Reports

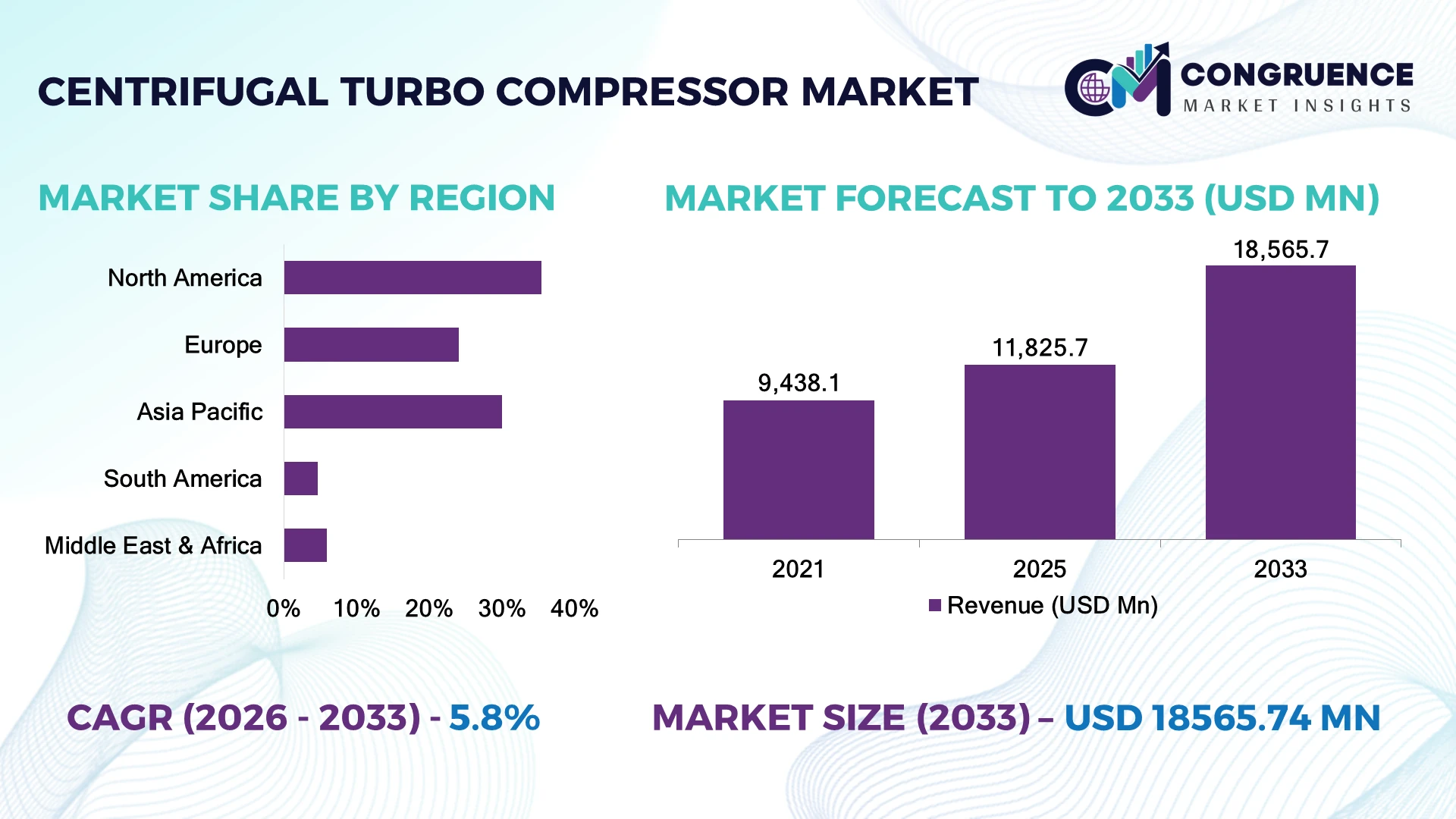

The Global Centrifugal Turbo Compressor Market was valued at USD 11,825.7 Million in 2025 and is anticipated to reach a value of USD 18,565.7 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033. Growth is being driven by LNG infrastructure expansion, industrial decarbonization projects, and increasing deployment of high-efficiency compression systems across hydrogen, petrochemical, and natural gas processing facilities.

The United States accounts for approximately 27% of global centrifugal turbo compressor demand, supported by LNG export expansion, petrochemical capacity additions, and large-scale pipeline infrastructure. Compared with Germany's process-industry-driven installations, the U.S. deploys nearly 2.3 times more high-capacity compressors in oil & gas and LNG applications. Following global energy security priorities after the Russia-Ukraine conflict, demand for digitally monitored compression systems has increased by approximately 19%, strengthening investment in high-efficiency industrial assets.

Manufacturers investing in digital diagnostics, low-emission compressor technologies, and localized production capabilities will strengthen operational competitiveness and long-term market leadership.

Market Size & Growth: USD 11,825.7 Million in 2025, projected to reach USD 18,565.7 Million by 2033 at a CAGR of 5.8%, driven by LNG infrastructure and industrial modernization.

Top Growth Drivers: LNG expansion (39%), hydrogen projects (33%), and petrochemical investments (31%) continue accelerating demand.

Short-Term Forecast: By 2028, advanced compressor systems are expected to improve energy efficiency by nearly 11%.

Emerging Technologies: Digital twins, AI predictive maintenance, and magnetic bearing technology enhance compressor performance.

Regional Leaders: North America exceeds USD 4.4 Billion, Asia-Pacific approaches USD 4.2 Billion, and Europe surpasses USD 3.5 Billion through industrial investments.

Consumer/End-User Trends: Nearly 59% of industrial buyers prioritize energy-efficient turbo compressors with digital monitoring.

Pilot/Case Example: A 2026 LNG facility upgrade reduced compressor energy consumption by approximately 13%.

Competitive Landscape: The leading supplier holds nearly 18% market share alongside Baker Hughes, Siemens Energy, Atlas Copco, and MAN Energy Solutions.

Regulatory & ESG Impact: High-efficiency compressors lower electricity consumption by over 15% in continuous-duty operations.

Investment & Funding: More than USD 12 Billion supports LNG terminals, hydrogen facilities, and compressor modernization projects.

Innovation & Future Outlook: Variable-speed drives, hydrogen-ready compressors, and AI-based asset optimization are redefining industrial compression.

Centrifugal Turbo Compressor Market demand remains concentrated in LNG facilities, refineries, petrochemical plants, chemical processing, and industrial gas production. Magnetic bearing technology, variable-speed drives, and AI-enabled condition monitoring are improving equipment reliability and reducing lifecycle operating costs. Approximately 48% of newly specified industrial compressor packages now include predictive diagnostics, supported by increasing operational efficiency targets and emissions reduction initiatives, setting the foundation for the strategic market assessment.

Centrifugal turbo compressors have become strategically important as industrial operators seek higher process efficiency, lower energy consumption, and greater operational reliability across LNG, hydrogen, petrochemical, and gas processing facilities. Industrial decarbonization initiatives, expanding LNG infrastructure, and modernization of continuous-process industries are accelerating investment in advanced compression technologies with digital monitoring and predictive maintenance capabilities.

Modern integrally geared centrifugal compressors improve energy efficiency by approximately 10% compared with conventional fixed-speed systems while reducing maintenance interventions by nearly 18% through intelligent diagnostics and optimized rotor dynamics. North America leads deployment through LNG expansion and pipeline modernization, whereas Asia-Pacific continues scaling installations to support petrochemical production, industrial manufacturing, and hydrogen infrastructure. Over the next two to three years, magnetic bearing systems, AI-assisted performance optimization, and variable-speed drive integration are expected to become standard procurement requirements across high-capacity industrial installations.

Industrial operators are increasingly replacing aging compression assets with digitally connected equipment integrated into plant-wide automation platforms. Manufacturers are expanding localized production, strengthening aftermarket service networks, and investing in hydrogen-compatible compressor technologies through strategic partnerships. Organizations combining energy-efficient engineering, advanced digital lifecycle management, and application-specific customization will secure stronger competitive positioning while supporting long-term industrial productivity and sustainability objectives.

Global LNG infrastructure expansion and industrial decarbonization are accelerating deployment of advanced centrifugal turbo compressors across gas processing, petrochemicals, hydrogen, and industrial gas facilities. Approximately 62% of newly commissioned LNG terminals specify high-efficiency centrifugal compression systems, while variable-speed compressor technology reduces energy consumption by nearly 12%. The United States continues expanding LNG export capacity, increasing demand for high-throughput compression equipment with digital monitoring capabilities. This structural shift improves operational reliability, lowers lifecycle costs, and strengthens plant efficiency. Manufacturers are responding by expanding localized production, integrating AI-based predictive maintenance, and forming engineering partnerships to develop hydrogen-ready compressor platforms. Companies combining energy efficiency with digital lifecycle services are securing stronger positions in high-value industrial projects.

Advanced centrifugal turbo compressors rely on precision-machined impellers, magnetic bearings, specialty alloys, and sophisticated control systems that remain exposed to supply-chain disruptions and material price volatility. Critical alloy costs have fluctuated by approximately 14%, while procurement lead times for selected rotating components have extended by nearly 20% in recent procurement cycles. Germany and Italy continue facing skilled manufacturing constraints for high-performance compressor assemblies, affecting delivery schedules and project execution. These pressures increase capital costs, reduce installation flexibility, and compress supplier margins. Manufacturers are mitigating risks through supplier diversification, regional manufacturing investments, long-term procurement contracts, and increased localization of high-value components to improve supply resilience and operational continuity.

Hydrogen production, carbon capture, and industrial electrification are opening high-value opportunities for next-generation centrifugal turbo compressors designed for demanding process environments. Hydrogen-related industrial projects are expected to represent approximately 18% of new large-scale compressor procurement over the next few years, while digitally optimized compression systems improve operating efficiency by nearly 10%. Japan and South Korea continue expanding hydrogen infrastructure, creating demand for specialized compression technologies with enhanced sealing and process control. Manufacturers are investing in R&D, advanced aerodynamic designs, and magnetic bearing platforms while partnering with EPC contractors to strengthen project participation. Early development of hydrogen-compatible compressor portfolios provides a significant competitive advantage as industrial energy systems diversify.

Deploying modern centrifugal turbo compressors increasingly requires seamless integration with plant automation, digital twins, predictive analytics, and industrial cybersecurity platforms. Nearly 47% of large industrial facilities now require compressor compatibility with enterprise-wide digital asset management systems, while commissioning periods may extend by approximately 15% when integrating legacy control architectures. Industrial operators in China and the Middle East are expanding smart manufacturing facilities that demand interoperable compression solutions with high operational reliability. Companies must strengthen software engineering capabilities, workforce training, cybersecurity architecture, and lifecycle support to ensure consistent performance. Organizations capable of delivering fully integrated mechanical and digital solutions will sustain long-term competitiveness across complex industrial environments.

Digital Compressor Intelligence AI-enabled monitoring platforms are now integrated into nearly 58% of newly installed centrifugal turbo compressors, reducing unexpected downtime by approximately 18% while improving maintenance planning. Industrial operators increasingly connect compressors to enterprise asset management platforms, prompting manufacturers to expand digital service offerings, remote diagnostics, and predictive maintenance partnerships for higher equipment availability.

Hydrogen-Ready Compression Systems Growing hydrogen infrastructure investments are accelerating deployment of compressors designed for low-carbon industrial applications. Approximately 24% of newly developed industrial compressor platforms now incorporate hydrogen-compatible sealing technologies and advanced materials. Manufacturers are restructuring product portfolios and expanding engineering collaborations to meet evolving industrial decarbonization requirements while improving long-term equipment flexibility.

Magnetic Bearing Adoption Oil-free magnetic bearing technology is improving compressor efficiency by nearly 9% while reducing maintenance frequency by approximately 22% in continuous industrial operations. Process industries increasingly prioritize these systems to lower lifecycle operating costs and improve reliability. Equipment suppliers continue scaling production and expanding application-specific engineering to strengthen competitiveness in premium industrial segments.

Localized Manufacturing Strategies Supply-chain resilience has become a strategic priority as manufacturers regionalize production of critical compressor components. Local sourcing programs have shortened delivery cycles by approximately 17% and reduced logistics exposure during global trade disruptions. Companies are expanding regional manufacturing facilities, strengthening supplier partnerships, and increasing inventory flexibility to improve execution speed for large industrial infrastructure projects.

Multi-stage centrifugal turbo compressors account for approximately 49% of the global market owing to their ability to deliver high-pressure ratios, continuous operation, and superior efficiency across LNG, refinery, petrochemical, and industrial gas facilities. Their scalability for large process plants and compatibility with advanced digital monitoring systems make them the preferred choice for mission-critical operations. Single-stage compressors remain well established in medium-pressure industrial applications because of their lower installation cost and simplified maintenance requirements.

Integrally geared centrifugal compressors represent the fastest-growing segment, supported by increasing demand for energy-efficient compressed air and industrial gas systems. Their compact footprint and efficiency improvements of nearly 10% over conventional designs are accelerating adoption across chemical processing and manufacturing facilities. Axially split centrifugal compressors continue serving large power generation and pipeline applications where high flow capacity is essential. Manufacturers are expanding integrally geared product portfolios, investing in advanced impeller technologies, and strengthening application-specific engineering to capture evolving industrial demand, shifting investment priorities toward high-efficiency compression platforms.

According to findings published by the U.S. Department of Energy in 2025, advanced multi-stage centrifugal compression systems deployed in continuous industrial processes can reduce electricity consumption by approximately 10–15% through optimized aerodynamic design and variable-speed operation.

Oil & Gas represents the largest application segment with approximately 41% of global demand, supported by extensive deployment across LNG terminals, natural gas transmission, offshore production, gas processing, and refinery operations. High operating reliability, continuous-duty capability, and process efficiency keep centrifugal turbo compressors indispensable for large hydrocarbon infrastructure. Petrochemical & Chemical Processing remains another mature segment, while Industrial Gas production continues expanding steadily through oxygen, nitrogen, and hydrogen processing facilities.

Hydrogen and Industrial Gas applications are emerging as the fastest-growing segment as energy transition investments reshape industrial infrastructure. Approximately 27% of recently specified compressor packages now incorporate hydrogen-ready features or advanced sealing technologies. Power Generation continues adopting high-capacity compressors for combined-cycle and carbon capture facilities, while industrial manufacturing increasingly integrates digitally optimized compression systems to reduce operating costs. Equipment suppliers are scaling automation capabilities, strengthening EPC partnerships, and expanding modular compressor packages to address evolving operational requirements across multiple industries.

A 2026 enterprise survey conducted by the Gas Machinery Research Council indicated that energy efficiency and lifecycle operating cost ranked among the top procurement priorities for more than 70% of industrial compressor users evaluating new centrifugal compression systems.

Oil & Gas Companies remain the largest end-user segment, accounting for approximately 43% of market demand due to continuous investment in LNG production, gas gathering, pipeline transportation, and refining infrastructure. Their large-scale operations require highly reliable centrifugal turbo compressors capable of continuous operation under demanding process conditions. Chemical & Petrochemical Companies continue representing a substantial share through process compression applications, while Industrial Gas Producers strengthen demand through expanding hydrogen and specialty gas production capacity.

Power Utilities represent the fastest-growing end-user category as flexible gas-fired generation, carbon capture projects, and hydrogen-ready facilities expand worldwide. Nearly 35% of newly planned thermal power projects specify advanced compression technologies with digital monitoring capabilities. Industrial Manufacturing companies continue increasing investments in energy-efficient compressor systems for steel, fertilizer, cement, and process industries. Manufacturers are responding through customized engineering, long-term service agreements, localized support networks, and predictive maintenance solutions to improve lifecycle value and strengthen competitive differentiation.

According to a 2025 industrial equipment survey by the International Energy Agency, digital condition monitoring has been incorporated into more than 60% of newly commissioned large industrial rotating equipment projects, reflecting the growing emphasis on predictive maintenance and operational reliability.

North America accounted for the largest market share at 35.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Digital Compression and LNG Expansion Strengthen Market Leadership

North America leads the Centrifugal Turbo Compressor Market through expanding LNG export terminals, natural gas pipeline modernization, petrochemical investments, and advanced industrial automation. The region contributes approximately 35.4% of global demand, supported by extensive deployment across gas processing, refining, industrial gases, and power generation. More than 63% of newly commissioned LNG facilities integrate digitally monitored centrifugal turbo compressors with predictive maintenance capabilities, improving operational availability and reducing maintenance interruptions. Compressor manufacturers continue strengthening regional engineering centers, aftermarket services, and localized assembly operations while collaborating with EPC contractors on large infrastructure projects. AI-enabled asset monitoring and variable-speed drive adoption continue improving plant efficiency, making North America the benchmark for high-performance industrial compression technologies.

United States Market Outlook: The United States dominates regional demand through large-scale LNG exports, expanding natural gas infrastructure, and one of the world's largest petrochemical manufacturing bases. Industrial operators increasingly procure high-capacity compressors equipped with digital diagnostics and remote monitoring platforms. More than 45% of recently sanctioned LNG expansion projects include next-generation centrifugal compression systems designed to improve operational flexibility, energy efficiency, and long-term asset reliability.

Energy Transition Accelerates Efficient Industrial Compression

Europe continues modernizing industrial compression infrastructure through decarbonization initiatives, hydrogen development, and process efficiency upgrades. The region accounts for approximately 25% of global market demand, driven by chemical manufacturing, industrial gases, and refinery modernization. Nearly 58% of newly specified compressor packages emphasize energy-efficient operation and low-emission process integration. Manufacturers are investing in magnetic bearing technology, advanced impeller designs, and digital asset management while strengthening engineering partnerships to support industrial sustainability objectives and operational optimization.

Germany Market Outlook: Germany remains the region's largest market owing to its advanced manufacturing ecosystem, strong chemical industry, and leadership in industrial automation. Process industries continue replacing legacy compression systems with digitally integrated equipment capable of supporting hydrogen production and energy-efficient manufacturing. Domestic engineering expertise and precision manufacturing capabilities reinforce Germany's position as a key innovation hub for centrifugal turbo compressor technologies.

Industrial Scale and Manufacturing Investment Drive Expansion

Asia-Pacific represents the fastest-growing regional market as industrialization, LNG infrastructure, semiconductor manufacturing, and petrochemical capacity continue expanding. The region contributes approximately 30% of global demand, with China, India, Japan, and South Korea driving large-scale compressor deployment. Around 61% of newly constructed petrochemical complexes utilize advanced centrifugal turbo compressors featuring automated process control and high-efficiency aerodynamic designs. Equipment manufacturers continue expanding localized manufacturing, engineering support, and regional supply chains to improve delivery performance and support rapidly increasing industrial demand.

China Market Outlook: China leads regional deployment through continuous investment in refining, petrochemicals, LNG terminals, industrial gases, and hydrogen infrastructure. Large manufacturing clusters increasingly specify high-efficiency centrifugal compressors integrated with smart factory platforms. Local production capabilities and expanding domestic component manufacturing strengthen project execution while reducing dependence on imported industrial equipment.

Natural Gas Infrastructure Supports Market Development

South America continues expanding centrifugal turbo compressor deployment through natural gas infrastructure investments, refinery upgrades, mining operations, and industrial modernization. The region contributes approximately 4.7% of global market demand, supported by growing pipeline networks and increasing industrial gas production. Modern compressor installations improve energy efficiency by approximately 9% while supporting continuous process operations across energy-intensive industries. Manufacturers are strengthening regional service capabilities, maintenance partnerships, and localized technical support despite financing constraints affecting large infrastructure developments.

Brazil Market Outlook: Brazil represents the largest regional market through expanding offshore oil and gas production, refinery modernization, and growing natural gas utilization. Industrial operators increasingly deploy advanced centrifugal compression systems to improve operational reliability across upstream and downstream facilities. LNG investments and industrial diversification continue creating opportunities for high-capacity compressor manufacturers and engineering service providers.

Hydrocarbon Investments Sustain High-Capacity Deployment

The Middle East & Africa market remains strategically important because of ongoing investments in upstream oil & gas, LNG facilities, petrochemical expansion, and industrial diversification. The region accounts for approximately 15% of global market demand, with more than 60% of major hydrocarbon developments specifying advanced centrifugal turbo compressors for continuous-duty operations. Suppliers continue expanding regional service centers, localized maintenance capabilities, and engineering partnerships to improve lifecycle support and operational efficiency across large energy projects.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through major petrochemical investments, natural gas processing projects, and industrial diversification initiatives. National infrastructure programs continue deploying high-capacity centrifugal turbo compressors for gas gathering, hydrogen development, and refinery modernization. Increasing localization of industrial manufacturing and long-term equipment service agreements further strengthen the country's position as a strategic market for advanced industrial compression technologies.

Competition is led by Atlas Copco, Baker Hughes, Siemens Energy, MAN Energy Solutions, and Elliott Group, with global OEMs competing against specialized process-compressor manufacturers, while regional engineering firms challenge through faster delivery and localized service. The top five companies collectively control approximately 69% of the global market. Competition centers on compressor efficiency, lifecycle reliability, digital diagnostics, and aftermarket capabilities rather than equipment pricing alone. Advanced aerodynamic designs improve energy efficiency by nearly 11%, predictive maintenance reduces unplanned downtime by approximately 18%, and localized manufacturing shortens project delivery by almost 16%. Market leaders continue expanding service centers, investing in hydrogen-compatible compressor technologies, forming EPC partnerships, and integrating digital asset management into lifecycle contracts. Competitive momentum is shifting toward AI-enabled monitoring, magnetic bearing systems, and flexible compression solutions for hydrogen and LNG applications. High engineering complexity, stringent API compliance, and precision manufacturing requirements remain major entry barriers. Long-term success depends on technological differentiation, lifecycle support, operational efficiency, and execution reliability.

Atlas Copco AB

Baker Hughes Company

Siemens Energy AG

Elliott Group

MAN Energy Solutions

Ingersoll Rand Inc.

Mitsubishi Heavy Industries, Ltd.

Sulzer Ltd.

Kawasaki Heavy Industries, Ltd.

Howden Group

Kobelco Compressors Corporation

FS-Elliott Co., LLC

Sundyne LLC

Digitalization is transforming centrifugal turbo compressor performance through AI-enabled predictive maintenance, digital twins, magnetic bearing technology, and variable-speed drives. Approximately 60% of newly specified industrial compressors now incorporate intelligent monitoring systems capable of continuously optimizing performance. Predictive analytics reduce maintenance costs by nearly 15%, while advanced aerodynamic impeller designs improve operating efficiency by approximately 9%. These technologies enable higher equipment availability, lower lifecycle costs, and more accurate operational planning across LNG, petrochemical, industrial gas, and hydrogen facilities.

Compared with conventional oil-lubricated compressors, magnetic bearing centrifugal compressors reduce mechanical losses by approximately 12% while lowering maintenance requirements by nearly 20% through oil-free operation and reduced component wear. Companies adopting digitally connected compressor platforms gain stronger operational visibility, faster diagnostics, and improved energy management. Global OEMs with integrated software, automation, and long-term service capabilities continue strengthening their competitive advantage over equipment-only suppliers.

Between 2026 and 2028, hydrogen-ready compression systems, AI-assisted autonomous optimization, additive-manufactured impellers, and cloud-based asset performance management will reshape industrial compressor deployment. Advanced materials supporting higher rotational speeds and enhanced corrosion resistance will improve long-term reliability. Manufacturers investing in integrated digital ecosystems, flexible compression platforms, and remote lifecycle services will strengthen customer retention while enabling industrial operators to maximize productivity, reduce emissions, and optimize total cost of ownership.

May 2024 Atlas Copco completed the acquisition of Tecturbo, a Brazilian manufacturer and service provider for centrifugal compressor components, strengthening regional aftermarket capabilities and expanding support for industrial process customers. Source: Atlas Copco Group

October 2024 Baker Hughes secured an order to supply electrically driven centrifugal compressors for TotalEnergies' Kaminho FPSO project in Angola, supporting one of Africa's major offshore developments with lower-emission compression technology. Source: Baker Hughes

March 2024 Atlas Copco introduced its next-generation GA and GA+ smart compressor range featuring drivetrain lifetime improvements of 33% and integrated connectivity, enhancing industrial efficiency and predictive maintenance capabilities. Source: Atlas Copco UK

January 2026 Atlas Copco expanded its Compressor Technique business through multiple strategic acquisitions, including Air Compressor Works and Centroar, reinforcing global service capabilities and localized aftermarket support for industrial compressor customers. Source: Atlas Copco Annual Report.

This report delivers comprehensive analysis of the Centrifugal Turbo Compressor Market across single-stage, multi-stage, integrally geared, and axially split compressor technologies. It evaluates applications spanning oil & gas, petrochemical and chemical processing, power generation, industrial manufacturing, and industrial gases while assessing procurement trends among oil & gas companies, utilities, chemical manufacturers, industrial gas producers, and process industries. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level analysis of major industrial markets.

The study examines digital twins, AI-enabled predictive maintenance, magnetic bearing technology, variable-speed drives, hydrogen-compatible compression systems, and advanced impeller engineering shaping market evolution between 2026 and 2033. It highlights deployment trends, equipment modernization, service strategies, technology adoption, competitive positioning, and industrial investment priorities, providing decision-makers with actionable intelligence to strengthen expansion planning, operational optimization, supplier evaluation, and long-term market competitiveness.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 11,825.7 Million |

|

Market Revenue in 2033 |

USD 18,565.7 Million |

|

CAGR (2026 - 2033) |

5.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Atlas Copco AB, Baker Hughes Company, Siemens Energy AG, Elliott Group, MAN Energy Solutions, Ingersoll Rand Inc., Mitsubishi Heavy Industries, Ltd., Sulzer Ltd., Kawasaki Heavy Industries, Ltd., Howden Group, Kobelco Compressors Corporation, FS-Elliott Co., LLC, Sundyne LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |