Reports

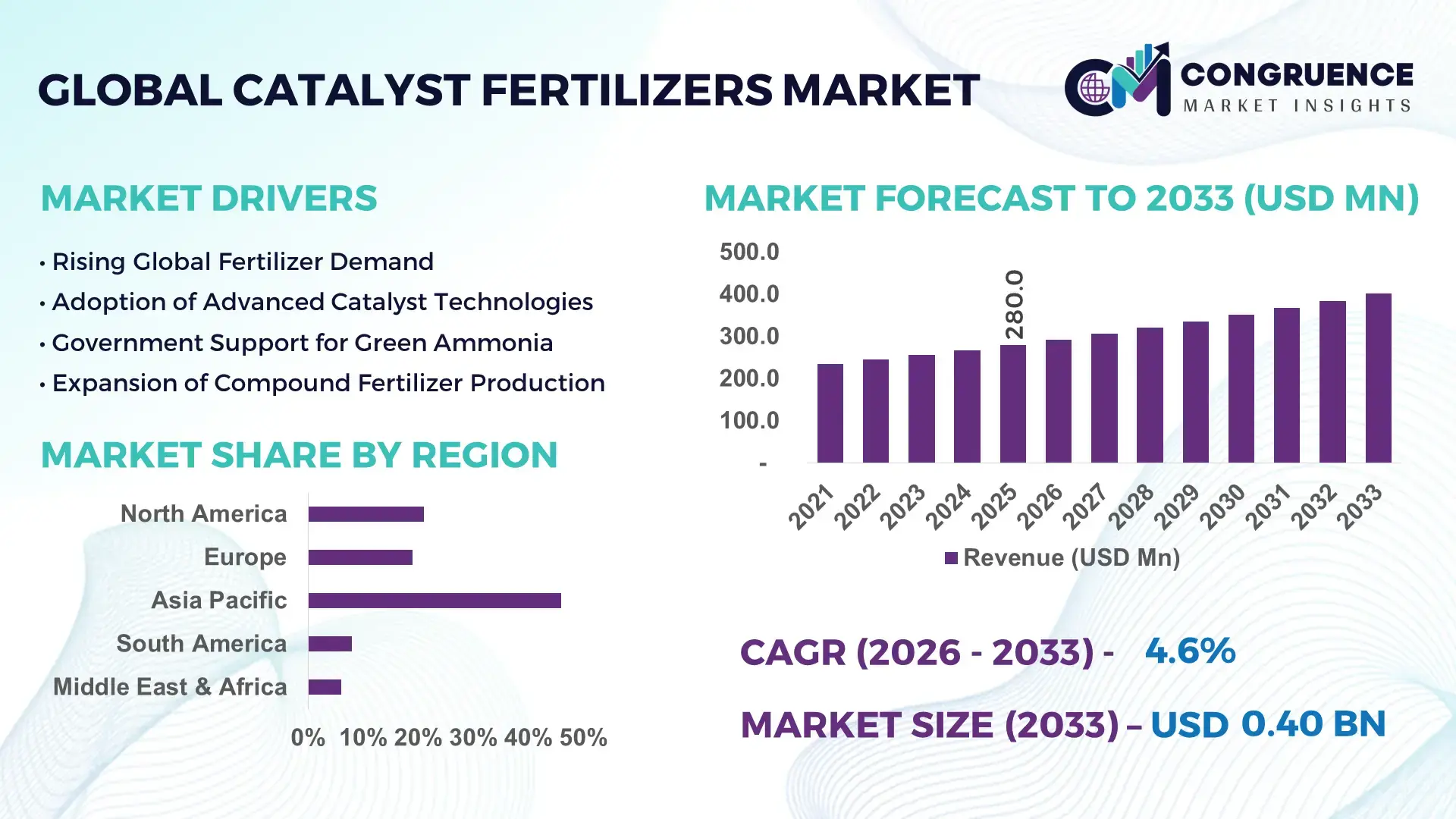

The Global Catalyst Fertilizers Market was valued at USD 280.0 Million in 2025 and is anticipated to reach a value of USD 401.2 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing adoption of catalytic additives in nitrogen-based fertilizers to enhance nutrient efficiency and reduce greenhouse gas emissions during production.

China represents the dominant country in the Catalyst Fertilizers Market, supported by its fertilizer production capacity exceeding 60 million metric tons of nitrogenous fertilizers annually. The country accounts for over 30% of global ammonia output, supported by more than 200 large-scale ammonia and urea production plants. Investments in catalytic reforming and low-NOx ammonia technologies have increased by nearly 18% over the past five years. Advanced oxidation catalysts are widely deployed across over 70% of newly commissioned ammonia plants to improve conversion efficiency and reduce energy consumption by approximately 10–12%. Domestic adoption of high-performance catalysts in compound fertilizer blending units has exceeded 45%, particularly in grain-producing provinces, reinforcing industrial-scale utilization and technology penetration.

Market Size & Growth: Valued at USD 280.0 Million in 2025, projected to reach USD 401.2 Million by 2033, expanding at 4.6% CAGR; growth is driven by efficiency optimization and emission reduction mandates in fertilizer manufacturing.

Top Growth Drivers: 35% increase in nitrogen efficiency adoption, 28% rise in low-emission catalyst deployment, 22% improvement in ammonia plant conversion efficiency.

Short-Term Forecast: By 2028, catalyst optimization technologies are expected to improve production energy efficiency by 15% and reduce nitrous oxide emissions by 12%.

Emerging Technologies: Nano-structured catalysts, AI-based process monitoring systems, and low-pressure ammonia synthesis catalysts.

Regional Leaders: Asia Pacific projected to reach USD 162.0 Million by 2033 with large-scale ammonia capacity expansion; North America to exceed USD 92.0 Million driven by emission compliance upgrades; Europe to approach USD 78.0 Million supported by green ammonia initiatives.

Consumer/End-User Trends: Over 60% of large fertilizer producers are integrating catalytic emission control systems; specialty fertilizer manufacturers show 25% higher adoption of advanced oxidation catalysts.

Pilot or Case Example: In 2024, a Chinese ammonia facility achieved 14% energy savings and 11% emission reduction through catalyst retrofitting.

Competitive Landscape: Market leader holds approximately 24% share, followed by Clariant, Johnson Matthey, Haldor Topsoe, and BASF.

Regulatory & ESG Impact: Stricter NOx emission regulations targeting 20% reduction by 2030 are accelerating catalyst upgrades across ammonia plants.

Investment & Funding Patterns: Over USD 500 Million invested globally in ammonia plant modernization and catalytic process enhancement projects during 2023–2025.

Innovation & Future Outlook: Integration of green hydrogen-based ammonia production and recyclable catalyst materials is shaping long-term sustainable expansion.

Nitrogen-based fertilizers contribute nearly 65% of catalyst demand, followed by phosphate blends at 20% and specialty micronutrient fertilizers at 15%. Recent innovations in nano-porous catalytic materials have improved reaction selectivity by 18%. Environmental mandates targeting 25% reduction in nitrous oxide emissions are influencing production upgrades, while Asia Pacific accounts for over 48% of global catalyst consumption. Growth in sustainable agriculture and green ammonia projects is strengthening long-term market prospects.

The Catalyst Fertilizers Market holds strong strategic relevance within the global agricultural value chain as fertilizer producers prioritize efficiency, compliance, and sustainability. Catalysts directly influence ammonia conversion rates, energy intensity, and emission control performance. Advanced nano-structured catalyst technology delivers 18% higher reaction efficiency compared to conventional iron-based catalytic standards, enabling measurable reductions in energy use per metric ton of ammonia produced. Asia Pacific dominates in production volume, while Europe leads in adoption intensity with over 62% of ammonia facilities integrating advanced emission-reduction catalyst systems.

Over the next two to three years, digital catalyst performance monitoring integrated with AI-driven predictive maintenance is expected to cut unplanned downtime by 20% by 2028. Companies are committing to ESG metrics, including 25% reductions in nitrous oxide emissions and 15% energy efficiency improvements by 2030. In 2024, China achieved a 14% energy consumption reduction in a major ammonia plant through catalyst retrofitting and process optimization initiatives.

Strategically, fertilizer manufacturers are aligning catalyst procurement with green hydrogen-based ammonia production projects to future-proof operations. Firms are investing in recyclable catalyst materials capable of extending lifecycle performance by 30%, reducing waste disposal costs. As carbon taxation frameworks expand and emission ceilings tighten globally, the Catalyst Fertilizers Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable agricultural growth.

The Catalyst Fertilizers Market is influenced by evolving agricultural productivity requirements, emission control mandates, and technological modernization of ammonia and urea production facilities. Increasing pressure to reduce nitrous oxide emissions—recognized as nearly 300 times more potent than CO₂—has compelled fertilizer manufacturers to upgrade catalytic systems. Over 55% of global ammonia production units have undergone partial modernization in the past decade. The market is also shaped by feedstock variability, particularly natural gas price fluctuations impacting operating efficiency strategies. Industrial decarbonization policies and green ammonia initiatives are reshaping investment priorities, while digital monitoring systems are improving catalyst lifecycle tracking by up to 20%. Regional capacity expansions in Asia and sustainability-led retrofitting projects in Europe and North America continue to influence supply-demand dynamics.

Global food demand is projected to increase by nearly 35% by 2050, requiring higher crop yields per hectare. Nitrogen-based fertilizers account for approximately 50% of global crop productivity improvements, making catalytic efficiency central to agricultural output. Advanced catalysts enhance ammonia synthesis conversion rates by up to 18%, reducing raw material consumption and energy intensity per ton produced. Over 40% of newly commissioned ammonia plants integrate secondary and tertiary catalyst beds to optimize yield. Additionally, regulatory mandates targeting 20% emission reductions have accelerated catalyst replacement cycles. The push for precision agriculture has further driven demand for controlled-release fertilizers, increasing the need for advanced catalytic blending technologies that improve nutrient availability by 15%.

Catalyst performance is closely tied to feedstock quality and stable operating temperatures. Natural gas accounts for nearly 60–70% of ammonia production costs, and price volatility exceeding 25% annually in some regions affects capital allocation for catalyst upgrades. Smaller fertilizer producers often delay retrofitting projects due to high installation and downtime costs, which can temporarily reduce plant output by 8–10%. Additionally, spent catalyst disposal and regeneration processes require compliance with hazardous waste regulations, increasing operational expenses. Limited technical expertise in emerging economies also slows adoption of advanced nano-structured catalysts, creating uneven global penetration rates and extending replacement cycles beyond optimal performance windows.

Green ammonia production, powered by renewable hydrogen, is expanding rapidly with over 30 announced global projects as of 2025. These facilities require next-generation catalysts capable of operating efficiently at lower pressures and variable hydrogen purity levels. Advanced catalysts designed for electrolysis-based hydrogen feedstocks demonstrate up to 15% higher stability under intermittent renewable energy supply conditions. Governments in Europe and Asia have introduced incentive frameworks targeting 25% decarbonization in fertilizer production by 2030. Adoption of recyclable catalyst materials, extending operational life by 30%, further creates cost-optimization opportunities. Integration with carbon capture technologies also opens additional application segments for emission-control catalysts within fertilizer plants.

Compliance with tightening emission norms, including nitrous oxide and NOx thresholds, requires continuous catalyst performance validation and monitoring. Plants failing to meet emission benchmarks may face penalties equivalent to 5–10% of operational expenditure in certain jurisdictions. Certification procedures for new catalyst formulations can extend beyond 18 months, delaying commercialization. Variability in regional environmental standards creates complexity for multinational fertilizer producers operating across multiple compliance frameworks. Furthermore, catalyst deactivation due to impurities such as sulfur compounds can reduce performance by 12–15%, necessitating more frequent regeneration or replacement. These technical and regulatory hurdles increase lifecycle management costs and complicate cross-border standardization efforts.

18% Efficiency Gains from Nano-Structured Catalysts: Adoption of nano-porous and high-surface-area catalysts has increased by 32% since 2022. These materials improve ammonia conversion efficiency by up to 18% while reducing operating pressure by 10%. Over 45% of newly upgraded nitrogen plants are deploying nano-structured catalytic beds to enhance reaction selectivity and extend lifecycle performance by 25%.

20% Reduction in Emissions through Advanced Oxidation Systems: Secondary and tertiary catalytic emission control systems are now installed in over 60% of large-scale ammonia facilities. These systems reduce nitrous oxide emissions by 20% and improve environmental compliance reporting accuracy by 15%. Adoption is strongest in Europe and North America where emission standards require sub-0.5 kg N₂O per ton of nitric acid production.

15% Energy Savings via Digital Catalyst Monitoring: More than 38% of tier-one fertilizer producers have integrated AI-enabled process analytics with catalyst monitoring platforms. Real-time temperature and pressure optimization has lowered energy consumption by approximately 15% while reducing unscheduled downtime by 12%. Predictive maintenance models are improving catalyst utilization rates by 20%.

30% Lifecycle Extension through Recyclable Catalyst Materials: Recyclable and regenerable catalyst technologies have gained 27% adoption across ammonia and urea production units. These solutions extend usable catalyst life by nearly 30% and reduce hazardous waste generation by 22%. Manufacturers are increasingly investing in closed-loop regeneration systems to support ESG commitments and operational sustainability targets.

The Catalyst Fertilizers Market is segmented by type, application, and end-user, reflecting the diverse operational requirements of ammonia, nitric acid, and compound fertilizer production facilities. From a product standpoint, catalyst selection is closely aligned with feedstock composition, pressure conditions, and emission compliance standards. Nitrogen synthesis catalysts account for the largest installed base due to their central role in ammonia production, which supports over 60% of global fertilizer output. Application segmentation highlights ammonia synthesis and nitric acid production as core demand centers, driven by regulatory mandates targeting nitrous oxide reduction and process efficiency optimization. End-user segmentation indicates that large-scale integrated fertilizer manufacturers represent the dominant adoption group, given their higher capital expenditure capacity and stricter environmental compliance obligations. Meanwhile, specialty fertilizer producers and green ammonia developers are emerging as high-potential adopters of next-generation catalytic technologies, particularly those enabling lower-pressure and renewable hydrogen-based synthesis.

The Catalyst Fertilizers Market by type includes Ammonia Synthesis Catalysts, Nitric Acid Catalysts, DeNOx Catalysts, Reforming Catalysts, and Specialty Blending Catalysts. Ammonia Synthesis Catalysts currently account for approximately 48% of total adoption due to their essential function in nitrogen fixation, which underpins nearly 70% of global fertilizer production processes. Nitric Acid Catalysts hold close to 27%, primarily deployed in nitric acid plants to reduce nitrous oxide emissions and improve oxidation efficiency. However, DeNOx Catalysts represent the fastest-growing type, expanding at an estimated CAGR of 6.8%, driven by tightening emission standards requiring up to 20% additional reduction in NOx levels across industrial fertilizer facilities. Reforming Catalysts and Specialty Blending Catalysts collectively contribute around 25% of market adoption, supporting feedstock pre-treatment and micronutrient fertilizer manufacturing. Reforming Catalysts enhance hydrogen purity by nearly 12%, while Specialty Blending Catalysts improve nutrient stabilization in controlled-release fertilizers by approximately 15%.

Application-wise, the Catalyst Fertilizers Market is segmented into Ammonia Production, Nitric Acid Production, Compound Fertilizer Manufacturing, and Emission Control Systems. Ammonia Production dominates with nearly 52% of total catalyst utilization, reflecting ammonia’s foundational role in urea and nitrate fertilizer manufacturing. Nitric Acid Production accounts for approximately 24%, supported by oxidation catalysts designed to lower nitrous oxide emissions below 0.5 kg per ton of output. However, Emission Control Systems represent the fastest-growing application, expanding at an estimated CAGR of 7.2%, driven by regulatory frameworks mandating up to 25% reduction in industrial greenhouse gas emissions by 2030. Compound Fertilizer Manufacturing and other niche applications collectively hold about 24%, particularly in specialty nutrient blends and slow-release fertilizer segments. In 2025, more than 44% of fertilizer plants globally reported integrating catalyst-based emission control upgrades. Additionally, nearly 38% of large-scale producers are piloting AI-enabled catalyst monitoring systems to enhance operational efficiency.

By end-user, the Catalyst Fertilizers Market is categorized into Large Integrated Fertilizer Manufacturers, Specialty Fertilizer Producers, Independent Ammonia Producers, and Green Ammonia Developers. Large Integrated Fertilizer Manufacturers account for approximately 55% of total catalyst adoption due to their multi-plant operations and stricter compliance mandates. Specialty Fertilizer Producers hold around 18%, focusing on enhanced-efficiency and micronutrient-enriched formulations. Independent Ammonia Producers represent nearly 15%, supplying feedstock for downstream fertilizer blending operations. Green Ammonia Developers are the fastest-growing end-user segment, expanding at an estimated CAGR of 8.1%, supported by over 30 announced renewable hydrogen-based ammonia projects globally. These facilities require advanced catalysts capable of maintaining stability under variable hydrogen purity and intermittent renewable energy supply. In 2025, nearly 42% of newly planned ammonia projects incorporated low-pressure catalytic technologies. Furthermore, more than 40% of large fertilizer enterprises reported upgrading catalyst systems to align with carbon reduction commitments.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific’s leadership is supported by more than 60% of global ammonia production capacity and over 55% of nitrogen fertilizer consumption concentrated in China and India. The region operates over 300 large-scale ammonia and nitric acid plants, many of which have integrated advanced iron-based and oxidation catalyst systems. North America holds approximately 21% of the market, driven by modernization of over 70 ammonia facilities and emission compliance upgrades. Europe represents nearly 19% of total demand, reflecting strong regulatory pressure to reduce nitrous oxide emissions by up to 25% by 2030. South America accounts for around 8%, supported by Brazil’s expanding fertilizer blending capacity exceeding 45 million metric tons annually. The Middle East & Africa collectively hold 6%, anchored by large-scale ammonia export hubs in the Gulf region producing more than 20 million metric tons annually.

North America represents approximately 21% of the global Catalyst Fertilizers Market, supported by over 70 operational ammonia plants and more than 25 nitric acid production facilities. The region’s fertilizer industry produces nearly 18 million metric tons of ammonia annually, with catalyst upgrades focused on achieving emission reductions of up to 20%. Regulatory frameworks such as federal clean air standards require continuous monitoring of nitrous oxide and NOx emissions, accelerating retrofitting projects. Key industries driving demand include large integrated fertilizer manufacturers and independent ammonia producers supplying agricultural and industrial sectors. Over 40% of producers have adopted AI-enabled catalyst performance monitoring systems to reduce downtime by 12%. A leading regional player, CF Industries, has invested in modernization initiatives incorporating advanced reforming catalysts to improve hydrogen efficiency by nearly 10%. Regional consumer behavior reflects higher enterprise-level adoption of digital optimization technologies, particularly in agriculture-driven states and industrial hubs.

Europe accounts for nearly 19% of the Catalyst Fertilizers Market, with Germany, France, and the UK leading regional adoption. The region operates more than 40 major ammonia and nitric acid plants, many undergoing upgrades to comply with emission reduction targets of 25% by 2030. Sustainability initiatives aligned with carbon reduction frameworks are prompting rapid integration of secondary and tertiary emission-control catalysts. Germany contributes significantly through advanced chemical manufacturing infrastructure, while France emphasizes green ammonia pilot projects. Approximately 62% of fertilizer producers in the region have implemented advanced nitrous oxide abatement catalysts. Yara International has deployed next-generation catalyst systems across several European facilities, achieving emission reductions exceeding 15%. Regulatory pressure drives demand for measurable and transparent emission performance, influencing procurement strategies toward recyclable catalyst materials and closed-loop regeneration systems.

Asia-Pacific holds the largest share at 46% and ranks first in global catalyst consumption volume. China, India, and Japan are the top consuming countries, collectively producing more than 65 million metric tons of ammonia annually. The region hosts over 300 ammonia and urea plants, with modernization programs improving energy efficiency by up to 12%. Infrastructure expansion, particularly in India’s fertilizer self-sufficiency initiatives, has resulted in over 15 new ammonia projects commissioned between 2022 and 2025. Technological innovation hubs in China are advancing nano-structured catalyst development, increasing reaction efficiency by approximately 18%. A major Chinese fertilizer producer recently upgraded oxidation catalyst systems across multiple nitric acid plants, reducing nitrous oxide emissions by 11%. Regional adoption patterns show strong demand from large-scale agricultural producers, with nearly 50% of facilities prioritizing efficiency-focused retrofits.

South America accounts for approximately 8% of the Catalyst Fertilizers Market, led by Brazil and Argentina. Brazil alone consumes over 40 million metric tons of fertilizers annually, driving steady demand for ammonia and nitric acid catalysts. Infrastructure investments in domestic ammonia production aim to reduce import dependency by nearly 20%. Energy sector developments, including natural gas exploration, support feedstock availability for fertilizer production. Government incentives promoting agricultural output expansion by 15% over the next decade are encouraging plant upgrades. Petrobras has initiated energy efficiency programs within fertilizer-linked operations, improving process stability and reducing emissions intensity. Regional adoption trends indicate demand closely tied to agribusiness cycles, with large soybean and corn producers influencing fertilizer blending and catalyst utilization patterns.

The Middle East & Africa region represents around 6% of the Catalyst Fertilizers Market, anchored by major ammonia production hubs in the UAE and Saudi Arabia, collectively producing more than 20 million metric tons annually. Export-oriented fertilizer manufacturing drives sustained catalyst consumption. Technological modernization initiatives aim to enhance hydrogen reforming efficiency by 10–12%. In Africa, South Africa leads regional adoption through nitric acid plant upgrades aligned with environmental compliance requirements. Trade partnerships with Asian and European fertilizer importers encourage capacity expansion projects. A leading Gulf-based producer has integrated advanced reforming catalysts to extend catalyst lifecycle by nearly 25%. Regional behavior reflects strong industrial-scale demand, particularly within export-driven ammonia complexes and infrastructure-supported industrial zones.

China – 32% Market Share: Leadership supported by over 60 million metric tons annual nitrogen fertilizer production capacity and large-scale ammonia plant modernization programs.

United States – 14% Market Share: It is driven by advanced emission compliance upgrades across more than 70 ammonia production facilities and high adoption of digital catalyst monitoring systems.

The Catalyst Fertilizers Market is moderately consolidated, with the top five companies collectively accounting for approximately 58% of global market share. More than 35 active competitors operate across ammonia synthesis, nitric acid oxidation, reforming, and emission-control catalyst segments. The competitive environment is characterized by high technical barriers to entry, given that catalyst performance directly influences ammonia conversion rates, which can vary by 10–18% depending on formulation quality and operating conditions.

Market leaders focus heavily on R&D, allocating an estimated 6–9% of annual operating budgets toward catalyst innovation, particularly nano-structured materials and recyclable catalyst systems capable of extending lifecycle performance by up to 30%. Strategic initiatives include multi-year supply agreements with fertilizer producers operating more than 50 ammonia plants globally, as well as partnerships to support green ammonia pilot projects exceeding 25 announced facilities worldwide.

Product launches emphasizing low-pressure synthesis compatibility and advanced DeNOx abatement technologies have intensified competition. Several players are investing in digital catalyst monitoring platforms that reduce unplanned downtime by nearly 12% and improve process optimization accuracy by 15%. Mergers and technology collaborations are increasingly targeting carbon capture integration and hydrogen reforming efficiency improvements of 10–12%, reinforcing innovation-led differentiation.

BASF SE

Honeywell International Inc.

Axens Group

LKAB Minerals

JGC Catalysts and Chemicals Ltd.

Dorf Ketal Chemicals

Süd-Chemie India Pvt. Ltd.

Quality Magnetite

Unicat Catalyst Technologies

Porocel Corporation

KBR Inc.

Thyssenkrupp Uhde

Technological advancements in the Catalyst Fertilizers Market are centered on improving reaction efficiency, reducing greenhouse gas emissions, and extending catalyst lifespan. Iron-based ammonia synthesis catalysts remain the industry standard, supporting over 70% of global ammonia production. However, next-generation nano-structured catalysts with enhanced surface area are improving nitrogen conversion efficiency by up to 18% while lowering operating pressure requirements by nearly 10%.

Secondary and tertiary nitric acid catalysts are increasingly deployed to reduce nitrous oxide emissions by up to 20%, aligning with industrial decarbonization targets. More than 60% of newly modernized nitric acid plants incorporate advanced abatement catalyst systems capable of achieving emission thresholds below 0.5 kg N₂O per ton of production.

Digital transformation is also reshaping catalyst lifecycle management. AI-driven process optimization platforms are now integrated into approximately 40% of large-scale ammonia facilities, improving temperature control accuracy by 15% and reducing catalyst degradation rates by 12%. Predictive analytics models extend operational life by nearly 20% through early detection of deactivation caused by sulfur or other impurities.

Emerging technologies include catalysts designed for green ammonia production using renewable hydrogen feedstocks. These formulations demonstrate up to 15% greater stability under intermittent energy supply conditions. Additionally, recyclable catalyst materials capable of recovering more than 80% of active metal content are gaining traction, supporting circular economy objectives and reducing hazardous waste generation by 22%.

• In March 2024, Clariant launched CLARITY™ Prime, an advanced AI-powered digital service for optimizing catalyst operations across ammonia, methanol, and hydrogen plants. The platform offers machine-learning-based performance projections and automated health alerts, with Indorama Eleme Fertilizer & Chemicals being the first customer to implement the service at its ammonia plant in Port Harcourt, Nigeria. Source: www.clariant.com

• In July 2025, Clariant and Shanghai Electric formalized a strategic alliance focused on advancing China’s energy transition by sharing high-performance catalysts for producing green methanol, green ammonia, and sustainable fuels. The cooperation enhances China’s capacity in clean chemical production and strengthens Clariant’s footprint in large-scale sustainable projects. Source: www.clariant.com

• In November 2025, Clariant signed a 10-year contract to expand CLARITY Prime digital services with SECCO Petrochemicals in Shanghai. Under the agreement, Clariant will provide 24/7 AI-driven catalyst performance monitoring and optimization support for SECCO’s 900-KTA ethylene plant, boosting reliability, safety, and operational efficiency. Source: www.pressreleasefinder.com

• In November 2025, Topsoe was selected by Synergen Green Energy to supply its proprietary ammonia production technology license and fertilizer catalysts for planned green ammonia facilities in the United States, targeting production capacities of approximately 210,000 metric tons per year and improved operational efficiency.

The Catalyst Fertilizers Market Report provides comprehensive coverage of product types including ammonia synthesis catalysts, nitric acid oxidation catalysts, DeNOx catalysts, reforming catalysts, and specialty blending catalysts. The analysis spans core applications such as ammonia production, nitric acid manufacturing, emission control systems, and compound fertilizer blending. More than 60% of global catalyst demand is linked to nitrogen-based fertilizer production, making process efficiency and emission management central focus areas.

Geographically, the report evaluates five key regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—covering over 30 major fertilizer-producing countries. It assesses production infrastructure including more than 300 ammonia plants worldwide and examines modernization trends impacting over 55% of existing facilities.

Technological scope includes nano-structured catalytic materials, low-pressure synthesis catalysts, AI-enabled catalyst monitoring platforms, recyclable catalyst systems, and green ammonia-compatible formulations. The report also examines industrial decarbonization initiatives targeting up to 25% emission reduction across fertilizer manufacturing by 2030.

In addition to mainstream fertilizer applications, the scope includes niche segments such as renewable hydrogen-integrated ammonia synthesis, carbon capture-enabled catalytic systems, and extended lifecycle regeneration technologies capable of improving operational durability by up to 30%. The report is structured to support strategic decision-making across production optimization, sustainability planning, investment prioritization, and competitive benchmarking within the Catalyst Fertilizers Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 280.0 Million |

| Market Revenue (2033) | USD 401.2 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Clariant AG; Johnson Matthey Plc; Topsoe A/S; BASF SE; Honeywell International Inc.; Axens Group; LKAB Minerals; JGC Catalysts and Chemicals Ltd.; Dorf Ketal Chemicals; Süd-Chemie India Pvt. Ltd.; Quality Magnetite; Unicat Catalyst Technologies; Porocel Corporation; KBR Inc.; Thyssenkrupp Uhde |

| Customization & Pricing | Available on Request (10% Customization Free) |