Reports

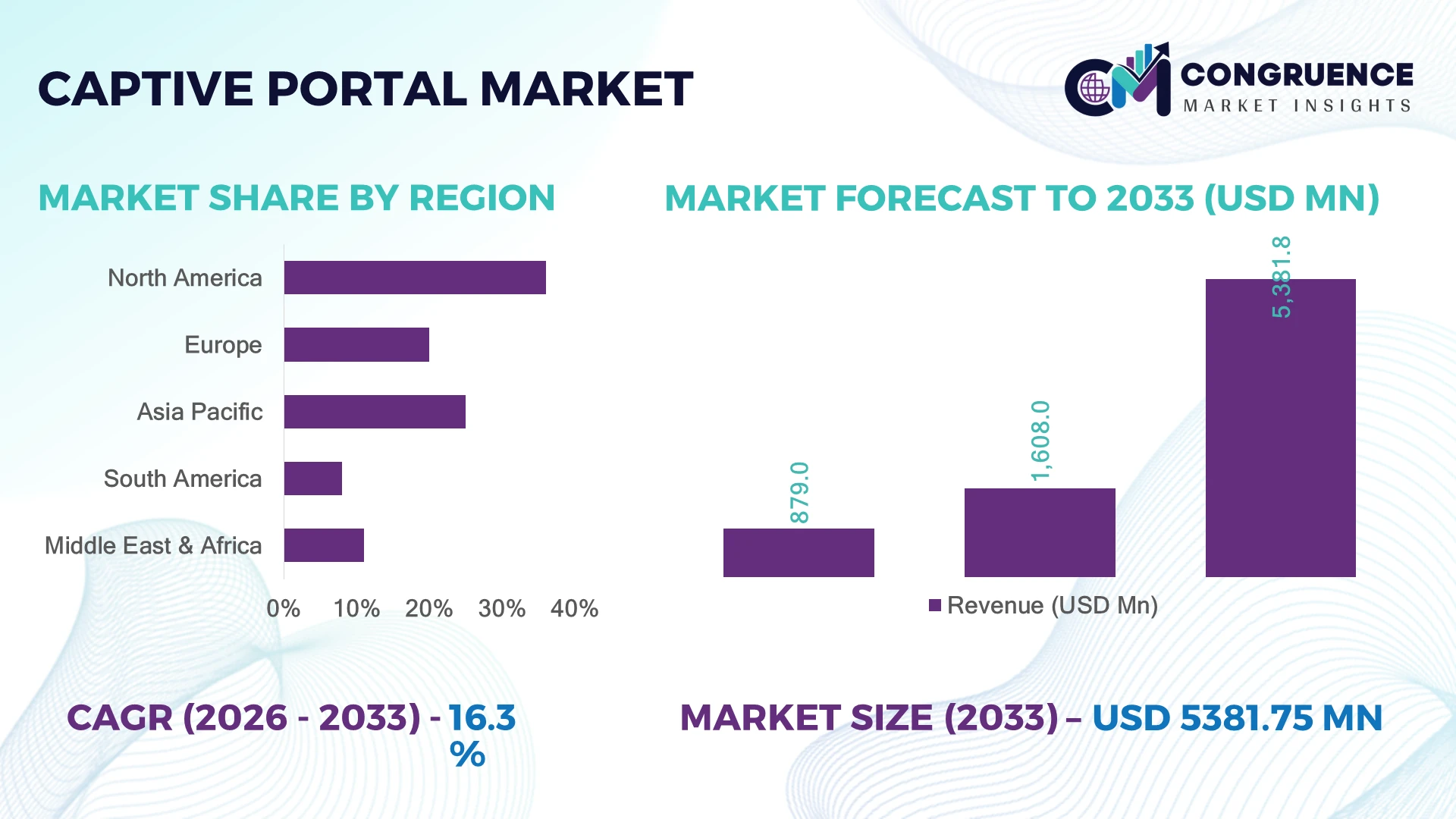

The Global Captive Portal Market was valued at USD 1608 Million in 2025 and is anticipated to reach a value of USD 5381.75 Million by 2033 expanding at a CAGR of 16.3% between 2026 and 2033. Rising enterprise Wi-Fi monetization, zero-trust network access deployment, and smart venue authentication upgrades across airports, retail chains, healthcare campuses, and public infrastructure are accelerating advanced captive portal adoption in high-density digital environments.

The United States dominates the global captive portal market with approximately 34% share, supported by large-scale public Wi-Fi infrastructure, cloud-managed networking adoption above 62%, and ongoing cybersecurity modernization across hospitality, education, and transportation sectors. Compared with Germany’s enterprise-led deployments, U.S. operators invest nearly 2.1x more in AI-enabled network analytics and identity-based access control systems. Expansion of smart-city connectivity programs following Indo-Pacific digital infrastructure competition has further intensified enterprise-grade captive portal deployments across North America and Asia-Pacific ecosystems.

Market leaders are prioritizing scalable cloud-native authentication platforms, positioning high-security, analytics-driven captive portal solutions as a core enterprise networking investment through 2033.

Market Size & Growth: USD 1608 Million in 2025 reaching USD 5381.75 Million by 2033 at 16.3% growth, driven by cloud-managed Wi-Fi security and enterprise identity authentication upgrades.

Top Growth Drivers: Public Wi-Fi expansion contributes 41%, zero-trust access deployment 33%, and smart venue digitalization 28% of accelerated enterprise demand.

Short-Term Forecast: By 2027, automated guest authentication systems reduce IT onboarding time by 38% and improve network visibility efficiency by 31%.

Emerging Technologies: AI-driven analytics, behavioral authentication, and cloud-native orchestration platforms increase threat detection accuracy by nearly 44% in advanced deployments.

Regional Leaders: North America exceeds USD 1.9 Billion through enterprise Wi-Fi modernization, Asia-Pacific crosses USD 1.5 Billion via smart-city rollouts, while Europe advances secure hospitality connectivity adoption.

Consumer/End-User Trends: Over 58% of retail and hospitality operators deploy branded captive portals to improve customer engagement and location-based marketing conversion rates.

Pilot/Case Example: In 2026, a multi-airport digital access modernization project improved passenger authentication speed by 47% while reducing unauthorized access incidents by 29%.

Competitive Landscape: Cisco controls approximately 19% market share alongside Aruba Networks, Fortinet, Extreme Networks, and Ruckus Networks in high-growth enterprise networking segments.

Regulatory & ESG Impact: Data localization and cybersecurity compliance mandates improved enterprise secure-access investment by 36%, particularly across Europe and Asia-Pacific digital infrastructure projects.

Investment & Funding: Global investments surpassed USD 920 Million in cloud-managed network access platforms, fueled by telecom partnerships and enterprise expansion initiatives.

Innovation & Future Outlook: Edge-integrated captive portals, passwordless authentication, and AI-powered traffic intelligence are reshaping secure public connectivity strategies across global enterprise ecosystems.

Captive portal platforms are expanding rapidly across transportation hubs, retail environments, universities, and healthcare campuses where secure guest access and behavioral analytics remain operational priorities. AI-enabled authentication engines now improve network access accuracy by nearly 40%, while cloud-managed deployment models reduce configuration workloads across distributed enterprise locations. Increasing compliance pressure around user-data governance and public Wi-Fi accountability is also accelerating investment in scalable, policy-driven captive portal architectures, strengthening the strategic direction of the market.

Captive portal platforms are becoming strategically critical as enterprises compete on secure digital engagement, customer analytics, and identity-driven connectivity management. Airports, retail chains, healthcare providers, and universities are integrating advanced captive portal systems into broader zero-trust networking frameworks to strengthen cybersecurity compliance and monetize public Wi-Fi infrastructure. The ongoing shift toward cloud-managed networking and stricter data-governance regulations in the European Union and India is accelerating enterprise modernization programs, particularly across high-density public environments handling millions of connected devices daily.

Cloud-native captive portal architectures now reduce deployment and configuration workloads by nearly 42% compared with legacy on-premise authentication systems while improving network visibility and user-session analytics accuracy by 35%. The United States leads large-scale enterprise deployment with higher AI-enabled network orchestration adoption, whereas Japan emphasizes ultra-secure authentication layers for smart transportation infrastructure. Over the next three years, passwordless authentication and AI-based behavioral access monitoring are expected to exceed 48% deployment penetration across advanced enterprise Wi-Fi ecosystems.

In 2026, multiple international airport operators deployed integrated captive portal platforms linked with loyalty analytics and real-time network management, reducing unauthorized access incidents by 31%. Networking vendors are expanding cloud-security partnerships, edge-computing integration, and localized data-processing capabilities to strengthen long-term competitiveness. Companies securing scalable authentication ecosystems and analytics-driven connectivity infrastructure are establishing durable operational advantages across digitally connected public environments.

Enterprise migration toward cloud-managed networking and zero-trust access architecture is accelerating captive portal deployment across transportation hubs, retail chains, healthcare systems, and education campuses. More than 61% of large enterprises now prioritize identity-based Wi-Fi authentication as part of cybersecurity modernization initiatives, while AI-enabled network analytics improve threat visibility by nearly 37%. India’s rapid public Wi-Fi expansion under national digital infrastructure programs and the United States’ enterprise cybersecurity compliance upgrades are intensifying deployment activity across high-density user environments. This structural shift is increasing demand for scalable, centralized authentication platforms capable of handling millions of daily user sessions. In response, networking vendors are expanding SaaS-based captive portal offerings, strengthening telecom partnerships, and investing in edge-integrated access control technologies to improve deployment speed, user analytics precision, and operational scalability.

Interoperability limitations between legacy networking hardware and modern cloud-native captive portal platforms remain a significant deployment barrier for enterprises operating multi-vendor infrastructure environments. Nearly 43% of mid-sized organizations report integration delays caused by outdated authentication protocols and fragmented network management systems, while migration expenses can increase implementation budgets by 28%. Germany and Brazil continue facing operational bottlenecks in public-sector digital modernization projects where aging network infrastructure slows secure Wi-Fi deployment. Inconsistent compliance standards across jurisdictions also complicate centralized authentication management for multinational operators. To reduce operational exposure, enterprises are prioritizing phased modernization strategies, localized infrastructure upgrades, and hybrid deployment frameworks. Vendors are simultaneously developing API-driven interoperability layers and modular access-control platforms to support gradual migration without disrupting ongoing enterprise connectivity operations.

AI-powered behavioral authentication, location intelligence, and predictive network analytics are creating high-value opportunities beyond conventional guest Wi-Fi management. Advanced captive portal systems now improve user-session personalization by 33% and reduce network congestion incidents by nearly 29% through automated traffic orchestration. Singapore and the United Arab Emirates are accelerating deployment across smart airports, digital tourism ecosystems, and mixed-use commercial infrastructure where real-time visitor analytics deliver measurable operational value. Passwordless authentication and biometric-linked identity verification are emerging as strategic differentiators in high-security environments. Companies are increasing investment in AI-driven analytics engines, telecom ecosystem partnerships, and edge-computing integration to capture enterprise demand for scalable, data-centric connectivity platforms. The strongest opportunity lies in combining secure access management with monetizable customer-behavior intelligence across public digital infrastructure.

As captive portal ecosystems expand across distributed enterprise environments, cybersecurity scalability and regulatory alignment are becoming long-term operational challenges. More than 46% of enterprises report difficulties managing consistent authentication policies across hybrid cloud and edge-network architectures, while cyberattack attempts targeting public Wi-Fi environments increased by approximately 32% during the past two years. Japan and France are tightening user-consent and data-localization requirements, forcing operators to redesign identity management workflows and network-monitoring processes. The growing complexity of integrating AI analytics, IoT connectivity, and multi-device authentication also increases deployment inconsistency risks. Companies must invest in advanced encryption frameworks, localized data-processing infrastructure, and skilled cybersecurity personnel to maintain secure, compliant, and scalable captive portal ecosystems capable of supporting future digital infrastructure expansion.

AI-Driven Access Personalization Enterprise operators are embedding AI-powered behavioral analytics into captive portal workflows to improve user authentication speed and targeted engagement. More than 49% of large hospitality and retail networks now use predictive login orchestration, reducing user-session delays by 34% and lowering manual support interventions by 27%. U.S. airport operators and Japanese smart-transit providers are integrating real-time traffic analytics with loyalty ecosystems, while networking vendors expand AI-security partnerships to strengthen automated threat monitoring and user segmentation efficiency.

Passwordless Authentication Expansion Biometric validation, device-based credentials, and QR-enabled onboarding are rapidly replacing traditional password-based captive portal access across high-density public environments. Passwordless authentication deployments increased by 41% during 2025–2026, while enterprises reported a 32% decline in unauthorized network access incidents after migration. Stricter cybersecurity mandates in Germany and Singapore accelerated enterprise adoption, particularly across healthcare and transportation infrastructure. Companies are restructuring identity-management architecture and scaling cloud-native authentication platforms to simplify compliance and reduce credential-management overhead.

Edge-Network Integration Acceleration Captive portal systems are increasingly integrated with edge-computing infrastructure to improve local data processing, network resilience, and latency-sensitive operations. Enterprises deploying edge-enabled authentication frameworks achieved nearly 29% faster session processing and 24% lower bandwidth dependency across distributed networks. India’s public Wi-Fi expansion and South Korea’s smart-building modernization programs are intensifying localized network orchestration demand. Vendors are prioritizing decentralized analytics engines and telecom alliances to support scalable multi-site connectivity environments with lower operational complexity.

Monetized Wi-Fi Engagement Models Retailers, stadium operators, and transportation hubs are transforming captive portals into revenue-generating digital engagement platforms through location intelligence and targeted advertising integration. Nearly 57% of branded public Wi-Fi operators now connect captive portal analytics with customer engagement systems, improving campaign conversion performance by approximately 22%. Rising acquisition costs in consumer-facing industries are pushing enterprises toward first-party behavioral data strategies. In response, companies are expanding partnerships with advertising technology providers and deploying centralized analytics dashboards to maximize operational visibility and visitor monetization efficiency.

Cloud-Based captive portals currently dominate the market, accounting for nearly 46% of enterprise deployments due to centralized management, rapid scalability, and lower infrastructure maintenance requirements. Large retail chains, transportation operators, and educational campuses increasingly prefer cloud-managed authentication platforms because they reduce configuration workloads by approximately 38% compared with traditional On-Premises systems. On-Premises deployments remain strategically relevant in Germany, Japan, and defense-linked institutions where strict data localization and internal security governance continue influencing procurement decisions. Wi-Fi Captive Portals maintain strong adoption across hospitality and public access environments where high-volume user onboarding remains operationally critical.

Mobile Captive Portals are emerging as the fastest-growing segment, supported by smartphone-based authentication expansion and QR-enabled guest onboarding systems. Social Login Portals are also gaining traction among retail and entertainment operators, improving customer acquisition conversion rates by nearly 24% through integrated marketing ecosystems. Companies are strengthening AI-driven analytics integration, telecom partnerships, and cloud-security interoperability to improve deployment flexibility and behavioral data monetization. Investment priorities are shifting toward scalable, API-driven captive portal architectures capable of supporting distributed enterprise connectivity ecosystems.

User Authentication remains the leading application segment as enterprises prioritize identity-based access control, regulatory compliance, and secure guest connectivity management across public and private network environments. More than 58% of enterprises now integrate captive portals directly with centralized identity-management systems to strengthen zero-trust network frameworks and improve authentication visibility. Network Security applications are also expanding rapidly as cyberattack attempts targeting public Wi-Fi infrastructure increased by nearly 32% during the past two years. Guest Wi-Fi Access continues to hold strong deployment relevance across hotels, airports, and commercial venues where frictionless onboarding directly impacts customer experience and operational efficiency.

Customer Analytics is emerging as the fastest-growing application due to rising enterprise demand for behavioral intelligence and location-based engagement insights. Retailers deploying analytics-integrated captive portals improved customer retention performance by approximately 21% through personalized engagement workflows. Marketing Campaigns are increasingly integrated with loyalty systems and targeted advertising infrastructure, particularly across stadiums and shopping centers. Companies are scaling AI-driven data analytics, expanding cloud-network integration, and automating user-session intelligence to strengthen operational visibility and improve monetizable customer interaction capabilities.

The Hospitality Industry remains the dominant end-user segment due to large-scale guest Wi-Fi dependency, multi-property network operations, and rising demand for personalized digital engagement services. More than 64% of premium hotel operators now integrate captive portals with loyalty management and customer analytics platforms to improve retention and optimize digital service delivery. Transportation Hubs represent the fastest-growing end-user category as airports, metro systems, and railway terminals modernize high-density connectivity infrastructure to manage millions of daily user sessions securely. Japan and the United States continue accelerating smart-transit authentication deployments linked with AI-enabled network monitoring systems.

Retail Sector adoption is strengthening through targeted advertising integration and first-party customer data collection initiatives, while Healthcare Facilities prioritize secure visitor authentication and compliance-focused access management. Educational Institutions remain major adopters because centralized captive portal frameworks simplify student access control across large campus ecosystems. Corporate Offices are increasingly implementing identity-based captive portals to support hybrid workforce environments and secure guest-network segmentation. Vendors are responding with customized subscription models, sector-specific analytics tools, and telecom ecosystem partnerships to improve deployment flexibility and strengthen competitive positioning across high-intensity enterprise environments.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.1% between 2026 and 2033.

Enterprise-Scale Secure Wi-Fi Modernization

North America maintains the highest deployment concentration in the captive portal market due to advanced enterprise networking infrastructure, large-scale public Wi-Fi ecosystems, and accelerated zero-trust cybersecurity implementation. The region contributes approximately 34% of global deployment activity, supported by extensive adoption across airports, retail chains, universities, and healthcare systems. More than 59% of enterprise-grade public Wi-Fi environments in the United States and Canada now integrate AI-enabled authentication and cloud-managed captive portal platforms. Hospitality operators and transportation hubs are expanding partnerships with telecom providers to improve real-time user analytics and secure access orchestration. Increasing cyber-risk exposure and stricter enterprise compliance frameworks are driving large-scale modernization of guest-network infrastructure across commercial environments.

United States Market Outlook: The United States leads regional deployment through large-scale enterprise networking investments, advanced cybersecurity infrastructure, and widespread public Wi-Fi monetization strategies. More than 64% of large hospitality and transportation operators have integrated centralized captive portal analytics into customer engagement and identity-management ecosystems. Airport modernization programs and smart-campus infrastructure upgrades continue accelerating demand for cloud-native authentication platforms with AI-driven traffic intelligence and behavioral analytics capabilities.

Regulatory-Led Network Security Transformation

Europe’s captive portal market is shaped by strict digital privacy regulations, enterprise cybersecurity modernization, and smart public infrastructure investments. The region accounts for nearly 27% of global deployment activity, with Germany, France, and the United Kingdom leading enterprise-grade secure-access implementations. More than 48% of European enterprises upgraded guest-network authentication systems during 2025–2026 to align with tightening data-governance and user-consent standards. Transportation operators and healthcare institutions are increasingly adopting localized authentication management and encrypted access-control frameworks. Cross-border digital infrastructure initiatives are also strengthening demand for interoperable captive portal ecosystems capable of supporting secure multi-site operations without compromising regulatory compliance or network visibility.

Germany Market Outlook: Germany remains a strategic market due to strong industrial digitalization, advanced enterprise IT infrastructure, and stringent cybersecurity governance frameworks. Approximately 44% of large German enterprises now prioritize localized captive portal deployment to support secure employee and visitor authentication across distributed facilities. Manufacturing campuses, transportation networks, and public institutions are accelerating adoption of hybrid cloud-network architectures integrated with centralized policy enforcement and encrypted access-management technologies.

Massive Public Connectivity Expansion Momentum

Asia-Pacific is emerging as the fastest-scaling captive portal market due to rapid smart-city deployment, expanding public Wi-Fi infrastructure, and rising enterprise digitalization across transportation, education, and retail sectors. The region contributes approximately 29% of global deployment activity, with China, India, Japan, and South Korea driving high-density network expansion programs. More than 52% of new public Wi-Fi infrastructure projects across major Asian urban centers now include cloud-managed captive portal integration. Telecom operators and infrastructure providers are increasing investments in AI-enabled traffic orchestration, localized authentication processing, and mobile-first onboarding systems to support rising connected-device volumes and smart mobility ecosystems.

China Market Outlook: China leads regional deployment scale through extensive smart-city investments, transportation digitization, and nationwide public connectivity expansion programs. More than 68% of newly deployed municipal Wi-Fi environments now integrate centralized captive portal management and behavioral analytics capabilities. Large commercial complexes, railway networks, and smart tourism infrastructure projects continue strengthening enterprise demand for scalable, edge-integrated authentication systems capable of managing ultra-high user-session density efficiently.

Retail and Telecom Connectivity Expansion

South America’s captive portal market is expanding steadily through telecom-led public Wi-Fi deployment, retail digitalization, and growing enterprise demand for centralized guest-network management. Brazil and Chile remain the primary deployment hubs, collectively accounting for nearly 58% of regional enterprise implementation activity. More than 41% of shopping malls, hospitality operators, and transportation facilities upgraded cloud-managed authentication systems during 2025–2026 to improve visitor analytics and secure-access visibility. Infrastructure limitations and uneven broadband modernization continue creating operational deployment disparities across secondary urban markets. Enterprises are responding through phased cloud migration strategies and telecom infrastructure partnerships designed to improve scalability while controlling implementation complexity and connectivity management costs.

Brazil Market Outlook: Brazil dominates regional captive portal deployment through large-scale retail connectivity expansion, airport modernization projects, and growing public digital infrastructure investments. Approximately 46% of enterprise guest-network upgrades in Brazil now include AI-enabled analytics and mobile-first authentication capabilities. Hospitality groups and telecom providers are strengthening localized cloud-network partnerships to improve authentication scalability, customer engagement intelligence, and centralized policy management across distributed urban commercial environments.

Smart Infrastructure Investment Acceleration

The Middle East & Africa captive portal market is advancing through smart-city investment programs, airport modernization, and hospitality-sector digital transformation initiatives. The United Arab Emirates and Saudi Arabia lead regional deployment activity, supported by large-scale public infrastructure digitization and advanced tourism connectivity projects. Nearly 39% of new commercial real-estate developments across Gulf economies now incorporate centralized captive portal systems integrated with AI-driven network analytics and access-control frameworks. Expanding transportation hubs and mixed-use developments are increasing demand for scalable guest-authentication ecosystems capable of supporting multilingual, high-density connectivity environments. Enterprises are prioritizing cloud-managed deployment models and telecom partnerships to improve operational flexibility and reduce infrastructure management complexity.

United Arab Emirates Market Outlook: The United Arab Emirates maintains strong market momentum through smart tourism infrastructure, airport expansion projects, and enterprise digital transformation strategies. More than 51% of premium hospitality properties in Dubai and Abu Dhabi now operate integrated captive portal platforms linked with customer analytics and loyalty ecosystems. Large-scale smart-building projects and government-backed digital infrastructure initiatives continue driving demand for secure, cloud-native authentication systems with centralized operational intelligence capabilities.

The captive portal market is led by Cisco, Aruba Networks, Fortinet, Extreme Networks, and Ruckus Networks, with the top five players controlling nearly 58% of global enterprise deployments. Global networking leaders compete against agile regional cloud-managed access providers, while AI-driven security innovators challenge traditional hardware-centric vendors through faster deployment cycles and analytics-led differentiation. Competition increasingly centers on cloud scalability, cybersecurity orchestration, authentication speed, and behavioral analytics integration, with enterprises demanding up to 35% faster onboarding efficiency and nearly 30% lower network management overhead. Vendors are expanding telecom partnerships, acquiring identity-management capabilities, and integrating edge-computing frameworks to strengthen distributed network performance. Japanese and U.S. operators prioritize AI-enabled authentication precision, while cost-focused Latin American providers emphasize subscription-based deployment flexibility. Rising regulatory compliance costs and interoperability complexity create strong entry barriers for smaller providers. Winning requires scalable cloud-native architecture, advanced security intelligence, and enterprise-grade integration capabilities across multi-site digital connectivity ecosystems.

Cisco Systems

Aruba Networks

Fortinet

Extreme Networks

Ruckus Networks

Huawei Technologies

Juniper Networks

Ubiquiti Inc.

Cambium Networks

Purple WiFi

IronWiFi

Cloud4Wi

Boingo Wireless

Tanaza

Cloud-native captive portal platforms are replacing legacy appliance-based systems across enterprise Wi-Fi environments due to faster orchestration, centralized authentication, and AI-enabled network visibility. More than 61% of large enterprises now deploy cloud-managed captive portal infrastructure integrated with zero-trust access frameworks. Compared with traditional on-premises authentication systems, cloud-native architectures reduce configuration workloads by nearly 42% and improve session analytics accuracy by 35%. Hospitality operators, airports, and universities are prioritizing API-driven integration with CRM, identity-management, and behavioral analytics systems to strengthen user personalization and operational efficiency.

Emerging technologies are shifting captive portals from basic login gateways toward intelligent engagement and cybersecurity ecosystems. AI-driven traffic orchestration improves network congestion management by approximately 29%, while passwordless authentication deployments increased by 41% during 2025–2026. Edge-computing integration is also accelerating, particularly across smart transportation and retail infrastructure in Japan and the United States, where localized data processing reduces authentication latency by 24%. Vendors are scaling telecom partnerships and AI-security integration to improve multi-site deployment consistency and compliance-driven identity governance.

Between 2026 and 2028, biometric verification, behavioral authentication, and AI-assisted network automation will become major competitive differentiators. Enterprises adopting predictive network analytics are expected to lower unauthorized access incidents by nearly 31%, benefiting providers capable of delivering scalable, encrypted, analytics-centric captive portal ecosystems.

June 2025 – Cisco Systems launched AI-powered secure network architecture integrating unified management and low-latency campus networking, reducing network task execution from hours to minutes through AgenticOps automation. The rollout strengthened enterprise captive portal scalability and AI-driven authentication efficiency across distributed workplaces. Source: newsroom.cisco.com

August 2024 – Fortinet expanded its unified SASE platform with sovereign cloud capabilities and generative AI integration, strengthening secure guest-access management and centralized authentication visibility. The enhancement improved deployment flexibility for enterprises managing multi-site captive portal environments under tightening cybersecurity and data-localization regulations. Source: investor.fortinet.com

February 2026 – Cisco Systems introduced the Silicon One G300 networking chip using 3-nanometer architecture, accelerating AI networking workloads by up to 28% while improving traffic rerouting efficiency within microseconds. The development strengthened high-density captive portal infrastructure performance across enterprise and transportation connectivity ecosystems.

May 2026 – Cisco Systems initiated AI-focused operational restructuring after networking product orders increased more than 50% and data-center switching demand rose above 40%. The company redirected investments toward silicon, security, and edge-network infrastructure to strengthen scalable authentication and AI-enabled enterprise connectivity capabilities. Source: reuters.com

The Captive Portal Market report delivers detailed analysis across Cloud-Based, On-Premises, Wi-Fi Captive Portals, Social Login Portals, and Mobile Captive Portals, covering evolving deployment priorities and enterprise networking modernization trends between 2026 and 2033. The study evaluates operational demand across Guest Wi-Fi Access, User Authentication, Marketing Campaigns, Network Security, and Customer Analytics applications, alongside adoption patterns across hospitality, transportation, retail, healthcare, education, and corporate environments. More than 60% of enterprise deployments analyzed within the report involve cloud-managed authentication infrastructure integrated with AI-driven analytics and zero-trust security frameworks.

The report further examines strategic regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, infrastructure modernization, and regulatory transformation influencing enterprise investment decisions. It also evaluates competitive positioning, AI-enabled authentication innovation, edge-network integration, telecom ecosystem partnerships, and passwordless authentication adoption shaping future operational strategies and scalable captive portal deployment models.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1608 Million |

Market Revenue in 2033 | USD 5381.75 Million |

CAGR (2026 - 2033) | 16.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Cisco Systems, Aruba Networks, Fortinet, Extreme Networks, Ruckus Networks, Huawei Technologies, Juniper Networks, Ubiquiti Inc., Cambium Networks, Purple WiFi, IronWiFi, Cloud4Wi, Boingo Wireless, Tanaza |

Customization & Pricing | Available on Request (10% Customization is Free) |