Reports

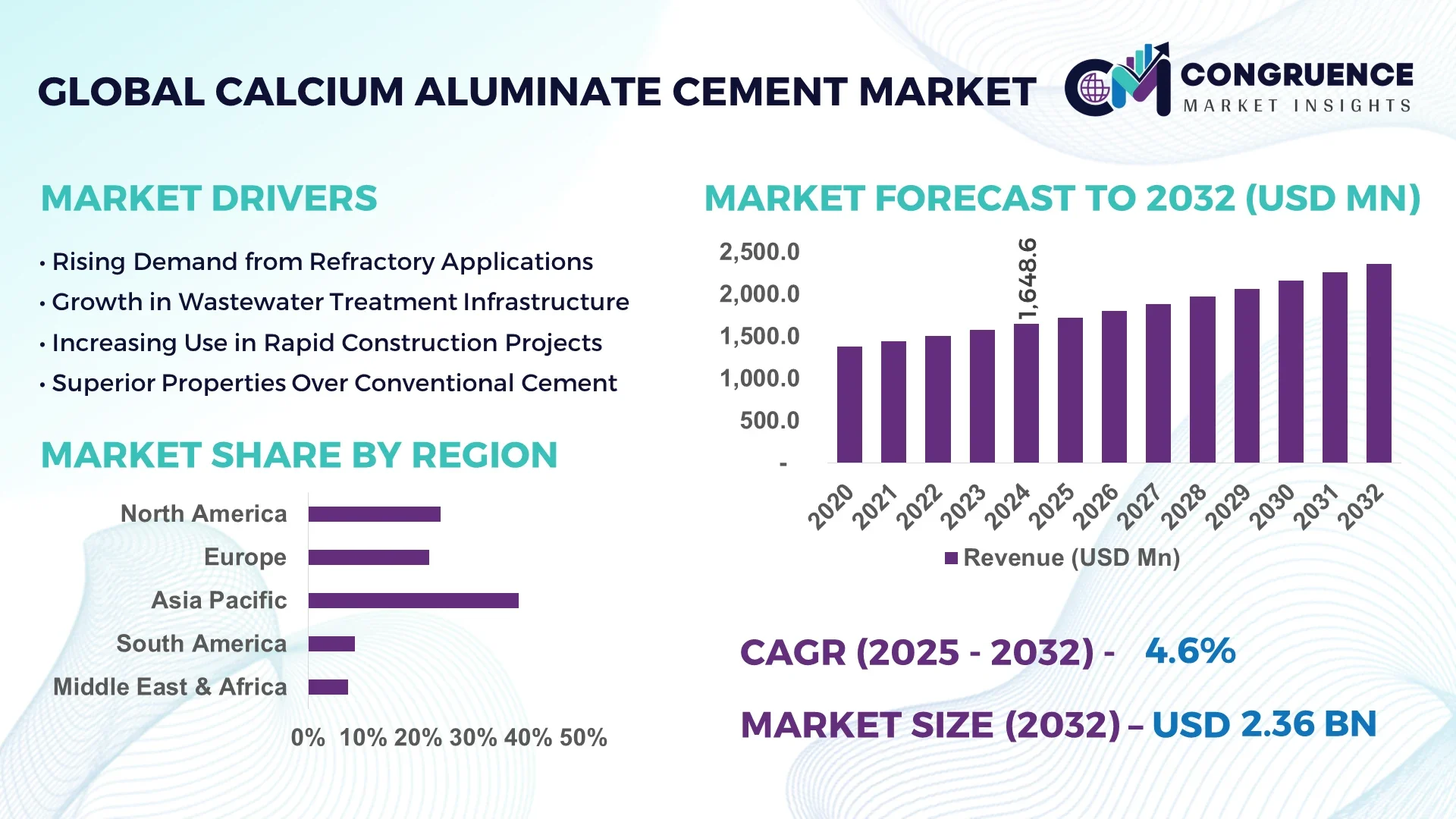

The Global Calcium Aluminate Cement Market was valued at USD 1,648.63 Million in 2024 and is anticipated to reach a value of USD 2,362.5 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032.

Calcium aluminate cement, known for its high resistance to chemical corrosion and elevated temperature durability, is gaining widespread acceptance across construction, wastewater, and refractory industries. Its accelerated setting time and enhanced mechanical strength make it suitable for manufacturing structural concrete, castables, and corrosion-resistant coatings. Growing infrastructure development projects, especially in emerging nations, are further fueling demand for calcium aluminate cement. The market is also witnessing innovation in cement formulations to improve sustainability, performance, and versatility across end-use sectors, leading to a notable shift in the global cement industry landscape.

Artificial Intelligence (AI) is playing a transformative role in the Calcium Aluminate Cement Market, reshaping production processes, quality control, and logistics management. AI-enabled predictive maintenance systems are reducing equipment downtimes by analyzing sensor data in real-time, thereby increasing plant productivity. Smart manufacturing facilities are utilizing machine learning algorithms to optimize the blending process of raw materials, ensuring consistent cement quality. Furthermore, AI-driven robotic systems are automating packaging and material handling, reducing labor costs while improving safety standards. AI-based demand forecasting tools are helping manufacturers align their inventory with fluctuating customer demands, leading to minimized waste and optimized supply chains. Cement producers are integrating AI into kiln operation management, enabling precise thermal control that results in lower energy consumption and reduced emissions. These technologies are not only enhancing operational efficiency but also contributing to sustainable manufacturing practices in the calcium aluminate cement industry.

"In 2024, RHI Magnesita implemented AI-powered optical sensors at its French facility to detect real-time mineral composition in calcium aluminate cement production, boosting quality assurance and reducing wastage significantly."

Infrastructure spending in developing nations like India and Brazil has surged, leading to heightened demand for high-performance cement. The requirement for quick-setting and durable construction materials for bridges, highways, and urban housing is driving the adoption of calcium aluminate cement. For instance, India’s National Infrastructure Pipeline (NIP) alone accounted for over 9,000 infrastructure projects in 2024. This increased investment is pushing forward the market expansion for cement products that can withstand harsh environmental and chemical conditions, such as those found in coastal or industrial regions.

Bauxite, a primary raw material for calcium aluminate cement, is witnessing global supply fluctuations due to export restrictions and environmental regulations. In 2024, China, one of the leading bauxite suppliers, imposed stringent export norms, impacting global supply chains. Additionally, the high energy requirements associated with sintering and clinker formation contribute to increased operational costs. Smaller players in the market are struggling to maintain price competitiveness, hampering market penetration in cost-sensitive regions.

The increasing need for effective sewage and wastewater treatment infrastructure, particularly in urban and industrial zones, is opening new avenues for calcium aluminate cement applications. Its high resistance to biogenic corrosion makes it ideal for sewer linings and treatment plant structures. In 2024, over 45% of global wastewater treatment projects in Asia Pacific incorporated calcium aluminate cement products due to their superior performance in acidic and high-moisture environments. This trend is expected to strengthen, driven by environmental regulations and sustainability goals.

One of the key challenges in the calcium aluminate cement market is the lack of global standardization. Manufacturers often have to tailor formulations based on regional climate, application requirements, and local regulations, increasing production complexity. For example, cement compositions used in Middle Eastern refractory applications differ significantly from those in European construction environments. This customization increases lead times, complicates inventory management, and requires advanced technical support, which many small manufacturers struggle to provide consistently.

The Calcium Aluminate Cement Market is witnessing significant trends centered on sustainability, innovation, and digital integration. Eco-efficient cement variants with lower carbon footprints are gaining traction, driven by the global push for green construction materials. In 2024, more than 30% of newly developed calcium aluminate cement types were formulated with recycled industrial by-products to reduce environmental impact. The industry is also embracing modular and precast construction technologies, where fast-setting and high-strength cements like calcium aluminate are in high demand. Additionally, manufacturers are integrating digital twins and AI-powered process monitoring tools for real-time quality control and predictive analytics. Refractory applications are seeing robust growth, especially in steel and non-ferrous metal sectors, due to the need for thermal shock-resistant linings. The Asia Pacific region continues to dominate demand, fueled by rapid industrial expansion and urbanization. Meanwhile, strategic collaborations and mergers among key players aim to enhance production capacity and distribution efficiency across high-growth markets.

The Calcium Aluminate Cement Market is segmented into four major types: Pre-Mixed, Low Purity, Medium Purity, and High Purity. Each type serves distinct use cases across various industries, depending on required mechanical strength, setting time, and corrosion resistance. On the application side, the cement finds usage in refractories, construction, sewage treatment, and other specialized areas due to its high thermal resistance and fast-setting properties. From an end-user perspective, the key sectors driving demand include building & construction, metallurgy, wastewater treatment, and others such as chemical processing and marine infrastructure. Below is a detailed analysis of each segment:

Pre-Mixed: Pre-mixed calcium aluminate cement is gaining traction due to its ease of use and consistent quality. This type eliminates on-site blending, thereby reducing labor costs and minimizing errors in formulation. It is primarily used in small- to mid-scale construction and repair projects where time and accuracy are critical. In 2024, over 28% of cement used in ready-mix repair mortars in North America was pre-mixed CAC. This segment is especially popular in urban redevelopment projects and modular construction setups, where accelerated timelines are prioritized.

Low Purity: Low purity calcium aluminate cement contains less than 40% alumina content and is mainly used in low-demand construction applications. It is cost-effective and commonly employed for non-critical structural repairs, low-end refractory castables, and subflooring. In 2024, this segment contributed to over 20% of total CAC volume consumption in South America, driven by its affordability. Although it lacks the mechanical strength of higher-grade variants, it remains a preferred choice for budget-sensitive infrastructure development.

Medium Purity: Medium purity variants, typically comprising 40–70% alumina, offer a balanced mix of performance and affordability. These are extensively used in precast shapes and linings that require moderate thermal and chemical resistance. In industrial furnaces, medium purity CAC supports temperatures up to 1,400°C. By 2024, over 35% of refractory bricks used in Asia Pacific steel plants were manufactured using medium purity CAC, showcasing its relevance in metallurgy and manufacturing sectors.

High Purity: High purity calcium aluminate cement, with alumina content exceeding 70%, is utilized in critical applications that demand superior chemical resistance, low porosity, and high strength. This type is crucial for high-temperature refractories, specialty concretes, and sewerage systems exposed to aggressive environments. In 2024, high purity CAC held a dominant share in European foundries and incinerator plants, where thermal shock resistance and durability are mandatory. Its use is also expanding in green building materials due to better lifecycle performance.

Refractories: Refractories remain the leading application segment for calcium aluminate cement due to its ability to withstand extreme temperatures and thermal cycling. In 2024, over 45% of total CAC demand came from refractory production, particularly in the steel, glass, and non-ferrous metal sectors. The cement is used in castables, monolithics, and bricks, offering superior bonding and resistance to slag and alkalis. Its high-performance capabilities in rotary kilns, ladles, and electric arc furnaces continue to drive growth in this segment globally.

Construction: In the construction sector, calcium aluminate cement is highly valued for its fast-setting nature and early strength development. It is used in structural repair mortars, self-leveling flooring, and quick-set concretes. In 2024, rapid repair projects across urban transit systems in Europe used CAC-based products to minimize downtime. The material's ability to perform in high-moisture and chemically aggressive environments makes it ideal for underground construction, tunnel linings, and marine infrastructure, significantly expanding its application scope.

Sewage Treatment: Sewage and wastewater treatment facilities utilize CAC for its outstanding resistance to biogenic corrosion and sulfate attack. In 2024, over 32% of new wastewater plants built in Asia used CAC for lining tanks, pipes, and sumps. Its low permeability and excellent bonding characteristics make it ideal for long-term performance in aggressive chemical environments. Municipalities and private contractors are adopting CAC-based linings to reduce maintenance frequency and improve the durability of infrastructure.

Others: Other applications of calcium aluminate cement include its use in industrial flooring, chemical processing plants, and marine projects. It is especially valued in areas exposed to high abrasion or aggressive chemicals. In 2024, the Middle East saw a rise in CAC usage for desalination plant construction and offshore oil platform components. These specialized uses are opening up new opportunities in niche markets that prioritize material longevity and environmental resilience.

Building & Construction: Building and construction represent the largest end-user segment for calcium aluminate cement. In 2024, more than 40% of all CAC consumption globally was attributed to construction-related activities. Projects focused on bridges, tunnels, airports, and high-rise buildings rely on CAC for rapid deployment and structural integrity. The cement’s early strength development and adaptability to various climate conditions make it indispensable in this segment, particularly for emergency repairs and high-speed project rollouts.

Metallurgy: The metallurgy industry heavily depends on high and medium purity calcium aluminate cement for manufacturing refractory linings that endure extreme heat and chemical exposure. In 2024, steel plants across China and India upgraded over 2 million metric tons of refractory output using CAC-based formulations. These linings are vital in furnaces, ladles, and tundishes where thermal resistance and structural stability are essential. The growing global demand for steel and non-ferrous metals continues to boost CAC usage in this segment.

Wastewater Treatment: Municipal and industrial wastewater treatment facilities are emerging as critical end-users of CAC, thanks to its durability in acidic and corrosive environments. In 2024, over 25% of CAC used in Europe was allocated to wastewater projects. Applications include pipe linings, tank construction, and protective coatings. As environmental regulations tighten and the need for sustainable infrastructure grows, this segment is expected to expand rapidly, particularly in urban centers facing sewage overloads.

Others: Other end-users include the chemical processing and marine infrastructure sectors, which require high-performance materials for structural protection against corrosion and mechanical wear. In 2024, over 10% of CAC demand came from offshore engineering projects, especially in South East Asia and the Gulf. Applications span tank linings, jetties, and submerged installations. The cement’s resistance to chloride penetration and low water absorption make it a preferred choice in these highly demanding environments.

Asia Pacific accounted for the largest market share at 38.2% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2025 and 2032.

The global demand for calcium aluminate cement is being driven by rapid industrialization, expanding urban infrastructure, and rising investments in wastewater management across these regions. Asia Pacific's dominance stems from its extensive usage in refractory materials for steel and metal industries. Meanwhile, the Middle East & Africa region is witnessing a boom in construction and desalination plant development, pushing demand for high-performance cement solutions.

Sustainable Infrastructure Projects Driving CAC Adoption

In North America, the calcium aluminate cement market is experiencing steady growth due to increased focus on sustainable infrastructure and maintenance of aging public utilities. The United States led the regional market with over 62% share in 2024, driven by projects targeting rapid concrete repairs, tunnel waterproofing, and wastewater treatment. In Canada, the use of CAC in precast products for cold climates has seen a 12% year-on-year increase. Government investments in green building certifications have further elevated demand for eco-efficient materials like calcium aluminate cement that offer low permeability and chemical durability.

Rising Use of CAC in Wastewater and Tunnel Construction

Europe's calcium aluminate cement market is supported by its mature industrial base and stringent environmental standards. Germany, holding a 28% regional market share in 2024, saw extensive usage of CAC in tunnel reinforcements and sewage infrastructure renovations. The UK and France have increased demand due to ongoing metro rail expansions and chemical-resistant flooring in processing plants. In 2024, over 18% of all sewer rehabilitation work in Europe involved CAC-based products due to their resistance to biogenic corrosion. Additionally, refurbishment of aging nuclear and energy facilities is contributing to sustained usage across Central and Eastern Europe.

Steel Industry and Urbanization Fueling CAC Demand

Asia-Pacific remains the powerhouse of calcium aluminate cement demand, led by China, India, and Japan. China alone accounted for 45% of the region’s CAC consumption in 2024, thanks to its vast steel production and refractory requirements. India followed with significant adoption in water treatment facilities and low-cost housing construction. The region also saw a 15% rise in CAC use in marine infrastructure projects across Southeast Asia. Rapid urbanization, growing metallurgical output, and government-backed housing and sanitation missions continue to drive high-volume usage of CAC products in the Asia-Pacific region.

Desalination and Mega Projects Boosting Demand

The Middle East & Africa region is emerging as a fast-growing market for calcium aluminate cement. In 2024, the UAE and Saudi Arabia together accounted for over 58% of the region's demand, driven by ongoing megaprojects like NEOM and various smart city initiatives. CAC is increasingly used in desalination plants and marine installations due to its resistance to saltwater corrosion. In South Africa and Egypt, growth is spurred by municipal investments in sewage infrastructure and cement-based lining technologies. The region’s strategic focus on long-life infrastructure and harsh environment resilience is making CAC a material of choice across sectors.

The global calcium aluminate cement (CAC) market is characterized by a competitive landscape with several key players striving to enhance their market presence. Companies are focusing on strategic initiatives such as mergers and acquisitions, product innovations, and expansion into emerging markets to gain a competitive edge. For instance, in 2024, Calucem invested in upgrading its manufacturing facility in Croatia to increase efficiency and environmental sustainability. Similarly, Imerys Aluminates expanded its production capacity in India to meet the growing demand in the Asia-Pacific region. These strategic moves are aimed at catering to the increasing demand for CAC in various applications, including refractories, construction, and sewage treatment. The market is also witnessing collaborations between companies and research institutions to develop innovative CAC formulations that meet specific performance requirements. With the rising demand for high-performance and sustainable construction materials, the competition among CAC manufacturers is expected to intensify in the coming years.

Calucem

Almatis GmbH

Cimsa Cemento

Denka Company Limited

Gorka Cement

Imerys Aluminates

Union Cement

Zhengzhou Dengfeng Smelting Materials Co. Ltd.

Henan Suntek International Co. Ltd.

ABC Supply Co. Inc.

Technological advancements are playing a pivotal role in shaping the calcium aluminate cement market. Manufacturers are increasingly adopting sustainable production techniques to reduce carbon emissions and energy consumption. For example, the implementation of dry processing methods has improved production efficiency and minimized environmental impact. Additionally, companies are investing in research and development to create CAC formulations with enhanced properties such as higher early strength, improved chemical resistance, and better workability. The integration of digital technologies, including AI and IoT, in manufacturing processes has enabled real-time monitoring and quality control, ensuring consistent product quality. Furthermore, the development of pre-blended dry mixes and monolithic refractory castables has expanded the application scope of CAC in various industries. These technological innovations are not only improving the performance characteristics of CAC but also contributing to cost savings and sustainability goals. As the demand for high-performance and eco-friendly construction materials continues to rise, technological advancements will remain a key driver in the growth of the calcium aluminate cement market.

In April 2022, Calucem announced a $35 million investment to establish a new manufacturing facility in New Orleans, USA, aiming to strengthen its position in the North American market.

In October 2022, Imerys inaugurated a calcium aluminate binder plant in Atchutapuram, India, with an initial capacity of 30,000 tons per year, planning to expand to 50,000 tons by 2030 to meet the growing demand in the region.

In June 2023, Denka Company Limited introduced a new line of high-purity calcium aluminate cement products designed for advanced refractory applications, enhancing performance in extreme temperature conditions.

In August 2023, Gorka Cement launched an innovative CAC formulation with improved setting time and strength development, targeting the construction and wastewater treatment sectors.

In December 2023, Almatis GmbH expanded its research collaboration with leading universities to develop next-generation CAC products with enhanced durability and environmental sustainability.

The calcium aluminate cement market report provides a comprehensive analysis of the current market trends, growth drivers, challenges, and opportunities. It covers various segments based on type, application, end-user, and geography, offering detailed insights into each category. The report examines the competitive landscape, profiling key players and their strategic initiatives to gain a competitive edge. It also delves into technological advancements shaping the market, highlighting innovations in production processes and product formulations. Furthermore, the report includes recent developments and investments by major companies, shedding light on the dynamic nature of the market. By providing in-depth information and analysis, the report serves as a valuable resource for stakeholders, investors, and industry participants seeking to understand the calcium aluminate cement market and make informed decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,648.63 Million |

|

Market Revenue in 2032 |

USD 2,362.5 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Calucem, Almatis GmbH, Cimsa Cemento, Denka Company Limited, Gorka Cement, Imerys Aluminates, Union Cement, Zhengzhou Dengfeng Smelting Materials Co. Ltd., Henan Suntek International Co. Ltd., ABC Supply Co. Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |