Reports

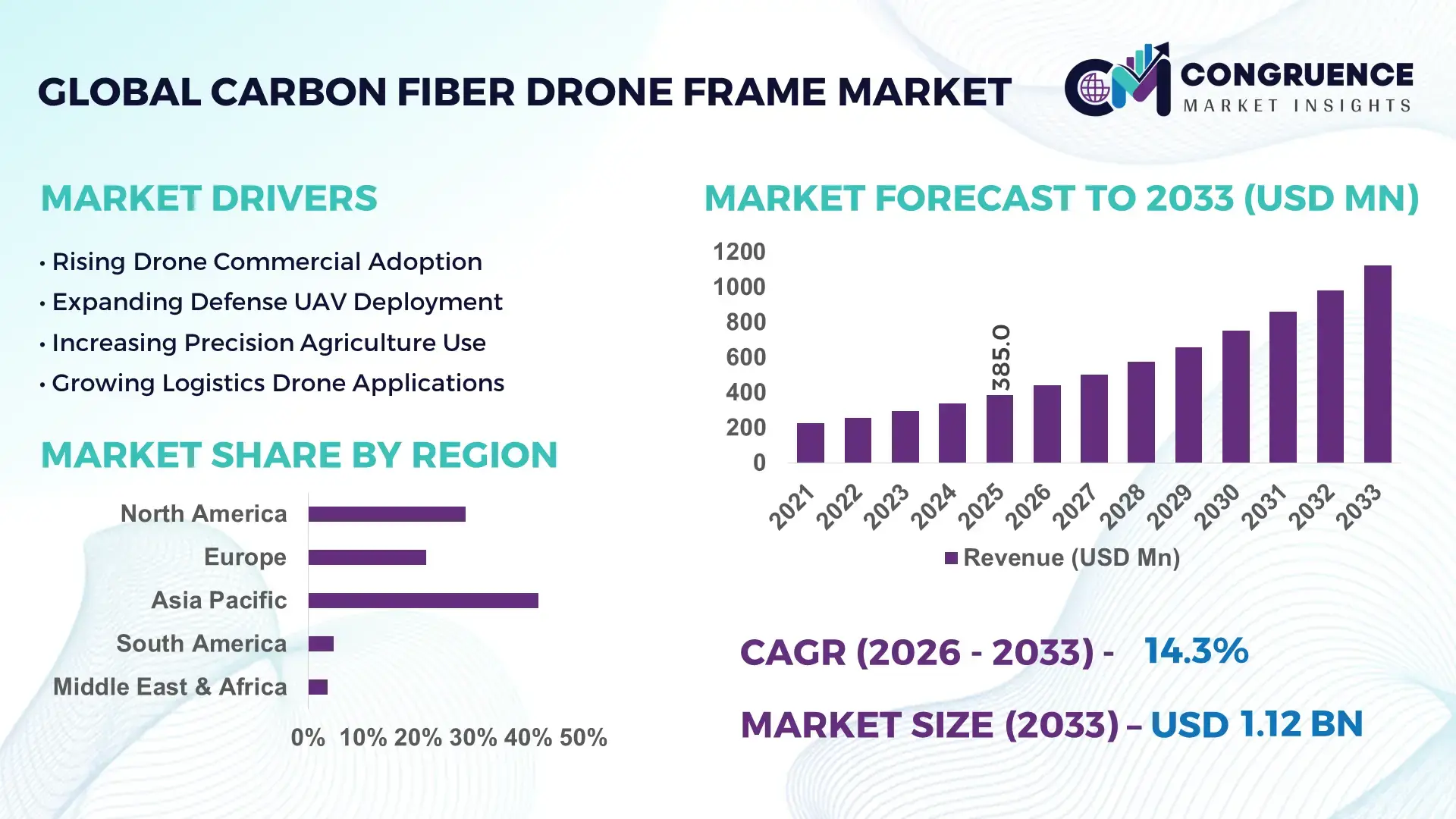

The Global Carbon Fiber Drone Frame Market was valued at USD 385.0 Million in 2025 and is anticipated to reach a value of USD 1,121.6 Million by 2033 expanding at a CAGR of 14.3% between 2026 and 2033. Growth is being accelerated by rising deployment of lightweight UAV platforms across defense surveillance, industrial inspection, precision agriculture, and commercial logistics applications where high-strength carbon fiber structures improve payload efficiency and flight endurance.

China remains the dominant country in the carbon fiber drone frame ecosystem, accounting for approximately 38% of global drone manufacturing output and over 45% of commercial UAV exports, supported by large-scale aerospace composites production and advanced manufacturing clusters. In comparison, the United States maintains stronger defense-oriented drone adoption, while China leads in production scale and supply-chain integration. Government-backed low-altitude economy initiatives and expanding industrial drone fleets have increased carbon composite utilization rates by more than 25% across leading manufacturers.

Strategically, companies that secure composite material supply chains and advanced frame-design capabilities are positioned to capture higher-value opportunities across next-generation autonomous drone programs.

Market Size & Growth: USD 385.0 Million in 2025, projected to reach USD 1,121.6 Million by 2033, driven by lightweight composite adoption that reduces drone structural weight by up to 30%.

Top Growth Drivers: Defense UAV procurement (+22%), industrial inspection drone deployment (+18%), and precision agriculture drone usage (+16%) are accelerating demand.

Short-Term Forecast: By 2028, advanced frame architectures are expected to improve payload efficiency by 20% while reducing maintenance requirements by 15%.

Emerging Technologies: AI-assisted flight control, automated composite manufacturing, and topology-optimized carbon structures are improving operational performance.

Regional Leaders: Asia-Pacific (USD 460+ Million), North America (USD 320+ Million), and Europe (USD 210+ Million) benefit from expanding commercial drone ecosystems and aerospace investments.

Consumer/End-User Trends: More than 55% of industrial drone operators prioritize lightweight airframes to extend mission duration and payload capacity.

Pilot/Case Example: In 2024, advanced carbon-fiber inspection drones demonstrated flight endurance improvements exceeding 18% versus conventional frame designs.

Competitive Landscape: The top five manufacturers collectively control nearly 42% of market activity, including AeroXcraft, Holybro, Tarot-RC, T-Motor, and iFlight.

Regulatory & ESG Impact: Low-emission drone operations reduce inspection-related vehicle travel by over 35%, supporting sustainability and infrastructure monitoring goals.

Investment & Funding: More than USD 1.2 Billion has been directed toward drone manufacturing, composite materials, and UAV ecosystem expansion globally since 2023.

Innovation & Future Outlook: Modular carbon-fiber platforms, autonomous fleet integration, and digital-twin-based frame engineering are reshaping competitive positioning.

Carbon Fiber Drone Frame Market demand is increasingly concentrated in defense reconnaissance, energy infrastructure inspection, precision agriculture, and commercial mapping operations. Manufacturers are introducing high-modulus composite structures and modular airframe designs that improve durability while lowering weight. More than 40% of newly launched industrial UAV platforms now incorporate advanced carbon-composite architectures. Ongoing low-altitude airspace reforms and supply-chain localization initiatives are further strengthening market development, creating a foundation for broader strategic expansion.

Carbon fiber drone frames are becoming strategically important as governments, industrial operators, and technology companies prioritize longer-endurance UAV operations, lower lifecycle costs, and mission-specific performance optimization. The market is increasingly linked to defense modernization, critical infrastructure monitoring, and autonomous aerial operations. Supply-chain restructuring efforts following geopolitical trade disruptions have accelerated investments in localized composite manufacturing and advanced materials capabilities.

Compared with conventional aluminum-based structures, carbon fiber drone frames deliver up to 30% lower structural weight while improving strength-to-weight performance by more than 20%, enabling higher payload efficiency and extended flight duration. China continues to lead large-scale manufacturing and commercial deployment, while the United States focuses on defense-grade UAV innovation and specialized aerospace applications. Europe is strengthening adoption through industrial inspection and infrastructure digitization programs.

Recent deployments in utility-grid inspection and pipeline monitoring demonstrate how lightweight airframes improve operational coverage while reducing maintenance cycles. Manufacturers are expanding composite production capacity, establishing strategic supplier agreements, and pursuing technology partnerships to secure advanced material access. Over the next two to three years, increasing autonomous drone integration and rising industrial fleet utilization are expected to elevate demand for specialized frame platforms. Organizations that combine advanced composite engineering, supply resilience, and application-specific design capabilities will secure stronger competitive positioning and long-term operational advantage.

Industrial and defense operators are prioritizing lightweight airframe technologies to improve flight endurance, payload capacity, and mission flexibility. Carbon fiber structures reduce frame weight by up to 30% while increasing structural rigidity by nearly 25%, making them increasingly attractive for surveillance, mapping, and inspection applications. Defense drone procurement programs have expanded by more than 20% across several major economies, while industrial drone deployments continue rising in energy and infrastructure sectors. This operational shift is creating sustained demand for advanced composite frame solutions. In response, manufacturers are investing in automated composite fabrication, strengthening aerospace-grade material partnerships, and expanding production capacity. A key strategic insight is that frame engineering is becoming a performance differentiator rather than a commodity component, allowing suppliers to command premium positioning within UAV value chains.

The market continues to face pressure from carbon fiber pricing volatility and concentrated raw-material production networks. Aerospace-grade carbon fiber typically costs 3–5 times more than conventional structural materials, creating margin challenges for drone manufacturers operating in competitive commercial segments. More than 60% of global carbon fiber production capacity remains concentrated among a limited group of suppliers, increasing exposure to trade restrictions and logistics disruptions. Recent supply-chain bottlenecks have extended procurement lead times by approximately 15–20% for some specialized composite grades. Companies are responding through long-term procurement contracts, supplier diversification strategies, and localized manufacturing initiatives. A notable operational insight is that supply security increasingly influences procurement decisions as much as frame performance, particularly for large-scale drone fleet deployments.

Rapid expansion of autonomous aerial systems is creating opportunities for next-generation carbon fiber frame solutions optimized for endurance, modularity, and payload flexibility. More than 50% of enterprise drone programs are evaluating autonomous mission capabilities, while AI-enabled fleet management platforms are accelerating operational deployment. Emerging manufacturing techniques, including automated fiber placement and topology optimization, can reduce material waste by nearly 20% while improving structural efficiency. China and India are actively promoting commercial drone ecosystems through supportive policy initiatives and domestic manufacturing incentives. Companies are increasing R&D spending, pursuing composite technology partnerships, and developing modular frame architectures for specialized applications. An important strategic insight is that future value creation will increasingly originate from integrated platform design rather than standalone hardware production.

As drone deployments expand across commercial and defense sectors, manufacturers face growing challenges related to production scalability, quality assurance, and engineering standardization. Composite fabrication processes can generate performance variations of 10–15% if manufacturing precision is not tightly controlled. Workforce shortages in advanced composites engineering and automated production systems continue to affect operational efficiency across several manufacturing hubs. In addition, increasingly sophisticated autonomous drone systems require tighter integration between structural components, sensors, and onboard electronics. Companies are addressing these challenges through digital manufacturing technologies, automated inspection systems, and strategic partnerships with aerospace engineering specialists. A critical strategic insight is that long-term competitiveness will depend on the ability to scale high-quality production without compromising reliability, certification requirements, or operational consistency across expanding drone fleets.

Automated Composite Manufacturing Expansion Manufacturers are accelerating automated layup and CNC-based composite processing, reducing production cycle times by nearly 25% and lowering material waste by approximately 18%. Rising labor costs in China and growing demand for precision airframe tolerances are pushing suppliers toward robotics-assisted fabrication. Companies are scaling automated production lines and implementing digital quality-control systems, improving throughput consistency while supporting higher-volume industrial and defense drone programs.

Modular Frame Architecture Adoption Drone OEMs are increasingly deploying modular carbon fiber frame platforms that shorten configuration and maintenance time by more than 20% while reducing spare-part inventories by nearly 15%. Enterprise customers increasingly require mission-specific customization for logistics, mapping, and surveillance operations. In response, manufacturers are restructuring product portfolios around interchangeable components and expanding partnerships with payload and sensor providers to accelerate deployment flexibility and operational efficiency.

Localized Composite Supply Networks Supply-chain resilience has become a major operational priority following trade restrictions and logistics disruptions. More than 30% of leading drone manufacturers have expanded regional sourcing strategies, while localized composite procurement programs have increased by approximately 22% since 2024. Companies are diversifying supplier bases, establishing long-term material agreements, and investing in domestic composite processing capabilities to reduce lead-time volatility and improve production predictability.

Defense-Grade Lightweight Optimization Defense drone developers are increasingly adopting high-modulus carbon fiber structures that improve payload efficiency by 15% and enhance structural durability by over 20% compared with conventional composite configurations. Rising demand for longer-endurance reconnaissance platforms is driving rapid airframe redesign initiatives. A less obvious trend is the growing convergence between commercial and military frame engineering standards, prompting companies to accelerate certification programs, advanced simulation tools, and aerospace-grade manufacturing processes.

Multirotor carbon fiber drone frames remain the leading type segment, accounting for approximately 52% of total market demand due to their operational flexibility, ease of deployment, and compatibility with inspection, surveillance, and commercial mapping applications. Their modular architecture supports rapid payload integration and lower maintenance complexity, making them the preferred choice for enterprise operators. Manufacturers continue expanding lightweight frame portfolios and introducing reinforced composite structures that improve durability by nearly 20% without significantly increasing weight. Fixed-wing carbon fiber drone frames represent the fastest-growing segment as long-range operations, border surveillance, and agricultural monitoring programs expand. These platforms can deliver flight endurance improvements exceeding 40% compared with conventional multirotor systems, making them increasingly attractive for large-area coverage missions. Hybrid VTOL platforms are also gaining attention for combining vertical takeoff capability with fixed-wing efficiency, while racing and recreational frame categories maintain specialized demand among performance-focused users. Investment priorities are shifting toward advanced aerodynamics, modular frame engineering, and mission-specific platform optimization.

Industrial inspection remains the leading application segment, representing approximately 34% of total demand as utilities, oil & gas operators, telecommunications providers, and infrastructure owners increasingly deploy drones for asset monitoring. Carbon fiber frames provide superior structural rigidity and reduced weight, improving flight stability and inspection efficiency. More than 50% of large infrastructure drone fleets now utilize carbon-composite airframes to maximize operational uptime and payload performance. Manufacturers are expanding application-specific designs optimized for thermal imaging, LiDAR, and advanced sensor integration. Logistics and delivery applications are emerging as the fastest-growing segment due to increasing focus on autonomous transportation networks and last-mile delivery programs. Demand for lightweight, high-strength structures has increased by nearly 28% among commercial delivery drone projects seeking greater payload efficiency. Agriculture, aerial mapping, and defense surveillance continue generating stable demand, while emergency response applications are adopting advanced frame designs for rapid deployment requirements. Companies are responding through integrated platform development, autonomous flight optimization, and fleet-scale deployment partnerships.

Defense and government agencies constitute the dominant end-user segment, accounting for nearly 38% of market demand due to extensive deployment requirements for surveillance, reconnaissance, border security, and public-safety operations. Carbon fiber drone frames are favored because they enhance endurance, reduce structural weight, and support mission-critical payload integration. Procurement programs increasingly emphasize durable composite platforms capable of operating in challenging environments. Manufacturers are strengthening defense partnerships, expanding certification capabilities, and developing specialized military-grade airframe solutions. Commercial enterprises represent the fastest-growing end-user category as utilities, construction firms, logistics operators, and industrial asset owners scale drone deployments. Enterprise fleet utilization has increased by approximately 25% over the past two years, driven by inspection automation and digital asset management initiatives. Agricultural operators continue adopting drones for precision farming, while research institutions and service providers remain important niche buyers. Companies are targeting these segments through subscription-based support services, customized frame configurations, and ecosystem partnerships that simplify operational deployment and lifecycle management.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2026 and 2033.

North America represented approximately 28.6% of global market activity in 2025, supported by strong defense procurement programs, industrial drone deployments, and advanced composite manufacturing capabilities. The region benefits from a mature UAV ecosystem serving infrastructure inspection, energy monitoring, precision agriculture, and security operations. Growing adoption of autonomous drone fleets has increased demand for lightweight carbon fiber airframes capable of supporting extended mission durations and advanced payload systems. More than 45% of enterprise drone operators in the region now deploy drones for recurring industrial workflows. Strategic partnerships between aerospace suppliers and drone manufacturers continue strengthening domestic production capacity while improving material supply resilience.

United States Market Outlook: The United States remains the primary market driver due to its leadership in defense UAV programs, aerospace composites expertise, and commercial drone innovation. The country accounts for the majority of regional defense drone procurement activity and continues expanding industrial drone utilization across utilities, transportation, and energy sectors. More than 60% of large-scale infrastructure drone inspection programs operate within the U.S. market. Continued investment in autonomous systems, domestic manufacturing initiatives, and advanced carbon-composite technologies is reinforcing the country's position as a critical hub for next-generation drone frame development.

Europe accounted for nearly 21.4% of global demand, driven by infrastructure digitization, industrial automation initiatives, and harmonized drone operating frameworks. Carbon fiber drone frame adoption is accelerating as enterprises seek lighter, more durable UAV platforms for inspection, mapping, and environmental monitoring. The region's strong aerospace manufacturing base supports advanced composite innovation and specialized airframe development. Cross-border regulatory standardization has improved commercial deployment efficiency, while enterprise demand for automated asset monitoring continues rising. Several aerospace and drone manufacturers have expanded composite production partnerships to strengthen local supply chains and improve operational flexibility.

Germany Market Outlook: Germany leads the European market through its advanced engineering capabilities, industrial automation leadership, and strong aerospace ecosystem. Manufacturing companies, utility operators, and logistics enterprises are increasingly integrating drones into operational workflows. Industrial inspection deployments have expanded significantly across energy and transportation networks, creating sustained demand for high-performance carbon fiber airframes. Germany's emphasis on precision manufacturing and advanced materials research continues supporting innovation in lightweight drone structures, reinforcing its strategic importance within the European drone value chain.

Asia-Pacific remains the dominant regional market with approximately 41.8% share, supported by large-scale drone manufacturing, extensive composite supply chains, and expanding commercial UAV adoption. The region hosts many of the world's largest drone production hubs, creating strong demand for carbon fiber frame components across industrial, agricultural, and logistics applications. Export-oriented manufacturing operations continue strengthening regional competitiveness. More than 50% of global commercial drone assembly activity is concentrated within major Asia-Pacific manufacturing clusters. Companies are investing in automated composite production systems and expanding supplier networks to support growing domestic and international demand.

China Market Outlook: China serves as the strategic center of the global carbon fiber drone frame industry due to its integrated manufacturing ecosystem, composite materials capacity, and drone export leadership. The country accounts for a substantial share of worldwide commercial drone production and maintains extensive supplier networks spanning frame manufacturing, electronics, and propulsion systems. Government support for low-altitude economic development and industrial drone deployment continues accelerating adoption. Large-scale manufacturing efficiency and vertically integrated supply chains allow Chinese producers to maintain strong cost competitiveness while expanding advanced carbon-composite capabilities.

South America represented approximately 4.7% of global market activity, with demand primarily supported by agricultural monitoring, mining operations, and environmental surveying applications. Carbon fiber drone frames are increasingly preferred due to their durability and operational efficiency across large geographic areas. Expanding precision agriculture programs are creating demand for lightweight UAV platforms capable of supporting multispectral sensors and extended flight operations. Infrastructure limitations and uneven regulatory development continue affecting deployment speed in certain markets. Nevertheless, increasing private-sector investment and technology partnerships are strengthening regional adoption capabilities.

Brazil Market Outlook: Brazil is the leading market within South America, supported by its extensive agricultural sector and growing utilization of drone-based crop monitoring solutions. Large-scale farming operations increasingly deploy drones for field mapping, irrigation assessment, and crop-health analysis. Precision agriculture programs have expanded rapidly across major farming regions, driving demand for durable carbon fiber airframes capable of operating in demanding environments. Continued investment in agricultural technology and digital farming initiatives is positioning Brazil as the region's primary growth center for commercial drone applications.

The Middle East & Africa accounted for roughly 3.5% of global market demand, supported by expanding infrastructure monitoring programs, energy-sector applications, and government-led modernization initiatives. Carbon fiber drone frames are increasingly utilized for pipeline inspection, security operations, and large-scale construction monitoring. Investment in smart-city projects and digital infrastructure management is creating additional deployment opportunities. Several regional organizations have accelerated UAV adoption programs to improve operational efficiency and reduce inspection costs. Strategic technology partnerships are helping strengthen local drone capabilities while improving access to advanced composite platforms.

United Arab Emirates Market Outlook: The UAE stands out as the region's most strategically significant market due to its strong investment environment, advanced infrastructure projects, and proactive drone adoption policies. Government agencies and enterprise operators are increasingly utilizing drones for urban planning, infrastructure monitoring, logistics testing, and public-safety operations. Smart-city initiatives have accelerated deployment activity across multiple sectors, while regulatory support has encouraged commercial UAV innovation. The country's emphasis on technology-driven modernization continues creating favorable conditions for advanced carbon fiber drone frame adoption and ecosystem expansion.

The Carbon Fiber Drone Frame Market is characterized by competition between integrated drone manufacturers such as DJI and iFlight, specialized frame developers including Holybro and Tarot-RC, and emerging defense-focused UAV producers such as PDW and Raphe mPhibr. The top five participants collectively account for approximately 42% of market activity, creating a moderately concentrated competitive structure. Global leaders compete on advanced composite engineering, supply-chain control, and platform integration, while regional players focus on cost efficiency and application-specific customization. Technology performance remains the primary differentiator. Lightweight carbon fiber architectures improve payload efficiency by 15–20%, while automated composite manufacturing can reduce material waste by nearly 18%. Companies are increasingly pursuing vertical integration, supplier partnerships, and localized production strategies to secure carbon fiber availability and shorten lead times by more than 20%. The competitive shift is moving from price-based competition toward manufacturing resilience, advanced design capabilities, and defense-grade certification readiness. Supply-chain access remains a significant entry barrier. Success increasingly depends on combining composite innovation, scalable manufacturing, and mission-specific platform performance.

Holybro

iFlight Innovation Technology

Tarot-RC

T-Motor

SpeedyBee

GEPRC

Flywoo

Foxeer

Axis Flying

Performance Drone Works (PDW)

Raphe mPhibr

SkyFall

Autel Robotics

The current technology landscape is centered on high-modulus carbon fiber composites, CNC-machined structural components, and lightweight modular frame architectures. Advanced carbon-composite frames improve strength-to-weight performance by more than 20% compared with conventional aluminum structures while reducing overall airframe weight by nearly 30%. More than 55% of newly developed industrial UAV platforms now incorporate carbon-composite structural designs to extend endurance and increase payload flexibility. Companies deploying these technologies achieve measurable gains in mission duration, inspection coverage, and operational efficiency.

Emerging technologies include automated fiber placement, AI-assisted structural optimization, and digital-twin-based frame engineering. Compared with traditional manual composite fabrication, automated manufacturing can reduce material waste by approximately 18% while improving dimensional consistency by over 15%. Advanced simulation environments allow manufacturers to test hundreds of frame configurations virtually before production. Large drone OEMs and defense contractors benefit most from these capabilities because they accelerate product development cycles and improve certification readiness.

Disruptive innovation between 2026 and 2028 will increasingly focus on lattice-structured composites, additive composite manufacturing, and integrated smart airframes. Recent lightweight composite designs have demonstrated up to 10% lower structural weight than comparable commercial frames while maintaining durability. Companies that invest early in automated composites, digital engineering, and next-generation structural materials will gain stronger competitive advantages through lower production costs, higher performance, and faster deployment readiness.

January 2025 – DJI launched the Matrice 4 Series enterprise drone platform featuring AI-enabled aerial intelligence and enhanced sensing capabilities. The platform integrates advanced lightweight structural engineering to improve operational reliability and enterprise deployment efficiency. Business impact: strengthens DJI’s position in industrial UAV applications. Source: www.dji.com

June 2025 – Raphe mPhibr secured USD 100 million in funding to expand aircraft design and manufacturing operations in India. The financing increased total capital raised to USD 145 million, supporting advanced aerospace production and composite manufacturing capabilities. Business impact: accelerates domestic UAV ecosystem development.

August 2025 – Performance Drone Works (PDW) opened its 90,000-square-foot Drone Factory 01 facility in Alabama to expand tactical drone manufacturing capacity. The facility centralizes design, production, testing, and delivery operations. Business impact: significantly strengthens U.S.-based drone production scalability.

October 2025 – Kineco Exel Composites India achieved full-scale production at its Banda manufacturing plant, supplying carbon fiber structural components through dedicated production lines. The facility completed commissioning and entered volume-delivery operations. Business impact: strengthens carbon-fiber component availability across aerospace and advanced manufacturing supply chains.

The report provides comprehensive coverage of the Carbon Fiber Drone Frame Market across major frame types, applications, end-user categories, and geographic regions. The analysis evaluates multirotor, fixed-wing, hybrid VTOL, and specialized frame platforms while assessing deployment patterns across industrial inspection, agriculture, logistics, mapping, surveillance, and defense operations. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting manufacturing concentration, adoption trends, and operational deployment dynamics. More than 55% of enterprise drone programs now prioritize lightweight composite structures, making material innovation a critical area of analysis.

The study further examines advanced composite manufacturing technologies, automated production systems, AI-enabled design optimization, and evolving supply-chain strategies. Competitive benchmarking includes leading drone manufacturers, frame specialists, and emerging defense-focused developers. Strategic insights support investment planning, product expansion, partnership development, supply-chain positioning, and technology prioritization. The report also evaluates emerging opportunities in autonomous drone ecosystems, localized manufacturing initiatives, and next-generation composite architectures expected to influence market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 385.0 Million |

| Market Revenue (2033) | USD 1,121.6 Million |

| CAGR (2026–2033) | 14.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DJI; Holybro; iFlight Innovation Technology; Tarot-RC; T-Motor; SpeedyBee; GEPRC; Flywoo; Foxeer; Axis Flying; Performance Drone Works (PDW); Raphe mPhibr; SkyFall; Autel Robotics |

| Customization & Pricing | Available on Request (10% Customization Free) |