Reports

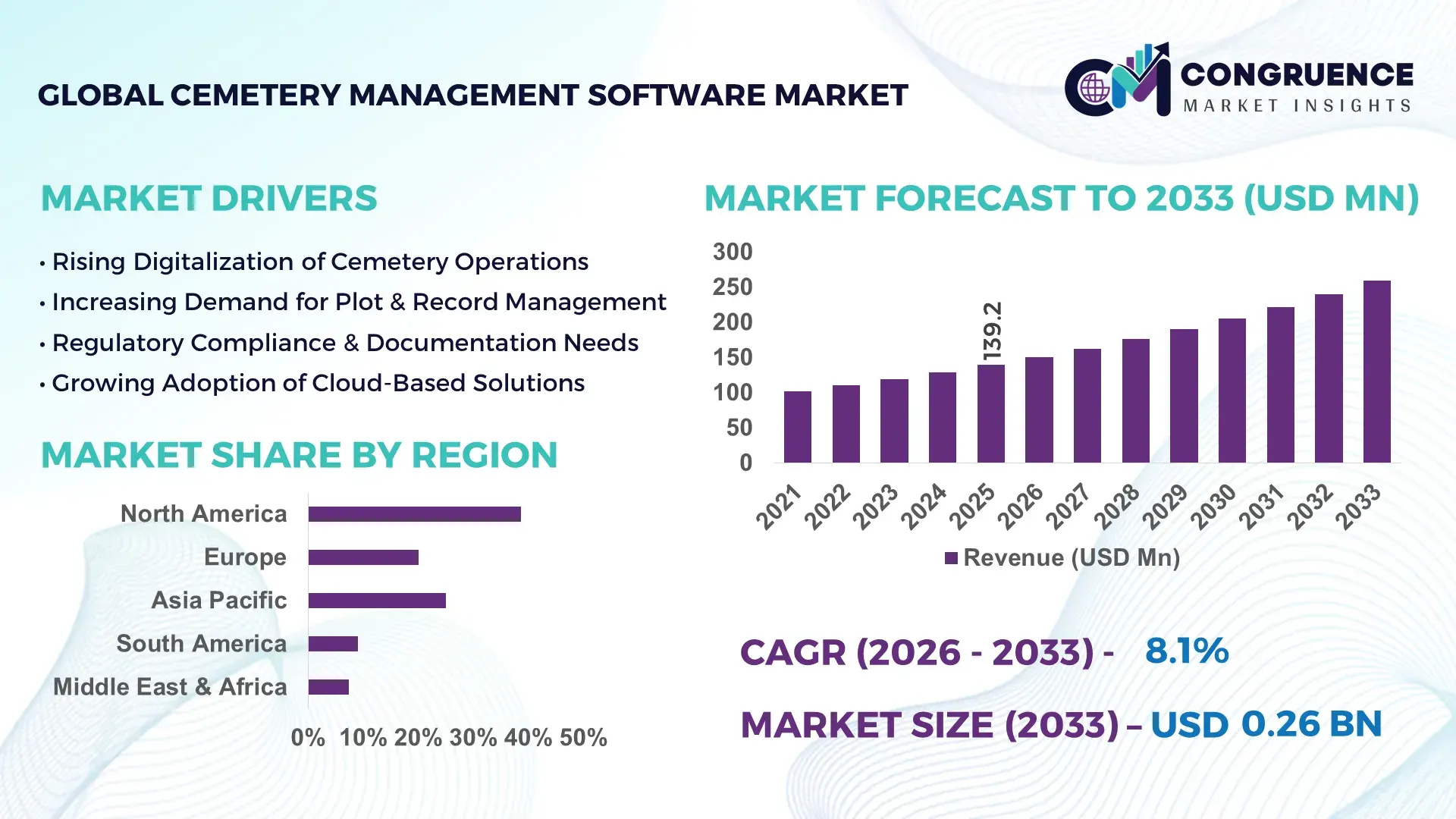

The Global Cemetery Management Software Market was valued at USD 139.2 Million in 2025 and is anticipated to reach a value of USD 259.56 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033. Growth is supported by rising digitization of burial records and increasing demand for centralized cemetery operations management.

The United States represents the dominant country in the global Cemetery Management Software market, supported by a large, digitally mature cemetery infrastructure. Over 155,000 public and private cemeteries operate nationwide, with more than 65% using some form of digital plot mapping or records software. Annual investments in municipal digital infrastructure exceed USD 95 billion, enabling sustained procurement of cloud-based cemetery solutions. Cemetery management software in the U.S. is widely applied across public memorial parks, private cemetery operators, religious institutions, and veterans’ cemeteries. Advanced GIS-based grave mapping, SaaS deployment models, mobile workforce management, and automated compliance reporting are increasingly embedded features, with cloud adoption exceeding 70% among mid-to-large cemetery operators. Besides spatial mapping via GIS, cemetery management software can provide inventory tracking, finance and contracts, records, memorials, scheduling, and operations among others.

Market Size & Growth: Valued at USD 139.2 Million in 2025 and projected to reach USD 259.56 Million by 2033, growing at a CAGR of 8.1%, driven by digital transformation of cemetery operations and recordkeeping.

Top Growth Drivers: Cloud adoption at 68%, operational efficiency improvement of 35%, and digital record conversion penetration of 52%.

Short-Term Forecast: By 2028, cemetery operators are expected to achieve up to 30% administrative cost reduction through workflow automation and digital mapping.

Emerging Technologies: GIS-enabled grave mapping, cloud-based SaaS platforms, AI-assisted record digitization, and mobile cemetery management applications.

Regional Leaders: North America projected at USD 92 Million by 2033 with cloud-first adoption; Europe at USD 71 Million driven by municipal digitization; Asia-Pacific at USD 58 Million supported by smart city initiatives.

Consumer/End-User Trends: Municipal cemeteries and private cemetery operators account for over 60% of deployments, with growing demand for self-service family portals.

Pilot or Case Example: In 2024, a U.S. municipal cemetery digitization pilot reduced record retrieval time by 48% and improved plot allocation accuracy by 41%.

Competitive Landscape: Market led by a single provider with ~18% share, followed by CemeteryFind, PlotBox, Chronicle, CIMS Software, and CemSites.

Regulatory & ESG Impact: Digital record mandates, data protection regulations, and sustainability-focused land-use planning are accelerating software adoption.

Investment & Funding Patterns: Over USD 420 Million invested globally since 2022, with rising venture funding for cloud-native cemetery platforms.

Innovation & Future Outlook: Integration with smart city systems, predictive land-use analytics, and AI-based legacy data digitization will shape future growth.

The Cemetery Management Software market serves municipal administrations, private cemetery operators, religious institutions, and memorial park developers, with municipal bodies contributing approximately 38% of total demand, followed by private operators at 34%. Recent innovations include GIS-integrated grave mapping, automated deed management, and cloud-native SaaS platforms with mobile access. Regulatory drivers include digital public record compliance, data privacy frameworks, and urban land-use optimization policies. Environmentally, software adoption supports sustainable land planning and reduced paper usage. North America and Europe remain high-consumption regions, while Asia-Pacific shows the fastest growth due to urbanization and smart governance programs. Future outlook points toward AI-enabled analytics, integration with digital memorial platforms, and expansion of subscription-based deployment models.

The strategic relevance of the Cemetery Management Software Market is strengthening as cemetery operators, municipalities, and private memorial service providers increasingly prioritize operational transparency, land optimization, regulatory compliance, and long-term asset management. Digitized cemetery platforms now function as core infrastructure systems rather than auxiliary tools, supporting plot lifecycle tracking, GIS-based grave mapping, digital deeds, and family engagement portals. Cloud-based cemetery management software delivers up to 42% workflow efficiency improvement compared to manual paper-based record systems, enabling faster plot allocation, reduced administrative errors, and improved service continuity.

North America dominates in operational volume due to the high number of registered cemeteries, while Europe leads in adoption, with approximately 61% of municipal cemetery authorities actively using cloud-enabled cemetery management platforms. By 2028, AI-assisted record digitization and predictive land-use analytics are expected to improve plot utilization efficiency by nearly 28%, directly extending usable cemetery capacity in urban-constrained regions. From a compliance and ESG perspective, cemetery operators are committing to sustainability metrics such as 35% paper reduction and 20% improvement in land-use efficiency by 2030 through digital documentation and spatial planning tools.

A micro-scenario illustrates this trajectory: in 2024, a UK municipal authority achieved a 44% reduction in record retrieval time and a 31% decrease in plot allocation disputes through the deployment of GIS-integrated cemetery software. Looking ahead, the Cemetery Management Software Market is positioned as a pillar of operational resilience, regulatory alignment, and sustainable infrastructure modernization, supporting long-term continuity for memorial services amid urbanization and demographic change.

Digital transformation across municipal services is a primary driver accelerating the Cemetery Management Software Market. Governments worldwide are digitizing land records, public registries, and citizen services, with over 70% of municipalities in developed economies operating formal digital transformation roadmaps. Cemetery management software aligns directly with these initiatives by enabling centralized databases, GIS-enabled plot visualization, and automated documentation workflows. Digitized systems reduce administrative processing time by up to 40% and significantly lower record loss risks compared to paper archives. Additionally, increasing demand for online access to burial records and genealogy data is pushing cemetery operators to deploy secure, searchable digital platforms. These factors collectively enhance operational accuracy, service responsiveness, and compliance, reinforcing sustained adoption of cemetery management software.

Budget limitations within smaller municipalities and religious cemetery operators present a notable restraint on the Cemetery Management Software Market. Many cemeteries continue to rely on legacy paper-based or locally hosted systems, with transition costs including data migration, staff training, and system integration posing financial challenges. Surveys indicate that nearly 38% of small cemetery operators delay software upgrades due to upfront implementation expenses and limited IT capacity. Additionally, fragmented historical records increase digitization complexity, slowing deployment timelines. Resistance to organizational change and concerns over data security further limit adoption, particularly in regions with low digital maturity or constrained public-sector funding environments.

Smart city initiatives present significant opportunities for the Cemetery Management Software Market by integrating cemetery data into broader urban planning ecosystems. Cemetery management software can support spatial analytics, population planning, and land-use forecasting when connected to municipal GIS and planning platforms. Over 55% of global smart city projects now incorporate digital land management components, creating demand for interoperable cemetery systems. Opportunities also exist in emerging economies where urban expansion is driving new cemetery developments that require digital-first infrastructure. Additionally, value-added services such as online memorialization portals, predictive capacity modeling, and mobile field management tools open new adoption pathways for software providers targeting modernized memorial services.

Data standardization and regulatory complexity pose ongoing challenges within the Cemetery Management Software Market. Cemetery records often span decades or centuries, stored in inconsistent formats that complicate digitization and system interoperability. Regulatory requirements for data protection, public record retention, and land-use compliance vary widely across jurisdictions, increasing customization demands for software vendors. Approximately 46% of cemetery operators report difficulties aligning digital systems with local compliance frameworks. Additionally, ensuring cybersecurity for sensitive personal and burial data requires continuous investment in system upgrades and governance controls. These challenges increase implementation complexity and operational risk, particularly for multi-jurisdictional cemetery networks.

• Accelerated Shift Toward Cloud-Native and SaaS Deployments: Cloud-based cemetery management software is increasingly replacing on-premise systems due to scalability and lower maintenance requirements. Over 68% of newly deployed cemetery management platforms are now cloud-native, enabling multi-site access, automated backups, and faster system updates. Organizations report up to 36% reduction in IT maintenance workloads and nearly 29% faster system deployment timelines. This trend is particularly strong among municipal cemetery networks managing more than 10,000 plots, where centralized cloud dashboards significantly improve operational coordination and data consistency.

• Expansion of GIS-Enabled Grave Mapping and Spatial Analytics: Geographic Information System (GIS) integration has become a core functional trend, with more than 62% of medium-to-large cemetery operators adopting digital grave mapping tools. GIS-enabled cemetery management software improves plot location accuracy by up to 45% and reduces allocation conflicts by nearly 33%. Spatial analytics also supports land-use optimization, enabling operators to extend effective cemetery capacity by approximately 18% through improved planning and re-use modeling, particularly in urban environments with limited land availability.

• Growing Adoption of Digital Public Access and Self-Service Portals: Consumer-facing digital portals are gaining traction as families and researchers increasingly expect online access to burial records. Approximately 57% of cemetery management software deployments now include public or semi-public self-service modules. These platforms reduce in-office inquiry volumes by nearly 41% and shorten record retrieval times by over 50%. Adoption is strongest in regions where digital public records policies are enforced, improving transparency and citizen engagement while lowering administrative overhead.

• Integration of Automation, AI, and Mobile Workforce Tools: Automation and AI-driven features are emerging as differentiators in cemetery management software. Automated record digitization tools improve historical data conversion accuracy by around 38%, while AI-assisted search functions reduce manual lookup time by nearly 47%. Mobile workforce applications are used by over 44% of field staff, increasing task completion efficiency by approximately 26%. These technologies collectively enhance operational reliability, compliance tracking, and real-time decision-making across cemetery operations.

The Cemetery Management Software market is segmented based on type, application, and end-user, reflecting the diverse operational needs of cemetery operators and governing authorities. By type, solutions range from on-premise legacy platforms to cloud-based and integrated GIS-enabled systems, each serving different scales of operation and compliance requirements. Application-wise, the market spans plot and grave management, digital recordkeeping, mapping and navigation, billing, and public-facing information portals, with usage intensity varying by regulatory environment and cemetery size. End-user segmentation highlights strong adoption among municipal cemetery authorities, followed by private cemetery operators and religious institutions, while emerging uptake is visible among memorial parks and heritage management bodies. These segmentation patterns demonstrate a clear shift toward data-driven, compliant, and citizen-accessible systems, driven by digitization mandates, land optimization needs, and rising expectations for transparency and service efficiency.

Cemetery Management Software types include cloud-based platforms, on-premise systems, and hybrid or GIS-integrated solutions. Cloud-based cemetery management software represents the leading type, accounting for approximately 48% of total adoption, due to centralized data access, lower infrastructure burden, and improved disaster recovery capabilities. On-premise systems hold around 27% of adoption, largely among smaller or legacy-operated cemeteries with limited digital transition budgets. However, GIS-integrated and hybrid solutions are the fastest-growing type, expanding at an estimated CAGR of 11.4%, driven by the need for precise grave mapping, spatial analytics, and land-use optimization. These advanced systems are increasingly preferred in urban cemeteries managing more than 20,000 plots. The remaining niche solutions—including standalone record digitization tools and customized local platforms—collectively contribute about 25% of the market, serving specific regulatory or historical record needs.

By application, grave and plot management is the dominant segment, accounting for nearly 39% of total usage, as accurate allocation and lifecycle tracking remain the core operational requirements for cemetery operators. Digital records and document management follow at 26%, supporting compliance, genealogy access, and long-term archival needs. However, mapping and navigation applications are the fastest-growing, advancing at an estimated CAGR of 12.1%, supported by increasing integration of GIS tools and mobile access for field staff and visitors. Billing, permits, and administrative workflow automation, along with public-facing information portals, together contribute approximately 35% of application usage, enhancing efficiency and citizen engagement.

Municipal and government-operated cemeteries represent the leading end-user segment, accounting for around 41% of total adoption, supported by public digital infrastructure programs and compliance-driven record management. Private cemetery operators follow with approximately 33%, leveraging software to standardize operations across multi-site portfolios and improve customer service. Religious and community-managed cemeteries account for about 16%, often adopting modular or scaled-down platforms. Memorial parks and heritage management organizations collectively contribute the remaining 10%. The fastest-growing end-user segment is private cemetery operators, expanding at an estimated CAGR of 10.6%, fueled by consolidation trends and the need for unified data systems.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America benefits from a highly digitized public infrastructure, with over 19,000 registered cemeteries and more than 65% using digital or semi-digital management systems. Europe followed with a 28.1% share, driven by municipal digitization mandates and sustainability-oriented land-use planning. Asia-Pacific held approximately 22.6%, supported by rapid urbanization, smart city investments exceeding USD 1.5 trillion, and rising adoption of cloud-based civic platforms. South America and the Middle East & Africa together accounted for the remaining 9.9%, where adoption is gradually increasing through government-backed digital governance programs. Regional differences in regulatory frameworks, digital maturity, and consumer access models continue to shape localized demand patterns across the Cemetery Management Software market.

How is advanced digital governance accelerating operational adoption across public infrastructure systems?

North America represents approximately 39.4% of the global Cemetery Management Software market, supported by extensive municipal ownership of cemeteries and advanced public-sector IT budgets. Demand is driven primarily by municipal authorities, private cemetery operators, and memorial park corporations managing large plot inventories. Regulatory requirements around digital public records, data retention, and accessibility have increased software deployment across city-managed cemeteries. Technological advancements include widespread adoption of cloud-native platforms, GIS-based grave mapping, and mobile workforce tools, with over 70% of large cemeteries using cloud-hosted solutions. Local software providers are expanding modular platforms focused on compliance automation and citizen self-service portals. Regional consumer behavior reflects higher enterprise adoption, with families increasingly expecting online access to burial records and digital memorial services, reducing in-person administrative interactions by nearly 40%.

Why are compliance-driven digital frameworks reshaping cemetery administration practices?

Europe accounts for nearly 28.1% of the global Cemetery Management Software market, with strong demand concentrated in Germany, the United Kingdom, and France. Municipal cemetery authorities dominate adoption, influenced by strict data protection laws, digital public record mandates, and sustainability-driven land management initiatives. Regional regulatory bodies emphasize transparent documentation and long-term archival integrity, accelerating demand for explainable and auditable software platforms. Emerging technologies such as GIS-integrated grave mapping and interoperable cloud systems are widely adopted, with over 60% of municipal operators using spatial planning tools. Local software firms focus on multilingual interfaces and compliance-centric design. Consumer behavior in this region is shaped by regulatory pressure, leading to preference for systems that offer traceability, audit logs, and standardized reporting.

How are urban expansion and smart city investments transforming digital cemetery operations?

Asia-Pacific ranks as the fastest-expanding regional market and holds approximately 22.6% of global adoption by volume. China, India, and Japan are the top consuming countries, driven by dense urban populations and expanding municipal infrastructure. Large-scale smart city initiatives and digitization of civic services are accelerating demand for cloud-based cemetery platforms, particularly in metropolitan regions managing over 100,000 burial records. Regional innovation hubs emphasize mobile-first platforms, AI-enabled digitization, and integration with municipal GIS systems. Local providers are developing scalable solutions tailored for high-density urban cemeteries. Consumer behavior reflects strong mobile usage, with more than 55% of interactions occurring via mobile portals, aligning with broader digital service consumption trends in the region.

What role do public modernization programs play in accelerating digital adoption?

South America contributes approximately 6.1% of the global Cemetery Management Software market, with Brazil and Argentina as key countries. Market demand is linked to gradual modernization of municipal services and investments in digital public infrastructure. Governments are introducing incentives for digital recordkeeping and administrative automation, indirectly supporting cemetery software adoption. Infrastructure upgrades in urban municipalities have increased demand for centralized record systems and billing automation tools. Regional software vendors are focusing on cost-efficient, cloud-hosted platforms tailored for mid-sized cemeteries. Consumer behavior shows growing preference for localized language support and simplified digital access, reducing manual inquiry volumes by nearly 30% in digitally enabled cities.

How is institutional digitization shaping emerging demand patterns?

The Middle East & Africa region accounts for roughly 3.8% of global market adoption, with demand concentrated in the UAE and South Africa. Digital transformation programs across public administration and urban development projects are driving interest in cemetery management platforms. Technological modernization trends include adoption of cloud-based record systems and centralized municipal dashboards. Regulatory alignment with data governance standards and regional trade partnerships support gradual software uptake. Local providers and system integrators are collaborating with municipalities to deploy modular solutions. Consumer behavior varies widely, but demand is increasingly linked to centralized administrative efficiency and improved public access to records in urban centers.

United States – 31.2% market share

Strong municipal digitization, large cemetery infrastructure base, and advanced cloud adoption drive leadership in the Cemetery Management Software market.

Germany – 9.4% market share

High regulatory compliance requirements and widespread municipal investment in digital public records support sustained adoption of Cemetery Management Software.

The Cemetery Management Software market exhibits a moderately fragmented competitive structure, characterized by the presence of approximately 35–45 active software vendors globally. The market is led by a small group of specialized providers offering end-to-end cemetery administration platforms, while a long tail of regional and niche players focus on localized compliance, language support, or specific functional modules such as GIS mapping or digital records management. The top five companies collectively account for nearly 52% of total deployments, indicating partial consolidation alongside ongoing competitive intensity.

Competition is primarily shaped by product differentiation, cloud deployment capabilities, GIS integration depth, and regulatory compliance features. More than 60% of leading vendors have transitioned their core offerings to SaaS-based architectures, enabling faster updates, lower implementation friction, and scalable pricing models. Strategic initiatives are common, including municipal partnerships, multi-site enterprise contracts, and feature expansions such as AI-assisted digitization and mobile workforce tools. Between 2023 and 2025, over 40% of major players launched upgraded platforms incorporating GIS visualization, automated reporting, or citizen-facing portals. Merger and acquisition activity remains selective, with fewer than 8 notable transactions in recent years, largely aimed at geographic expansion or technology enhancement. Innovation-driven competition continues to intensify as vendors focus on interoperability, data security, and long-term archival reliability.

PlotBox

Chronicle

CemSites

CIMS Software

CemeteryFind

PlotBox Global

CemSites Software

Chronicle Management Systems

The Cemetery Management Software market is witnessing a pronounced technological shift toward cloud-native architectures, advanced spatial intelligence, automation, and mobile-enabled operational tools. As of 2025, over 68% of cemetery management platforms are deployed on cloud infrastructure, enabling centralized access, automated backups, enhanced security protocols, and real-time updates across multi-site operations. Cloud delivery has become a baseline expectation, particularly among municipal authorities and larger private operators managing more than 20,000 burial records. On-premise systems persist among smaller operators but are increasingly supplemented with hybrid modules for remote access and disaster recovery. Geographic Information System (GIS) integration is a core differentiator in contemporary offerings. GIS-enabled cemetery management solutions provide visual plot mapping, spatial analytics, and land-use optimization, with approximately 62% of mid-to-large operators deploying such modules. These systems improve plot location accuracy by up to 45% and reduce allocation conflicts by around 33%, enhancing both administrative precision and long-term planning. Advanced GIS tools also support predictive spatial modeling to extend effective cemetery capacity in constrained urban environments.

Automation and artificial intelligence (AI) are reshaping data management processes. Automated record digitization accelerates migration from legacy paper archives, improving data conversion accuracy by roughly 38% and reducing manual input time by nearly 47%. AI-assisted search and classification features further reduce retrieval times and improve compliance reporting. Additionally, mobile workforce applications are being integrated by about 44% of field teams, enabling real-time task updates, on-site record validation, and streamlined coordination between office and field personnel. Enhanced cybersecurity measures, including multi-factor authentication, encryption at rest and in transit, and role-based access controls, are increasingly standard, with over 55% of deployments incorporating advanced security modules. Finally, public-facing portals offering self-service record access and interactive grave search tools are being adopted by around 57% of cemetery operations, reflecting evolving consumer expectations for transparency, accessibility, and digital engagement.

• In January 2025, webCemeteries announced the launch of integrated eSignature functionality within its Cemetery Management platform, enabling contract signing electronically, streamlining sales workflows, and reducing administrative friction for both in-person and remote interactions. This enhancement modernizes cemetery sales processes and improves support for family counselors. (webCemeteries™)

• On January 17, 2025, webCemeteries introduced Forever Plot, a new interactive website plugin allowing cemeteries to display property availability with detailed imagery and maps, generating real-time inquiries and enhancing digital engagement with families through seamless integration with the core management platform. (webCemeteries™)

• In July 2025, CemSites unveiled a strategic partnership with Grave Explorer to integrate cemetery management workflows with digital memorial platforms, aiming to enhance interoperability, streamline data exchange, and enrich customer and family engagement across service points.

• In 2024, PlotBox celebrated its 10-year anniversary, marking significant expansion in enterprise customer onboarding, strategic partnerships, and global footprint growth, while securing increased investment to support operations across North America, Europe, and APAC markets. (ACCA)

The scope of the Cemetery Management Software Market Report encompasses a comprehensive analysis of the solutions and services that support efficient cemetery operations, digital recordkeeping, plot management, mapping, billing, and customer engagement functionalities. The report covers a wide array of product segments, including cloud-based, on-premise, hybrid, and GIS-integrated platforms, with detailed segmentation that reflects deployment preferences among municipal authorities, private cemetery operators, religious institutions, memorial parks, and heritage management bodies. Geographically, the report examines market behavior and technology adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional variances in digital maturity, regulatory environments, and urban planning influences.

Application analysis within the report includes record management, plot and grave allocation, financial and billing systems, customer self-service portfolios, and public-facing portals that support interactive map access and genealogy queries. The report also explores emerging technology trends such as mobile workforce solutions, automation and AI-assisted tools for data digitization, predictive spatial modeling, and advanced GIS visualization. End-user insights detail adoption rates and operational priorities among different cemetery types, including large municipal portfolios versus smaller family-run operations. Additionally, niche segments such as interactive online memorialization services, environmental compliance modules, and subscription-based digital tools are assessed, offering decision-makers a clear view of current capabilities, unmet needs, and future innovation pathways within the global Cemetery Management Software landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 8.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | PlotBox, Chronicle, CemSites, CIMS Software, CemeteryFind, PlotBox Global, CemSites Software, Chronicle Management Systems |

Customization & Pricing | Available on Request (10% Customization is Free) |