Reports

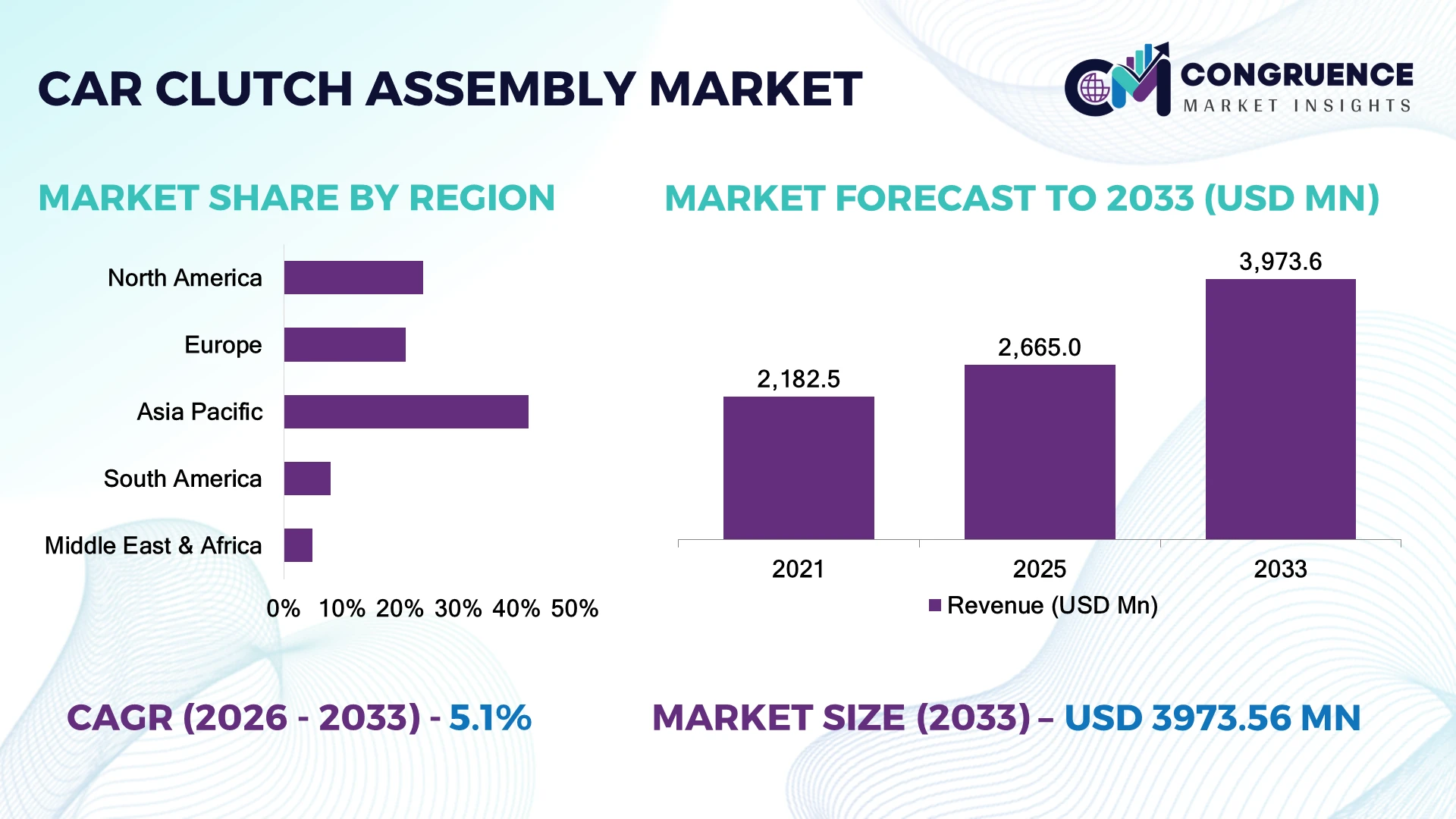

The Global Car Clutch Assembly Market was valued at USD 2,665.0 Million in 2025 and is anticipated to reach a value of USD 3,973.6 Million by 2033 expanding at a CAGR of 5.12% between 2026 and 2033. Growth is driven by rising adoption of automated manual transmissions, lightweight clutch components, and advanced friction materials improving vehicle efficiency and durability.

China dominates the market with nearly 32% share, supported by its automotive manufacturing base, over 30 million annual vehicle production capacity, and strong investments in electric and hybrid drivetrain technologies. Germany follows with advanced transmission engineering and automation expertise, where more than 40% of new passenger vehicles use advanced transmission systems. The U.S. continues expanding through aftermarket demand and vehicle modernization programs.

Strategic focus on localized production, material innovation, and efficient drivetrain solutions will define competitive advantage.

Market Size & Growth: USD 2.66 Billion in 2025 to USD 3.97 Billion by 2033 at 5.12% CAGR, driven by advanced transmission adoption and lightweight component development.

Top Growth Drivers: Automated transmission adoption (35%), lightweight materials usage (28%), and aftermarket replacement demand (22%) are key growth factors.

Short-Term Forecast: By 2028, advanced clutch systems reduce maintenance costs by 15% and improve transmission efficiency by 12%.

Emerging Technologies: AI-based manufacturing, automated inspection systems, and advanced composite friction materials are reshaping production.

Regional Leaders: Asia Pacific reaches USD 2.1 Billion by 2033 through automotive expansion; Europe reaches USD 1.0 Billion through premium vehicle innovation; North America reaches USD 0.8 Billion through aftermarket growth.

Consumer/End-User Trends: Over 45% of vehicle buyers prioritize smoother transmission performance and fuel efficiency features.

Pilot/Case Example: In 2024, automated production lines improved clutch assembly quality consistency by 18% through robotics and digital monitoring.

Competitive Landscape: Leading manufacturers hold around 40% combined market influence, including ZF, Schaeffler, BorgWarner, Valeo, and Eaton.

Regulatory & ESG Impact: Stricter emission standards push manufacturers toward components improving fuel efficiency by nearly 10%.

Investment & Funding: More than USD 500 Million invested in automotive component modernization, focusing on automation and regional supply-chain expansion.

Innovation & Future Outlook: Next-generation clutch systems emphasize smart sensors, hybrid compatibility, and digitally optimized manufacturing strategies.

The car clutch assembly market is evolving beyond traditional mechanical systems, with demand concentrated around passenger vehicles, commercial mobility, and hybrid powertrain applications. Manufacturers are introducing improved friction materials, electronically controlled clutch modules, and compact designs, with nearly 30% of new transmission developments integrating advanced control features. Supply-chain diversification across Asia and Europe is also influencing sourcing strategies as automotive companies strengthen regional production networks. These shifts are creating new opportunities for suppliers focused on precision engineering and sustainable manufacturing.

The car clutch assembly market is becoming strategically important as automotive manufacturers balance performance, efficiency, and changing drivetrain requirements. Rising automation in vehicle production, stricter emission regulations, and the transition toward hybrid mobility are reshaping component development strategies. Supply-chain restructuring after global disruptions has encouraged manufacturers to establish regional sourcing networks and strengthen local manufacturing capabilities.

Advanced clutch assemblies using improved friction materials and electronic controls provide measurable advantages over traditional systems, including up to 15% better durability and improved shift responsiveness compared with conventional mechanical designs. Europe leads in premium vehicle technology integration, while Asia Pacific maintains larger production scale due to high vehicle manufacturing volumes and expanding supplier ecosystems.

Over the next 2–3 years, manufacturers are increasing investments in smart production facilities, robotics, and digital quality monitoring to improve operational efficiency. Companies are forming partnerships with automotive OEMs to develop hybrid-compatible clutch solutions and optimize production capacity. Strategic positioning will depend on engineering innovation, supply-chain resilience, and the ability to deliver efficient drivetrain technologies for evolving mobility platforms.

Rising adoption of automated manual transmissions and hybrid-compatible clutch systems is accelerating demand for advanced car clutch assemblies. More than 35% of new passenger vehicles globally are incorporating automated transmission technologies, while lightweight material integration improves component efficiency by nearly 15%. China’s automotive manufacturing ecosystem is expanding investments in precision clutch production to support higher vehicle output and export demand. Companies are responding through robotics-enabled manufacturing, strategic OEM partnerships, and development of high-performance friction materials. The shift toward electronically controlled clutch modules is creating a competitive advantage for suppliers focused on durability, reduced weight, and improved drivetrain performance.

Volatility in steel, aluminum, and friction material prices remains a key limitation for clutch assembly manufacturers, with raw material fluctuations impacting component production costs by approximately 10–15%. Dependence on specialized suppliers for friction compounds and precision parts creates supply-chain vulnerabilities, particularly in manufacturing hubs across China and Europe. Increasing compliance requirements for automotive materials also add operational complexity and testing expenses. Companies are reducing exposure through supplier diversification, localized sourcing strategies, and long-term procurement agreements. The ability to stabilize input costs while maintaining quality standards is becoming a critical factor for protecting margins and ensuring consistent production capacity.

Development of smart clutch assemblies with sensors, electronic controls, and predictive maintenance capabilities is creating new opportunities across hybrid and advanced vehicle platforms. Intelligent clutch technologies can improve operational efficiency by nearly 12% while reducing maintenance requirements through real-time monitoring. Germany and Japan are advancing research partnerships focused on compact drivetrain solutions for next-generation mobility applications. Manufacturers are increasing R&D investments in sensor-based systems, automated production lines, and hybrid vehicle integration. A major untapped opportunity lies in aftermarket modernization, where digital diagnostics and modular clutch designs can improve replacement efficiency and extend vehicle lifecycle value.

Increasing drivetrain diversity creates engineering challenges as manufacturers adapt clutch assemblies for conventional, hybrid, and automated transmission architectures. Nearly 30% of new vehicle development programs now require customized transmission solutions, increasing testing requirements and production complexity. Limited availability of skilled automotive engineers and advanced manufacturing specialists affects scalability in countries expanding vehicle component production. Companies must address compatibility issues through digital simulation, advanced testing facilities, and cross-industry partnerships. Long-term competitiveness depends on achieving standardized yet flexible clutch designs that support multiple vehicle platforms while maintaining reliability, cost efficiency, and regulatory compliance.

Automation In Manufacturing: Car clutch assembly producers are increasing robotic machining, automated inspection, and digital quality control adoption, with automation improving production consistency by around 20% and reducing manual defects by nearly 15%. Automotive suppliers in China and Germany are expanding smart factories as labor availability pressures increase. Companies are restructuring workflows through AI-based monitoring and connected manufacturing systems to improve throughput, reduce downtime, and strengthen supply-chain reliability.

Lightweight Material Integration: Manufacturers are shifting toward aluminum alloys, advanced composites, and improved friction materials, reducing component weight by approximately 10–18% while supporting vehicle efficiency targets. Regulatory pressure on fuel consumption and emissions in markets such as the European Union is accelerating material innovation. Companies are partnering with material specialists and investing in engineering upgrades to deliver durable clutch assemblies with improved thermal performance.

Hybrid Vehicle Compatibility: The transition toward hybrid mobility is increasing demand for electronically controlled clutch systems, with nearly 30% of new transmission development programs requiring specialized integration capabilities. Automakers in Japan and South Korea are prioritizing compact clutch modules for hybrid platforms. Suppliers are expanding product portfolios through OEM collaborations, software integration, and advanced testing facilities to support evolving drivetrain architectures.

Supply Chain Localization Shift: Automotive component suppliers are diversifying production networks, with localized sourcing initiatives reducing dependency risks by approximately 15% in critical component procurement strategies. Recent global supply disruptions have encouraged manufacturers in India and Mexico to develop regional production hubs. Companies are increasing partnerships with local suppliers, strengthening inventory planning, and adopting digital procurement systems to improve operational resilience.

Manual clutch assemblies remain the leading type segment, accounting for approximately 55% of the global car clutch assembly market due to their cost efficiency, mechanical simplicity, and strong penetration in economy passenger vehicles and commercial fleets. Their lower maintenance requirements and compatibility with existing transmission platforms continue supporting adoption in countries such as India, China, and Brazil. Automated clutch systems represent the fastest-growing segment, expanding as vehicle manufacturers increase investments in automated manual transmissions and hybrid-compatible drivetrains. Automated systems are gaining adoption with nearly 20% faster integration across new vehicle platforms compared with traditional systems. Hydraulic and dual-clutch technologies continue gaining strategic importance, particularly in premium vehicles where smoother shifting and higher performance are priorities. Companies are increasing investments in electronically controlled clutch modules, advanced friction materials, and compact designs to address changing vehicle architectures. The market shift indicates a gradual transition from conventional mechanical systems toward intelligent clutch solutions, creating new opportunities for suppliers focused on automation and drivetrain innovation.

Passenger vehicles represent the dominant application segment, contributing nearly 70% of global car clutch assembly demand due to high vehicle production volumes and continuous replacement requirements. Rising ownership of personal vehicles, urban mobility expansion, and increasing demand for smoother transmission performance are strengthening adoption. Commercial vehicles account for a significant secondary segment, supported by fleet operators requiring durable clutch assemblies with longer service intervals. Hybrid and performance vehicle applications are emerging as the fastest-growing areas, with adoption increasing as automakers introduce more electrified drivetrain options. Passenger vehicle manufacturers are focusing on lightweight clutch designs and improved thermal resistance, while commercial vehicle suppliers are prioritizing durability and load-handling capabilities. Approximately 35% of new vehicle development programs now require enhanced transmission integration, encouraging companies to expand engineering partnerships and develop application-specific solutions. The evolving application landscape is pushing manufacturers toward modular clutch systems that support multiple vehicle categories and reduce production complexity.

Automotive OEMs represent the largest end-user segment, accounting for approximately 65% of clutch assembly demand due to direct integration into new vehicle production lines. Major vehicle manufacturers rely on advanced clutch suppliers for customized solutions, quality consistency, and compatibility with evolving transmission systems. Aftermarket service providers represent another important segment, supported by vehicle aging patterns and replacement demand, particularly in countries with large existing vehicle populations. Hybrid vehicle producers and specialized drivetrain manufacturers are emerging as the fastest-growing end-user group as electrification strategies create demand for advanced clutch technologies. Nearly 25% of automotive suppliers are increasing investment in hybrid transmission components and smart clutch solutions to support future vehicle platforms. Companies are strengthening OEM partnerships, expanding regional manufacturing capabilities, and developing customized product portfolios to address diverse customer requirements. Competitive positioning increasingly depends on supplier flexibility, engineering support, and the ability to deliver scalable solutions across different vehicle architectures.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

North America holds approximately 24% of the global car clutch assembly market, supported by strong automotive production networks, established aftermarket channels, and rising adoption of advanced transmission systems. The United States remains the primary contributor due to its large vehicle fleet and demand for replacement components. Automotive manufacturers are increasing investments in automated manufacturing facilities, with robotics adoption improving production efficiency by nearly 18%. Growth is concentrated around passenger vehicles, performance vehicles, and commercial fleets requiring durable drivetrain components. Supply-chain restructuring is encouraging localized sourcing strategies across the U.S. and Mexico, enabling manufacturers to reduce dependency on overseas suppliers and improve delivery reliability.

United States Market Outlook: The United States maintains a strategic position through its advanced automotive engineering ecosystem and extensive aftermarket network. Over 280 million registered vehicles support continuous replacement demand, while manufacturers are expanding domestic component production capabilities. Investments in automation, precision machining, and hybrid vehicle technologies are strengthening the country’s role in advanced clutch assembly development.

Europe contributes nearly 21% of the global car clutch assembly market, driven by premium vehicle manufacturing, strict emission standards, and advanced drivetrain engineering. Germany, France, and Italy remain major production centers with strong automotive supplier ecosystems. The shift toward hybrid vehicles and automated transmission systems is accelerating demand for electronically controlled clutch modules, with more than 30% of new European vehicle platforms integrating advanced transmission technologies. Regulatory pressure under European emission frameworks is pushing suppliers toward lightweight materials and efficient designs. Companies are expanding partnerships with automotive OEMs and investing in digital manufacturing systems to improve production flexibility and sustainability performance.

Germany Market Outlook: Germany leads Europe’s clutch assembly industry through its automotive manufacturing strength, engineering expertise, and high-performance vehicle production base. The country accounts for a significant share of European vehicle manufacturing and hosts extensive supplier networks focused on precision components. Over 40% of premium vehicle production incorporates advanced transmission technologies, supporting continued innovation in clutch systems.

Asia-Pacific dominates the global car clutch assembly market with approximately 42% share, supported by large-scale vehicle production, expanding supplier networks, and strong manufacturing capabilities. China, India, Japan, and South Korea represent major contributors, with China producing more than 30 million vehicles annually and maintaining a large automotive component ecosystem. Rising vehicle ownership, cost-efficient manufacturing, and increasing automation adoption are strengthening regional competitiveness. Companies are expanding production facilities, forming OEM partnerships, and investing in smart factories to improve output quality. The region’s supply-chain advantage enables faster component development and supports growing demand for both conventional and advanced clutch technologies.

China Market Outlook: China remains the largest automotive manufacturing hub globally, supported by extensive component production capacity and advanced industrial infrastructure. The country’s automotive ecosystem includes thousands of suppliers specializing in transmission components, enabling efficient scaling. Government-backed manufacturing modernization programs are accelerating automation adoption, with smart production systems improving operational efficiency across automotive component facilities.

South America represents nearly 8% of the global car clutch assembly market, supported by a large installed vehicle base and increasing demand for replacement components. Brazil and Argentina remain key automotive manufacturing centers, with Brazil contributing the majority of regional vehicle production. The aftermarket segment plays a significant role as aging vehicle fleets require frequent maintenance and component replacement. Companies are strengthening distribution networks and developing cost-effective clutch solutions to address price-sensitive markets. However, currency fluctuations and import dependency continue influencing procurement strategies. Manufacturers are responding through localized partnerships and regional inventory expansion to improve supply reliability.

Brazil Market Outlook: Brazil is the leading automotive market in South America, supported by domestic vehicle production and a mature component supplier network. The country produces more than 2 million vehicles annually, creating consistent demand for clutch assemblies across passenger and commercial segments. Local manufacturing partnerships are helping companies reduce import dependence and improve market responsiveness.

Middle East & Africa accounts for approximately 5% of the global car clutch assembly market, with growth supported by vehicle fleet expansion, infrastructure modernization, and increasing automotive service demand. Countries such as Saudi Arabia, the UAE, and South Africa are strengthening automotive ecosystems through industrial development initiatives and logistics investments. Rising demand for commercial vehicles and replacement components is encouraging suppliers to expand regional distribution networks. Automotive service centers are adopting improved diagnostic technologies, with digital maintenance solutions increasing operational efficiency by nearly 15%. Companies are focusing on partnerships, localized warehousing, and supply-chain improvements to address geographic challenges.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic automotive market due to industrial diversification programs and increasing mobility investments. The country’s vehicle market exceeds 10 million registered vehicles, supporting aftermarket demand for drivetrain components. Investments in manufacturing infrastructure and automotive supply-chain development are creating new opportunities for clutch assembly suppliers.

The car clutch assembly market features competition between global Tier-1 suppliers such as Schaeffler, ZF, BorgWarner, Valeo, and Aisin against regional manufacturers competing through cost efficiency and localized production. The top five players collectively account for approximately 45% of market influence, driven by OEM relationships and advanced drivetrain expertise. Competition is based on product technology, customization capability, supply-chain reliability, and manufacturing scale, with automated clutch solutions gaining nearly 25% higher adoption in advanced vehicle platforms. Companies are expanding through OEM partnerships, regional plants, and investments in smart manufacturing. The competitive landscape is shifting toward hybrid-compatible clutch modules, digital production, and integrated drivetrain solutions. High tooling costs, engineering expertise requirements, and strict automotive qualification processes create significant entry barriers. Winning players will combine technology leadership, localized supply networks, and flexible product development capabilities.

ZF Group

BorgWarner

Valeo

Aisin Corporation

Eaton

EXEDY Corporation

F.C.C. Co., Ltd.

Ningbo Tuopu Group

Hitachi Astemo

Yazaki Corporation

Schaeffler India

Advanced clutch technologies are shifting from conventional mechanical assemblies toward electronically controlled and hybrid-compatible systems. Automated clutch modules are gaining adoption across passenger vehicles, improving shift response by nearly 15% compared with traditional systems. Companies are integrating sensors, electronic actuators, and predictive monitoring to improve reliability and reduce maintenance requirements by around 10–12%.

Lightweight materials and advanced friction compounds are becoming critical technologies, replacing conventional materials with improved thermal-resistant solutions. New-generation clutch components reduce weight by approximately 10% while maintaining durability under higher operating loads. Suppliers benefiting most are those combining material science with automated manufacturing capabilities, particularly for hybrid and performance vehicle applications.

Between 2026 and 2028, digital manufacturing, AI-based quality inspection, and smart drivetrain integration will shape competitive positioning. Compared with older manual inspection processes, automated quality systems improve defect detection efficiency by nearly 20%. Companies investing in connected factories, software-enabled diagnostics, and flexible production platforms will gain advantages through faster customization, improved consistency, and stronger OEM partnerships.

May 2025 – BorgWarner secured two dual-clutch transmission programs in China, including a seven-year extension with a German OEM and a new clutch module supply agreement. The programs support SUV and sedan platforms, with production from BorgWarner facilities in China and improved efficiency through reduced friction losses. Source: www.borgwarner.com

June 2025 – Schaeffler launched the LuK RepSet 2CT DMF repair solution for double-clutch vehicles, combining clutch and dual-mass flywheel components into one service package. The innovation improves workshop efficiency by simplifying replacement processes and strengthening aftermarket service capabilities. Source: www.schaeffler.de

October 2025 – ZF Group expanded its India clutch business through a new heavy-duty clutch system supply agreement with a leading commercial vehicle manufacturer. The 430 mm clutch system will be produced at ZF’s Chakan facility, with production planned for mid-2026 and durability improvements of up to 20%. Source: www.press.zf.com

June 2025 – ZF Group advanced hybrid drivetrain technology through development of its 8HP evo hybrid transmission concept, focusing on improved efficiency and flexible electrified mobility applications. The technology supports lower emissions and strengthens ZF’s position in next-generation transmission systems.

The Car Clutch Assembly Market Report provides comprehensive coverage across product types, applications, end-users, regional markets, competitive positioning, and technology developments. The analysis evaluates manual, automated, hydraulic, and advanced clutch systems while examining applications across passenger vehicles, commercial vehicles, and emerging hybrid mobility platforms. It includes assessment of manufacturers, suppliers, aftermarket participants, and evolving drivetrain ecosystems.

The report analyzes major markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing hubs, adoption patterns, supply-chain strategies, and innovation trends. With more than 10 key industry participants evaluated, the study supports investment planning, expansion decisions, partnership strategies, and competitive positioning through insights into automation, lightweight materials, smart clutch technologies, and future mobility requirements from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,665.0 Million |

| Market Revenue (2033) | USD 3,973.6 Million |

| CAGR (2026–2033) | 5.12% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | ZF Group; BorgWarner; Valeo; Aisin Corporation; Eaton; EXEDY Corporation; F.C.C. Co., Ltd.; Ningbo Tuopu Group; Hitachi Astemo; Yazaki Corporation; Schaeffler India |

| Customization & Pricing | Available on Request (10% Customization Free) |