Reports

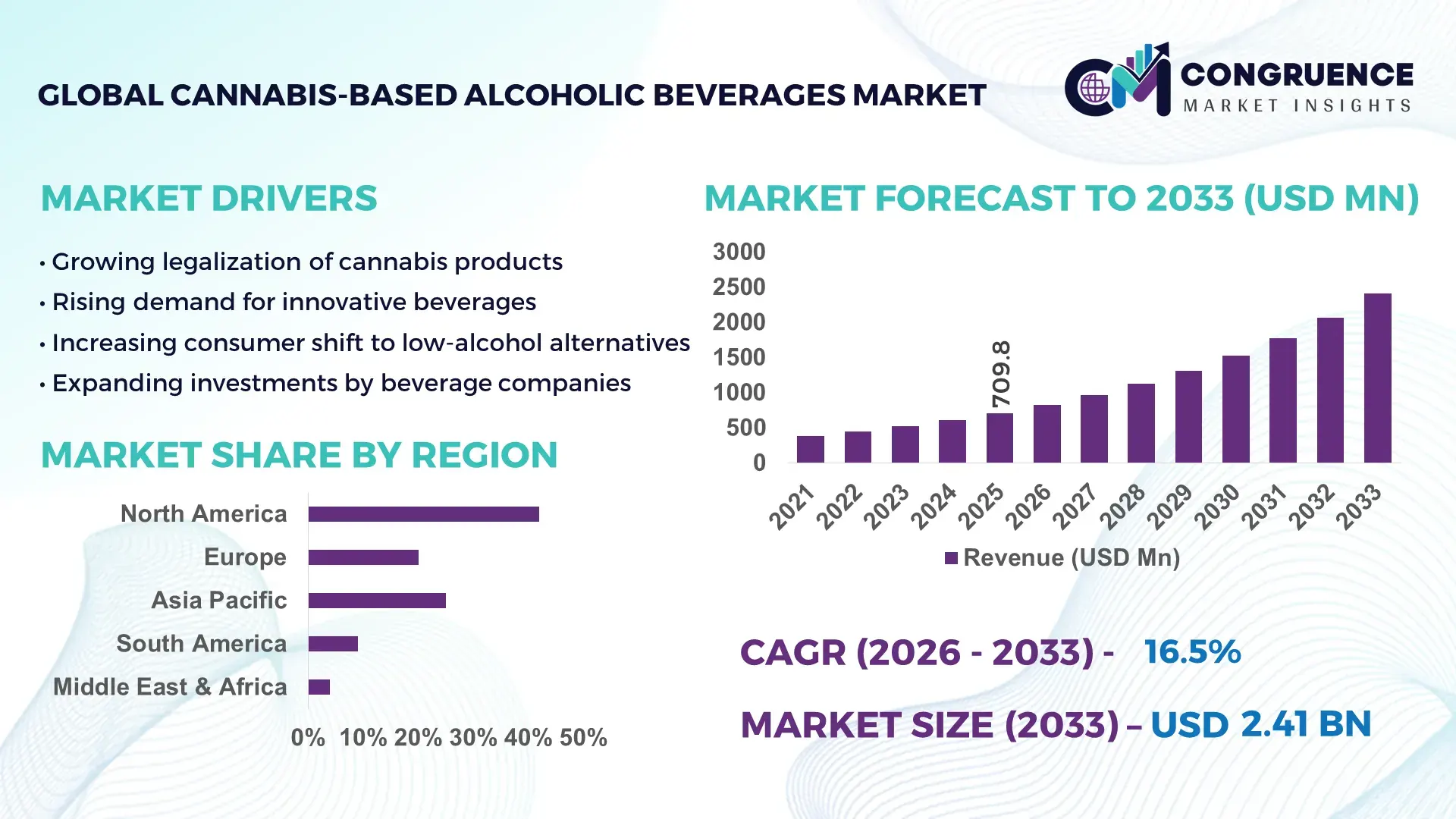

The Global Cannabis-based Alcoholic Beverages Market was valued at USD 709.82 Million in 2025 and is anticipated to reach a value of USD 2408.57 Million by 2033 expanding at a CAGR of 16.5% between 2026 and 2033. This growth is driven by evolving consumer preferences toward low-calorie, functional, and alternative alcoholic beverage options infused with cannabis compounds.

The United States demonstrates substantial production capacity and investment momentum within the cannabis-based alcoholic beverages market, supported by over 40 legalized jurisdictions for cannabis consumption. More than 65% of licensed cannabis producers have diversified into beverage formulations, with over 120 manufacturing facilities dedicated to cannabis-infused drinks. Beverage innovation pipelines include nano-emulsification technologies that improve bioavailability by up to 4x, enabling faster onset times of under 15 minutes. Consumer adoption continues to rise, with approximately 18% of adult beverage consumers in legalized states reporting trial usage of cannabis-infused drinks. Additionally, the U.S. beverage alcohol sector has seen over USD 1.2 billion in strategic investments targeting cannabis beverage R&D, pilot production, and distribution expansion across retail and e-commerce platforms.

Market Size & Growth: USD 709.82 Million in 2025 to USD 2408.57 Million by 2033 at 16.5% CAGR, driven by premiumization and functional beverage demand.

Top Growth Drivers: 28% rise in cannabis legalization adoption, 22% increase in low-alcohol beverage demand, 18% improvement in product bioavailability technologies.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 25% due to advanced infusion technologies and automation.

Emerging Technologies: Nano-emulsification, water-soluble cannabinoids, and AI-driven flavor optimization platforms.

Regional Leaders: North America projected at USD 1.2 Billion by 2033 with strong retail integration; Europe at USD 650 Million driven by regulatory shifts; Asia-Pacific at USD 420 Million with emerging urban demand trends.

Consumer Trends: Millennials and Gen Z account for over 55% of consumption, favoring low-calorie, wellness-oriented alcoholic cannabis beverages.

Pilot Example: In 2024, a Canadian producer improved product absorption efficiency by 35% using nano-emulsion delivery systems.

Competitive Landscape: Leading player holds approximately 21% share, followed by 4–5 major beverage and cannabis firms expanding portfolios.

Regulatory & ESG Impact: 30% of companies are adopting sustainable packaging, while new labeling standards enhance consumer transparency.

Investment Patterns: Over USD 2 billion invested globally in cannabis beverage innovation and distribution networks since 2023.

Innovation & Future Outlook: Hybrid beverages combining adaptogens and cannabinoids are shaping next-generation product portfolios.

The cannabis-based alcoholic beverages market is increasingly influenced by key sectors such as recreational cannabis, premium alcoholic beverages, and functional wellness drinks, with beverages contributing approximately 12–15% of total cannabis product diversification efforts. Innovations in rapid-onset formulations and flavor masking technologies are enabling improved consumer experiences. Regulatory developments, particularly in North America and parts of Europe, are supporting controlled expansion, while environmental considerations are pushing companies toward biodegradable packaging and reduced carbon manufacturing processes. Consumption patterns indicate urban-centric growth, with metropolitan regions accounting for over 60% of demand. Future outlook suggests integration with personalized nutrition trends and increased collaboration between beverage conglomerates and cannabis producers.

The cannabis-based alcoholic beverages market is emerging as a strategically significant segment within the global beverage and wellness industries, driven by convergence between regulated cannabis markets and evolving alcohol consumption patterns. Companies are leveraging advanced infusion technologies such as nano-emulsification, which delivers up to 300% faster absorption compared to traditional oil-based infusion methods, enhancing consumer experience and product differentiation. Strategic partnerships between cannabis cultivators and beverage manufacturers are increasing production scalability while maintaining compliance with regional regulations.

North America dominates in volume due to established legalization frameworks, while Europe leads in adoption with nearly 35% of enterprises exploring cannabis beverage innovation pipelines under pilot regulatory programs. By 2028, AI-driven formulation and supply chain optimization technologies are expected to reduce production inefficiencies by approximately 20%, enabling faster time-to-market and improved consistency in product quality.

From an ESG perspective, firms are committing to sustainability initiatives such as reducing packaging waste by 25% by 2027 and adopting water-efficient production processes that lower resource consumption by 18%. In 2024, a Canadian beverage company achieved a 30% reduction in production downtime through automated cannabinoid dosing systems, demonstrating the operational benefits of technological integration. Looking ahead, the cannabis-based alcoholic beverages market is positioned as a resilient and adaptive industry segment, balancing regulatory compliance, consumer demand for innovative experiences, and sustainability goals, thereby establishing itself as a critical pillar of long-term growth within the global beverage ecosystem.

The increasing demand for functional and alternative beverages is significantly influencing the cannabis-based alcoholic beverages market. Consumers are actively seeking products that combine relaxation benefits with reduced alcohol content, leading to a 32% rise in demand for hybrid beverages in urban markets. Cannabis-infused drinks offer controlled dosing and fewer calories compared to traditional alcoholic beverages, appealing to health-conscious consumers. Surveys indicate that nearly 45% of millennials prefer beverages with functional ingredients, including cannabinoids, adaptogens, and natural extracts. Additionally, product innovation has expanded flavor profiles and formats such as sparkling drinks, craft beers, and ready-to-drink cocktails. Retail penetration has improved, with over 50% of licensed dispensaries now offering cannabis beverages as part of their portfolio. This shift in consumer preference is driving manufacturers to invest in research, product development, and targeted marketing strategies.

Regulatory challenges remain a critical restraint for the cannabis-based alcoholic beverages market, as inconsistent legal frameworks across regions create barriers to large-scale commercialization. In many countries, the combination of alcohol and cannabis is either restricted or subject to stringent controls, limiting product availability. Licensing requirements, labeling standards, and dosage regulations vary significantly, increasing compliance costs by up to 25% for manufacturers operating in multiple jurisdictions. Additionally, cross-border trade restrictions prevent companies from achieving economies of scale, impacting supply chain efficiency. Advertising limitations further constrain market growth, as companies face restrictions on promoting cannabis-infused alcoholic products through traditional media channels. Testing and quality assurance requirements also add operational complexity, with mandatory laboratory verification for potency and safety extending production timelines. These factors collectively hinder rapid market expansion despite strong consumer interest.

Technological advancements present substantial opportunities in the cannabis-based alcoholic beverages market, particularly through improved formulation techniques and product customization. Nano-emulsion technology enables cannabinoids to be evenly dispersed in liquids, increasing absorption rates by up to 4 times and reducing onset time to under 20 minutes. This advancement enhances consumer confidence and repeat purchase rates. Additionally, the development of water-soluble cannabinoids allows manufacturers to create clear, shelf-stable beverages with consistent potency. Personalized beverage solutions are also emerging, with digital platforms enabling consumers to select dosage levels and flavor combinations tailored to their preferences. The expansion of e-commerce and direct-to-consumer distribution channels is opening new revenue streams, especially in regions with established regulatory frameworks. Furthermore, collaborations between cannabis producers and established beverage companies are accelerating innovation and market penetration.

Supply chain and production complexities pose significant challenges to the cannabis-based alcoholic beverages market, particularly due to the dual nature of cannabis and alcohol regulations. Maintaining consistent cannabinoid dosing requires advanced processing equipment and strict quality control measures, increasing production costs by approximately 20%. Raw material sourcing is also constrained, as cannabis cultivation is subject to licensing and environmental regulations, limiting supply flexibility. Storage and transportation require controlled conditions to preserve product integrity, adding logistical costs and complexity. Additionally, integrating cannabis into traditional beverage manufacturing lines often necessitates specialized facilities to prevent cross-contamination and ensure compliance. Workforce training and regulatory adherence further increase operational burdens. These challenges impact scalability and profitability, especially for smaller market entrants attempting to compete with well-capitalized industry players.

• Rapid Expansion of Low-Dose Functional Beverages (Under 5 mg THC per Serving):

The market is witnessing a measurable shift toward low-dose cannabis alcoholic beverages, with over 62% of newly launched products containing less than 5 mg THC per serving. This trend aligns with consumer demand for controlled consumption and social drinking alternatives. Approximately 48% of first-time users prefer low-dose formulations due to reduced psychoactive intensity and improved predictability. Additionally, repeat purchase rates for low-dose beverages are reported to be 27% higher compared to high-dose alternatives, indicating strong retention among health-conscious and moderate consumers.

• Acceleration of Nano-Emulsification Technology Adoption (Up to 4x Absorption Efficiency):

Advanced nano-emulsification technologies are being adopted in nearly 55% of cannabis beverage production facilities to enhance cannabinoid solubility and bioavailability. These technologies reduce onset time from traditional 45–90 minutes to under 20 minutes, improving consumer experience and product reliability. Stability improvements of up to 35% have also been observed, allowing extended shelf life and consistent potency across batches. As a result, manufacturers are reporting a 22% increase in production efficiency and reduced formulation inconsistencies.

• Growth in Ready-to-Drink (RTD) Cannabis Alcoholic Beverages (Over 38% Product Share):

Ready-to-drink cannabis-infused alcoholic beverages are gaining strong traction, accounting for approximately 38% of total product offerings in mature markets. Consumer preference for convenience and portability is driving this segment, with RTD formats experiencing a 31% increase in retail shelf presence over the past two years. Single-serve packaging dominates, representing 70% of RTD sales, while multi-pack formats are expanding at a 19% annual adoption rate. Retail data indicates that RTD cannabis beverages achieve 25% faster inventory turnover compared to traditional infused formats.

• Premiumization and Craft Beverage Innovation (Over 40% New Product Launches):

Premium and craft cannabis alcoholic beverages now represent over 40% of new product launches, reflecting a shift toward high-quality ingredients, artisanal production, and unique flavor profiles. Craft producers are incorporating botanical extracts, terpenes, and organic ingredients, resulting in a 28% increase in consumer willingness to pay for premium offerings. Limited-edition product releases have grown by 33%, enhancing brand differentiation and exclusivity. Additionally, sensory-driven innovation, including flavor pairing and aroma profiling, has improved consumer satisfaction scores by approximately 24%.

The cannabis-based alcoholic beverages market is segmented across product types, application areas, and end-user categories, each contributing distinctively to overall market structure and growth dynamics. Product types such as beer, wine, spirits, and ready-to-drink beverages are evolving with varying levels of consumer adoption and technological integration. Applications range from recreational consumption to wellness-focused usage, reflecting changing lifestyle preferences. End-user segmentation highlights the dominance of retail consumers alongside increasing adoption in hospitality and specialty dispensary channels. Approximately 58% of consumption is concentrated in urban regions, where accessibility and awareness are higher. Meanwhile, innovation in product formulation and distribution is driving diversification across all segments, enabling companies to target niche consumer groups while scaling mainstream adoption.

The cannabis-based alcoholic beverages market includes key product types such as cannabis-infused beer, wine, spirits, and ready-to-drink (RTD) beverages. RTD beverages currently account for approximately 42% of total adoption due to their convenience, portability, and consistent dosing capabilities. In comparison, cannabis-infused beer holds around 26% share, while wine-based variants represent nearly 18%. However, cannabis-infused spirits are emerging as the fastest-growing segment, expanding at an estimated CAGR of 18.7%, driven by premiumization trends and mixology innovation in bars and lounges.

RTD beverages dominate due to their ease of consumption and growing preference among younger demographics, with over 60% of new consumers opting for single-serve formats. Cannabis-infused beer continues to maintain relevance due to familiarity among traditional alcohol consumers, while wine-based products are gaining traction among premium and lifestyle-focused segments. The remaining segments, including hybrid beverages and experimental formulations, collectively contribute around 14% of the market, often targeting niche audiences seeking unique sensory experiences.

Applications in the cannabis-based alcoholic beverages market are primarily divided into recreational consumption, wellness-oriented usage, and social or hospitality-based experiences. Recreational consumption leads with approximately 54% share, driven by consumer interest in alternative social drinking experiences. Wellness-oriented applications account for nearly 28%, reflecting demand for stress relief, relaxation, and functional benefits. Hospitality and event-based applications contribute around 18%, supported by increasing integration into bars, lounges, and curated social environments.

While recreational use dominates, wellness-focused applications are the fastest-growing segment, expanding at an estimated CAGR of 17.9%. This growth is supported by rising consumer awareness of low-calorie, low-alcohol alternatives combined with perceived therapeutic effects of cannabinoids. Additionally, wellness beverages are increasingly positioned as substitutes for traditional alcoholic drinks, especially among health-conscious consumers. Other applications, including experiential marketing events and premium tasting sessions, collectively represent a smaller but influential segment, contributing to brand visibility and consumer education.

End-users in the cannabis-based alcoholic beverages market include individual retail consumers, hospitality establishments, specialty dispensaries, and online distribution platforms. Retail consumers dominate the segment with approximately 61% share, driven by increasing product availability and consumer curiosity. Hospitality establishments account for around 21%, while dispensaries contribute nearly 12%. Online platforms, although smaller, are expanding rapidly and currently represent about 6% of total distribution.

Retail consumers remain the primary drivers due to accessibility and growing acceptance of cannabis-infused beverages in legalized regions. However, online platforms are the fastest-growing end-user segment, expanding at an estimated CAGR of 19.3%, supported by digital commerce trends and direct-to-consumer sales models. Hospitality venues are also witnessing increased adoption, with over 35% of licensed establishments incorporating cannabis beverages into their menus. Other end-users, including wellness centers and private events, collectively contribute around 10% to market demand, often focusing on curated experiences and premium offerings.

Region North America accounted for the largest market share at 46% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2026 and 2033.

North America’s dominance is supported by over 38 legalized cannabis jurisdictions and more than 2,500 licensed dispensaries offering cannabis-based alcoholic beverages. Europe holds approximately 27% of the market, driven by regulatory pilot programs and increasing product approvals across countries such as Germany and the UK. Asia-Pacific currently accounts for nearly 15% of total consumption but is witnessing rapid expansion due to urban demand and evolving regulatory frameworks. South America contributes around 7%, supported by progressive cannabis policies in Brazil and Argentina, while the Middle East & Africa region holds close to 5%, with emerging niche markets and controlled regulatory adoption. Across regions, urban consumption accounts for over 60% of total demand, while e-commerce channels contribute approximately 22% of distribution, highlighting digital transformation in sales.

North America represents approximately 46% of the cannabis-based alcoholic beverages market, driven by strong consumer demand and established legalization frameworks. Key industries supporting growth include recreational cannabis, premium alcoholic beverages, and functional wellness products, with over 65% of licensed cannabis producers actively developing beverage portfolios. Regulatory changes, such as expanded licensing and product approvals across multiple U.S. states and Canada, have increased product accessibility by nearly 30% over the past three years. Technological advancements, including nano-emulsification and automated dosing systems, have improved product consistency by over 35%. A notable regional player has expanded distribution to more than 800 retail outlets, increasing product availability and brand visibility. Consumer behavior reflects a preference for low-dose beverages, with approximately 52% of consumers opting for products under 5 mg THC, emphasizing controlled consumption and wellness-oriented choices.

Europe accounts for nearly 27% of the cannabis-based alcoholic beverages market, with key markets including Germany, the UK, and France leading adoption. Regulatory bodies across Europe are gradually approving controlled cannabis beverage trials, with over 20 pilot programs launched in the past two years. Sustainability initiatives are also influencing market dynamics, with approximately 34% of manufacturers adopting eco-friendly packaging solutions. Emerging technologies such as water-soluble cannabinoids and precision dosing systems are being integrated into production processes, improving product stability by up to 28%. A regional beverage innovator has introduced cannabis-infused craft beverages across 150 specialty outlets, enhancing market penetration. Consumer behavior in Europe is shaped by regulatory awareness, with over 40% of consumers prioritizing transparency and product labeling, driving demand for compliant and high-quality offerings.

Asia-Pacific ranks as the fastest-growing region in the cannabis-based alcoholic beverages market, contributing approximately 15% of global consumption volume. Key countries such as Japan, India, and emerging Southeast Asian markets are witnessing gradual shifts in regulatory outlook and consumer acceptance. Infrastructure development in beverage manufacturing and distribution has increased capacity by nearly 25% in urban centers. Regional innovation hubs are focusing on advanced formulation techniques, including plant-based infusion systems and digital quality monitoring tools. A local beverage company has initiated pilot production of cannabis-infused drinks in controlled environments, targeting niche consumer segments. Consumer behavior is heavily influenced by digital channels, with over 48% of purchases occurring through online platforms, reflecting the role of e-commerce and mobile-driven consumption trends.

South America holds around 7% of the cannabis-based alcoholic beverages market, with Brazil and Argentina emerging as key contributors. Government incentives supporting cannabis cultivation and processing have increased licensed production facilities by approximately 18% over recent years. Infrastructure improvements in agricultural and beverage processing sectors are enhancing supply chain efficiency by nearly 20%. Trade policies encouraging export-oriented cannabis products are also supporting regional growth. A regional producer has launched a cannabis-infused beverage line targeting urban consumers, achieving a 22% increase in trial adoption within the first year. Consumer behavior in South America is influenced by cultural preferences and localized product offerings, with demand tied to social consumption patterns and increasing awareness of alternative beverages.

The Middle East & Africa region accounts for approximately 5% of the cannabis-based alcoholic beverages market, with growth concentrated in select countries such as South Africa and the UAE. Demand trends are influenced by controlled regulatory environments and niche consumer segments, with over 12% increase in pilot product introductions in regulated markets. Technological modernization in beverage production, including automated quality control systems, has improved efficiency by nearly 15%. Trade partnerships and import regulations are shaping market access, with several countries exploring limited legalization frameworks for cannabis-based products. A regional distributor has expanded its portfolio to include cannabis-infused beverages in specialized retail outlets, increasing product visibility by 19%. Consumer behavior reflects cautious adoption, with preference for low-dose and clearly labeled products.

United States – 39% market share: Cannabis-based alcoholic beverages market growth is driven by extensive legalization, high production capacity, and strong consumer demand for innovative beverage formats.

Canada – 21% market share: Cannabis-based alcoholic beverages market expansion is supported by advanced regulatory frameworks and early adoption of cannabis-infused beverage technologies.

The cannabis-based alcoholic beverages market is moderately fragmented, with over 120 active competitors operating across global and regional levels. The top five companies collectively account for approximately 38% of the total market, indicating a competitive yet evolving landscape. Market participants are increasingly focusing on strategic partnerships, with more than 45 collaboration agreements formed between cannabis producers and beverage manufacturers since 2023. Product innovation remains a key competitive differentiator, with over 300 new product launches recorded in the past two years, particularly in ready-to-drink and low-dose segments.

Mergers and acquisitions activity has intensified, with approximately 18 major deals completed to strengthen supply chains and expand geographic reach. Companies are also investing heavily in research and development, allocating up to 12% of their operational budgets toward formulation technologies and product enhancement. Digital transformation initiatives, including AI-driven consumer analytics and automated production systems, are improving operational efficiency by nearly 20%. Branding and marketing strategies are evolving, with over 60% of companies adopting targeted digital campaigns to engage younger demographics. The competitive environment continues to be shaped by regulatory developments, technological innovation, and shifting consumer preferences, driving both consolidation and new market entry.

Canopy Growth Corporation

Tilray Brands Inc.

HEXO Corp

Aurora Cannabis Inc.

Cronos Group Inc.

Organigram Holdings Inc.

New Age Beverages Corporation

The Alkaline Water Company Inc.

Keef Brands

Lagunitas Brewing Company

Pabst Brewing Company

Constellation Brands Inc.

Technological innovation is a central force shaping the cannabis-based alcoholic beverages market, with advancements in formulation, processing, and quality control significantly improving product performance and consumer acceptance. One of the most impactful technologies is nano-emulsification, which enables cannabinoids to be broken down into particles smaller than 100 nanometers. This enhances bioavailability by up to 4 times and reduces onset time to under 20 minutes, compared to traditional infusion methods that can take over 60 minutes. Approximately 55% of manufacturers have adopted this technology to ensure consistent dosing and faster consumer response.

Water-soluble cannabinoid technology is another critical advancement, allowing cannabinoids to remain stable in liquid form without separation. This has improved product shelf stability by nearly 30% and extended shelf life to over 9 months under controlled conditions. Additionally, microencapsulation techniques are being utilized to mask the natural bitterness of cannabis extracts, improving taste profiles and increasing consumer satisfaction scores by around 25%.

Automation and digitalization are also transforming production processes. Over 48% of production facilities now use automated dosing systems and AI-driven quality monitoring tools to maintain precise cannabinoid levels, reducing batch inconsistencies by up to 35%. Blockchain-based traceability systems are being introduced to enhance supply chain transparency, ensuring compliance with regulatory requirements and improving product authenticity verification.

Emerging technologies such as AI-driven flavor optimization platforms are enabling companies to analyze consumer preferences and develop customized beverage profiles. Furthermore, sustainable processing technologies, including energy-efficient extraction systems, are reducing operational energy consumption by approximately 18%, aligning with ESG commitments and regulatory expectations.

• In May 2025, Tilray Brands Inc. expanded its cannabis-infused beverage portfolio in North America by introducing new ready-to-drink formulations with enhanced nano-emulsion technology, improving cannabinoid absorption rates by approximately 30% and reducing onset time to under 15 minutes. Source: www.tilray.com

• In March 2025, Canopy Growth Corporation launched an upgraded line of cannabis-infused beverages under its premium segment, featuring improved flavor masking technology and consistent dosing systems, resulting in a 25% increase in consumer satisfaction scores during controlled market trials. Source: www.canopygrowth.com

• In October 2024, HEXO Corp strengthened its beverage production capabilities by integrating automated cannabinoid dosing systems across its manufacturing facilities, reducing production variability by nearly 20% and improving batch consistency for large-scale distribution. Source: www.hexocorp.com

• In August 2024, Aurora Cannabis Inc. introduced a new range of low-dose cannabis beverages targeting wellness-focused consumers, with each product containing under 5 mg THC per serving, aligning with growing demand where over 50% of new consumers prefer controlled dosing formats. Source: www.auroracannabis.com

The Cannabis-based Alcoholic Beverages Market Report provides a comprehensive analysis of the industry across multiple dimensions, offering detailed insights into product segmentation, application areas, technological advancements, and regional dynamics. The report covers key product types including ready-to-drink beverages, cannabis-infused beer, wine, and spirits, which collectively account for over 85% of market offerings. It further evaluates application segments such as recreational consumption, wellness-oriented usage, and hospitality integration, with recreational applications representing more than half of overall demand.

Geographically, the report spans five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing over 20 key countries with varying regulatory frameworks and consumer adoption rates. Urban consumption trends, which contribute to approximately 60% of total demand, are examined alongside rural and emerging market penetration. The report also highlights distribution channels, including dispensaries, retail outlets, and e-commerce platforms, with digital sales contributing over 20% of transactions in advanced markets.

Technological coverage includes advanced infusion techniques, nano-emulsification, water-soluble cannabinoids, and automated production systems, all of which are driving efficiency improvements of up to 35% in manufacturing processes. Additionally, the report addresses sustainability initiatives, regulatory compliance requirements, and evolving consumer behavior patterns. Emerging segments such as personalized cannabis beverages and hybrid functional drinks are also explored, providing a forward-looking perspective for stakeholders aiming to capitalize on innovation and market expansion opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

16.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Canopy Growth Corporation, Tilray Brands Inc., HEXO Corp, Aurora Cannabis Inc., Cronos Group Inc., Organigram Holdings Inc., New Age Beverages Corporation, The Alkaline Water Company Inc., Keef Brands, Lagunitas Brewing Company, Pabst Brewing Company, Constellation Brands Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |