Reports

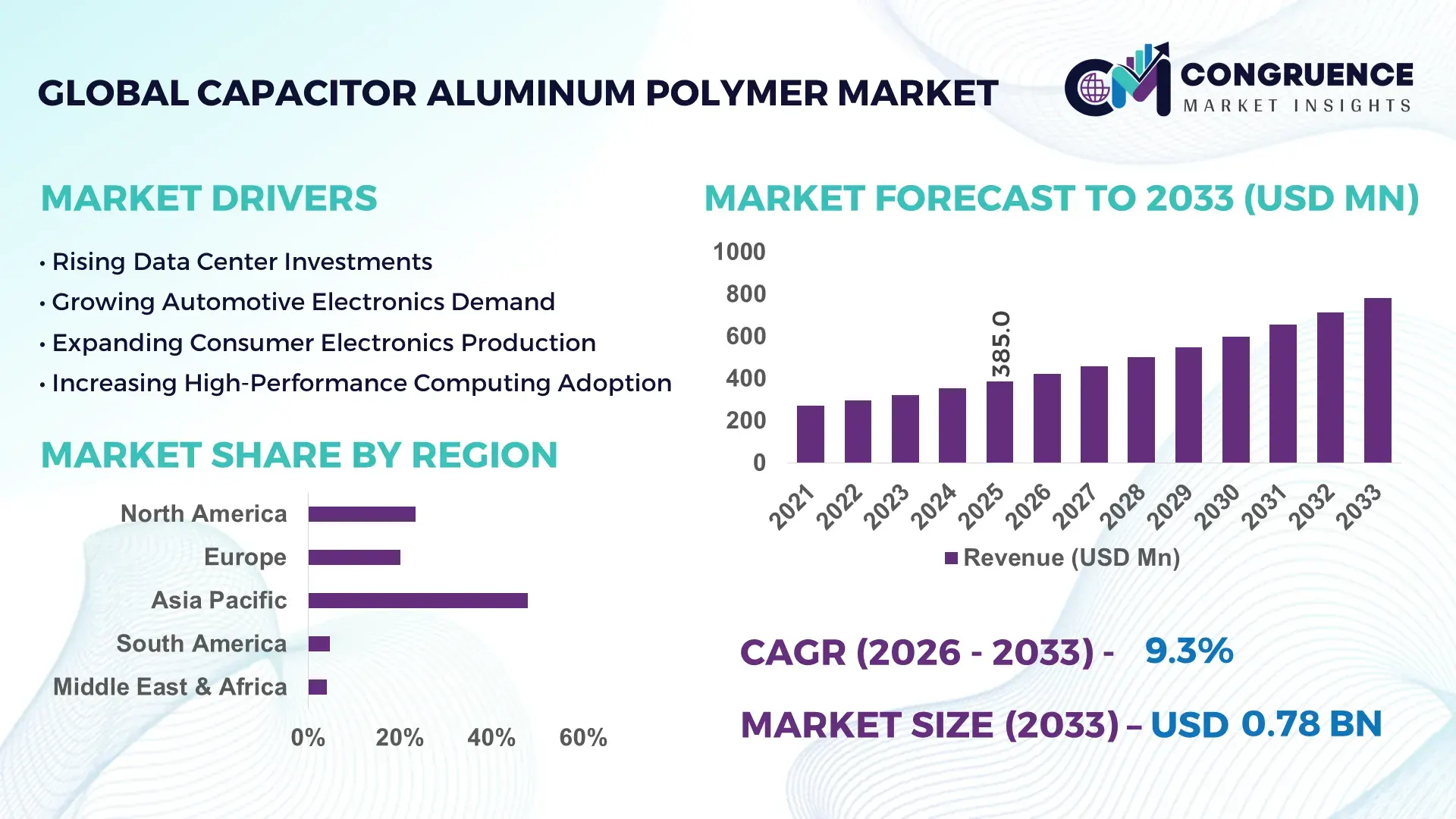

The Global Capacitor Aluminum Polymer Market was valued at USD 385.0 Million in 2025 and is anticipated to reach a value of USD 781.3 Million by 2033 expanding at a CAGR of 9.25% between 2026 and 2033. Rapid electrification of vehicles, rising deployment of high-density power electronics, and increasing demand for low-ESR capacitors in AI servers and industrial automation systems are accelerating market expansion.

China remains the dominant country, accounting for approximately 42% of global aluminum polymer capacitor manufacturing capacity, supported by over USD 18 billion in electronics component investments and a consumer electronics output exceeding 1.6 billion smart devices annually. Japan contributes nearly 21% of premium-grade capacitor production with stronger penetration in automotive electronics, while China maintains over 2x the manufacturing scale. The ongoing semiconductor localization initiatives following global supply-chain realignments continue to strengthen domestic component ecosystems.

Strategically, suppliers with advanced polymer formulations and localized manufacturing footprints are securing stronger positions across automotive, industrial, and high-performance computing value chains.

Market Size & Growth: USD 385.0 Million in 2025, projected to reach USD 781.3 Million by 2033, driven by rising AI server deployments, EV power systems, and advanced industrial electronics; CAGR stands at 9.25%.

Top Growth Drivers: EV electronics demand up 28%, AI data-center power infrastructure expansion above 30%, and industrial automation investments increasing by 18%.

Short-Term Forecast: By 2028, capacitor energy-efficiency performance is expected to improve by 15% while power-loss rates decline by nearly 12%.

Emerging Technologies: Conductive polymer innovations, automated capacitor assembly, and AI-enabled quality inspection are reducing defect rates by over 20%.

Regional Leaders: Asia Pacific exceeds USD 340 Million, North America approaches USD 180 Million, and Europe surpasses USD 140 Million, supported by electronics localization initiatives.

Consumer/End-User Trends: More than 65% of next-generation EV control modules are integrating advanced polymer capacitor architectures for improved thermal stability.

Pilot/Case Example: A 2024 automotive electronics upgrade program improved power-conversion efficiency by 14% through polymer capacitor integration.

Competitive Landscape: Top five suppliers collectively control approximately 55% of market activity, led by Panasonic, Nichicon, Rubycon, Nippon Chemi-Con, and KYOCERA AVX.

Regulatory & ESG Impact: Energy-efficiency standards are reducing electronic system losses by 10–15% across advanced power-management applications.

Investment & Funding: More than USD 2 billion has been committed globally toward electronic component expansion, localization, and manufacturing modernization.

Innovation & Future Outlook: High-temperature polymer materials, ultra-low ESR designs, and AI hardware optimization are reshaping next-generation capacitor strategies.

Capacitor Aluminum Polymer Market demand is increasingly concentrated in electric vehicles, advanced computing systems, telecommunications infrastructure, and industrial power management equipment. Recent innovations focus on ultra-low ESR designs, higher temperature tolerance, and miniaturized high-capacitance components. Nearly 35% of new high-performance power modules now utilize polymer-based capacitor architectures. Ongoing electronics supply-chain diversification and semiconductor ecosystem expansion are creating new procurement and design opportunities, setting the stage for deeper strategic evaluation.

The Capacitor Aluminum Polymer Market has become strategically important as manufacturers seek higher power efficiency, greater thermal stability, and compact component architectures across automotive, industrial, telecommunications, and computing applications. The market sits at the intersection of vehicle electrification, AI infrastructure expansion, and industrial digitalization. Recent supply-chain restructuring initiatives have encouraged electronics manufacturers to diversify sourcing networks and establish regional component ecosystems to improve operational resilience.

From a technology perspective, aluminum polymer capacitors deliver up to 40% lower equivalent series resistance compared with several conventional electrolytic capacitor configurations, enabling improved power delivery and reduced heat generation. Japan continues to lead in premium-grade capacitor engineering and reliability-focused applications, while China dominates large-scale production and manufacturing capacity. Over the next two to three years, adoption within AI servers, EV power control units, and industrial automation equipment is expected to accelerate as equipment manufacturers prioritize efficiency gains and footprint reduction.

A practical example can be seen in advanced automotive control systems where polymer capacitor integration improves voltage stability under high-load operating conditions. Companies are expanding partnerships with semiconductor suppliers, increasing investment in automated production lines, and strengthening regional manufacturing footprints. Organizations that secure technology differentiation, supply assurance, and advanced materials expertise will establish stronger competitive positioning and long-term operational advantages.

The rapid transition toward electrified transportation and advanced digital infrastructure is significantly increasing demand for aluminum polymer capacitors. More than 70% of modern EV power-control architectures now require enhanced thermal stability and low-resistance power management components. AI server installations have expanded by over 25% annually in major data-center markets, increasing requirements for high-reliability power-delivery systems. Following semiconductor and electronics supply-chain disruptions, manufacturers in China, Japan, and South Korea have accelerated investments in localized component production. This shift improves supply security while expanding manufacturing capacity. In response, capacitor producers are scaling automated production lines, developing next-generation conductive polymer technologies, and forming strategic partnerships with automotive and semiconductor companies. A notable insight is that power-density optimization has become a purchasing priority, elevating capacitor performance from a component-level consideration to a system-level design requirement.

Material cost instability remains a structural limitation for market participants. Conductive polymer compounds and specialty aluminum materials have experienced periodic price fluctuations exceeding 15% during supply disruptions. Energy-intensive manufacturing operations can account for nearly 20% of total production costs in certain facilities, reducing margin flexibility. Japan and South Korea continue to face elevated input-cost pressures due to dependence on specialized material supply chains. These challenges directly affect pricing strategies, inventory planning, and long-term procurement agreements. To mitigate risk, manufacturers are expanding supplier networks, localizing portions of production, and implementing long-duration sourcing contracts. A key operational insight is that firms with vertically integrated material procurement structures maintain stronger pricing stability and greater responsiveness during supply-chain volatility compared with manufacturers relying heavily on external sourcing.

The proliferation of AI computing infrastructure, intelligent manufacturing systems, and advanced telecommunications equipment is creating significant opportunity for aluminum polymer capacitor suppliers. Data-center power demand associated with AI workloads is increasing by more than 20% annually, while industrial automation deployments continue expanding across major manufacturing economies. New conductive polymer technologies are delivering approximately 15% improvements in thermal performance and operational reliability. India and Southeast Asian manufacturing hubs are emerging as attractive locations for electronics assembly and component integration due to expanding domestic electronics ecosystems. Companies are responding through R&D investments, joint-development agreements, and ecosystem partnerships with semiconductor and power-management firms. An important strategic insight is that suppliers capable of co-designing components alongside system manufacturers can secure higher-value positions within next-generation electronics supply chains.

As application requirements become more demanding, ensuring long-term reliability across diverse operating environments presents a major challenge. Automotive electronics often require operational consistency under temperature variations exceeding 125°C, while industrial systems demand extended service life and uninterrupted performance. Product qualification cycles can increase development timelines by 20–30%, particularly in safety-critical applications. The growing complexity of AI servers, renewable energy systems, and advanced industrial equipment further intensifies testing requirements. Companies must invest in advanced simulation platforms, accelerated lifecycle testing, and quality-control automation to maintain competitiveness. A critical operational insight is that reliability certification increasingly influences supplier selection decisions as much as pricing or capacity. Organizations that establish robust validation capabilities and application-specific engineering support will achieve stronger deployment consistency and long-term market relevance.

AI Server Power Optimization – Data-center operators are redesigning power-delivery architectures as AI rack densities increase by nearly 35%, driving a 22% rise in demand for ultra-low ESR capacitor configurations. Server manufacturers in China and the United States are integrating higher-capacitance polymer designs to reduce voltage fluctuation and improve processing stability. This transition is shortening power-management response times by approximately 15%, while suppliers are expanding automated production and advanced material partnerships to meet performance-focused procurement requirements.

Localized Electronics Supply Chains – Following semiconductor supply disruptions and industrial policy shifts, electronics manufacturers have increased regional component sourcing by roughly 18%. Japan and South Korea are strengthening domestic capacitor ecosystems through supplier consolidation and manufacturing modernization. Lead-time reductions approaching 20% are improving inventory efficiency and production planning. Companies are responding through facility upgrades, dual-sourcing strategies, and closer collaboration with semiconductor and automotive OEMs to improve operational resilience and procurement visibility.

Miniaturization Across Industrial Systems – Industrial automation equipment and compact power modules are driving a 25% increase in demand for smaller high-capacitance components. Advanced conductive polymer formulations are enabling footprint reductions of nearly 30% without sacrificing electrical performance. This trend supports faster product development cycles and improved equipment density. Manufacturers are accelerating investment in precision assembly technologies and automated inspection systems to maintain quality consistency while scaling production volumes.

High-Temperature Reliability Focus – Automotive electrification and industrial power applications are increasing demand for components capable of operating above 125°C. Reliability qualification requirements have expanded by nearly 20% in critical electronics programs, prompting greater emphasis on endurance testing and material engineering. A less obvious shift is the growing use of predictive quality analytics, reducing defect identification time by approximately 15%. Companies are strengthening testing infrastructure, implementing AI-assisted quality control, and forming long-term technology partnerships to enhance lifecycle performance.

Conductive Polymer Aluminum Electrolytic Capacitors remain the leading type segment, accounting for approximately 48% of total market demand due to their superior low-ESR performance, compact form factor, and strong integration across automotive electronics, industrial controllers, and computing equipment. Their ability to support stable power delivery and high-frequency operation makes them a preferred choice in advanced electronic assemblies. Manufacturers continue prioritizing this category through material innovation and production expansion. Hybrid Polymer Capacitors represent the fastest-growing type, supported by rising demand for improved ripple-current performance and enhanced reliability in electric vehicle systems and industrial power supplies. Traditional Aluminum Electrolytic Capacitors continue serving cost-sensitive applications where scale and affordability remain critical, while Specialty Polymer Capacitors are gaining traction in high-performance and mission-critical electronics. Hybrid configurations have experienced adoption increases exceeding 20% in advanced power-management designs, while conductive polymer solutions maintain penetration above 60% in premium electronic systems. Companies are expanding product portfolios, developing application-specific capacitor platforms, and strengthening OEM partnerships to address shifting design requirements and performance expectations.

Automotive Electronics represents the leading application segment, supported by the rapid proliferation of electric vehicles, advanced driver-assistance systems, battery-management platforms, and onboard power-conversion modules. Approximately 40% of total capacitor aluminum polymer consumption is linked to vehicle electronics, where thermal stability and voltage regulation are operationally critical. The fastest-growing application is AI and Data Center Infrastructure, driven by increasing server power density, accelerated computing deployments, and next-generation networking equipment. Adoption within AI-related power systems has expanded by more than 25% as operators seek improved efficiency and system reliability. Industrial Equipment remains a stable and mature application area due to automation investments and smart manufacturing initiatives, while Consumer Electronics continues generating significant volume demand through laptops, gaming devices, and communication hardware. Telecommunications Infrastructure is evolving through 5G expansion and network modernization projects, increasing demand for compact power-management solutions. Companies are scaling production capacity, integrating advanced automation, and developing application-specific capacitor platforms to address differentiated performance requirements across each end-use environment.

Consumer Electronics and Electronics Manufacturing Companies constitute the dominant end-user group, representing nearly 45% of overall demand due to large-scale production of smartphones, laptops, networking equipment, and intelligent electronic devices. High-volume manufacturing operations require compact, reliable, and thermally efficient capacitor technologies capable of supporting increasingly complex circuit architectures. The fastest-growing end-user category is Automotive OEMs and Tier-1 Suppliers, where electrification programs and advanced electronic content per vehicle are increasing procurement requirements. Capacitor utilization in vehicle power-management systems has risen by approximately 22% across new platform designs. Industrial Equipment Manufacturers maintain strong purchasing activity driven by automation, robotics, and factory digitalization initiatives, while Telecommunications Operators and Infrastructure Providers continue investing in network modernization and power-efficiency improvements. Data-center operators are emerging as an increasingly influential buyer group as computing intensity rises. To strengthen market positioning, suppliers are introducing customized capacitor solutions, forming long-term supply agreements, and expanding technical support capabilities for strategic customers. Competitive differentiation is increasingly linked to reliability engineering, application-specific design expertise, and supply-chain responsiveness rather than price alone.

Asia-Pacific accounted for the largest market share at 47.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2026 and 2033.

North America represents approximately 23.4% of global market activity, supported by strong deployment of AI data centers, advanced semiconductor manufacturing, industrial automation systems, and electric vehicle technologies. The region maintains a high concentration of high-performance computing infrastructure, where power-efficiency optimization has become a critical procurement criterion. More than 30% of newly commissioned hyperscale computing facilities are integrating advanced low-ESR power-management architectures. Ongoing investments in semiconductor reshoring and electronics manufacturing modernization continue strengthening component sourcing strategies. Market participants are increasingly focusing on application-specific capacitor solutions designed for high-density computing, telecommunications infrastructure, and industrial control platforms, improving operational reliability and reducing power losses across mission-critical systems.

United States Market Outlook: The United States remains the primary market contributor due to its leadership in AI infrastructure, semiconductor investment, defense electronics, and advanced manufacturing. More than 50 large-scale semiconductor and electronics projects have entered expansion or development phases in recent years, strengthening demand for high-performance capacitor technologies. The country's extensive cloud computing ecosystem and growing EV production base continue driving adoption of advanced power-management components. Domestic manufacturers are prioritizing supply-chain resilience, automation investments, and strategic technology partnerships to support increasingly sophisticated electronics applications.

Europe accounts for nearly 20.1% of market participation, supported by strong automotive electronics production, industrial automation investments, and energy-efficiency initiatives. Demand is increasingly influenced by vehicle electrification programs and modernization of industrial power systems. Advanced manufacturing facilities across the region are adopting compact electronic architectures to improve operational efficiency and equipment reliability. More than 25% of new industrial automation projects now incorporate enhanced power-management technologies designed to reduce energy losses and improve system stability. Manufacturers are emphasizing sustainability, product reliability, and localized sourcing strategies while expanding collaboration across automotive and industrial supply chains to strengthen long-term competitiveness.

Germany Market Outlook: Germany serves as the region's most influential market due to its extensive automotive manufacturing ecosystem, industrial automation leadership, and engineering-intensive electronics sector. The country accounts for a substantial share of advanced industrial equipment production and remains a key adopter of next-generation power electronics. Automotive electrification initiatives continue accelerating demand, with electronic content per vehicle increasing steadily across premium and commercial platforms. German enterprises are investing heavily in smart manufacturing technologies and advanced production facilities to enhance efficiency, reliability, and supply-chain responsiveness.

Asia-Pacific contributes approximately 47.8% of global market demand and remains the industry's primary manufacturing and deployment hub. The region benefits from large-scale electronics production, integrated semiconductor ecosystems, and extensive supply-chain infrastructure. China, Japan, South Korea, and Taiwan collectively account for a dominant share of capacitor manufacturing capacity and downstream electronics assembly activity. Electronics exports from major production centers continue expanding, while investments in semiconductor localization and advanced manufacturing exceed previous development cycles. Companies are increasing automation adoption, expanding production footprints, and strengthening material sourcing networks to support growing requirements from automotive electronics, consumer devices, telecommunications equipment, and industrial systems.

China Market Outlook: China maintains the strongest market position due to its vast electronics manufacturing base, semiconductor expansion programs, and integrated supply-chain infrastructure. The country is estimated to account for more than 40% of global aluminum polymer capacitor production capacity. Strong domestic demand from electric vehicles, telecommunications equipment, industrial automation, and consumer electronics supports continuous capacity utilization. Manufacturers are investing in advanced production technologies, localized material sourcing, and next-generation component development to improve competitiveness and strengthen supply assurance across domestic and export-oriented markets.

South America represents approximately 4.7% of global market activity, with growth supported by industrial modernization, telecommunications upgrades, and increasing adoption of automated production systems. Demand remains concentrated in industrial equipment, consumer electronics assembly, and power infrastructure applications. Electronics manufacturing capabilities are expanding gradually, supported by investment programs focused on improving local production capacity and reducing import dependence. Several infrastructure modernization initiatives have increased deployment of power-management systems by nearly 15% in selected industrial sectors. However, supply-chain limitations and dependence on imported electronic components continue influencing procurement strategies and production economics across the region.

Brazil Market Outlook: Brazil is the leading market within South America due to its industrial scale, manufacturing activity, and telecommunications infrastructure investments. The country hosts the region's largest electronics assembly ecosystem and continues expanding industrial automation deployment across key manufacturing sectors. Growing investments in smart factories, power distribution systems, and connected infrastructure are increasing demand for advanced capacitor technologies. Domestic enterprises are strengthening partnerships with international component suppliers while improving local assembly capabilities to support operational efficiency and supply continuity.

Middle East & Africa accounts for roughly 4.0% of global market demand, supported by investments in digital infrastructure, industrial diversification, telecommunications modernization, and smart-city development programs. Demand is increasing within data centers, power-management systems, industrial facilities, and communications networks. Governments and enterprises are prioritizing technology-enabled infrastructure projects, creating stronger requirements for reliable electronic components. More than 20% of recently announced digital infrastructure projects incorporate advanced power-efficiency objectives, driving adoption of higher-performance electronic architectures. Companies are expanding regional distribution networks, strengthening technical support capabilities, and pursuing partnerships aligned with infrastructure transformation priorities.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's most strategically important market due to large-scale infrastructure investment, industrial diversification programs, and expanding digital economy initiatives. Data-center development, smart-city projects, and industrial modernization efforts are increasing demand for advanced power-management technologies across multiple sectors. The country continues attracting technology and manufacturing partnerships aimed at strengthening local industrial capabilities. Growing deployment of telecommunications infrastructure and intelligent industrial systems is creating sustained demand for high-reliability capacitor solutions designed for demanding operating environments.

The market is led by Panasonic Industry, Nichicon Corporation, KYOCERA AVX, Rubycon Corporation, and Nippon Chemi-Con, which collectively control approximately 55–60% of global market activity. Competition is primarily between Japanese technology leaders and cost-focused Asian manufacturers, while automotive-grade specialists compete directly with industrial and communications-focused suppliers. Technology performance, thermal endurance, low ESR characteristics, and supply reliability have become more influential than pricing alone. Automotive-qualified products command procurement preference in over 65% of high-reliability applications, while advanced polymer solutions deliver up to 40% lower ESR than conventional alternatives. Companies are competing through capacity expansion, localized manufacturing, strategic OEM partnerships, and proprietary polymer-material development.

The competitive shift is moving toward supply-chain control and application-specific engineering rather than volume production. Strict qualification requirements, long design cycles, and reliability certification create substantial entry barriers. Winning requires differentiated performance, manufacturing resilience, and deep customer integration capabilities.

KYOCERA AVX

Rubycon Corporation

Nippon Chemi-Con Corporation

YAGEO Corporation

Vishay Intertechnology

Cornell Dubilier Electronics

KEMET Corporation

Samwha Capacitor Group

Lelon Electronics Corp.

Jianghai Capacitor Co., Ltd.

APAQ Technology Co., Ltd.

Conductive polymer technology is becoming the defining innovation across the market. Compared with conventional liquid-electrolyte capacitors, advanced polymer architectures provide up to 40% lower ESR and approximately 20% better ripple-current performance, improving power stability in automotive electronics, AI servers, and industrial controllers. Adoption has exceeded 60% in premium power-management applications where thermal reliability and compact design are operational priorities. Manufacturers with proprietary polymer formulations benefit through stronger qualification rates and deeper integration into high-value electronics platforms.

Emerging technologies focus on hybrid polymer-electrolyte designs, AI-assisted quality inspection, and automated precision manufacturing. Hybrid capacitors improve thermal endurance by approximately 15% while maintaining low-resistance characteristics required in vehicle electrification systems. Automated inspection platforms have reduced defect-detection times by nearly 20%, supporting higher production consistency. More than 45% of newly introduced automotive-grade capacitor platforms now incorporate advanced hybrid architectures. This shift is strengthening competitive positioning for suppliers capable of combining reliability engineering with scalable manufacturing operations.

Between 2026 and 2028, disruptive advances in high-temperature conductive materials, ultra-miniaturized capacitor structures, and intelligent manufacturing systems will reshape product development priorities. Suppliers investing early in high-density energy-storage designs and next-generation polymer chemistry are expected to achieve faster qualification cycles, stronger OEM engagement, and improved deployment across AI infrastructure, telecommunications equipment, and advanced mobility platforms.

April 2025 – Nichicon Corporation developed the GYG Series conductive polymer hybrid aluminum electrolytic capacitors featuring up to 1.8× higher ripple current than its GYA series, enabling circuit miniaturization and improved automotive and communications performance. This strengthens Nichicon’s high-reliability product portfolio.

April 2025 – Nichicon Corporation introduced the GWC Series hybrid capacitors delivering approximately 10% higher ripple current capacity than the previous GXC series while maintaining high-temperature endurance. The launch improves power-density optimization for automotive and industrial electronics applications.

September 2025 – Panasonic Industry commercialized new POSCAP conductive polymer capacitors with an industry-leading 3 mm profile, supporting USB Power Delivery 3.1 applications. The innovation enables device miniaturization and higher power density in laptops, tablets, and communication equipment. Source: www.news.panasonic.com

February 2024 – KYOCERA AVX launched TCD Series DLA 04051 and COTS-Plus conductive polymer capacitors for aerospace, defense, and industrial applications. The products feature very low ESR and high-frequency capacitance retention, strengthening KYOCERA AVX’s position in mission-critical electronics markets.

The report provides comprehensive analysis of the Capacitor Aluminum Polymer Market across major product types, applications, end-user industries, and regional markets. Coverage includes conductive polymer capacitors, hybrid polymer capacitors, traditional aluminum electrolytic variants, and specialized high-performance configurations. The study evaluates demand patterns across automotive electronics, industrial equipment, telecommunications infrastructure, AI data centers, consumer electronics, and emerging power-management applications. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering manufacturing concentration, deployment trends, and supply-chain positioning.

The report further examines technology evolution, material innovations, competitive dynamics, procurement strategies, and operational benchmarks influencing industry development. More than 60% of analysis focuses on high-growth deployment environments including electrified mobility, advanced computing infrastructure, and industrial automation. Strategic insights support investment planning, capacity expansion, product development prioritization, partnership evaluation, and competitive positioning. The study also highlights emerging opportunities in localized manufacturing, advanced polymer technologies, and next-generation electronics ecosystems expected to shape market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 385.0 Million |

| Market Revenue (2033) | USD 781.3 Million |

| CAGR (2026–2033) | 9.25% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Panasonic Industry; Nichicon Corporation; KYOCERA AVX; Rubycon Corporation; Nippon Chemi-Con Corporation; YAGEO Corporation; Vishay Intertechnology; Cornell Dubilier Electronics; KEMET Corporation; Samwha Capacitor Group; Lelon Electronics Corp.; Jianghai Capacitor Co., Ltd.; APAQ Technology Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |