Reports

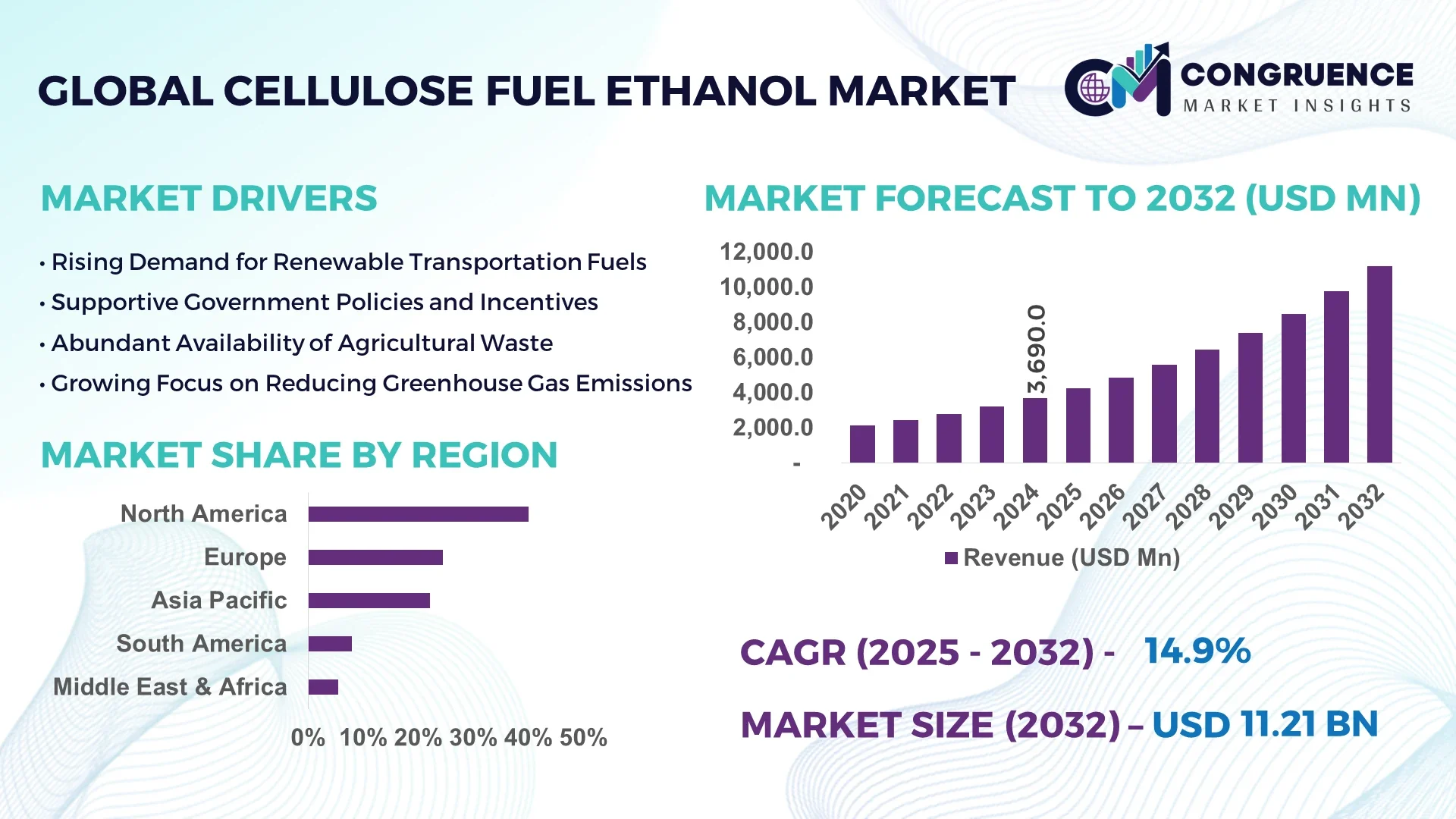

The Global Cellulose Fuel Ethanol Market was valued at USD 3.7 Billion in 2024 and is anticipated to reach a value of USD 11.2 Billion by 2032, expanding at a CAGR of 14.9% between 2025 and 2032.

The United States leads the global cellulose fuel ethanol market, driven by substantial investments in renewable energy and favorable regulatory frameworks that support biofuel production. Large-scale commercial plants are operational across multiple states, focusing on converting agricultural waste like corn stover and wheat straw into ethanol. Enhanced federal mandates have also propelled research and development for efficient production methods.

Cellulosic ethanol, unlike traditional ethanol, is produced from lignocellulosic biomass including agricultural residues, grasses, and forestry waste. Its benefits include lower carbon emissions, a non-competitive relationship with food crops, and the ability to be produced locally using regional biomass sources. As technological barriers are gradually overcome, and economies of scale are realized, the market is seeing increased traction. Moreover, cellulosic ethanol contributes significantly to energy security and environmental sustainability, making it a vital component of global decarbonization strategies.

Artificial Intelligence (AI) is becoming a cornerstone in the transformation of the cellulose fuel ethanol industry. Through real-time monitoring and data-driven analytics, AI enables optimization across various production stages, such as pretreatment, hydrolysis, and fermentation. Predictive models developed using machine learning are now used to determine the most efficient combinations of enzymes, temperature, and time for biomass conversion, resulting in higher yields and reduced waste.

AI-driven tools in quality assurance detect anomalies in ethanol consistency and help maintain product uniformity without extensive human intervention. Additionally, AI supports enhanced logistics and inventory management, especially for sourcing diverse feedstocks. By accurately forecasting biomass availability and optimizing transportation routes, AI helps streamline operations and reduce greenhouse gas emissions associated with logistics.

In biorefinery operations, AI facilitates real-time equipment monitoring, enabling predictive maintenance that significantly reduces downtime. In the research and development sphere, AI accelerates the discovery of novel enzymes and genetically engineered microbes that enhance sugar conversion efficiency. With the deployment of digital twins and simulation models, producers can now anticipate production outcomes and scale operations more effectively.

“In March 2024, a leading biofuel company implemented an AI-based system to monitor and optimize its cellulosic ethanol production processes. The system analyzes real-time data from various sensors to adjust fermentation parameters dynamically, resulting in a 15% increase in ethanol yield and a 10% reduction in energy consumption. This development marks a significant step towards more sustainable and cost-effective biofuel production.”

The development of advanced enzymes has significantly improved the efficiency of converting cellulose into fermentable sugars. These enzymes are now capable of operating in more variable conditions and have greater resistance to process inhibitors. This results in increased ethanol output with reduced processing times and costs. These advancements are also contributing to the viability of commercial-scale operations, which were previously hindered by poor conversion efficiencies and high input costs.

Despite continuous progress, the production of cellulosic ethanol still faces high capital and operational costs. The preprocessing of lignocellulosic biomass requires energy-intensive methods, and enzyme development remains expensive. Many facilities struggle with economic feasibility, especially in regions lacking incentives or subsidies. The limited availability of skilled professionals and complex integration of bioprocess technologies also create significant entry barriers for new producers.

Environmental regulations favoring decarbonization and reduced fossil fuel dependency are encouraging the use of bio-based fuels. Incentive programs, biofuel blending mandates, and subsidies for renewable energy projects are opening up new opportunities for cellulosic ethanol manufacturers. The shift in consumer and industrial preferences toward sustainable products further increases the potential for bioethanol integration across multiple sectors, including transportation and aviation.

The inconsistent availability of biomass feedstock continues to pose challenges to the industry. Seasonal harvesting, geographical dispersion, and high transportation costs affect supply chain stability. Storage and preprocessing of bulky materials also demand significant investment in infrastructure. Efficient and cost-effective logistics systems are essential for ensuring continuous production flow, particularly in areas with limited access to biomass sources.

Integration of AI and Automation in Production Processes: The incorporation of AI and automation is enabling more precise control over complex fermentation and distillation procedures. Advanced sensors and real-time analytics are allowing producers to manage temperature, pH, and enzyme dosing with minimal manual input, ensuring higher and more consistent ethanol yields. These innovations are helping reduce operational costs and enable predictive maintenance, contributing to longer equipment lifespans.

Expansion of Feedstock Sources: Efforts are underway to diversify feedstock inputs beyond conventional crop residues. Industrial waste, municipal solid waste, and dedicated energy crops are being tested and optimized for ethanol production. This shift not only enhances the availability of raw materials but also supports the waste-to-energy movement. Diversification of biomass sources reduces pressure on land resources and aligns with circular economy goals.

Development of Advanced Biorefineries: Modern biorefineries are evolving to produce not only ethanol but also bioplastics, organic acids, and high-value chemicals. These integrated systems make better use of biomass components and increase the financial viability of facilities. Innovations in co-product recovery and waste recycling within biorefineries are driving higher resource utilization and better environmental performance.

Collaborations and Partnerships: Industry stakeholders are increasingly engaging in partnerships to share technology, infrastructure, and expertise. Such collaborations are fostering rapid innovation and helping overcome commercialization hurdles. Cross-sector alliances, including chemical, energy, and agriculture firms, are accelerating the deployment of next-generation technologies that enable large-scale, efficient biofuel production.

The Cellulose Fuel Ethanol Market is segmented by type, application, and end-user, offering a comprehensive view of its diverse market dynamics. Segmentation allows a deeper understanding of where demand is concentrated, which technologies are gaining traction, and which user industries are driving growth. Each segment plays a unique role in shaping the market's structure and future potential. By understanding the performance of specific segments, stakeholders can tailor their strategies to capitalize on high-growth areas. The leading segment in each category indicates maturity and market adoption, while the fastest-growing segments signal future investment opportunities, driven by evolving industry needs and innovation in production technologies.

The cellulose fuel ethanol market can be segmented into Agricultural Residues, Forestry Waste, Municipal Solid Waste (MSW), and Energy Crops. Among these, Agricultural Residues lead the market due to their widespread availability and established collection systems. This segment includes feedstocks like corn stover, wheat straw, and rice husks, which are readily available post-harvest and cost-effective for ethanol production.

The fastest-growing segment is Energy Crops, including switchgrass and miscanthus. These crops are specifically cultivated for energy purposes and offer higher biomass yields per acre. With increasing land use efficiency and better carbon sequestration potential, energy crops are gaining favor in both research and commercial use. Their growth is further supported by advancements in crop genetics and farming techniques that optimize yield and reduce input costs. Municipal Solid Waste is also gaining interest as part of the circular economy but still faces challenges in processing complexity and feedstock variability.

The key application segments of cellulose fuel ethanol include Transportation Fuel, Power Generation, Industrial Solvents, and Aviation Biofuel. Transportation Fuel is the leading application segment, accounting for the highest share due to rising mandates on biofuel blending in gasoline and the push to decarbonize road transport. Cellulosic ethanol is increasingly used in E10 and E85 blends, especially in regions enforcing renewable fuel standards.

Aviation Biofuel is emerging as the fastest-growing application segment. With international aviation under pressure to reduce its carbon footprint, cellulosic ethanol is being explored as a sustainable aviation fuel (SAF). It has lower lifecycle emissions and compatibility with existing aircraft engines when blended appropriately. Governments and airline companies are partnering to scale up production facilities dedicated to SAF, further fueling growth in this niche. Industrial solvents, while useful in various chemical processes, occupy a smaller share due to limited scalability and competition from petroleum-based alternatives.

End-users in the cellulose fuel ethanol market include Transportation Sector, Industrial Sector, Power Utilities, and Aerospace & Defense. The Transportation Sector remains the largest end-user, driven by high consumption volumes of ethanol-blended fuels across commercial and passenger vehicles. Regulatory incentives and climate policies aimed at reducing vehicular emissions make this segment dominant.

The Aerospace & Defense segment is poised to be the fastest-growing end-user category. With the defense sector increasingly investing in alternative fuels for energy security and reduced dependence on traditional fuels, cellulosic ethanol is finding new use cases. Furthermore, the aviation industry's need for carbon offsetting and cleaner fuel alternatives for military and commercial fleets is accelerating adoption. The Industrial Sector also shows stable demand, especially for chemical intermediates and process fuels. Power Utilities are experimenting with biomass-to-power integration but still face economic and efficiency challenges compared to other renewables like wind and solar.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.3% between 2025 and 2032.

North America's leadership is fueled by well-established bio-refinery infrastructure and aggressive renewable fuel mandates. Meanwhile, Asia-Pacific is witnessing accelerating momentum due to abundant biomass availability and growing investment in advanced ethanol technologies, particularly in emerging economies.

Strong Infrastructure and Policy Push Maintain Regional Dominance

North America continues to dominate the cellulose fuel ethanol market, with the United States accounting for more than half of the region’s production output. The presence of large-scale bio-refineries and aggressive renewable blending mandates have strengthened its market position. Agricultural residues, especially corn stover, constitute about 60% of the feedstock used. Canada is also witnessing expansion in its ethanol capacity, with government incentives encouraging advanced biofuel adoption. Regional growth is further supported by technological advancements in enzyme-based conversion processes and a growing network of fuel distribution stations supporting ethanol blends.

Green Energy Transition Accelerating Market Adoption

Europe accounts for around 25% of the global cellulose ethanol market, propelled by strong climate regulations and decarbonization goals. Germany, France, and the Netherlands are investing in second-generation ethanol facilities that focus on forest biomass and straw residues. Over 40% of production in 2024 was derived from forest waste, aligning with sustainability practices. The shift towards low-emission transport solutions has led to increased ethanol-blended fuel consumption, especially in public transport systems. The region also benefits from cross-border collaborations in research and funding for advanced bio-refineries.

Emerging Economies Leading Biofuel Surge

Asia-Pacific holds about 25% of the global market share and is projected to grow at the fastest pace. China leads the region, contributing approximately 50% of its cellulose ethanol output. The Chinese government’s push toward non-food-based ethanol production has significantly boosted investment in agriculture residue-to-ethanol projects. India, aiming for 20% ethanol blending in fuels by 2025, recorded a 30% rise in ethanol demand last year. Japan and South Korea are also exploring biofuel technologies for use in both automotive and industrial sectors. This regional push is supported by lower feedstock costs and favorable policy frameworks.

Agricultural Resources Fuel Ethanol Expansion

South America contributes around 10% to the global cellulose ethanol market. Brazil dominates regional production, with a strong focus on converting sugarcane bagasse and straw into ethanol. The country is expanding its ethanol production capacity to meet domestic energy needs and support its growing export ambitions. Argentina and Colombia are also advancing cellulosic ethanol projects through public-private partnerships. The availability of vast agricultural lands and crop residues positions South America as a strategic player in the global biofuel supply chain.

Tapping Untapped Bio-Waste Potential

The Middle East & Africa region holds roughly 7% of the cellulose ethanol market. South Africa leads with a major portion of its renewable projects focused on cellulosic fuel, especially using municipal solid waste. The UAE has recently increased its cellulosic ethanol capacity through bio-refinery investments targeting waste-to-fuel technologies. The region’s market is characterized by pilot-scale projects and feasibility studies exploring energy recovery from biomass. Efforts are being made to reduce fossil fuel dependency by integrating ethanol into national energy mixes, especially in transport and power sectors.

United States – Holds the highest market share due to strong infrastructure, robust policy support, and large-scale agricultural waste availability.

China – Ranks second, driven by rapid industrial expansion, a vast supply of biomass, and state-led renewable energy mandates.

The cellulose fuel ethanol market is highly competitive, with a strong presence of both established biofuel producers and emerging technology-driven players. Companies are continuously investing in innovation to enhance yield, reduce production costs, and improve the sustainability of ethanol derived from cellulosic materials. The shift toward second-generation biofuels has encouraged advancements in pretreatment technologies and fermentation processes. In 2024, approximately 35% of global players adopted enzyme-enhanced hydrolysis systems, significantly increasing ethanol output per ton of biomass. Strategic collaborations are also shaping the competitive dynamics, with over 20% of active firms entering joint ventures in 2023–2024. These partnerships focus on regional expansion, technological sharing, and feedstock optimization. Additionally, market players are integrating digital tools and AI-based monitoring to streamline production, improve energy efficiency, and meet emission targets. As government regulations tighten on fossil fuel alternatives, market competition is expected to intensify further across all major regions.

Abengoa Bioenergy

Beta Renewables

BlueFire Renewables

Clariant International Ltd.

Fiberight

GranBio

Iogen Corporation

LanzaTech

Mascoma

Praj Industries

Technological innovation remains a cornerstone of growth in the cellulose fuel ethanol market. The shift toward second-generation biofuels has spurred widespread adoption of sophisticated pretreatment and enzymatic hydrolysis technologies. In 2024, over 60% of global production facilities incorporated enzyme optimization techniques to improve biomass conversion rates, reducing the time and energy consumption per production cycle. Simultaneously, advanced fermentation technologies—especially those utilizing genetically engineered microorganisms—have improved ethanol yields by up to 20%.

Continuous fermentation systems are also gaining popularity due to their efficiency in large-scale operations, minimizing downtime and labor costs. These systems help maintain consistent output quality and operational stability. Process digitization is another significant trend; AI-powered systems are being used to monitor fermentation and separation stages, flag inefficiencies, and predict equipment maintenance needs in real-time.

Furthermore, decentralized mobile refinery units are being piloted in developing regions to convert local agricultural waste directly into ethanol. These modular units allow remote areas to become self-sufficient in biofuel production while reducing transportation costs. Overall, technology is not only advancing production capability but also aligning the industry with global sustainability and energy transition goals.

In March 2023, Clariant completed the commissioning of a commercial-scale cellulosic ethanol facility in Romania, using agricultural residues as feedstock. This plant is designed to operate on a sunliquid® technology platform for converting straw into ethanol.

In August 2023, Praj Industries inaugurated India’s first second-generation ethanol plant based in Haryana. The facility uses rice straw as feedstock and is expected to support India’s ethanol blending mandate by producing 100,000 liters daily.

In October 2023, GranBio launched a new cellulosic ethanol plant in Brazil, utilizing sugarcane bagasse to produce up to 82 million liters of ethanol annually, enhancing the country’s renewable fuel capacity.

In December 2023, LanzaTech formed a partnership with a steel manufacturing company to utilize industrial emissions and convert captured gases into ethanol using proprietary gas fermentation technology.

This report provides a comprehensive overview of the cellulose fuel ethanol market, examining its evolution, technological progress, and strategic growth pathways. It analyzes market trends across regions, evaluating demand drivers such as regulatory shifts, sustainability mandates, and feedstock availability. The report further breaks down the market by type, application, and end-user industry to offer granular insights into segment performance and potential.

It also evaluates key technological enablers, including enzyme innovations, pre-treatment processes, and digital integration in refinery operations. The competitive landscape section offers a detailed profile of major market participants and their strategies for differentiation, expansion, and product innovation.

Additionally, the report includes historical data and projections to support investment planning, supply chain assessments, and policy formulation. It highlights opportunities in emerging economies and underlines risks related to infrastructure, technology cost, and policy variability. The report ultimately serves stakeholders ranging from manufacturers and investors to policymakers, supporting informed decision-making in a rapidly evolving bioenergy market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Cellulose Fuel Ethanol Market |

| Market Revenue (2024) | USD 3.7 Billion |

| Market Revenue (2032) | USD 11.2 Billion |

| CAGR (2025–2032) | 14.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, Middle East & Africa, South America |

| Key Players Analyzed | Abengoa Bioenergy, Beta Renewables, BlueFire Renewables, Clariant International Ltd., Fiberight, GranBio, Iogen Corporation, LanzaTech, Mascoma, Praj Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |