Reports

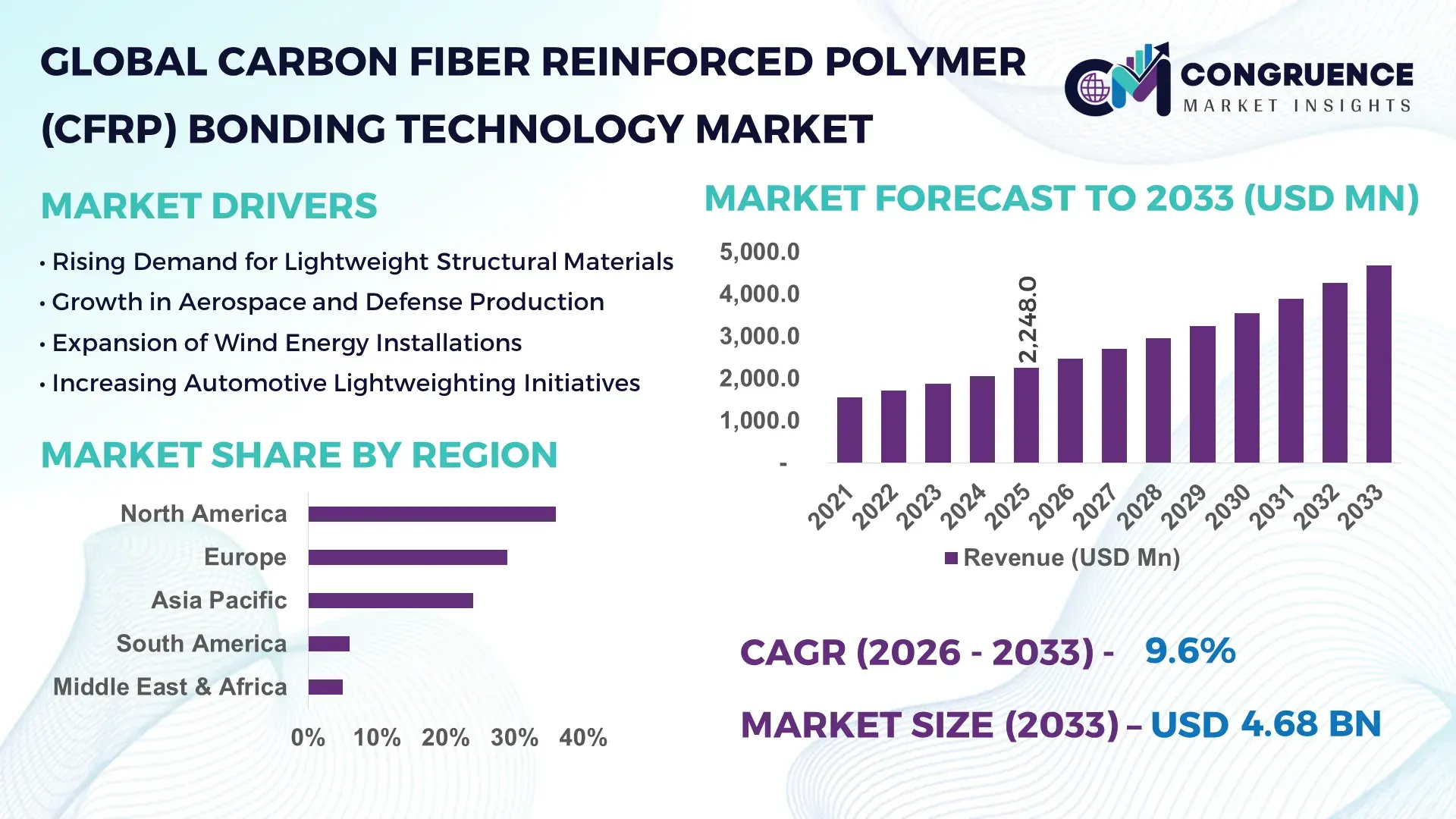

The Global Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market was valued at USD 2,248.0 Million in 2025 and is anticipated to reach a value of USD 4,680.4 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding due to increasing structural lightweighting requirements across aerospace, automotive, wind energy, and high-performance infrastructure applications.

The United States stands as a dominant country in the Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market, supported by strong aerospace and defense manufacturing capacity exceeding 5,000 composite-intensive aircraft components annually. The country accounts for over 35% of global commercial aircraft production, where bonded CFRP structures are extensively used in fuselage sections and wing assemblies. U.S.-based automotive OEMs have increased CFRP component integration by over 28% in electric vehicle platforms since 2022. Annual investments in advanced composite manufacturing facilities surpassed USD 1.2 billion in 2024, including automation-driven bonding lines and robotic adhesive application systems. The wind energy sector has installed more than 140 GW of cumulative capacity, with bonded CFRP blades exceeding 80 meters in length, driving high-performance structural adhesive demand and continuous technological refinement in surface treatment and curing systems.

Market Size & Growth: USD 2,248.0 Million in 2025, projected to reach USD 4,680.4 Million by 2033 at 9.6% CAGR, driven by 32% rise in lightweight composite integration across mobility and aerospace sectors.

Top Growth Drivers: EV lightweighting adoption up 28%; aerospace composite usage exceeding 50% of new aircraft structures; wind blade length expansion by 35%.

Short-Term Forecast: By 2028, automated bonding systems are expected to reduce assembly cycle time by 22% and defect rates by 18%.

Emerging Technologies: Nano-enhanced structural adhesives; induction-based rapid curing systems; AI-enabled surface inspection improving bond reliability by 25%.

Regional Leaders: North America projected at USD 1,620 Million by 2033 with aerospace dominance; Europe at USD 1,280 Million driven by EV platforms; Asia-Pacific at USD 1,150 Million with industrial composite expansion.

Consumer/End-User Trends: Aerospace accounts for over 40% of bonded CFRP demand, automotive 30%, wind energy 18%, with rising adoption in marine and infrastructure retrofitting.

Pilot or Case Example: In 2024, a U.S. aerospace facility achieved 20% strength consistency improvement through robotic adhesive dispensing and in-line ultrasonic inspection.

Competitive Landscape: Market leader holds approximately 18% share, followed by Henkel, 3M, Sika, Huntsman, and Arkema.

Regulatory & ESG Impact: Emission standards targeting 30% weight reduction in transport platforms are accelerating structural bonding adoption.

Investment & Funding Patterns: Over USD 2.3 billion invested globally since 2023 in automated composite bonding lines and advanced adhesive R&D.

Innovation & Future Outlook: Hybrid bonding combining mechanical fastening and adhesive systems is projected to improve fatigue life by 35% in next-generation platforms.

Aerospace contributes over 40% of total demand, followed by automotive at nearly 30% and wind energy at 18%, reflecting diversified end-use penetration. Recent innovations include nano-reinforced epoxy adhesives improving shear strength by 15% and induction-based curing reducing bonding time by 25%. Stricter emission norms and lightweight mandates across North America and Europe are accelerating consumption. Asia-Pacific shows double-digit installation growth in composite-intensive infrastructure, reinforcing long-term structural bonding demand.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market holds strategic importance in enabling lightweight structural design, energy efficiency, and performance optimization across critical industries. As aerospace platforms now incorporate more than 50% composite materials by structural weight, bonding technologies have become central to load transfer efficiency, fatigue resistance, and corrosion mitigation. Advanced nano-toughened epoxy systems deliver 18% higher lap shear strength compared to conventional epoxy formulations, enhancing aircraft durability and reducing lifecycle maintenance costs.

Automation is reshaping competitive strategy. AI-enabled robotic dispensing systems deliver 22% cycle-time improvement compared to manual adhesive application, while inline thermographic inspection reduces bonding defects by 17% versus traditional visual inspection standards. North America dominates in production volume due to large-scale aerospace and defense manufacturing, while Europe leads in adoption intensity with over 60% of electric vehicle manufacturers integrating structural adhesive bonding in battery enclosures and chassis systems.

By 2028, AI-driven predictive curing analytics is expected to reduce production rework rates by 20% and optimize adhesive usage efficiency by 15%. Firms are committing to ESG performance improvements such as 25% reduction in solvent emissions and 30% recyclable adhesive packaging by 2030. In 2024, a major U.S. aerospace manufacturer achieved 19% structural weight reduction through automated CFRP bonding optimization and digital twin-based stress validation.

Looking ahead, the Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market is positioned as a foundational enabler of resilient supply chains, regulatory compliance, and sustainable lightweight innovation across next-generation industrial platforms.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market is shaped by rising lightweight material penetration, automation in composite assembly, and performance-driven design mandates. Structural bonding solutions are increasingly replacing mechanical fasteners, reducing component weight by 15–25% while improving fatigue life by over 30% in dynamic load environments. Aerospace production rates exceeding 1,500 commercial aircraft deliveries annually are directly influencing bonded composite assembly volumes. The automotive transition toward electric mobility, with EV production surpassing 14 million units globally in 2024, is expanding demand for battery enclosure bonding and crash-resistant composite integration. Meanwhile, wind turbine blade lengths exceeding 100 meters are intensifying requirements for high-durability adhesive systems capable of withstanding cyclic loads above 20 years of operational lifespan.

Over 50% of modern aircraft structural weight now comprises composite materials, necessitating advanced bonding systems capable of sustaining extreme thermal and mechanical stress. Electric vehicle manufacturers report up to 28% structural weight reduction using bonded CFRP battery housings compared to steel assemblies. Bonded joints distribute stress more uniformly, improving crash performance by 20% and reducing vibration fatigue by nearly 30%. Wind energy manufacturers have expanded blade lengths by 35% over the past five years, requiring high-strength bonding capable of withstanding multi-megapascal cyclic stress loads, significantly reinforcing demand for advanced adhesive formulations and precision curing technologies.

Advanced structural adhesives incorporate specialty resins and nano-fillers that increase material costs by 18–25% compared to conventional bonding agents. Surface preparation, curing validation, and non-destructive testing procedures can add 12–15% to overall assembly costs. Aerospace certification cycles often exceed 24 months, requiring extensive fatigue and environmental testing under stringent safety regulations. Additionally, curing energy consumption for autoclave-based bonding systems can increase operational expenditure by up to 20%, creating barriers for small-scale manufacturers and limiting rapid market penetration in cost-sensitive regions.

Automated robotic adhesive application improves placement precision by 30% and reduces material waste by 15%. AI-driven ultrasonic inspection technologies detect sub-surface defects with 95% accuracy, enhancing reliability in aerospace-grade assemblies. Rapid induction curing reduces bonding cycle time by 25%, enabling higher throughput in automotive production lines exceeding 500,000 units annually. Emerging hydrogen storage tanks made from bonded CFRP structures require ultra-high-strength adhesive systems capable of withstanding pressures above 700 bar, presenting significant industrial expansion opportunities in clean energy infrastructure.

Long-term durability testing under humidity, salt spray, and thermal cycling exceeding 1,000 hours is mandatory in aerospace and marine applications. Adhesive degradation risks under temperature fluctuations from –40°C to 120°C require advanced formulation stability. Regulatory requirements targeting 30% volatile organic compound reduction are pressuring manufacturers to reformulate solvent-based systems. Disposal and recycling of bonded composite structures remain complex, with less than 15% of thermoset composites currently recyclable at scale, presenting environmental and lifecycle management challenges.

32% Increase in Automated Robotic Bonding Lines: Over 32% of large aerospace and automotive composite facilities adopted robotic adhesive dispensing between 2022 and 2025. Automation has reduced bonding variability by 20% and improved throughput by 25%, particularly in North America and Germany where high-precision manufacturing standards drive efficiency benchmarks.

35% Expansion in Wind Blade Structural Bonding Demand: Wind turbine blades exceeding 100 meters now represent nearly 40% of new offshore installations. Structural adhesives used in spar cap and shear web bonding have improved fatigue life by 30%, supporting operational lifespans beyond 25 years under high cyclic loads.

28% Growth in EV Composite Battery Enclosure Bonding: Electric vehicle platforms integrating CFRP battery enclosures increased by 28% since 2023. Bonded assemblies have reduced enclosure weight by 22% and improved crash energy absorption by 18%, aligning with global emission reduction targets.

25% Reduction in Curing Time via Induction & Rapid Thermal Systems: Adoption of induction-based rapid curing systems has lowered bonding cycle time by 25% and energy consumption by 15%. These systems enable continuous composite assembly lines exceeding 10,000 bonded components per month in high-volume automotive production environments.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market is structured across three primary dimensions: type, application, and end-user industries. By type, the market comprises epoxy-based structural adhesives, polyurethane adhesives, acrylic adhesives, and hybrid/nano-modified systems, each tailored to performance, curing time, and environmental resistance requirements. Epoxy-based systems dominate due to their superior shear strength and thermal endurance, particularly in aerospace-grade bonding exceeding 120°C tolerance.

From an application standpoint, aerospace structural assembly represents the most intensive use case, followed by automotive lightweight platforms and wind turbine blade bonding. Increasing electrification and decarbonization mandates are shifting application demand toward battery enclosures and renewable energy infrastructure.

End-user segmentation reflects concentration in aerospace & defense, automotive OEMs, wind energy manufacturers, marine fabricators, and infrastructure retrofitting contractors. Aerospace and automotive collectively account for more than 70% of bonded CFRP consumption, while emerging hydrogen storage and modular infrastructure projects are expanding future addressable segments. This segmentation structure highlights diversified industrial dependency and evolving innovation pathways.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market by type includes epoxy-based adhesives, polyurethane adhesives, acrylic adhesives, and hybrid or nano-reinforced bonding systems. Epoxy-based adhesives currently account for approximately 48% of total adoption due to their high lap shear strength exceeding 35 MPa and superior fatigue resistance in aerospace fuselage and wing assemblies. Polyurethane adhesives hold nearly 22%, offering flexibility and impact absorption advantages in automotive crash structures. Acrylic adhesives represent around 14%, favored for rapid curing in industrial assembly lines. The remaining 16% comprises hybrid and nano-modified adhesive systems designed for extreme-temperature and high-pressure applications.

While epoxy systems lead in adoption, hybrid nano-reinforced adhesives are the fastest-growing type, expanding at an estimated CAGR of 12.4% due to their 18–22% improvement in impact resistance and enhanced crack propagation control. These systems are increasingly integrated into electric vehicle battery modules and hydrogen storage vessels operating above 700 bar pressure thresholds.

Application segmentation in the Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market spans aerospace structural assembly, automotive lightweight components, wind turbine blade manufacturing, marine structures, and infrastructure reinforcement. Aerospace accounts for approximately 42% of total application demand, supported by aircraft platforms comprising over 50% composite structural weight. Automotive applications represent about 30%, driven by electric vehicle chassis and battery enclosures achieving up to 22% mass reduction. Wind energy applications contribute nearly 18%, particularly in blades exceeding 100 meters requiring high-durability adhesive bonding.

Although aerospace leads in share, automotive bonding is the fastest-growing application segment, advancing at approximately 11.8% CAGR due to EV production expansion surpassing 14 million units annually. Marine and civil infrastructure collectively represent the remaining 10%, focusing on corrosion-resistant composite retrofitting.

In 2025, more than 41% of global automotive OEMs reported piloting automated composite bonding systems for EV battery enclosures. Additionally, over 35% of wind blade manufacturers transitioned to robotic adhesive application platforms to enhance bonding uniformity.

End-user segmentation includes aerospace & defense manufacturers, automotive OEMs, wind energy producers, marine builders, and infrastructure contractors. Aerospace & defense leads with approximately 44% of overall bonded CFRP consumption, as commercial and military aircraft increasingly rely on bonded composite fuselage sections and empennage structures. Automotive OEMs account for roughly 29%, integrating bonded CFRP into EV platforms and performance vehicles. Wind energy manufacturers represent 17%, while marine and infrastructure retrofitting collectively contribute around 10%.

Although aerospace dominates in volume, automotive OEMs are the fastest-growing end-user group, expanding at an estimated CAGR of 12.1%, fueled by EV platform scaling and crash-performance optimization. Over 46% of EV manufacturers globally reported structural adhesive integration in battery modules by 2025. Additionally, nearly 38% of large infrastructure contractors have adopted composite bonding systems for bridge reinforcement and seismic retrofitting projects.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

North America’s dominance is supported by aerospace production exceeding 1,500 commercial aircraft deliveries annually and electric vehicle output crossing 2.8 million units in 2025. Europe held approximately 29% share, driven by strong automotive electrification targets and offshore wind installations exceeding 35 GW cumulative capacity. Asia-Pacific captured nearly 24% share, supported by composite-intensive infrastructure development and over 50% of global EV manufacturing concentrated in China, Japan, and South Korea. South America accounted for around 6%, with Brazil leading regional aerospace assembly, while the Middle East & Africa represented nearly 5%, driven by wind energy expansion and high-performance infrastructure projects. Cross-regional digitalization trends show over 40% of large composite manufacturers integrating robotic bonding systems, while 33% have adopted AI-driven defect detection platforms to enhance structural reliability and compliance.

North America represents approximately 36% of the global Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market volume, primarily driven by aerospace & defense and electric vehicle manufacturing. The region produces over 35% of the world’s commercial aircraft, where bonded CFRP structures exceed 50% of structural weight in next-generation platforms. Automotive OEMs have expanded CFRP battery enclosure integration by 28% since 2023. Regulatory initiatives targeting 30% transport emission reduction by 2030 are accelerating structural lightweighting programs. Digital transformation is notable, with over 45% of Tier-1 aerospace suppliers implementing robotic adhesive dispensing systems. A leading regional player, 3M, has expanded structural adhesive manufacturing capacity by introducing advanced epoxy bonding systems optimized for high-temperature aerospace environments. Regional adoption patterns show higher enterprise implementation in aerospace and automotive manufacturing clusters, with strong preference for automated, AI-assisted quality inspection technologies.

Europe accounts for nearly 29% of global Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market demand, led by Germany, France, and the United Kingdom. Germany alone produces over 3.5 million vehicles annually, many incorporating bonded composite components in EV platforms. Offshore wind capacity surpassed 35 GW in 2025, requiring advanced adhesive bonding for turbine blades exceeding 90 meters. Regulatory frameworks emphasizing carbon neutrality by 2050 are pushing manufacturers toward solvent-free adhesive systems and recyclable composite solutions. Approximately 52% of European automotive OEMs have integrated structural bonding for battery enclosures. Companies such as Sika have expanded composite bonding portfolios, focusing on high-durability polyurethane systems for automotive lightweighting. Regional consumer behavior reflects strong regulatory-driven adoption, with manufacturers prioritizing low-VOC adhesives and ESG-compliant bonding technologies.

Asia-Pacific ranks third in market share at approximately 24% but leads in volume expansion of electric vehicle production, with China manufacturing over 9 million EV units annually. Japan and South Korea contribute significantly through aerospace component manufacturing and hydrogen storage development. Infrastructure modernization programs across India and Southeast Asia have driven a 20% rise in composite bridge reinforcement projects. Over 50% of global EV battery production occurs within the region, intensifying demand for high-strength CFRP bonding systems. Toray Industries has expanded carbon fiber output capacity by over 15% in recent years, reinforcing supply integration with advanced adhesive technologies. Regional behavior indicates strong manufacturing-driven adoption, with rapid implementation of automated bonding lines to support high-volume production environments.

South America accounts for approximately 6% of the global Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market. Brazil is the primary contributor, supported by regional aerospace manufacturing exceeding 200 commercial aircraft annually. Wind energy installations in Brazil surpassed 25 GW cumulative capacity, increasing demand for bonded composite blade components. Argentina is investing in renewable energy corridors, encouraging lightweight infrastructure reinforcement. Trade policies supporting industrial manufacturing modernization have facilitated composite technology imports. Local aerospace manufacturers have incorporated bonded CFRP fuselage panels to reduce structural fastener counts by nearly 25%. Regional adoption trends indicate growing preference for durable bonding systems in energy and aviation sectors, though overall industrial automation remains comparatively moderate.

The Middle East & Africa region represents approximately 5% of global Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market demand. The UAE and Saudi Arabia are investing heavily in renewable energy projects exceeding 10 GW combined capacity, incorporating composite-intensive structures. South Africa leads in wind energy expansion within the continent, with installations surpassing 3.5 GW. Mega infrastructure projects require corrosion-resistant composite reinforcement systems capable of withstanding extreme temperature fluctuations above 45°C. Technological modernization is evident, with 30% of large-scale contractors adopting automated composite bonding solutions. Regional trade partnerships are encouraging advanced materials imports to support aerospace maintenance hubs and offshore energy platforms. Consumer adoption patterns emphasize durability and climate-resilient bonding systems in oil & gas and infrastructure sectors.

United States – 31% Market Share: Dominates due to high aerospace production capacity, strong EV manufacturing expansion, and advanced automation integration in composite assembly lines.

Germany – 18% Market Share: Holds significant position, driven by automotive electrification leadership, offshore wind expansion, and strong regulatory push toward lightweight, low-emission mobility platforms.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market is moderately consolidated, with the top five companies collectively accounting for approximately 52% of global market share. More than 35 active global and regional competitors operate across structural adhesives, surface treatment solutions, and automated bonding systems. Market leaders differentiate themselves through high-performance epoxy and polyurethane formulations capable of exceeding 35 MPa lap shear strength and sustaining thermal resistance above 120°C.

Strategic initiatives increasingly focus on capacity expansion and advanced material innovation. Between 2023 and 2025, over 18 major product launches were recorded in nano-modified adhesive systems and rapid-curing technologies. Approximately 40% of leading manufacturers have integrated AI-enabled quality inspection tools into their composite bonding portfolios. Partnerships between adhesive manufacturers and aerospace OEMs have increased by 22% over the past two years, emphasizing long-term supply contracts and co-development programs.

The competitive environment is shaped by R&D intensity, with leading players allocating 4–6% of annual operating budgets to advanced composite bonding innovation. Automation-driven differentiation is accelerating, as over 30% of Tier-1 suppliers now offer robotic adhesive dispensing systems integrated with ultrasonic inspection. Mergers and acquisitions activity has remained steady, with at least 6 strategic acquisitions in specialty adhesive technologies since 2024, reinforcing technological depth and geographic expansion. The market’s competitive intensity is defined by performance certification, regulatory compliance, and long-term OEM integration rather than price competition alone.

Huntsman Corporation

Arkema S.A.

H.B. Fuller Company

Dow Inc.

LORD Corporation

Hexcel Corporation

Gurit Holding AG

Solvay S.A.

Toray Industries, Inc.

Permabond LLC

DELO Industrie Klebstoffe GmbH & Co. KGaA

Master Bond Inc.

Technological advancement in the Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market is centered on high-strength structural adhesives, rapid-curing systems, nano-enhanced formulations, and digital quality assurance. Epoxy-based structural adhesives remain dominant, delivering lap shear strengths above 35 MPa and fatigue resistance exceeding 1 million load cycles in aerospace validation tests. Polyurethane systems provide 20% higher flexibility compared to traditional epoxies, supporting automotive crash-energy absorption improvements of nearly 18%.

Nano-reinforced adhesive systems incorporating graphene and silica nanoparticles have demonstrated 15–22% improvements in impact resistance and crack propagation control. These systems are increasingly deployed in hydrogen storage tanks rated above 700 bar pressure. Induction and microwave-assisted curing technologies reduce bonding cycle time by up to 25%, supporting high-volume EV production lines exceeding 10,000 bonded assemblies per month.

Automation integration is another defining trend. Robotic adhesive dispensing platforms improve placement accuracy by 30% and reduce material waste by 12–15%. Inline ultrasonic and thermographic inspection technologies detect sub-surface bonding defects with 95% reliability, significantly reducing post-production rework. Digital twin simulations are being adopted by over 28% of aerospace composite manufacturers to predict stress distribution across bonded joints before physical validation. Sustainability-focused technologies, including solvent-free and low-VOC adhesives, are gaining traction as regulatory frameworks target 30% emission reductions by 2030. These innovations collectively enhance structural durability, operational efficiency, and regulatory compliance across critical end-use industries.

• In January 2026, Toray Industries, Inc. completed successful testing of an innovative bonding technique that joins thermoset and thermoplastic CFRP aircraft structures at nearly three times the speed of conventional adhesive and mechanical bonding methods, enhancing bond strength while significantly boosting assembly productivity in aerospace applications. Source: www.plasticstoday.com

• In March 2024, Arkema expanded its high-performance adhesive capabilities through the acquisition of Ashland’s performance adhesives business, absorbing advanced structural adhesive technologies designed for aerospace and industrial composite bonding, thus broadening its materials portfolio and manufacturing footprint.

• In April 2025, Henkel AG & Co. KGaA introduced new eco-friendly epoxy structural adhesive solutions with enhanced bond strength and reduced curing time specifically tailored for automotive lightweight composite components, aligning with stringent environmental mandates and advanced manufacturing performance demands.

• In August 2024, Arkema (through its Bostik brand) announced a production expansion in Southeast Asia, targeting high-performance and specialty adhesive technologies to better serve rising regional composite bonding demand across automotive, aerospace, packaging, and industrial applications.

The Carbon Fiber Reinforced Polymer (CFRP) Bonding Technology Market Report provides comprehensive coverage across material types, applications, end-user industries, and geographic regions. The scope encompasses structural adhesive systems including epoxy, polyurethane, acrylic, and hybrid nano-modified formulations designed for aerospace, automotive, wind energy, marine, and infrastructure applications. It evaluates over 4 primary product categories and analyzes performance benchmarks such as shear strength above 30 MPa, thermal tolerance exceeding 120°C, and fatigue life surpassing 1 million cycles.

Geographically, the report covers five major regions and more than 15 key countries contributing to global demand, including the United States, Germany, China, Japan, Brazil, and the UAE. Application-level insights include aerospace structural bonding representing over 40% of adoption, automotive lightweight integration near 30%, and wind energy installations exceeding 18% share.

The report further examines automation penetration, where approximately 40% of large composite manufacturers have adopted robotic adhesive systems, and digital inspection integration exceeding 30% in aerospace-grade production facilities. Emerging niche segments such as hydrogen storage tanks, composite pressure vessels, and modular infrastructure reinforcement are evaluated for strategic growth potential. The analysis supports decision-makers by outlining technology advancements, regulatory influences, ESG considerations, and competitive positioning within a performance-driven industrial ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,248.0 Million |

| Market Revenue (2033) | USD 4,680.4 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M; Henkel AG & Co. KGaA; Sika AG; Huntsman Corporation; Arkema S.A.; H.B. Fuller Company; Dow Inc.; LORD Corporation; Hexcel Corporation; Gurit Holding AG; Solvay S.A.; Toray Industries, Inc.; Permabond LLC; DELO Industrie Klebstoffe GmbH & Co. KGaA; Master Bond Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |