Reports

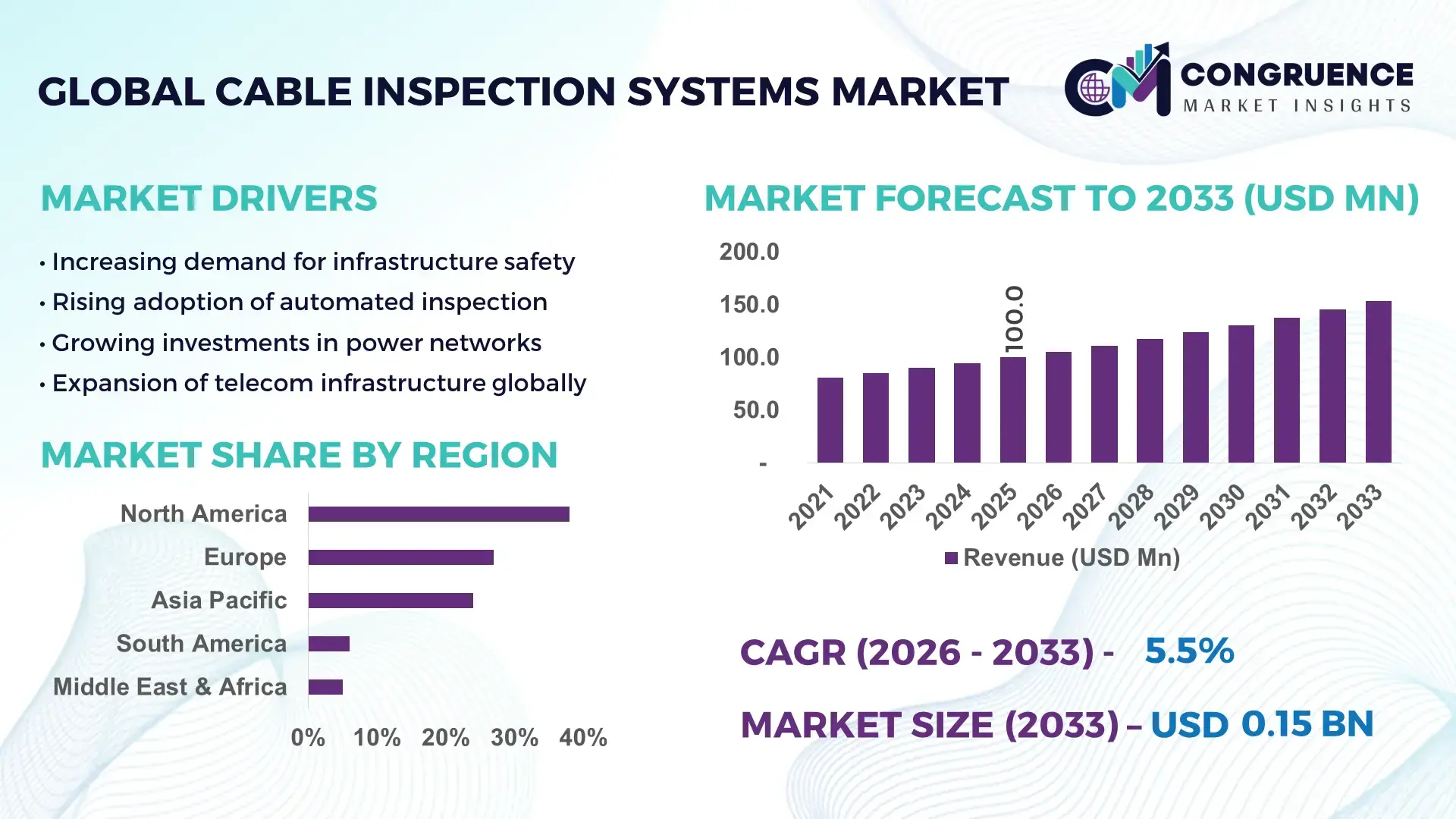

The Global Cable Inspection Systems Market was valued at USD 100.0 Million in 2025 and is anticipated to reach a value of USD 153.5 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing demand for predictive maintenance and real-time monitoring across critical infrastructure networks.

The United States dominates the Cable Inspection Systems Market with strong technological integration and large-scale infrastructure investments. The country operates over 7.3 million kilometers of power transmission and distribution lines, creating sustained demand for inspection solutions. Approximately 62% of utilities in the U.S. have adopted automated inspection technologies, including robotic and AI-based systems for cable diagnostics. Investments exceeding USD 25 billion annually in grid modernization further support deployment of advanced cable monitoring solutions. Key applications include energy utilities, telecommunications, and offshore oil & gas, where inspection frequency has increased by over 40% due to regulatory compliance and asset longevity requirements.

Market Size & Growth: USD 100.0 Million in 2025, projected to reach USD 153.5 Million by 2033, growing at 5.5% CAGR, driven by rising need for predictive maintenance.

Top Growth Drivers: Automation adoption (48%), inspection efficiency improvement (35%), infrastructure expansion (42%).

Short-Term Forecast: By 2028, automated inspection systems expected to reduce maintenance costs by 28%.

Emerging Technologies: AI-based defect detection, robotic crawlers, drone-enabled inspection systems.

Regional Leaders: North America (USD 52 Million by 2033) driven by grid modernization; Europe (USD 41 Million) driven by regulatory compliance; Asia-Pacific (USD 38 Million) driven by infrastructure expansion.

Consumer/End-User Trends: Utilities and telecom sectors account for over 65% usage with increasing preference for real-time diagnostics.

Pilot or Case Example: In 2024, a utility pilot reduced cable downtime by 32% using AI-based inspection systems.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 key global players with strong regional presence.

Regulatory & ESG Impact: Over 55% of companies adopting inspection systems to meet ESG and safety compliance standards.

Investment & Funding Patterns: More than USD 1.2 Billion invested globally in grid inspection and monitoring technologies in recent years.

Innovation & Future Outlook: Integration of IoT-enabled sensors and cloud analytics expected to enhance fault detection accuracy by over 45%.

Cable Inspection Systems Market is influenced by energy (42%), telecommunications (28%), and oil & gas (18%) sectors. Technological advancements such as AI-enabled diagnostics and robotic inspection tools are improving defect detection accuracy by over 40%. Regulatory frameworks focusing on grid reliability and safety compliance are accelerating adoption. Asia-Pacific shows rising consumption driven by infrastructure expansion, while Europe emphasizes sustainability. Future trends indicate increasing integration of predictive analytics and remote monitoring systems.

The Cable Inspection Systems Market holds significant strategic relevance as global infrastructure networks expand and age simultaneously, increasing the need for efficient monitoring systems. Advanced inspection technologies such as AI-driven visual analytics deliver 45% improvement in fault detection accuracy compared to traditional manual inspection methods. Utilities, telecommunications providers, and oil & gas companies are increasingly integrating these systems into their asset management frameworks to minimize downtime and operational risks.

North America dominates in volume due to extensive grid infrastructure, while Asia-Pacific leads in adoption with over 58% of utilities implementing digital inspection solutions. The shift toward automation is further supported by growing investments in smart grid infrastructure and industrial IoT deployment. By 2028, AI-powered inspection platforms are expected to reduce operational downtime by 30% and improve maintenance scheduling efficiency by 35%.

From a compliance perspective, firms are committing to ESG goals such as reducing cable failure-related outages by 25% by 2030. Governments are enforcing stricter inspection regulations, particularly in energy and offshore industries, leading to higher adoption of automated systems.

In 2025, a U.S.-based utility achieved a 33% reduction in inspection time through deployment of drone-based cable monitoring systems integrated with AI analytics. Such measurable outcomes highlight the transformative potential of advanced technologies.

Looking ahead, the Cable Inspection Systems Market is poised to become a critical pillar of infrastructure resilience, regulatory compliance, and sustainable industrial growth, supporting long-term operational efficiency across multiple sectors.

The Cable Inspection Systems Market is shaped by increasing infrastructure complexity, aging grid networks, and rising demand for operational efficiency across industries. The growing deployment of smart grids and fiber-optic networks has increased inspection frequency by over 35% globally. Industries such as energy, telecommunications, and oil & gas are adopting automated inspection technologies to reduce manual errors and improve asset lifespan. Digital transformation initiatives, including integration of AI, IoT, and robotics, are enabling real-time monitoring and predictive maintenance. Additionally, regulatory mandates for safety and reliability are pushing organizations to adopt advanced inspection systems. The market is also influenced by increasing offshore energy projects and expansion of renewable energy infrastructure, which require consistent cable monitoring solutions to ensure uninterrupted operations.

Rapid expansion of global infrastructure, particularly in energy and telecommunications, is significantly driving demand for cable inspection systems. Over 60% of new infrastructure projects globally incorporate automated monitoring solutions to ensure long-term reliability. The expansion of renewable energy installations, including offshore wind farms, has increased demand for subsea cable inspection by nearly 40%. Additionally, urbanization has led to a 35% rise in underground cable deployments, requiring advanced inspection tools for fault detection. Governments are also investing heavily in smart grid infrastructure, with over 50% of utilities upgrading legacy systems to digital monitoring platforms. These factors collectively increase the need for efficient, real-time inspection systems that enhance performance and reduce operational risks.

High initial investment and operational costs remain a major restraint for the Cable Inspection Systems Market. Advanced inspection technologies such as robotic systems and AI-based analytics require significant capital expenditure, often exceeding 20–30% higher costs compared to traditional methods. Small and medium-sized enterprises face budget constraints, limiting adoption rates. Additionally, maintenance and training costs for skilled personnel add to operational expenses. Integration with existing infrastructure systems can also be complex, increasing deployment timelines by up to 25%. These financial and technical barriers hinder widespread adoption, particularly in developing regions where cost sensitivity is higher and return on investment timelines are longer.

Digital transformation offers significant growth opportunities in the Cable Inspection Systems Market through integration of AI, IoT, and cloud-based analytics. Over 55% of enterprises are investing in predictive maintenance technologies to reduce unplanned downtime. The adoption of IoT-enabled sensors has improved real-time monitoring capabilities by 45%, enabling early fault detection. Emerging markets are witnessing a 30% increase in infrastructure digitization, creating demand for scalable inspection solutions. Additionally, the rise of smart cities and connected infrastructure is driving demand for automated cable monitoring systems. These technological advancements present opportunities for companies to develop cost-effective, scalable solutions tailored to diverse industry needs.

Data integration and lack of standardization present significant challenges for the Cable Inspection Systems Market. Different inspection systems often operate on incompatible platforms, leading to inefficiencies in data analysis and decision-making. Approximately 40% of organizations report difficulties in integrating inspection data with existing asset management systems. Additionally, absence of uniform standards across regions complicates implementation and compliance processes. Cybersecurity risks also increase as more systems become connected, requiring additional investments in data protection. These challenges limit the effectiveness of inspection systems and slow down adoption, particularly in industries requiring high levels of data accuracy and reliability.

• Growing Adoption of AI-Based Inspection Systems: Over 52% of inspection operations now utilize AI-driven analytics, improving defect detection accuracy by 47% and reducing inspection time by 35%. Utilities are increasingly deploying machine learning models to predict cable failures, enhancing maintenance efficiency across large-scale infrastructure networks.

• Expansion of Drone and Robotic Inspection Solutions: Drone-based inspections have increased by 44% globally, particularly in offshore and hard-to-access areas. Robotic crawlers are improving inspection coverage by 38%, enabling detailed analysis of underground and subsea cables while reducing human intervention risks.

• Integration of IoT and Real-Time Monitoring Systems: IoT-enabled sensors are deployed in over 48% of modern cable networks, enabling continuous monitoring and reducing unexpected failures by 32%. Real-time analytics platforms are improving response times by 28%, supporting proactive maintenance strategies.

• Increased Focus on Sustainability and ESG Compliance: Around 57% of companies are adopting eco-friendly inspection solutions to reduce environmental impact. Advanced systems help minimize energy losses by 22% and improve asset lifespan by 30%, aligning with global sustainability targets.

The Cable Inspection Systems Market is segmented based on type, application, and end-user, each playing a critical role in shaping demand patterns. Inspection technologies vary from manual systems to fully automated robotic and AI-driven solutions, with increasing preference for digital and remote inspection tools. Applications span across energy, telecommunications, oil & gas, and infrastructure sectors, where reliability and safety are critical. End-user adoption is driven by utilities, telecom providers, and industrial sectors, each requiring tailored inspection solutions. Increasing adoption of smart infrastructure and digital monitoring systems is influencing segmentation trends, with automation gaining traction across all segments.

The Cable Inspection Systems Market includes robotic inspection systems, drone-based inspection systems, and fixed monitoring systems. Robotic inspection systems lead the segment with approximately 46% share due to their ability to operate in confined and hazardous environments, improving inspection accuracy by over 40%. Drone-based systems are gaining traction rapidly and are the fastest-growing segment, expanding at a CAGR of 7.2% driven by their flexibility and ability to cover large areas quickly. Fixed monitoring systems and manual inspection tools collectively account for nearly 34% of the market, offering cost-effective solutions for basic inspection needs.

• In 2025, a national grid operator implemented robotic inspection systems across 2,000 km of transmission lines, reducing manual inspection requirements by 50% and improving fault detection rates significantly.

Energy sector dominates applications with around 48% share due to extensive use in power transmission and distribution networks. Telecommunications holds approximately 27%, driven by increasing fiber optic deployments. Oil & gas applications are growing fastest with a CAGR of 6.8%, supported by rising offshore exploration activities and need for subsea cable monitoring. Other applications, including infrastructure and transportation, contribute nearly 25% combined share. In 2025, over 41% of global enterprises reported adopting cable inspection systems for predictive maintenance in energy networks. Additionally, around 36% of telecom operators are implementing automated inspection technologies to improve network reliability.

• In 2025, a global energy organization deployed automated inspection systems across multiple facilities, improving operational efficiency by 34% and reducing outage incidents significantly.

Utilities lead the end-user segment with approximately 52% share due to high dependency on reliable power transmission infrastructure. Telecommunications companies account for around 26%, while oil & gas companies represent the fastest-growing segment with a CAGR of 6.5% driven by offshore exploration needs. Other industries, including transportation and manufacturing, contribute a combined 22% share. In 2025, over 44% of utility companies globally integrated AI-based inspection systems into their operations. Additionally, nearly 38% of industrial enterprises reported increased investment in automated inspection technologies to enhance asset performance.

• In 2025, a leading utility provider implemented AI-powered inspection systems across its network, improving fault detection efficiency by 37% and reducing maintenance costs significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America benefits from advanced infrastructure and high adoption of automated inspection technologies, with over 60% of utilities deploying AI-based systems. Europe holds approximately 27% share, driven by stringent regulatory frameworks and sustainability initiatives. Asia-Pacific accounts for nearly 24%, supported by rapid infrastructure expansion and industrialization in China and India. South America and Middle East & Africa collectively represent around 11%, with increasing investments in energy and infrastructure projects driving demand for cable inspection systems.

North America holds approximately 38% market share driven by extensive energy and telecom infrastructure. Key industries include utilities, telecommunications, and oil & gas. Regulatory mandates for grid reliability and safety compliance are accelerating adoption of automated inspection systems. Technological advancements such as AI analytics and drone inspections are improving efficiency by over 40%. A leading regional player has expanded robotic inspection deployments across multiple states, enhancing inspection coverage significantly. Consumer behavior indicates higher enterprise adoption in utilities and financial sectors, with over 60% organizations prioritizing predictive maintenance solutions.

Europe accounts for around 27% market share, with major contributions from Germany, UK, and France. Regulatory bodies emphasize sustainability and safety, driving adoption of eco-friendly inspection technologies. Over 50% of companies are integrating digital monitoring solutions to comply with environmental standards. Technological advancements include AI-based analytics and IoT integration for real-time monitoring. A regional company has introduced advanced inspection tools focusing on reducing energy losses. Consumer behavior reflects strong regulatory-driven demand for transparent and reliable inspection systems.

Asia-Pacific ranks among the fastest-growing regions with significant contributions from China, India, and Japan. The region benefits from expanding infrastructure and manufacturing activities, with over 45% increase in cable installations. Technological innovation hubs are driving adoption of automated inspection systems. A regional player has developed cost-effective inspection solutions tailored for large-scale infrastructure projects. Consumer behavior shows growth driven by industrial expansion and digital transformation initiatives across multiple sectors.

South America accounts for approximately 6% market share, led by Brazil and Argentina. Infrastructure and energy sector investments are increasing demand for inspection systems. Government policies supporting modernization of power grids are contributing to market growth. A regional company is focusing on developing affordable inspection technologies to support local industries. Consumer behavior indicates demand tied to infrastructure development and energy sector expansion.

Middle East & Africa represent around 5% market share, driven by oil & gas and construction sectors. Countries such as UAE and South Africa are investing in infrastructure modernization. Technological adoption includes advanced monitoring systems for offshore operations. A regional player is expanding its inspection capabilities to support large-scale energy projects. Consumer behavior shows increasing demand for reliable inspection systems to support industrial growth.

United States – 34% Market share: Driven by extensive infrastructure and high adoption of automated inspection technologies

China – 21% Market share: Supported by rapid industrialization and large-scale infrastructure development

The Cable Inspection Systems Market is moderately fragmented with over 35 active global and regional players competing across various segments. The top five companies collectively hold approximately 42% of the market share, indicating a mix of consolidation and competitive diversity. Key players focus on strategic initiatives such as product innovation, partnerships, and mergers to strengthen their market position. Over 60% of companies are investing in AI-based inspection technologies to enhance product capabilities. Collaboration between technology providers and utilities has increased by 30% in recent years, enabling development of integrated solutions.

Additionally, companies are expanding their geographic presence, particularly in emerging markets, to capitalize on infrastructure growth. Innovation trends include development of drone-based inspection systems and IoT-enabled monitoring platforms, improving efficiency and reducing operational costs. The competitive environment is driven by technological advancements, regulatory compliance requirements, and increasing demand for automated inspection solutions.

Nexans

General Electric

Siemens AG

ABB Ltd

FLIR Systems

Teledyne Technologies

Keysight Technologies

Megger Group

Omicron Electronics

SKF Group

Baker Hughes

National Instruments

Schneider Electric

Technological advancements are significantly transforming the Cable Inspection Systems Market, with increasing integration of artificial intelligence, robotics, and IoT-enabled solutions. AI-based inspection systems are improving defect detection accuracy by over 45%, enabling predictive maintenance and reducing unplanned downtime. Robotics technology, including crawler systems, is enhancing inspection capabilities in confined and hazardous environments, increasing operational efficiency by nearly 38%. Drone-based inspection solutions are gaining popularity, particularly in offshore and large-scale infrastructure projects, improving inspection speed by over 40%.

IoT-enabled sensors are being widely deployed to enable real-time monitoring of cable conditions, with over 48% of modern networks integrating such technologies. Cloud-based analytics platforms are facilitating centralized data management and improving decision-making processes. Digital twin technology is emerging as a key innovation, allowing simulation and monitoring of cable performance, reducing maintenance costs by approximately 30%.

Advanced imaging technologies, including thermal imaging and high-resolution cameras, are enhancing fault detection capabilities. Integration of machine learning algorithms is enabling continuous improvement in inspection accuracy. These technological developments are driving efficiency, reliability, and scalability across inspection systems, positioning the market for sustained growth.

• In March 2026, Prysmian announced the development of the world’s first negative-carbon-footprint cable, reinforcing its sustainability-driven innovation strategy. The initiative integrates advanced materials and lifecycle optimization techniques to significantly reduce environmental impact while supporting next-generation grid monitoring and inspection systems. Source: www.prysmiangroup.com

• In March 2026, Prysmian introduced enhanced broadband and data infrastructure solutions through its Sirocco Ultra cables, designed to improve efficiency in high-density networks and 5G rollouts. The solution supports improved inspection accuracy and longevity, with cable lifespan exceeding 50 years in optimized deployment environments.

• In November 2024, Nexans outlined a strategic investment plan of approximately €1.2 billion for 2025–2028 to accelerate electrification and advanced cable technologies. The company is focusing on grid modernization and AI-enabled systems to enhance inspection and monitoring capabilities across energy infrastructure networks.

• In November 2024, Nexans, along with Prysmian and other European manufacturers, secured contracts to supply and install around 5,200 km of underground cables for France’s transmission operator RTE. This large-scale infrastructure project supports grid modernization and increases demand for inspection systems to ensure operational reliability.

The Cable Inspection Systems Market Report provides a comprehensive analysis of industry dynamics, covering a wide range of technologies, applications, and end-user segments. The report evaluates key product categories including robotic inspection systems, drone-based solutions, and fixed monitoring systems, offering insights into their operational efficiencies and adoption trends. Applications analyzed include energy, telecommunications, oil & gas, and infrastructure sectors, which collectively account for over 85% of market demand.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional variations in adoption patterns and infrastructure investments. The study also examines technological advancements such as AI integration, IoT-enabled monitoring, and digital twin technologies, which are transforming inspection processes.

Additionally, the report explores regulatory frameworks, ESG considerations, and industry standards influencing market growth. Emerging segments such as smart grid inspection and offshore cable monitoring are also analyzed. The scope includes competitive landscape assessment, profiling key players, and evaluating strategic initiatives shaping the market. This comprehensive coverage enables stakeholders to make informed decisions regarding investments, technology adoption, and market entry strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 100.0 Million |

| Market Revenue (2033) | USD 153.5 Million |

| CAGR (2026–2033) | 5.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Prysmian Group; Nexans; General Electric; Siemens AG; ABB Ltd; FLIR Systems; Teledyne Technologies; Keysight Technologies; Megger Group; Omicron Electronics; SKF Group; Baker Hughes; National Instruments; Schneider Electric |

| Customization & Pricing | Available on Request (10% Customization Free) |