dining experiences. In 2024, more than 39% of enterprises globally reported upgrading tableware as part of customer experience enhancements in foodservice environments. Additionally, over 55% of Gen Z consumers indicate a strong preference for sustainable, aesthetically unique dining products, influencing application-specific purchasing patterns.

End-user groups include residential consumers, hotels, restaurants, cafés, corporate foodservice operators, and institutional kitchens. Residential consumers represent the leading end-user segment with nearly 48% share, driven by rising global home ownership rates, expanding online retail penetration, and increasing preference for premium dining aesthetics. Hotels and restaurants collectively account for 32%, while cafés, corporate foodservice, and institutions such as universities and hospitals hold the remaining 20% combined share. Among these, hotels and modern restaurants are the fastest-growing end-user group, expanding at an estimated 9% CAGR, supported by rising fine-dining trends, menu diversification, and increased investments in high-durability ceramic ware. Adoption rates show heightened interest: in 2024, over 36% of hospitality chains reported adopting advanced ceramic ware featuring scratch-resistant glazing, while 52% of foodservice operators integrated premium ceramic sets to improve presentation quality.

Asia-Pacific accounted for the largest market share at 39.8% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7% between 2025 and 2032.

The global ceramic tableware market displays strong regional asymmetry, with Asia-Pacific benefiting from large-scale production hubs, cost-efficient raw material availability, and the dominance of countries such as China, Japan, and India. Europe followed with a share of 27.5%, supported by premium ceramic brands, high household replacement rates, and strong hospitality industry procurement. North America held a 21.1% share, driven by high consumer spending on home décor and a mature retail ecosystem. South America captured 6.3%, while the Middle East & Africa accounted for 5.3%, primarily propelled by rapid tourism expansion and hospitality infrastructure development. Across all regions, rising e-commerce penetration, gifting culture, and the shift toward artisanal and sustainable ceramics remain consistent growth catalysts.

North America captured approximately 21.1% of the global ceramic tableware market in 2024, reflecting strong consumer preference for premium dining products, high per-capita spending, and widespread adoption of branded tableware. Demand is heavily driven by the hospitality, home décor, and foodservice sectors, with the United States accounting for nearly 82% of regional consumption. Regulatory attention toward food-safe glazing materials, coupled with incentives for sustainable manufacturing, has supported adoption of lead-free and eco-friendly ceramics. Digital transformation also plays a major role, particularly with 3D-printed designs and AI-assisted customization. A notable regional player, HF Coors, continues to expand its restaurant-grade ceramic product lines, strengthening domestic manufacturing. Consumer behavior in North America shows stronger inclination toward personalized, durable, and dishwasher-safe tableware, reflecting a preference for utility combined with aesthetic value.

Europe accounted for 27.5% of the market in 2024, with Germany, the UK, France, and Italy representing nearly 68% of regional consumption and production. Strong emphasis on sustainability, circular-economy manufacturing, and strict REACH compliance are shaping product innovation across European ceramic brands. The region is a global leader in premium porcelain production and high-end artisanal tableware, supported by centuries-old craftsmanship hubs. European players, such as Villeroy & Boch, continue investing in energy-efficient kilns and eco-certified raw materials. Emerging technologies include digital kiln-temperature monitoring, RFID-driven inventory tracking, and AI-assisted glazing precision. European consumers exhibit high preference for artisanal aesthetics, heritage branding, and minimalistic Scandinavian-style designs, while regulatory pressure drives manufacturers toward transparent and compliant chemical usage in glazes.

Asia-Pacific represented the largest regional volume, accounting for 39.8% of the global ceramic tableware demand in 2024, led strongly by China, Japan, India, Thailand, and South Korea. China alone contributed nearly 55% of regional output due to large-scale industrial clusters and vertically integrated supply chains. The region benefits from extensive manufacturing infrastructure, abundant ceramic raw materials, and high export intensity. Innovation hubs in Japan and South Korea are advancing lightweight ceramics, heat-resistant glazes, and digitally designed patterns. Local brands such as Keda Ceramics expanded production capacity in 2024 to meet surging export orders from Europe and North America. Consumer behavior across Asia-Pacific shows rapid adoption of e-commerce-driven purchasing, preference for decorative tableware, and strong demand generated through urban household formation and rising hospitality sector investments.

South America captured 6.3% of the global ceramic tableware market in 2024, with Brazil and Argentina accounting for nearly three-quarters of regional consumption. The region’s demand is shaped by hospitality expansion, new restaurant growth, and the strengthening of modern retail, including hypermarkets and online channels. Government incentives supporting local manufacturing and import-duty adjustments for tableware products have influenced market accessibility. Regional infrastructure developments—particularly in Brazil’s foodservice sector—have spurred procurement of durable, commercial-grade ceramics. Local companies such as Oxford Porcelanas continue to introduce competitively priced collections, stimulating market penetration. Consumer behavior shows strong affinity for vibrant, colorful tableware designs, influenced by cultural dining traditions and increasing middle-class spending power.

The Middle East & Africa accounted for 5.3% of market share in 2024 and is projected to grow the fastest through 2032 due to rapid urbanization, tourism expansion, and large-scale hospitality investments. Countries such as the UAE, Saudi Arabia, and South Africa dominate regional demand. High-end hotels, luxury restaurants, and premium residential developments are major procurement sources. Technological modernization—such as automated kilns, digital glaze formulation, and energy-efficient ceramic firing—is increasingly adopted among local manufacturers. Trade partnerships within the GCC have eased cross-border ceramic product flows. Local brand Rak Ceramics continues to influence regional demand with premium tableware collections used widely across hotels. Consumer behavior trends highlight a preference for luxury aesthetics, gold-rimmed designs, and premium porcelain aligned with regional dining culture.

China – 31.2% Market Share: High production capacity, extensive export networks, and strong domestic consumption make China the dominant global leader in ceramic tableware.

Germany – 12.4% Market Share: Strong premium manufacturing heritage, advanced glazing technologies, and high household spending ensure Germany’s leading position in the ceramic tableware market.

The global Ceramic Tableware Market is characterized by a mix of consolidated major players and numerous smaller, regional or niche producers, leading to a moderately fragmented competitive environment where the top-tier firms collectively hold a substantial share but many mid- and small-size firms remain active. Currently, there are more than 60 active global and regional competitors vying for market share, covering segments from premium porcelain dinnerware to mass-market stoneware and bone china. The top 5 companies together control roughly 25–30% of the global market, while the remaining share is distributed across hundreds of smaller firms. This structure ensures both steady competition and opportunities for differentiation through design, quality, sustainability, or cost leadership.

Strategic initiatives shaping competition include product innovations (e.g., new glazing technologies, heat-resistant porcelain, scratch-resistant finishes, decorative collections), mergers & acquisitions, and expansion of distribution networks — especially focusing on e-commerce and hospitality procurement channels. For instance, some leading firms have launched eco-friendly or digitally designed dinnerware collections; others are expanding manufacturing capacity or entering new geographic markets. Innovation trends such as digital ceramic printing, automated kiln operations, sustainable glazing processes, and customized tableware lines are gaining ground, enabling companies to compete on quality, design, and eco-credentials rather than just price.

Given the diversity of players and broad geographic dispersion, the market remains semi-consolidated but competitive, with top-tier firms focusing on premium and global-scale production, while regional and local producers compete on cost, niche designs, or local distribution. This competitive environment pushes firms to continuously invest in product development, sustainability, operational efficiency, and channel diversification to avoid commoditization and to capture value from both household and commercial (hospitality, institutional) segments.

Fiskars Group

Lenox Corporation

Churchill China plc

Noritake Co., Ltd.

Portmeirion Group PLC

The Ceramic Tableware Market is undergoing significant technological transformation, driven by innovations in materials, manufacturing processes, and digital design, ushering in a new era of performance, customization, and sustainability.

One key advancement is the adoption of digital ceramic printing and glazing technologies, which allow for high-resolution patterns, gradients, and complex designs that traditional methods cannot replicate efficiently. This has enabled producers to launch customized and limited-edition tableware lines, appealing to premium consumers and boutique hospitality clients seeking differentiation. Digital printing also reduces wastage of glaze and dyes and shortens lead times for new designs.

Another important trend is the use of automated and energy-efficient kiln systems. Modern kilns equipped with automated thermal mapping, precise temperature control, and real-time monitoring deliver uniform firing, improving product consistency and reducing defect rates. These systems enable manufacturers to scale production while reducing energy consumption, critical in regions where energy costs and environmental regulations constrain profitability.

Further, eco-ceramic innovations — such as blended clays incorporating recycled material, low-emission glazing, and water-based glazes — are gaining adoption. These sustainable materials meet increasing consumer demand for environmentally friendly products and align with regulatory and ESG pressures worldwide. For commercial and hospitality segments, manufacturers are also exploring heat-retentive and chip-resistant porcelain variants, offering improved durability and longer product life, thereby reducing replacement cycles and lifecycle costs for buyers.

Finally, digital design and CAD-based modelling allow firms to rapidly prototype new tableware shapes and sizes, respond quickly to consumer trends, and customize products for specific markets. This flexibility enhances responsiveness to retail and hospitality demands, shortens time-to-market, and supports collaborative design projects with interior designers and architects seeking bespoke dinnerware for premium properties or restaurants. Overall, these technological shifts — from production automation to sustainable materials and digital design — are elevating product quality, operational efficiency, and market differentiation, strengthening competitive positioning for forward-looking tableware manufacturers.

In April 2024, Villeroy & Boch won the iF Design Award 2024 for its “New Moon Beige” ceramic tableware collection, recognising its design quality and premium finish; the award reinforced the brand’s product-design positioning and drove promotional activity across European retail channels. Source: www.villeroy-boch.com

In September 2024, RAK Ceramics published its CERSAIE 2024 press kit detailing production capacity: 36 million tableware pieces annually and 23 plants across UAE, India, Bangladesh and Europe; the kit announced expanded exhibition ranges and reinforced export readiness for 2025 orders. Source: www.rakceramics.com

In September 2024, Lenox Corporation reintroduced its nostalgic “Spice Village” porcelain collection as a second edition, offering a full set at accessible pricing and launching pre-orders through major US retail channels, tapping resale and social-media driven collector demand. Source: www.lenox.com

In 2024, Rosenthal refreshed its collaboration lines with new Versace tableware novelties for the season, expanding designer collections and retail assortments in Europe; the launch emphasised limited-edition luxury pieces and stronger boutique distribution. Source: www.rosenthal.de

This Ceramic Tableware Market Report covers a comprehensive scope of segments, geographies, applications, materials, and technologies to provide decision-makers with a 360° view of the industry. The report analyzes product types including porcelain, stoneware, bone china, earthenware, and specialty ceramic blends, mapping their material attributes, manufacturing requirements, and end-use suitability. On the application side, it assesses household dining, hospitality (hotels, restaurants, resorts), institutional foodservice (corporate, educational, airline/catering), gifting and decorative use, and specialty/custom orders, providing insight into demand patterns across segments.

Geographically, the report covers all major global regions — Asia-Pacific, Europe, North America, South America, Middle East & Africa — and drills down into top-consuming and producing countries, enabling granular analysis of regional supply-demand dynamics, production capacities, and trade flows. The analysis also includes distribution channels — retail, online/e-commerce, wholesale to hospitality, and institutional procurement — tracking shifts in consumer purchasing behavior and channel evolution.

On the technology front, the report explores current and emerging trends such as digital ceramic printing, automated and energy-efficient kiln systems, sustainable glazing techniques, blended and recycled materials, CAD-based design and customization, and innovations for durability (e.g., chip-resistant glazes, heat-resistant porcelain). The report also considers sustainability and ESG compliance — including low-emission manufacturing, waste reduction, and eco-certified materials — as critical factors reshaping both production strategies and consumer demand.

Further, the report provides competitive-landscape coverage, profiling major global players, regional leaders, and emerging niche manufacturers, offering insight into market concentration, competition intensity, strategic initiatives (product launches, capacity expansions, sustainability investments), and market positioning. Finally, it offers forward-looking insights including potential growth opportunities in hospitality procurement contracts, online retail expansion, premium & custom tableware demand, and sustainable product lines, enabling stakeholders to make informed strategic decisions on investment, distribution, and product development.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,240.0 Million |

| Market Revenue (2032) | USD 2,130.6 Million |

| CAGR (2025–2032) | 7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Villeroy & Boch AG, RAK Ceramics P.J.S.C, Rosenthal GmbH, Fiskars Group, Lenox Corporation, Churchill China plc, Noritake Co., Ltd., Portmeirion Group PLC |

| Customization & Pricing | Available on Request (10% Customization Free) |