Reports

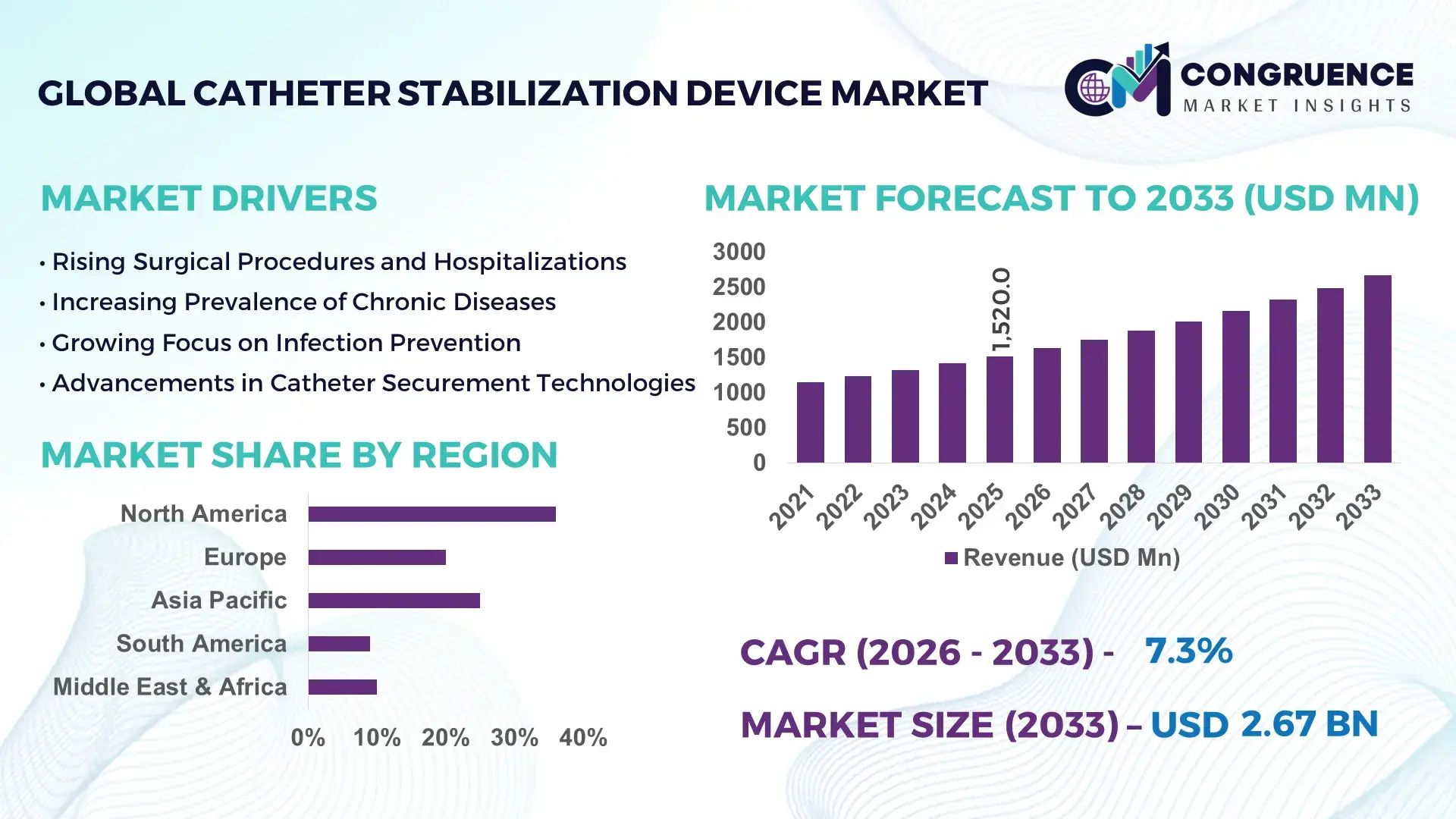

The Global Catheter Stabilization Device Market was valued at USD 1520 Million in 2025 and is anticipated to reach a value of USD 2670.79 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. This growth is primarily driven by the rising prevalence of chronic diseases and increased demand for minimally invasive procedures.

In the United States, which represents a dominant landscape for catheter stabilization device production and innovation, over 45 million catheterization procedures are performed annually across hospitals and ambulatory care centers. The country benefits from advanced healthcare infrastructure, with more than 6,000 hospitals integrating securement technologies to reduce catheter-related complications. Investments in medical device R&D exceeded USD 15 billion in 2024, with a significant portion allocated to vascular access and infection prevention solutions. Additionally, adoption rates of advanced adhesive-based stabilization devices exceed 70% in critical care units, reflecting strong clinical preference for infection control and patient safety. Technological advancements such as antimicrobial-coated securement systems and skin-friendly adhesives are further enhancing clinical outcomes and operational efficiency.

Market Size & Growth: Valued at USD 1520 Million in 2025 and projected to reach USD 2670.79 Million by 2033 at a CAGR of 7.3%, driven by increasing surgical volumes and infection prevention focus.

Top Growth Drivers: 35% rise in catheterization procedures, 28% improvement in infection prevention adoption, 22% increase in ICU admissions globally.

Short-Term Forecast: By 2028, healthcare facilities are expected to achieve up to 30% reduction in catheter-related bloodstream infections through advanced stabilization solutions.

Emerging Technologies: Antimicrobial securement devices, silicone-based adhesive platforms, and AI-enabled patient monitoring integration.

Regional Leaders: North America projected at USD 980 Million by 2033 with high clinical adoption; Europe at USD 720 Million driven by regulatory compliance; Asia-Pacific at USD 610 Million due to expanding healthcare access.

Consumer/End-User Trends: Hospitals account for over 65% usage, with growing adoption in home healthcare and outpatient settings.

Pilot or Case Example: In 2024, a multi-hospital implementation reduced catheter dislodgement rates by 27% using advanced stabilization systems.

Competitive Landscape: Market leader holds approximately 32% share, followed by key players including major global medical device manufacturers and regional innovators.

Regulatory & ESG Impact: Stringent infection control guidelines and sustainability initiatives targeting 20% reduction in medical waste by 2030.

Investment & Funding Patterns: Over USD 2 billion invested in vascular access technologies in recent years, with strong venture capital interest in smart medical devices.

Innovation & Future Outlook: Integration of digital health tracking, eco-friendly materials, and next-generation adhesive technologies shaping long-term growth.

The catheter stabilization device market is influenced by multiple healthcare sectors, including hospitals, ambulatory surgical centers, and home healthcare, with hospitals contributing over 65% of total demand. Technological advancements such as antimicrobial coatings, breathable adhesive materials, and skin-sensitive fixation systems are improving patient outcomes and reducing infection risks. Regulatory frameworks emphasizing infection prevention and patient safety are accelerating product adoption across developed and emerging economies. Increasing healthcare expenditure, particularly in Asia-Pacific and Latin America, is expanding access to advanced catheter securement solutions. Additionally, the shift toward outpatient care and home-based treatment is driving demand for user-friendly and long-wear stabilization devices. Future trends indicate strong growth potential through integration with digital monitoring systems and environmentally sustainable materials.

The catheter stabilization device market holds strategic importance within the broader medical device ecosystem due to its direct impact on patient safety, infection control, and clinical efficiency. Healthcare providers are increasingly prioritizing advanced stabilization technologies to minimize catheter-related complications, which account for nearly 30% of hospital-acquired infections globally. Modern adhesive securement technologies deliver 40% improvement in catheter stability compared to traditional tape-based methods, significantly reducing dislodgement and associated risks.

North America dominates in procedural volume, while Asia-Pacific leads in adoption growth, with over 55% of healthcare institutions rapidly integrating cost-effective stabilization solutions into clinical workflows. By 2028, AI-enabled monitoring systems integrated with catheter stabilization devices are expected to improve patient monitoring efficiency by up to 35%, enabling proactive intervention and reduced hospital stays.

From a compliance and ESG perspective, firms are committing to measurable sustainability goals, including a 25% reduction in non-biodegradable medical waste by 2030 through the development of eco-friendly materials. In 2024, a leading healthcare system in Europe achieved a 22% reduction in catheter-related infections by implementing antimicrobial stabilization technologies combined with digital tracking systems.

Strategically, the catheter stabilization device market is evolving toward smart, patient-centric solutions that align with regulatory requirements and sustainability goals. As healthcare systems emphasize value-based care, the market is positioned as a critical pillar supporting resilience, compliance, and long-term sustainable growth.

The increasing number of catheter-based procedures globally is a primary driver of the catheter stabilization device market. Over 300 million vascular access procedures are performed annually worldwide, with a significant portion requiring securement solutions to prevent complications. Catheter dislodgement rates can reach up to 15% without proper stabilization, leading to increased healthcare costs and patient discomfort. Advanced stabilization devices reduce these risks by improving fixation strength and patient comfort. The expansion of intensive care units and emergency care facilities, particularly in emerging economies, has further accelerated demand. Additionally, the growing adoption of minimally invasive surgeries, which rely heavily on catheter use, is boosting the need for reliable stabilization technologies across healthcare settings.

Despite technological advancements, cost-related challenges and limited awareness in developing regions continue to restrain the catheter stabilization device market. Advanced stabilization devices, particularly those with antimicrobial coatings and specialized adhesives, can be significantly more expensive than traditional methods such as tape. In low- and middle-income countries, healthcare budgets are often constrained, leading to slower adoption of premium solutions. Furthermore, lack of training and awareness among healthcare professionals regarding the benefits of advanced stabilization devices contributes to continued reliance on conventional techniques. Studies indicate that nearly 40% of healthcare facilities in developing regions still use basic fixation methods, limiting market penetration and slowing overall growth.

The expansion of home healthcare services and advancements in medical device technology present significant opportunities for the catheter stabilization device market. Home-based care is growing at a rate exceeding 10% annually, driven by aging populations and the need for cost-effective treatment solutions. This shift is increasing demand for user-friendly, long-duration stabilization devices that can be safely managed outside hospital settings. Additionally, innovations such as skin-sensitive adhesives, breathable materials, and antimicrobial coatings are enhancing product performance and patient comfort. Digital integration, including sensor-enabled devices that monitor catheter positioning and patient condition, is also opening new avenues for market growth. These advancements are expected to improve patient outcomes and expand the application scope across diverse healthcare environments.

The catheter stabilization device market faces challenges related to stringent regulatory requirements and persistent infection risks. Medical devices must comply with rigorous safety and performance standards, which can delay product approvals and increase development costs. Additionally, variations in regulatory frameworks across regions create complexities for manufacturers seeking global expansion. Infection risks remain a critical concern, as improper use or low-quality devices can contribute to catheter-related bloodstream infections, affecting patient safety and healthcare outcomes. Reports indicate that such infections can increase hospital stays by up to 10 days, adding operational burdens on healthcare systems. Addressing these challenges requires continuous innovation, robust quality assurance, and comprehensive training programs for healthcare professionals.

• Increasing Adoption of Antimicrobial Stabilization Devices:

Healthcare facilities are rapidly transitioning toward antimicrobial-coated catheter stabilization devices to reduce infection risks. Studies indicate that over 60% of intensive care units have adopted antimicrobial securement systems, leading to a 25%–35% reduction in catheter-related bloodstream infections. These devices incorporate advanced coatings such as chlorhexidine and silver ions, which actively inhibit bacterial growth. Adoption is particularly strong in North America and Europe, where hospital-acquired infection rates are closely monitored. Additionally, more than 70% of hospitals with infection control programs have integrated antimicrobial stabilization solutions into their protocols, reflecting a measurable shift toward safer patient care practices.

• Shift Toward Silicone-Based and Skin-Friendly Adhesives:

The demand for silicone-based adhesive catheter stabilization devices has increased by over 40% in the last three years due to improved patient comfort and reduced skin irritation. Approximately 55% of long-term catheter users experience skin complications with traditional adhesives, prompting healthcare providers to adopt hypoallergenic alternatives. Silicone-based solutions demonstrate up to 30% better skin compatibility and 20% improved device retention compared to conventional materials. This trend is especially prominent in geriatric and pediatric care, where skin sensitivity is a critical concern, driving hospitals to prioritize patient-centric stabilization technologies.

• Expansion of Home Healthcare and Outpatient Usage:

The growing shift toward home healthcare has significantly influenced the catheter stabilization device market, with over 35% of catheter-based treatments now administered outside hospital settings. Demand for easy-to-use and long-wear stabilization devices has increased by approximately 45% among home healthcare providers. These devices are designed for extended wear of up to 7 days, reducing the need for frequent replacements. In addition, patient compliance rates have improved by nearly 28% with user-friendly designs, supporting the broader adoption of outpatient care models and reducing hospital readmissions.

• Integration of Smart Monitoring and Digital Health Technologies:

The integration of digital health technologies into catheter stabilization devices is emerging as a transformative trend, with smart devices improving monitoring accuracy by up to 32%. Sensor-enabled stabilization systems can detect early signs of catheter displacement or infection, enabling timely clinical intervention. Approximately 20% of advanced healthcare facilities have begun pilot programs using connected stabilization devices linked to hospital monitoring systems. These technologies have demonstrated a 22% reduction in catheter-related complications and a 15% improvement in clinical workflow efficiency, indicating strong potential for future large-scale adoption.

The catheter stabilization device market is segmented based on type, application, and end-user, each contributing distinctively to overall industry performance. Product types range from adhesive-based securement devices to mechanical stabilization systems, with adhesive solutions dominating due to ease of use and patient comfort. Application-wise, the market is driven by cardiovascular, urological, and general intravenous catheterization procedures, with cardiovascular applications accounting for a significant share due to high procedure volumes. End-user segmentation highlights hospitals as the primary consumers, followed by ambulatory surgical centers and home healthcare providers. Increasing outpatient procedures and rising adoption of home-based care are reshaping demand patterns across segments. Furthermore, technological advancements and infection control requirements are influencing segmentation trends, encouraging the adoption of advanced stabilization solutions across all healthcare settings.

Adhesive-based catheter stabilization devices represent the leading segment, accounting for approximately 58% of total adoption due to their ease of application, cost-effectiveness, and enhanced patient comfort. These devices provide secure fixation while minimizing skin irritation, making them suitable for both short-term and long-term catheterization. Mechanical stabilization devices hold around 27% of the market, offering stronger fixation for critical care scenarios, particularly in high-movement environments such as intensive care units. However, adoption in hybrid stabilization systems, which combine adhesive and mechanical features, is rising fastest, expected to grow at a CAGR of 8.5% due to their superior performance in preventing catheter dislodgement.

Other niche types, including sutures and securement tapes, collectively contribute nearly 15% of the market, primarily used in low-resource settings or specific clinical scenarios. These traditional methods are gradually declining due to higher risks of infection and patient discomfort.

Cardiovascular catheterization applications dominate the catheter stabilization device market, accounting for approximately 46% of total usage due to the high volume of procedures such as angiography and central venous catheter placements. Urological applications represent around 24% of the market, driven by the increasing prevalence of urinary disorders and long-term catheter use in aging populations. Meanwhile, general intravenous applications account for nearly 30%, covering a wide range of medical treatments including fluid administration and drug delivery.

Among these, home-based intravenous therapy is the fastest-growing application segment, projected to expand at a CAGR of 9.2% as healthcare systems increasingly shift toward outpatient care. The growing emphasis on reducing hospital stays and improving patient convenience is accelerating adoption in this segment.

Hospitals remain the leading end-user segment in the catheter stabilization device market, accounting for approximately 65% of total demand due to the high volume of inpatient procedures and critical care requirements. Ambulatory surgical centers contribute around 20%, benefiting from the increasing number of same-day surgical procedures and the need for efficient catheter management. Home healthcare providers account for nearly 15% of the market, reflecting the growing trend toward decentralized healthcare delivery.

Home healthcare is the fastest-growing end-user segment, with an expected CAGR of 10.1%, driven by the rising aging population and the need for cost-effective treatment solutions. Adoption rates in home healthcare settings have increased by over 35% in recent years, supported by advancements in user-friendly stabilization devices.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

North America maintains leadership with over 25 million catheter procedures performed annually and more than 70% adoption of advanced stabilization devices across hospitals. Europe holds approximately 28% share, supported by over 15,000 healthcare facilities implementing infection prevention protocols. Asia-Pacific accounts for nearly 22% of global demand, with China and India collectively contributing over 45% of regional consumption due to expanding healthcare infrastructure. South America represents around 7% share, while Middle East & Africa contributes close to 5%, with increasing investments in healthcare modernization. Across regions, adoption rates of antimicrobial stabilization devices exceed 60% in developed markets, compared to 35%–40% in emerging economies, reflecting varying levels of clinical integration and regulatory enforcement.

How Are Advanced Clinical Standards Driving High Adoption of Securement Solutions?

North America holds approximately 38% of the catheter stabilization device market, driven by strong demand from hospitals, ambulatory surgical centers, and long-term care facilities. The region performs over 25 million catheterization procedures annually, creating consistent demand for advanced stabilization technologies. Regulatory frameworks such as strict infection control mandates have pushed over 75% of hospitals to adopt antimicrobial and silicone-based devices. Digital transformation is also evident, with nearly 30% of healthcare systems integrating smart monitoring solutions with stabilization devices. A key regional player has introduced adhesive systems that improve catheter securement efficiency by 28%, enhancing patient outcomes. Consumer behavior reflects a high preference for clinically validated and premium products, with more than 65% of healthcare providers prioritizing safety-certified devices over cost considerations.

Why Are Stringent Healthcare Regulations Accelerating Demand for Advanced Securement Devices?

Europe accounts for around 28% of the catheter stabilization device market, with major contributions from Germany, the United Kingdom, and France. The region benefits from strong regulatory oversight focused on patient safety and infection control, leading to adoption rates exceeding 68% for advanced stabilization solutions. Sustainability initiatives are also shaping product innovation, with nearly 40% of manufacturers focusing on eco-friendly materials. Emerging technologies such as breathable adhesives and antimicrobial coatings are widely integrated across healthcare systems. A regional manufacturer has developed biodegradable stabilization devices, reducing medical waste by approximately 18% in pilot programs. Consumer behavior in this region is influenced by regulatory compliance, with healthcare providers prioritizing certified and environmentally sustainable solutions.

What Factors Are Accelerating Adoption of Cost-Effective and Scalable Securement Technologies?

Asia-Pacific ranks as the fastest-growing region and accounts for nearly 22% of global catheter stabilization device consumption. China, India, and Japan are the leading markets, collectively contributing over 60% of regional demand. The region performs more than 40 million catheter procedures annually, driven by expanding healthcare infrastructure and increasing chronic disease prevalence. Manufacturing capabilities are rapidly improving, with over 50% of local production focused on cost-efficient adhesive-based devices. Innovation hubs in countries such as Japan are developing advanced skin-friendly materials, improving patient comfort by up to 25%. A regional player has scaled production capacity by 35% to meet rising domestic and export demand. Consumer behavior is characterized by cost sensitivity, with approximately 55% of healthcare providers opting for affordable yet effective stabilization solutions.

How Are Healthcare Investments and Policy Support Driving Market Expansion?

South America represents approximately 7% of the global catheter stabilization device market, with Brazil and Argentina as key contributors. The region performs over 8 million catheter-related procedures annually, supporting steady demand for stabilization devices. Government healthcare programs and import-friendly trade policies have increased access to advanced medical devices, with adoption rates rising by nearly 20% in public hospitals. Infrastructure improvements in urban healthcare facilities are further boosting demand. A regional supplier has expanded distribution networks by 30%, improving accessibility across remote areas. Consumer behavior varies significantly, with public healthcare institutions focusing on cost-effective solutions, while private hospitals show a growing preference for advanced antimicrobial devices.

What Role Does Healthcare Modernization Play in Driving Device Adoption?

The Middle East & Africa region accounts for nearly 5% of the catheter stabilization device market, with key growth countries including the UAE and South Africa. The region is witnessing increasing demand due to healthcare modernization initiatives and rising investments in hospital infrastructure, with over USD 20 billion allocated to healthcare development projects in recent years. Advanced technologies such as antimicrobial coatings and digital monitoring systems are gradually being adopted, with penetration rates reaching 35% in major urban hospitals. Trade partnerships and regulatory reforms are improving access to high-quality medical devices. A local distributor has increased product availability by 25% through strategic collaborations. Consumer behavior reflects a mix of premium adoption in private healthcare and cost-driven purchasing in public sectors.

United States Catheter Stabilization Device Market – 34% share: Strong healthcare infrastructure and high procedural volume exceeding 45 million catheter uses annually.

Germany Catheter Stabilization Device Market – 9% share: Advanced medical device regulations and high adoption of infection control technologies across hospitals.

The catheter stabilization device market is moderately fragmented, with over 25 active global and regional competitors competing across product innovation, pricing strategies, and distribution networks. The top five companies collectively account for approximately 58% of the market, indicating a competitive yet structured landscape. Leading players are focusing on product differentiation through antimicrobial coatings, silicone-based adhesives, and integrated digital monitoring capabilities. Strategic initiatives such as mergers and acquisitions have increased by 18% in the past three years, enabling companies to expand their product portfolios and geographic presence. Partnerships with hospitals and healthcare systems are also a key strategy, with over 40% of major players engaging in long-term supply agreements. Innovation remains central to competition, with more than 30% of companies investing in R&D to develop next-generation stabilization solutions. Additionally, new entrants are targeting niche segments such as home healthcare and outpatient care, intensifying competition and driving technological advancements across the market.

3M Company

Becton, Dickinson and Company (BD)

Baxter International Inc.

Smiths Medical

Cardinal Health

ConvaTec Group Plc

Centurion Medical Products

Merit Medical Systems

Medline Industries

Dale Medical Products, Inc.

Technological innovation in the catheter stabilization device market is centered on improving patient safety, reducing infection rates, and enhancing ease of application. One of the most significant advancements is the development of antimicrobial-embedded stabilization devices, which incorporate agents such as chlorhexidine and silver ions. These technologies have demonstrated the ability to reduce catheter-related bloodstream infections by up to 30%–40% in clinical settings, making them increasingly standard in critical care environments.

Another key area of innovation is the transition toward silicone-based and hydrocolloid adhesive platforms. These materials provide up to 35% better skin compatibility and reduce medical adhesive-related skin injuries, which affect nearly 20% of long-term catheter patients. Breathable adhesive technologies are also gaining traction, allowing moisture vapor transmission rates exceeding 800 g/m²/day, thereby improving skin integrity and patient comfort during extended use.

Mechanical stabilization systems are evolving with low-profile locking mechanisms that enhance catheter retention strength by approximately 25% compared to traditional tape methods. Additionally, hybrid systems combining adhesive and mechanical features are being adopted in high-mobility clinical environments, improving securement performance without compromising patient comfort.

Digital integration is an emerging frontier, with sensor-enabled catheter stabilization devices capable of detecting displacement or early infection indicators. These smart systems improve monitoring accuracy by over 30% and are being piloted in nearly 20% of advanced healthcare facilities. Furthermore, manufacturing technologies such as precision molding and automated assembly have increased production efficiency by 15%–20%, enabling scalability while maintaining product consistency. These advancements collectively position the market toward more intelligent, patient-centric, and clinically efficient stabilization solutions.

• In February 2025, 3M expanded its vascular access portfolio by enhancing its Tegaderm CHG dressing line with improved antimicrobial protection and extended wear time of up to 7 days, supporting better infection control protocols in hospitals. Source: www.3m.com

• In October 2024, Becton, Dickinson and Company (BD) introduced an updated StatLock catheter stabilization platform featuring enhanced adhesive technology that improves securement strength by approximately 20% while reducing skin irritation in long-term catheter patients. Source: www.bd.com

• In March 2025, Cardinal Health strengthened its medical products segment by launching advanced securement solutions designed for outpatient and home healthcare settings, focusing on ease of use and reducing catheter dislodgement incidents by nearly 25%. Source: www.cardinalhealth.com

• In August 2024, Medline Industries expanded its catheter securement product line with new antimicrobial stabilization devices aimed at lowering infection risks, achieving up to 28% reduction in catheter-related complications during initial hospital trials. Source: www.medline.com

The catheter stabilization device market report provides a comprehensive analysis of product types, applications, end-user segments, and geographic distribution, offering actionable insights for healthcare providers, manufacturers, and investors. The report covers key product categories including adhesive-based devices, mechanical stabilization systems, and hybrid securement solutions, with adhesive devices accounting for over 50% of total usage due to their clinical efficiency and ease of application.

From an application perspective, the report examines cardiovascular, urological, and general intravenous catheterization procedures, which collectively represent more than 90% of device utilization across healthcare settings. It also highlights emerging applications in home healthcare, where usage has increased by over 35% in recent years, reflecting the shift toward decentralized care models.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing variations in adoption rates, regulatory frameworks, and healthcare infrastructure. Developed regions demonstrate adoption rates exceeding 65% for advanced stabilization technologies, while emerging markets show rapid growth driven by expanding healthcare access and infrastructure investments.

The report further explores technological advancements such as antimicrobial coatings, silicone-based adhesives, and smart sensor integration, which are improving device performance and patient outcomes. It also includes analysis of regulatory trends, sustainability initiatives targeting up to 20% reduction in medical waste, and competitive dynamics involving more than 25 key market participants. Overall, the scope provides a detailed and structured view of current industry conditions and evolving opportunities within the catheter stabilization device market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3M Company, Becton, Dickinson and Company (BD), Baxter International Inc., Smiths Medical, Cardinal Health, ConvaTec Group Plc, Centurion Medical Products, Merit Medical Systems, Medline Industries, Dale Medical Products, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |